Covid-19 has further deteriorated the status of women’s finances. Here are four money ideas for women to consider now.

In 1920 the Nineteenth Amendment guaranteed women the right to vote, Over the next hundred years the investment process has been democratized. It has never been more important to understand your financial picture.

Sharon Snow, Metropolitan Capital/RIA Advisors.

Nicole Bateman and Martha Ross penned an essay for Brookings.edu titled “Why has COVID-19 been especially harmful for working women?” In their eye-opening work, the authors outline the economic challenges for women before and during the pandemic.

Nearly half of working women (pre-pandemic), 46% – 28 million, worked in low-wage jobs with median earnings of less than eleven dollars an hour. A significant number support themselves and families with low-paying positions. Per the analysis, 50% are single parents, 63% are in prime working years (age 25-54), and 57% work full time year-round, indicating this isn’t a side gig.

A panel survey of 2,557 working parents between last Mother’s Day and Father’s Day revealed that one out of every four women who lost jobs during the pandemic did so due to a lack of childcare.

More significant job loss among women.

A later study by Pew’s Stateline posted in September 2020 discovered that mothers of children 12 years old and younger lost nearly 2.2 million jobs between February and August, a 12% drop. Fathers of small children saw a 4% drop of about 870,000 jobs.

Overall, the Labor Force Participation Rate for women has increased for most cohorts. The labor force for women 75 and older has skyrocketed – rising over 107% since 2000. The LFPR for men is up half as much.

Women continue to experience longevity risk (women live longer than men) and a lifetime of lower wages. As the customary stay-at-home parents, women earn lower Social Security retirement benefits and are more dependent on spousal and survivor benefits. Due to Covid-related economic conditions, these benefits are even more critical.

Covid-19 has created more worry among women.

The sixth annual Nationwide Advisor Authority study polled 2,500 women and men, including 1,768 financial professionals and 817 investors. Harris Poll conducted the online survey from May through June 2020.

Results showcased how Covid-19 further exacerbated women’s ongoing retirement angst. Women have less room for error in saving and investing. They are more concerned with risk mitigation than men. So, it wasn’t surprising to discover that 72% of females polled said the pandemic impacted how long they will be able to live off current savings.

Also, women are more receptive to guaranteed income solutions. Over 59% of women stated they would feel more secure with a portion of their portfolios invested in annuity structures that protect against market risks. It makes sense as outliving their nest eggs is a formidable concern.

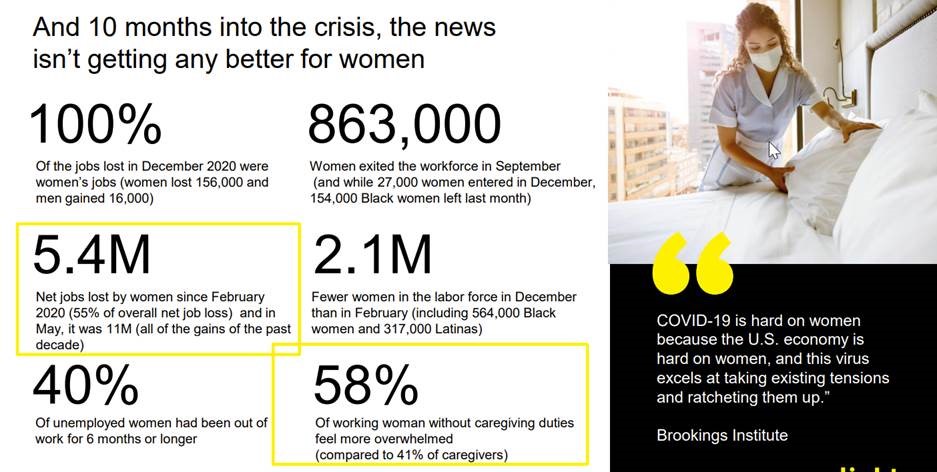

The Tsunami for working women.

Sharon sent me a copy of The Washington Women’s Leadership Initiative January 2021 presentation titled The Tsunami For Working Women – Exploring the direct impact of COVID-19 on women in the workplace.

The results didn’t surprise me. However, the ongoing damage warrants dramatic improvement and requires widespread efforts. From corporate boardrooms to advisors to inside the psyche of females, change is imminent.

Women’s financial empowerment is a topic near and dear to my heart. I have a 22-year-old daughter raised to be financially independent. She’s embraced numbers so much she begins the graduate program at Emory for scientific mathematics in the spring.

As part of the Emory Scientific Computing Group, she’ll develop fast, reliable numerical algorithms required to solve complicated mathematical problems in a wide variety of applications.

We must not let our daughters, sisters, mothers, all women, be intimidated by numbers.

In light of the state of women’s finances, here are four survival tips to consider.

