Cyber Monday stock gains erased a good chunk of Black Friday’s losses. Fear of another high-powered Covid variant was tempered over the weekend, and investors, like shoppers, bought into Cyber Monday deals. Oil recovered some of its Friday meltdown rising 2.5%.

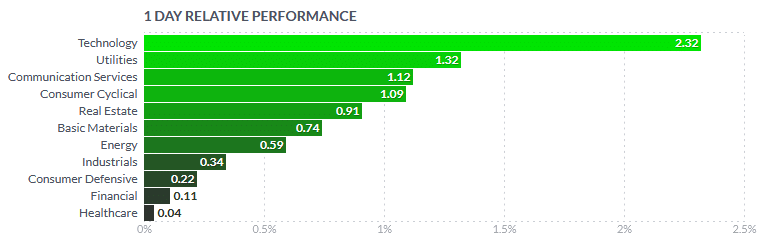

Despite the renewed optimism, there remains a little trepidation in the market. We can best see it in the travel and lodging sectors. For example, Bookings.com (BKNG) only picked up 1.25% of its 7% decline from Friday. Many of the largest resorts and casinos were red on the day. Technology led the way higher, as shown below, while healthcare and financials barely eked out gains.

What To Watch Today

Economy

- 9:00 a.m. ET: FHFA House Price Index, month-over-month, September (1.2% expected, 1.0% in August)

- 9:00 a.m. ET: S&P CoreLogic Case-Shiller 20-City Composite Index, month-over-month, September (1.20% expected, 1.17% in August)

- 9:00 a.m. ET: S&P CoreLogic Case-Shiller 20-City Composite Index, September (19.30% expected, 19.66% during prior month)

- 9:45 a.m. ET: MNI Chicago PMI, November (67.0 expected, 68.4 in October)

- 10:00 a.m. ET: Conference Board Consumer Confidence Index, November (110.0 expected, 113.8 in October)

Earnings

- 4:05 p.m. ET: Salesforce.com (CRM) to report adjusted earnings of 92 cents on revenue of $6.80 billion

