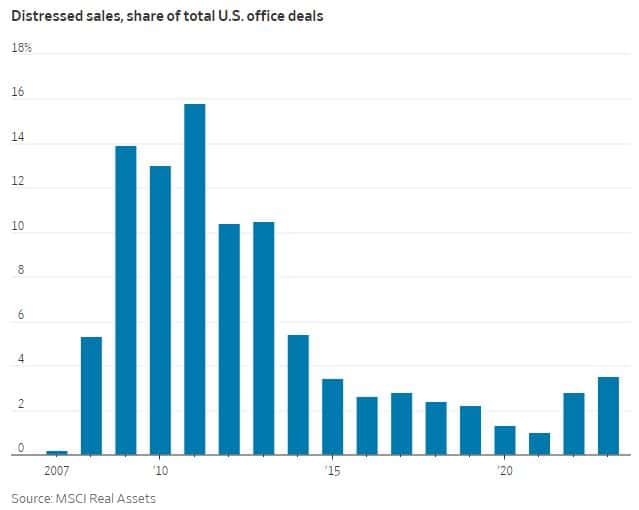

The vacancy rate of commercial real estate is higher today than at any point in the 2008 global financial crisis, per the Wall Street Journal. Yet, the CRE industry isn’t experiencing the pain one might expect to see with such high vacancy rates. CRE deals involving distressed sellers are still surprisingly low, at just 3.5% of all deals formed in the US in 2023. Per MSCI Real Assets, that number is closer to 2.7% with the most recent data.

Many CRE investors owe a few favors to lenders with good graces that have delayed the pain accompanying distressed sales. Rather than forcing fire sales, some lenders are working out deals to extend loans in hopes of a market recovery. In other cases, distressed debt investors are coming forward to lend funds, albeit with less advantageous terms. Still, CBRE predicts that CRE landlords face a refinancing gap of $72.7 billion through the end of 2025. While Jerome Powell has acknowledged the CRE pain faced by regional banks and the risk of contagion to GSIBs, he’s confident that the situation is manageable.

Lenders are also eager to kick the can down the road. They don’t want to force borrowers to sell buildings into a weak commercial real-estate market, which would lead to punishing losses.

This might explain why debt maturities aren’t triggering the kind of distress that some property watchers expected. Of the $35.8 billion of office loans that came due in the commercial mortgage-backed securities market last year, only a quarter were paid off in full, according to data from real-estate analytics firm CRED iQ. Other loans were extended or sent to a special servicer—a third party that tries to find the best outcome for the debt, which may include modified payment terms or foreclosure.

