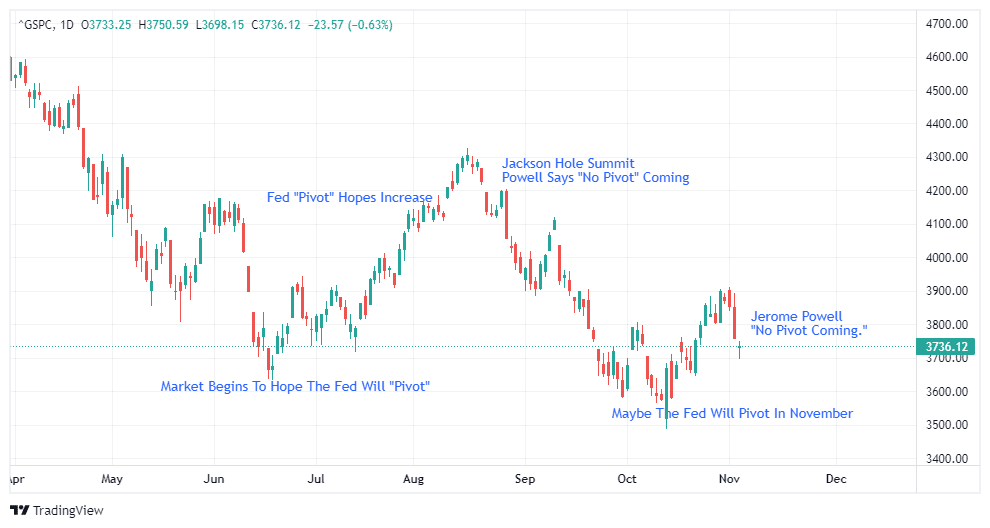

As we wrote on Friday, investors were disappointed again last week after Jerome Powell failed to take a different perspective on the path of monetary policy. Bets that Powell will say something even slightly dovish this year are misplaced, given the implications for financial conditions based on what we’ve seen already. Instead, Powell will likely let other FOMC members float those ideas to the public between meetings.

What To Watch Today

Economy

- 3:00 p.m. ET: Consumer Credit, September ($30.000 billion, $32.241 billion)