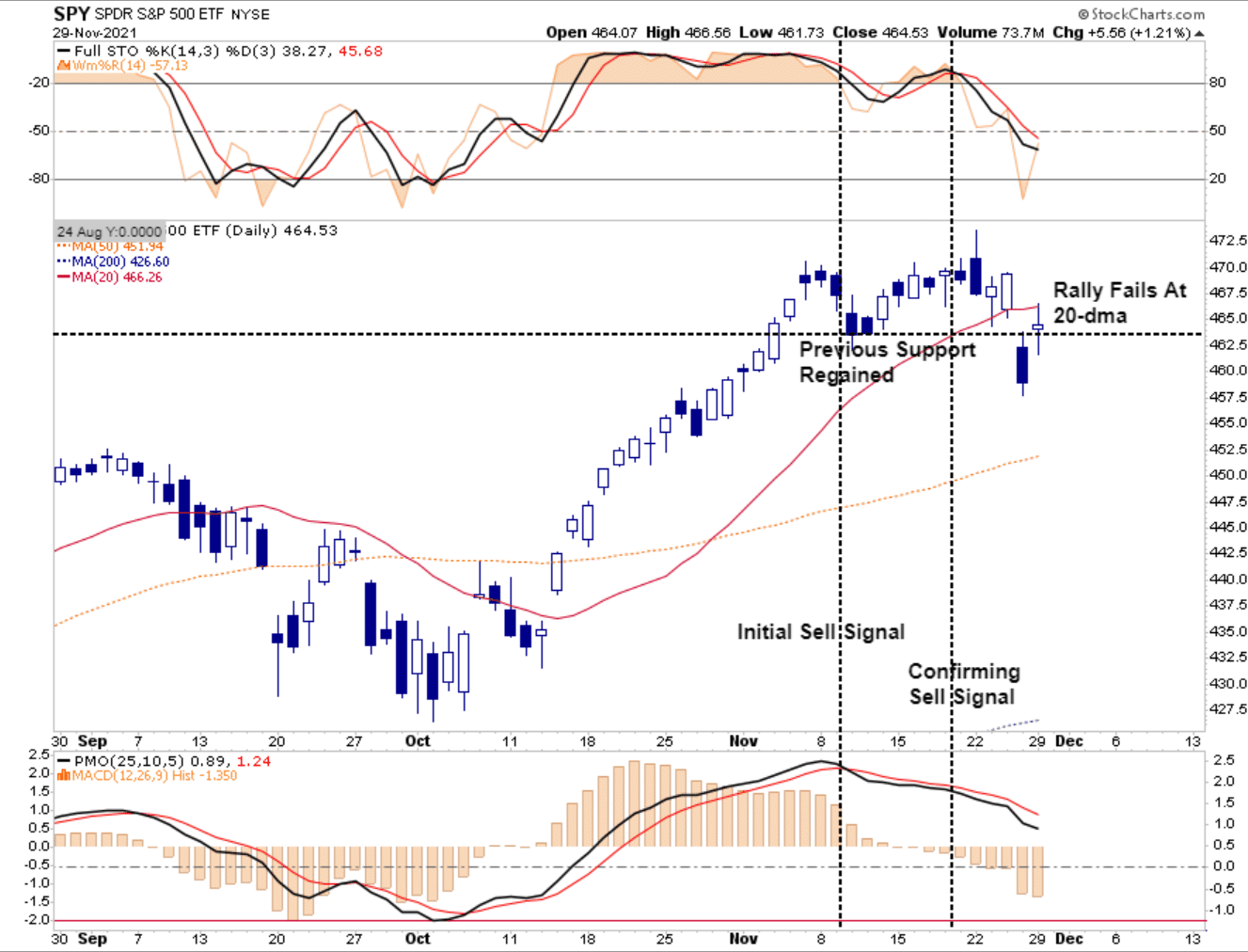

Technical Backdrop Still Questionable

Yesterday’s “Cyber Monday” rally was not surprising given the depth of the decline on “Black Friday.” However, while the rally was strong enough to put the market back above broken support, it failed resistance at the 20-dma. Also, with major “sell signals” still intact, we could see some volatility in the days ahead.

This morning fears are resurfacing over the omicron variant and futures are sliding lower once again. But that is just the excuse to explain the sell-off we have been discussing for the last two weeks.

However, with the market getting decently oversold on a short-term basis, such should set investors up for the seasonal “year-end” rally. Therefore, it is a good idea to start “making your list, and checking it twice,” and using opportunistic entry points to add equity exposure heading into 2022.