What To Watch Today

Earnings

- No notable earnings releases

Economy

Market Trading Update

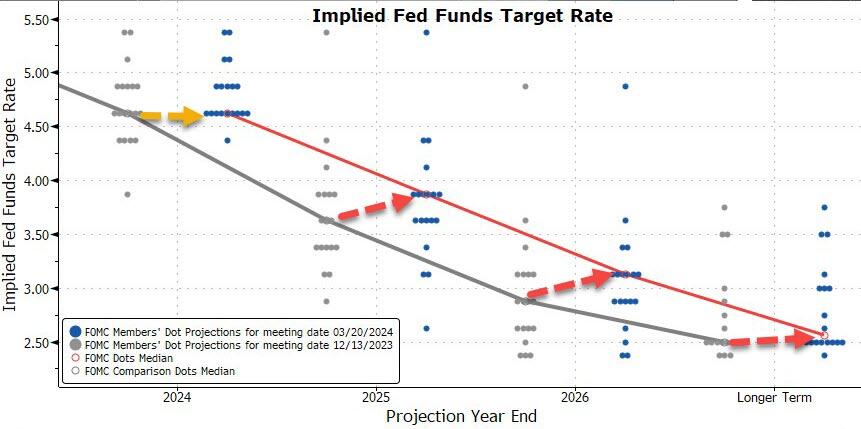

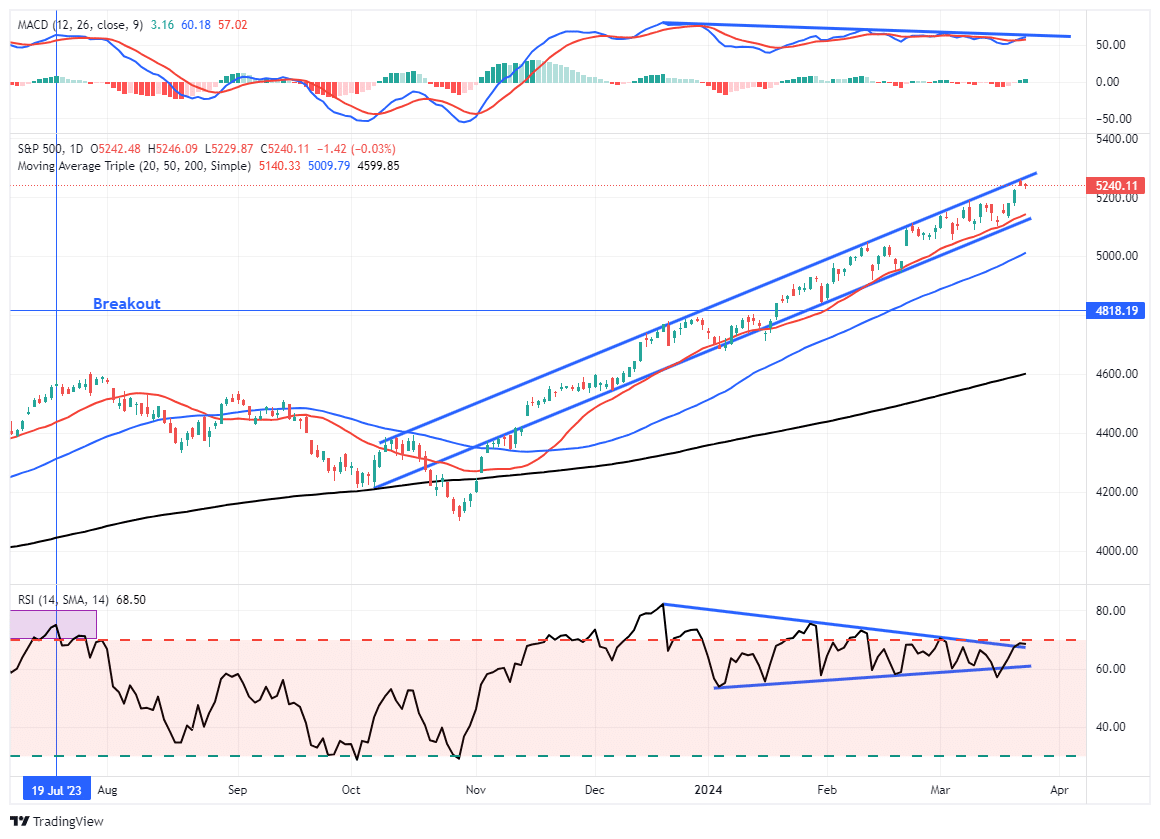

Last week, we suggested we could see a further correction given some of the weaknesses that had been accruing. Such was the case until Wednesday’s FOMC meeting announcement. While the meeting was largely as expected, with no real change to outlook, the outcome was seen as largely “dovish” as Powell reaffirmed the Fed was still on track to cut rates three times this year.

“While The Fed kept its median dot at 3 cuts for 2024, beyond that the dots signal considerably less aggressive Fed rate-cutting. We also note that while the median 2024 dot remained the same, 8 Fed voters were for 50bps or less in Dec, now it’s 9. The Fed now expects one less rate-cut in 2025 and 2026… and the so-called ‘neutral’ rate has also been increased.“ – Zerohedge

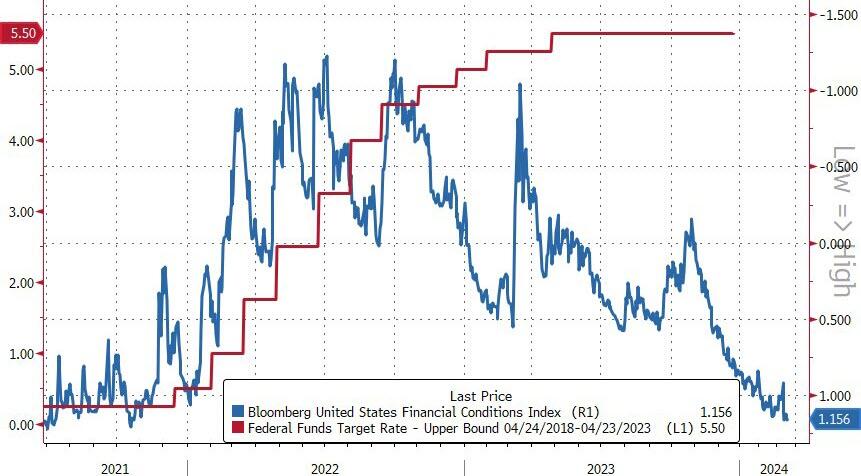

With financial conditions now as loose as they were before the Fed started hiking rates, the markets remain unmoved by slightly more hawkish rhetoric.