1. Embrace all that feels uncomfortable.

It may be uncomfortable to stray from a comfort zone; however, think of yourself from now on as ‘the lone survivor.’ With longevity, women must embrace and understand the ‘flow’ of their household finances. After her partner is gone, it’s essential for a woman not to feel financially ‘lost.’

Perhaps your husband handles the money chores. That’s fine, but no excuse to avoid engagement at least thirty minutes a week. Consider a money date, a financial update that includes a complete review of credit usage, savings, investment goals, and spending.

Academic studies show how women are better than men at risk management. So it’s up to them to make sure male partners can communicate spending, debt controls, and saving rates. As a couple, are you both investing in a balanced, risk-efficient manner? Is your spouse riskier than you prefer with your asset allocation?

Consider hiring on an hourly basis a Certified Financial Planner, a fiduciary, to help create a comprehensive financial plan. An objective planner will coach you through the red flags, validate good fiscal habits, and outline areas of improvement.

2. Remember these two words: Risk mitigation.

In the paper “Understanding the True Cost of Health Care in Retirement, ” Nick Halen, RICP, Kelli Faust, FSA, MAAA, and Todd Taylor, FSA outline two risks that increase spending variability in retirement: long-term care events and longevity or the probability of longer life expectancy.

Studies by The Metlife Mature Market Institute®, a center of expertise in aging, longevity, and the generations outline that U.S. women live extra-long lives and 8% longer than men on average. Women face a unique series of challenges such as aging solo and overall higher healthcare expenses resulting from living extended lives.

Listen up, women: With the strong possibility of outliving a partner, investment assets must live as long you do. Special attention needs to be paid to the life and long-term care insurance areas so that retirement assets are at less risk from early depletion.

Guaranteed income products should be a strong consideration for women.

Women should consider guaranteed income structures such as annuities to bolster Social Security spousal and survivor benefits. Men are overconfident. Heck, we think we’re going to live forever. Unfortunately, we hesitate to view outlier events that can affect non-working spouses!

Subsequently, the only path to understanding how much insurance is required to mitigate risks is holistic financial planning. I rarely understand how consumers arbitrarily opt to purchase annuities or insurance products without a laser-targeted plan that includes specific dollars allocated to insurance-related products.

3. Avoid Social Security benefits blunders.

The right method to claim Social Security can make or break a woman’s household, especially if she’s aging solo and relying primarily on survivor benefits (all too common). Women suffer greater retirement insecurity than men since, generally, they’re the ones who stay at home or have careers interrupted to raise children.

A stalled work history creates what I deem “a ZERO problem,” whereby a female’s Social Security statement reflects years of earning 0, resulting in lower lifetime benefits. Thus, a higher-wage earner must wait until age 70 to claim benefits to afford higher survivor benefits for a spouse.

Our team also suggests that the non-working spouse returns to the workforce and fill those zeroes with earned income. Several years ago, I helped a female client return to her career, and I’m happy to learn how her own Social Security benefits increased from $1,200 a month to close to $1,700. Tackling those zeroes makes a big difference in lifetime benefits.

Older adults believe women live to 83.7. In actuality, they will live to 89 years old. On average, men will live to be 87. More senior adults think men will live to be 81.6. Longer life expectancies warrant serious consideration to postponing Social Security until age 70, especially in the face of dwindling private pensions.

In other words, a guaranteed income is vital to the survivability of an investment portfolio. During periods of future low investment returns, the maximization of guaranteed income options can help retirees adjust or reduce portfolio withdrawals.

Waiting until 70 is a smart Social Security strategy.

If a future Social Security recipient waits until age 70, monthly payments can be 32 percent higher than the benefits earned at full retirement age. Currently, the full retirement age is 66 and 2 months for those born in 1955; for people born in 1960 or later, FRA is 67.

It’s essential to partner with a financial professional who understands the devastating impact of impetuous Social Security claiming decisions. RIA Certified Financial Planners® have prevented individuals from losing thousands of dollars in lifetime and survivor income benefits due to misinformation from brokers, friends with strong opinions, and understandable old misconceptions.

4. Take control now!

Although inadequate financial literacy crosses both genders, women tend to score less than men on several key metrics. Women do not as well understand investment basics, life insurance, company retirement plans, and IRAs. That’s according to The American College’s Women’s Retirement Literacy Report from January.

On a positive note, their 2020 survey found that more than 9 out of 10 women with partners or spouses equally share or lead financial household decision-making. Didn’t need to tell me that. I witness it daily. Younger generations of women are more engaged, and for that, I’m thankful. However, there’s still more work to do.

Stay tuned for our upcoming live webinar/lunch & learn about how women can make better Social Security decisions.

Richard Rosso, MS, CFP, CIMA is the Head of Financial Planning for RIA Advisors. He is also a contributing editor to the “Real Investment Advice” website and published author of “Random Thoughts Of A Money Muse.” Follow Richard on Twitter

Customer Relationship Summary (Form CRS)

Also Read