Earnings

Market Trading Update

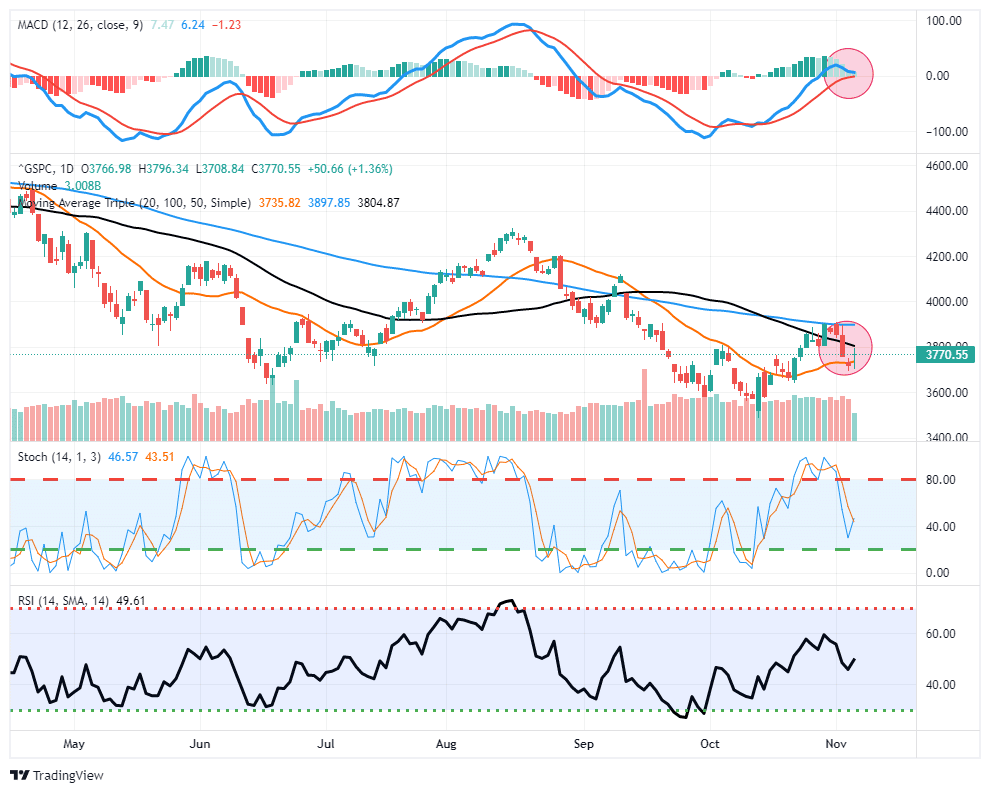

The October employment report on Friday was also strong, printing a 261,000 job increase, but the unemployment rate rose to 3.7%. Initially, stocks sold off but then rallied on expectations that future reports would begin to weaken. Notably, the market defended the important 20-dma moving average, keeping the bull market rally from the September lows alive. However, the MACD “buy signal,” which signaled the start of the most recent rally, is dangerously close to flipping.

The Week Ahead

Fed speakers will be out in droves this week following the end of the FOMC blackout period. Any remotely dovish comments from Powell this year led to loosening financial conditions- which directly works against the Fed’s goal. As mentioned above, the Fed may be tweaking its communication strategy by having Powell convey a strictly hawkish tone and allowing other members to walk it back slightly. Thus, we will be watching for comments supporting slowing the pace of rate hikes this week.

This week will be light on economic data. The BLS will release October’s CPI report Thursday morning— expectations for broad and core inflation are 0.7% and 0.5% MoM, respectively. While economists forecast broad CPI growth to accelerate MoM, they expect the pace of core inflation to slow from September. We’ll cap off the week with Friday’s preliminary consumer sentiment data for November. Expect consumer sentiment to take a breather after four consecutive increases from the low in June.

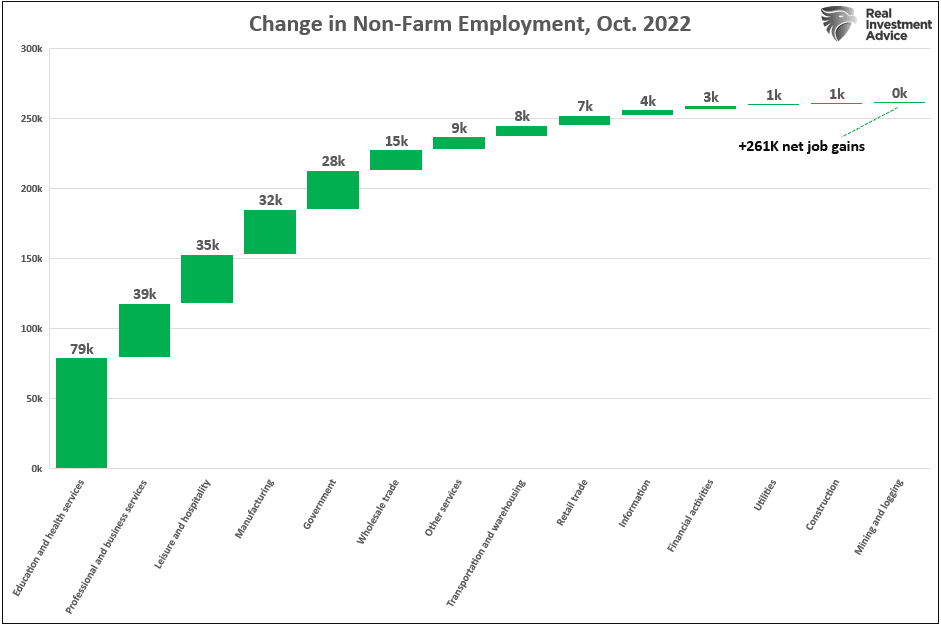

October Delivers Another Strong Jobs Report

Non-farm payrolls increased by 261,000 in October (200,000 expected), adding another month to the recent track record. Stocks ended 1.4% higher in a volatile session Friday, as the USD was crushed (-1.9%) and investors tempered expectations for future job growth. The unemployment rate ticked up to 3.7%, while the labor force participation rate fell to 62.2%.