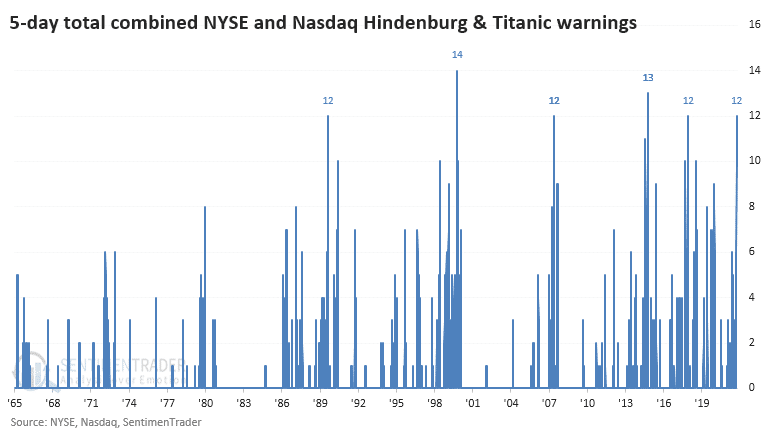

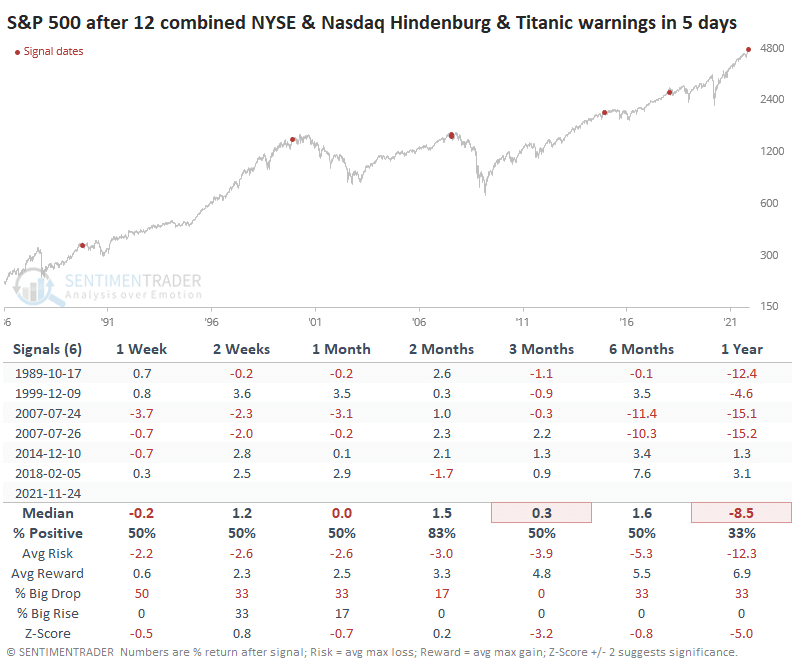

A Historic Cluster Of Warnings

“Single warning signs, like we saw in March, are less of a worry. It’s a more significant issue when we see multiple days of warnings and on more than a single exchange.

This is a problem now because they’ve been firing consistently lately, ahead of Friday’s carnage. In just 5 days, a combined 12 warning signs have triggered between the NYSE Hindenburg Omen, Nasdaq Hindenburg Omen, NYSE Titanic Syndrome, and Nasdaq Titanic Syndrome.” – Sentiment Trader

“It’s been rare to see such a big cluster of warnings across both exchanges over the past 25 years. The handful of times these clusters popped up, the S&P 500 had a tough time holding any upside momentum.”

Powell Pivots Gets Excuse To Slow Taper

We have wondered how long it would be before Jerome Powell came up with some excuse to delay tapering of the balance sheet and hiking the Fed funds rate. We now know the answer according to Zerohedge:

But for one market participant in particular, it’s a great excuse (especially after his re-nomination) as Fed Chair Powell’s prepared remarks ahead of The Coronavirus and CARES Act hearing before the Committee on Banking, Housing, and Urban Affairs, offered some insight into his next actions (after a token shift to more hawkish positions by some Fed speakers).

Here is the key paragraph:

“The recent rise in COVID-19 cases and the emergence of the Omicron variant pose downside risks to employment and economic activity and increased uncertainty for inflation.

Greater concerns about the virus could reduce people’s willingness to work in person, which would slow progress in the labor market and intensify supply-chain disruptions.“

That uncertainty can mean only one thing when it comes from The Fed… backing away from the taper’s current trajectory (and any guesses at when takeoff may occur).

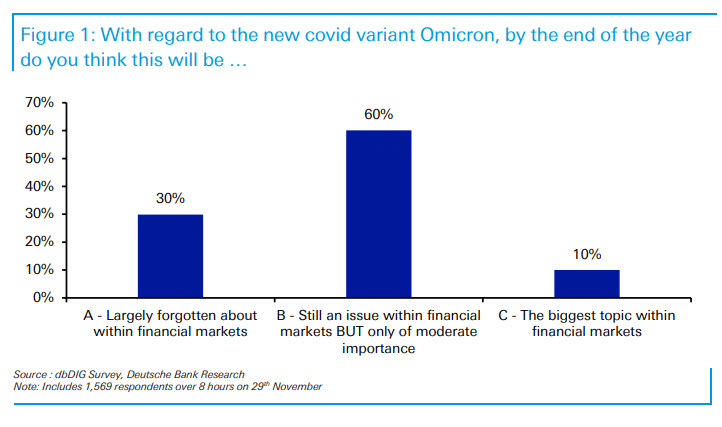

Of course, this is truly amusing because only 10% of Wall Street respondents to a flash DB poll thing Omicron will be a big issue at year end…

