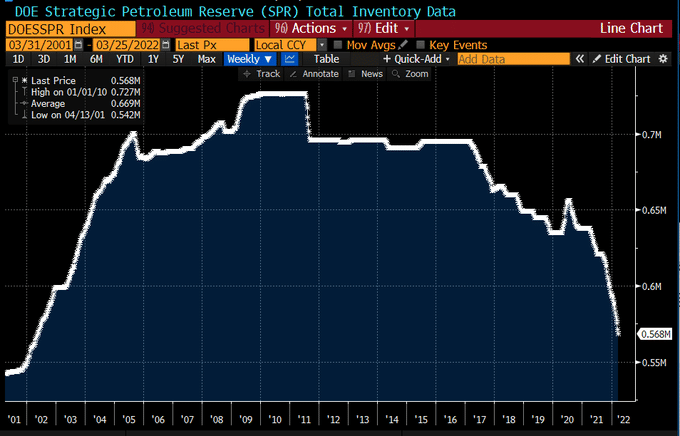

Crude oil prices tumbled Thursday as President Biden announced the DOE would release 1 million barrels of crude oil per day for 180 days, totaling 180 million barrels. The intention is to lower gas prices. While releasing more crude oil from strategic reserves may temper inflation, a few factors are worth considering. First, the International Energy Agency (IEA) recently warned that further sanctions and boycotts could reduce Russian supply by up to 3 million barrels per day.

Second, the proposed release represents about a third of the current strategic reserves. As we show below, reserves are already well below the reserve’s capacity. At some point, crude oil will be purchased to refill the reserves and in doing so, will push prices higher. Lastly, OPEC is not cooperating by increasing production. We are doubtful that Biden’s plan on its own will have a meaningful effect on oil prices.

What To Watch Today

Economy

- 8:30 a.m. ET: Change in Non-farm Payrolls, March (490,000 expected, 678,000 during prior month)

- 8:30 a.m. ET: Unemployment Rate, March (3.7% expected, 3.8% during prior month)

- 8:30 a.m. ET: Average Hourly Earnings, month-over-month, March (0.4% expected, 0.0% during prior month)

- 8:30 a.m. ET: Average Hourly Earnings, year-over-year, March (5.5% expected, 5.1% prior month)

- 8:30 a.m. ET: Labor Force Participation Rate, March (62.4% expected, 62.3% during prior month)

- 9:45 a.m. ET: S&P Global Manufacturing PMI, March final (58.5 expected, 58.5 during prior month)

- 10:00 a.m. ET: Construction Spending, month-over-month, February (1.0% expected, 1.3% during prior month)

- 10:00 a.m. ET: ISM Manufacturing, March (59.0 expected, 58.6 during prior month)

- 10:00 a.m. ET: ISM Prices Paid, March (80 expected, 75.6 prior month)

- 10:00 a.m. ET: ISM New Orders, March (61.7 during prior month)

- 10:00 a.m. ET: ISM Employment, March (52.9 during prior month)