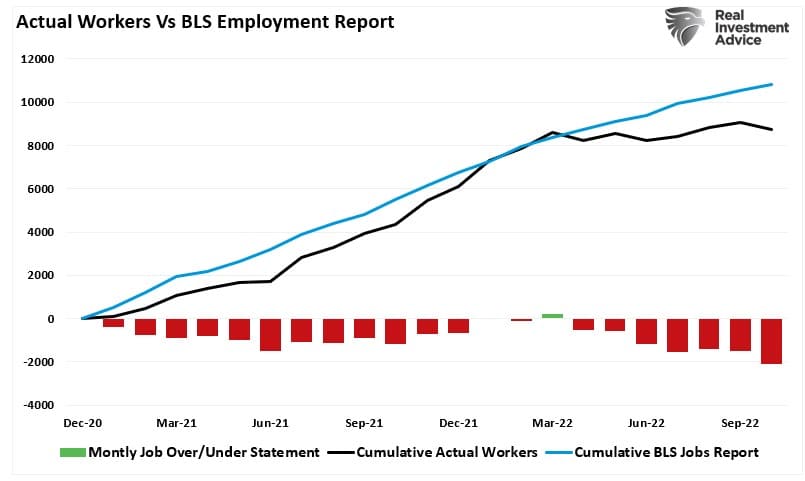

As noted in this weekend’s Newsletter, the Household Survey offers a different perspective.

“While the BLS employment report suggested employment was strong, the Household Survey, which is where the BLS report comes from, showed a rather significant loss of 328,000 jobs. Also, wage growth continues to slow, and the labor force participation rate dropped. That data suggests the Fed’s rate hikes are beginning to have an effect.”

Employment Not As Strong As It Appears

While the BLS employment report suggested employment was strong, the Household Survey, which is where the BLS report comes from, showed a rather significant loss of 328,000 jobs. Also, wage growth continues to slow, and the labor force participation rate dropped. That data suggests the Fed’s rate hikes are beginning to have an effect. As shown, while the BLS report continues to report strong monthly job growth, the Household Survey (which the BLS draws its report from) suggests a far weaker picture showing NO job gains since March of 2022.

We suspect that after the Midterm elections are behind us, we may see a “catch down” in the data. Such is especially the case with the rising number of layoff announcements almost daily.

While the Fed continues looking at inflation and employment for clues on when to stop hiking rates, they may have already gone too far.