With that announcement, the market surged to an all-time high, reversing the recent momentum weakness. The market remains in a nearly perfect trend that only Bernie Madoff could have designed. As we have repeated, to the point of “ad nauseam,” over the last several weeks, the market remains confined to a very defined channel. The 20-DMA continues as key support where computer algorithms continue to “buy dips,” and sellers resurface at the channel’s top.

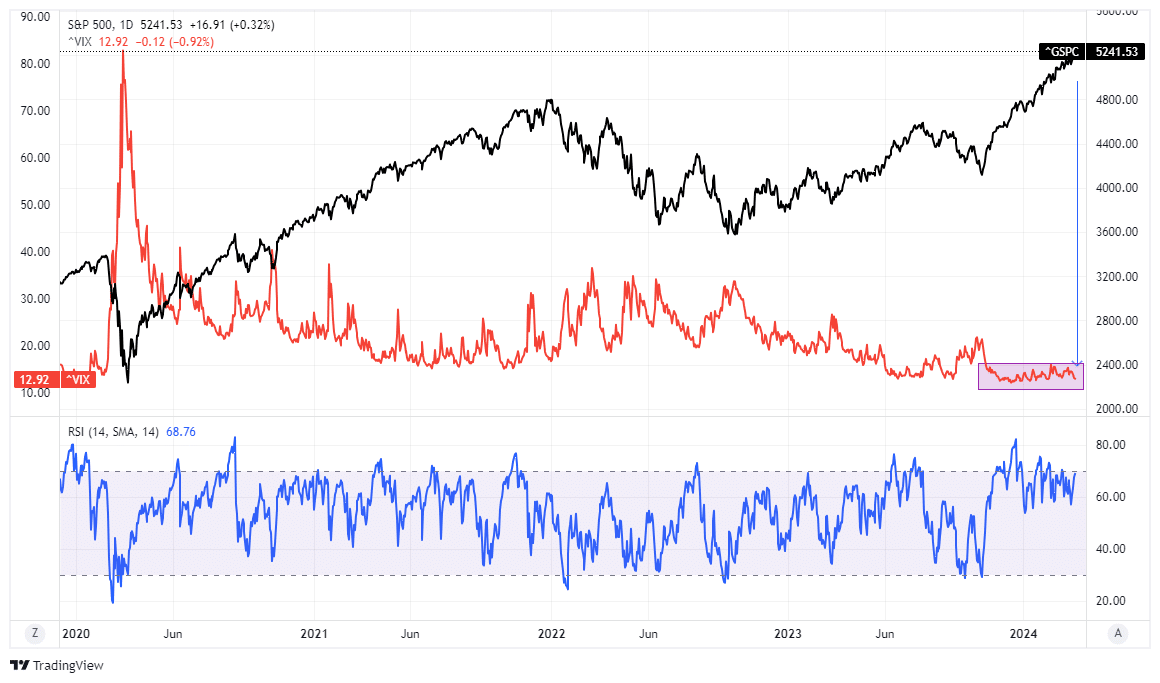

For now, this mind-numbingly narrow channel, with extremely low volatility and high complacency, remains. What will change that dynamic? I have no idea. As shown, volatility continues to plumb the “nether regions” as investor optimism surges.

However, as is always the case, at some point, this will reverse itself. What triggers it is unknown, but a good warning sign will be a violation of the 20-DMA. As noted, we suspect such a violation will trip the algorithms into “sell” mode and increase downside price pressures. The problem for investors is that this bullish trend has already lasted much longer than expected and could continue. Therefore, we must maintain our current positioning and remain vigilant for a break of the trend channel to take more aggressive risk reduction actions.

As they say at amusement parks, “Make sure your seat belts are fastened securely and enjoy the ride.”