Earnings

- No notable reports are scheduled for release

Today’s Blog Post

Market Trading Update – Stocks Retreat

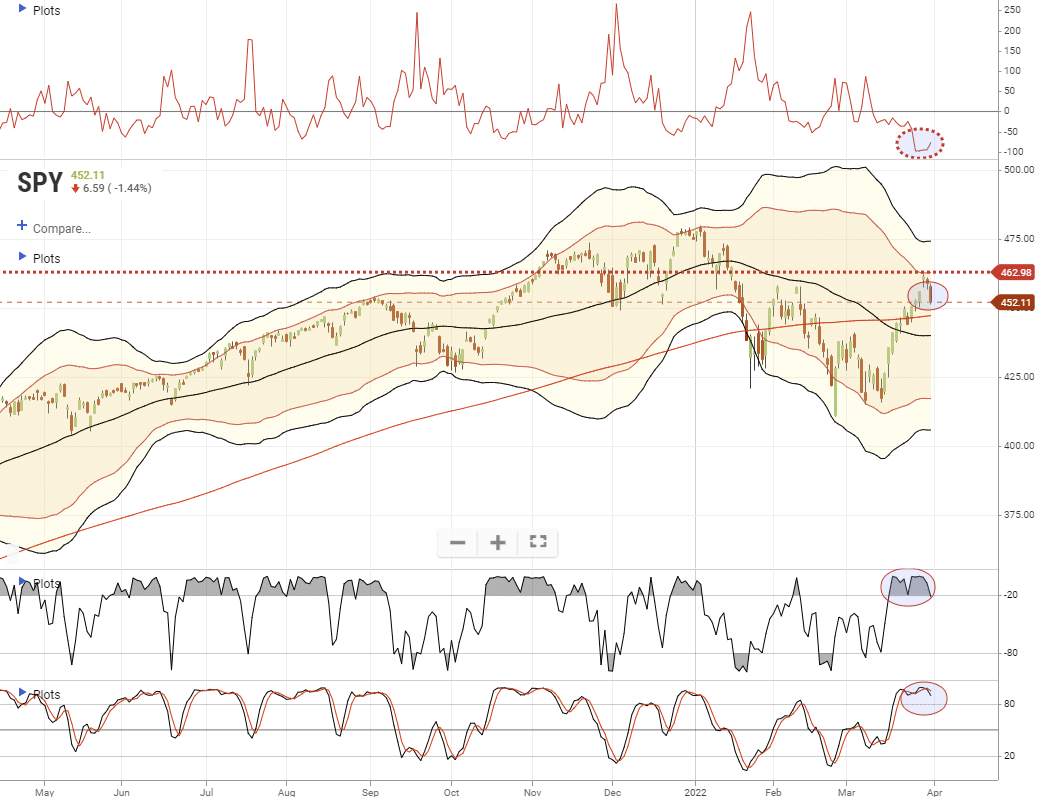

Over the last couple of days, we noted that the market had gotten to more extreme overbought levels after the two-week surge from oversold conditions. Yesterday the market retreated late in the afternoon as concerns over Russia, crude oil prices, and inflationary pressures remain. With quarter-end window dressing over, April will have to deal with the beginning of the Q1-earnings season start.

The pullback will start to test critical support at the 200-dma. That level needs to hold if the “bull market” is indeed back. With a short-term sell signal in place, and extremely overbought, there is downside risk present. Caution remains advised.

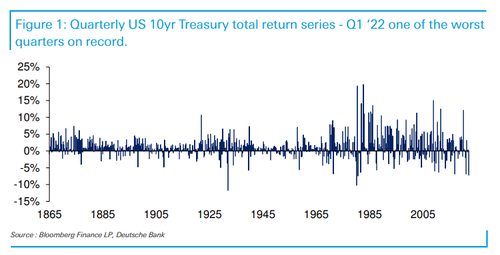

Q1 Was Unreal

- Global Bonds – worst drawdown ever

- US Bonds – 3rd worst Q1 since the Civil War

- US Yield Curve – greatest Q1 flattening ever

- Commodities – the best start to a year ever

- Crude Oil Prices – the best start to a year since 1999

- Regular Gasoline (at-the-pump) – fastest rise ever to record highs

- US Stocks – 3rd biggest short-squeeze rebound in March since Lehman after worst start to a year for stocks since 2009 (2nd worst in over 30 years)

- Ruble – stronger against the dollar in March after ugly Jan/Feb

“But stocks were saved by a massive short-squeeze at the end of the month. For some context as to just how much of a bounce this was., Nasdaq rallied a stunning 17% off the mid-March lows (in 10 days) and S&P up almost 12% in the same period.” – Zerohedge

“Domestically, according to BofA, Q1 is the worst quarter for their 10yr UST series since the early 1980s.“