A Different Perspective

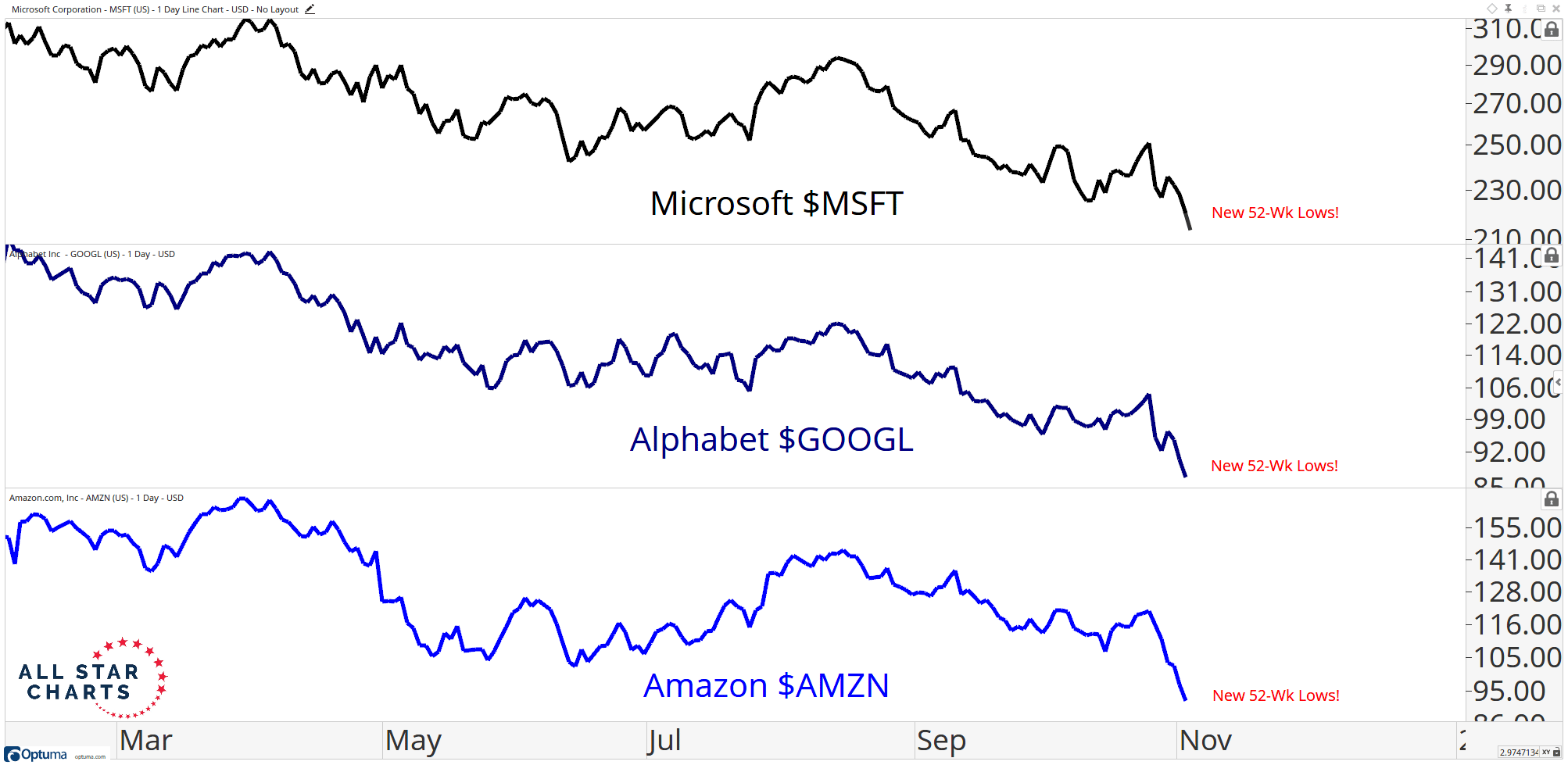

The rise of passive investing, along with other factors, led to a handful of stocks comprising a large portion of the market-cap weighted S&P 500 index. The FAANG stocks (including MSFT), which have held up relatively well YTD, now account for about 20% of the index. With the S&P buoyed by mega-caps holding on to lofty valuations throughout widespread carnage, a narrative developing in many circles held that passive investors would get killed when the “big boys” caved.

The tide is beginning to turn as the market generals took a beating on 3rd quarter earnings announcements. However, the index has held up surprisingly well so far due to solid performance by the other 80% of constituents. Now, a different perspective is coming to light. Is it a bullish sign that the overall index is still holding up as several generals make 52-week lows?

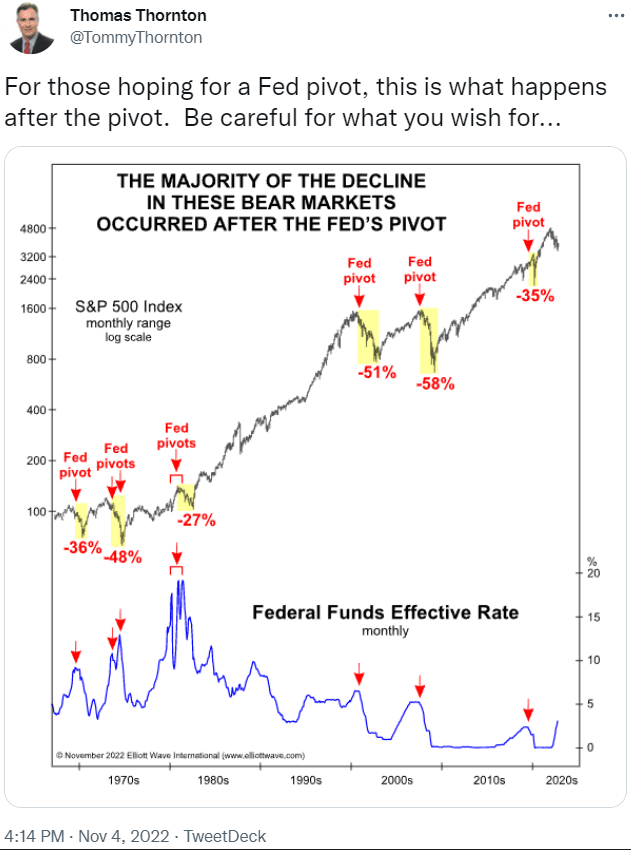

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read