Twitter Rollercoaster

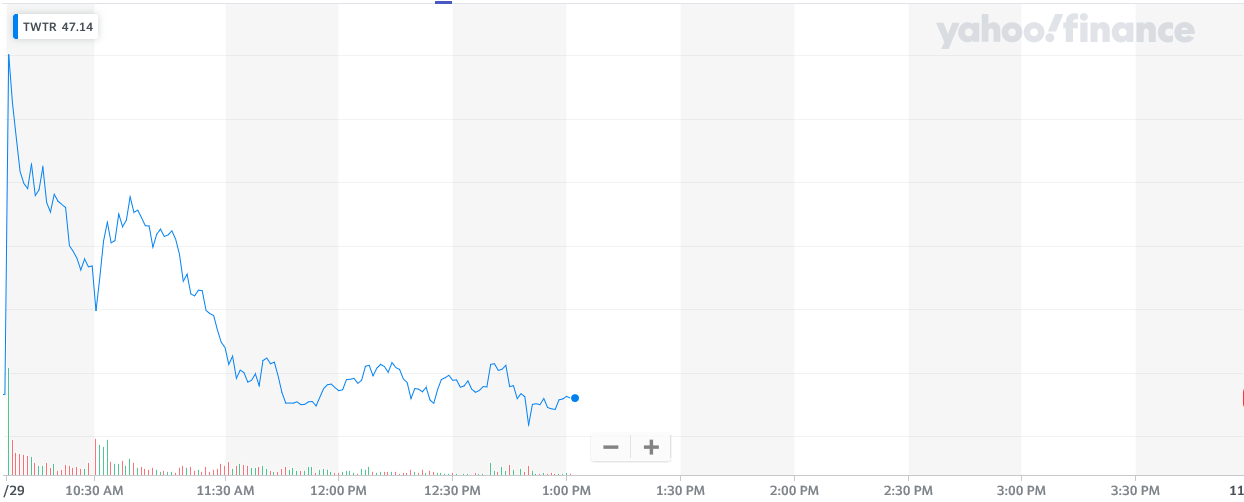

On “Cyber Monday,” Twitter’s stock jumped almost 10% at the market open on news that CEO Jack Dorsey will be stepping down. The gains were short-lived, as shown in the graph below. Twitter has become a large social media brand, but its stock price is flat since IPO’ing in 2013. After the initial rush of enthusiasm, it appears investors are concerned that promoting a long-time Twitter veteran (current CTO – Parag Agrawal) to replace Dorsey will not result in the types of changes investors are asking for.

Omicron Variant Shakes Wall Street

What’s Wrong with Foreign Stocks?

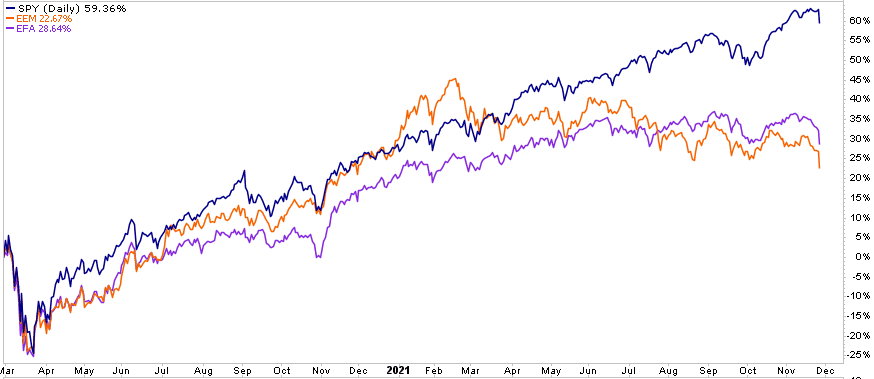

The graph below compares two widely followed foreign stock ETFs and the S&P 500, from the beginning of the Covid outbreak through today. EEM holds emerging market stocks, and EFA developed market stocks. As shown, all three ETFs performed similarly during the decline in early 2020 and the recovery afterward. However, starting in the spring of 2021, the foreign market ETFs peaked while the S&P 500 continued to new highs. Over the last nine months emerging markets (EEM)s have given up about 25% of their post-Covid gains, while developed markets (EFA) have essentially flatlined. The following factors help account for some of the U.S. equity outperformance:

- Since June 2021, the USD index is up about 8%.

- The economic recovery in the U.S. has been stronger than in most nations.

- The Fed is slightly more hawkish than other central banks.

- China’s economic activity has slowed significantly, weighing heavily on many emerging markets.

The Week Ahead

The week’s significant events will be the ADP employment report on Wednesday and the BLS report on Friday. Currently, the forecast is for a gain of 550k jobs in the November BLS jobs report. Investors are likely to focus on the labor participation rate as Fed Chairman Powell claims the lower rate is a sign of labor weakness. The current estimate is for the participation rate to uptick 0.1% to 61.7%.

Investors will also watch the ISM manufacturing and services surveys on Wednesday and Friday, respectively. Current indications are that both numbers will remain at their current levels. We will follow the price gauges in both surveys closely.

The next Fed meeting will be in two weeks on the 15th of December. Assuming the new covid variant does not become problematic for global economic activity, we might see some Fed members encouraging a faster tapering pace in speeches and comments this week. Voting Fed members go into their self-imposed media blackout period next week, so this week may be their last chance to speak up publically before the meeting.

Investors will be looking for retail results from Black Friday and Cyber Monday to help assess holiday sales.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

Also Read