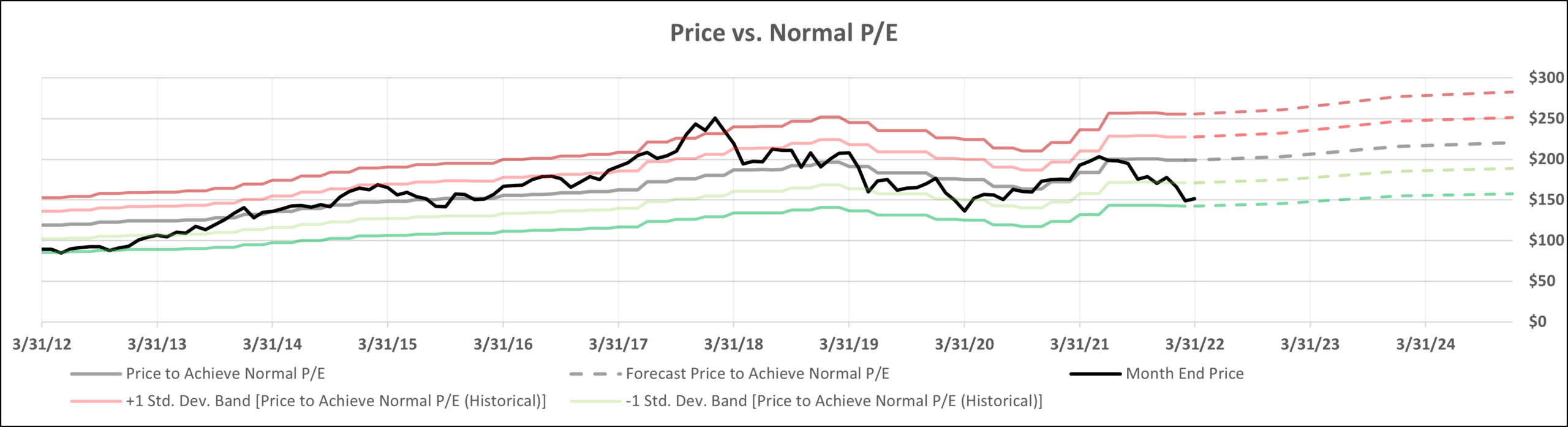

Value in MMM

Despite the recent market sell-off, many stocks, including value stocks remain expensive. P&G (PG), for example, is a quality company with steady earnings. It is often a top holding of value funds. Despite the classification, its P/E is 27, about 35% above its 20-year average and S&P 500 P/E. 3M (MMM) is also considered a value company, but unlike PG, its stock price has floundered. Over the last five years, PG is up nearly 100% while MMM is down about 10%. We share this brief analysis to remind you that value companies are not necessarily value stocks. This doesn’t matter in the current market but at some point, it will.

We use an internal model to help us assess well-established, profitable companies. Currently, we estimate MMM is trading at a 20-40% discount to fair value. Zacks has MMM at a 35% discount to its model’s fair value. In context, PG is overpriced by 27% in our model and 36%, according to Zacks. The graph below, from our model, shows MMM is nearly two standard deviations cheap to its normal P/E ratio. A price of approximately $200 per share would put MMM at fair value. *Disclaimer: we own PG and MMM in RIA Advisor models.

Mortgage Rates Matter

A reader asked us: “wouldn’t higher mortgage rates and a cooling down in house prices be beneficial longer-term?” Our answer is yes. But, it would entail short-term pain for homeowners and the economy. Real estate represents about 50% of global wealth. As our perceptions of wealth change, our spending habits change. Personal consumption drives two-thirds of economic growth; therefore, consumer sentiment matters. Therefore home prices matter.

Ben Bernanke was clear about the relationship between asset prices and economic activity regarding the stock market. In 2010 he said:

“And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.”

House prices and rising equity in houses have a similar economic effect as stock prices. While we think a normalization in home prices would be healthy we know the Fed keeps a close eye on consumer sentiment and spending. As we have seen over and over again, it will not take much consumer weakness before the Fed starts pushing mortgage rates lower to support the economy via stocks and house prices.

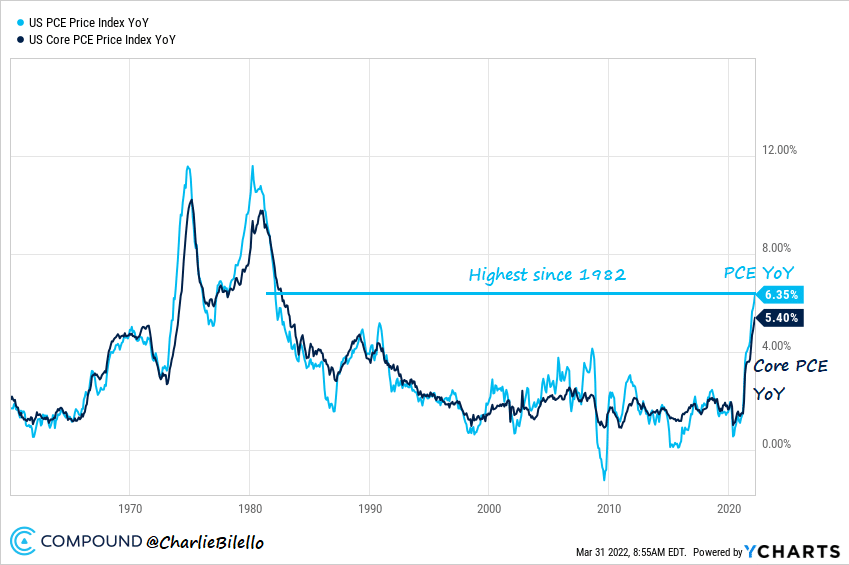

Inflation Remains Persistent

The good news in yesterday’s PCE inflation data was that February’s price data did not again surprise analysts. The bad news, as shown below, PCE is now at levels last seen over 40 years ago. PCE prices rose 0.6% monthly, the highest monthly increase in 14 years. On a year-over-year basis, prices are rising at a 6.35% clip. The data is for February, so it doesn’t incorporate the recent surge in gas prices. Personal Income grew by 0.5%, or 6% annualized. While robust, wages continue to lag inflation. Real (inflation-adjusted) spending fell 0.4% in February.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

Also Read