The Week Ahead

Following last week’s FOMC meeting, the focus will now be on the PCE price index this Friday. Inflation is falling but remains above the Federal Reserve’s target. After a sticky February CPI number, PCE will be even more important as it’s the Fed’s preferred measure of inflation. The consensus expectation is for the PCE price index to rise to 0.4% MoM in February, up from 0.3% MoM in January. Also to be released on Friday is the Personal Income and Expenditures data for February. Personal income is slated to grow 0.4% MoM, retreating from 1% growth in January. Meanwhile, personal spending is expected to rise 0.4% MoM following a 0.2% increase in January. Thus, the expectation is zero real growth in personal income and expenditures in February.

Other notable economic data this week include February Durable Goods Orders on Tuesday and the final estimate of fourth-quarter GDP growth on Thursday. Durable Goods Orders have been volatile over the past few years. The consensus anticipates 1% growth in February after falling 6.1% in January. Excluding Transportation, the consensus is for 0.4% growth in February following a decrease of 0.3% in January.

Market Forces Contribute to State Migration Losing Sparkle

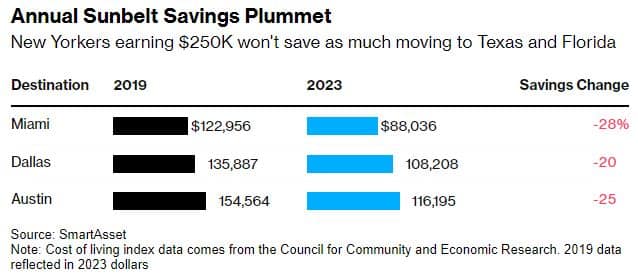

Higher home prices and inflation are eating into the savings of those looking to leave states like New York for Texas. The pandemic sparked a plunge into remote work culture, which presented those in high-cost-of-living states a sort of arbitrage opportunity. Per Bloomberg, those making $250k in New York in 2019 could have saved as much as $135k by moving from New York to Dallas.

Now, the benefits are waning as market forces take effect. Like any arbitrage opportunity, the net benefit will shrink until exploitation no longer makes sense, given the costs. As shown below, possible savings have fallen by nearly a quarter since 2019 as the markets adjust to supply/demand dynamics.

New Yorkers who left for sunny Miami in 2023 saved almost 30% less than they would have if they moved in 2019. Meanwhile, those who left Manhattan for Dallas or Austin saved about 20% to 25% less if they moved last year compared to 2019.

And while Manhattan is still the most expensive place to live in the US, higher inflation rates in Miami, Dallas, and Austin means costs in those popular destinations are catching up to New York, said Jaclyn DeJohn, the managing editor of economic analysis at SmartAsset.

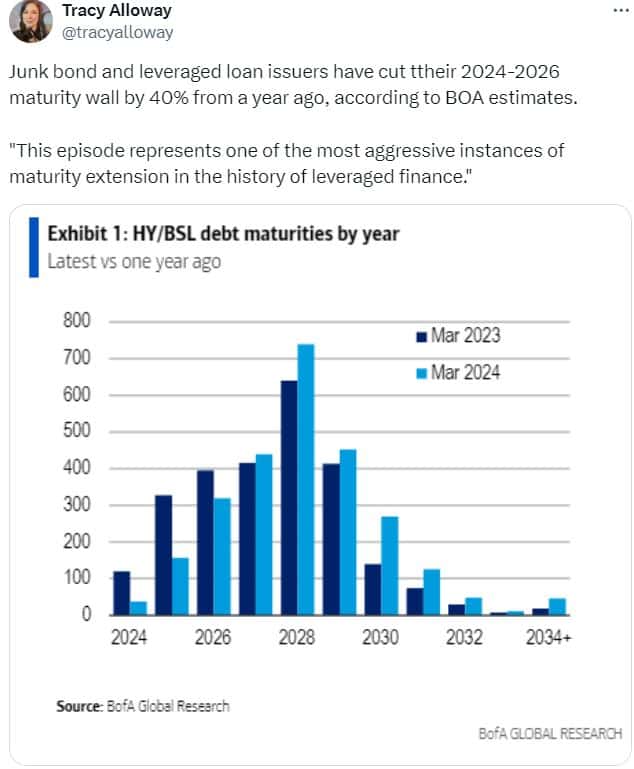

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read