Not surprisingly, the University of Michigan Consumer Sentiment Survey fell again. The index hit 59.7 versus expectations of 61.0 and the prior reading of 62.8. Driving the poor consumer sentiment is the Russian invasion and, possibly, more critical its effect on already high rates of inflation. To that end, one-year inflation expectations rose to 5.4% from 4.9%. As ZeroHedge shows below, that level was last seen in 1981. The current consumer sentiment survey reading of 59.7 is commensurate with prior levels during recessions. The following statement from the report is troubling considering that consumers account for two-thirds of economic activity. “Personal finances were expected to worsen in the year ahead by the largest proportion since the surveys started in the mid-1940s.“

What To Watch Today

Economy

- No notable reports scheduled for release

Earnings

Post-market

- Vail Resorts (MTN) to report adjusted earnings of $5.69 on revenue of $954.9 million

- Coupa Software (COUP) to report adjusted earnings of $0.06 on revenue of $186.46 million

Weekly Market Recap With Adam Taggart

Market Trading Update

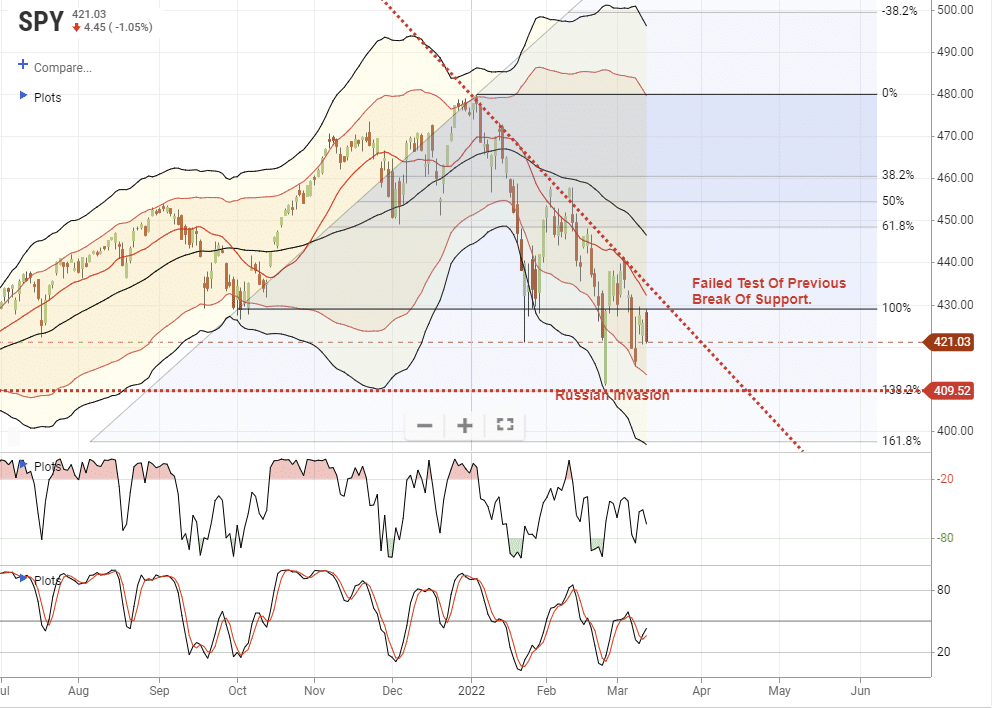

As has been the case all year, market volatility remained constant last week. Stocks surged early in the week on hopes of talks between Russia and Ukraine, but hopes faded into Friday. Notably, the S&P 500 index broke the main support level of the January and September lows.

That break sets the market up for a retest of the lows set when Russia initially invaded Ukraine. A failure to hold that low and we are looking at a 161.8% Fibonacci retracement from the all-time highs, which would be roughly 4000 on the S&P index. The consumer sentiment survey is collapsing quickly which is recessionary in nature.

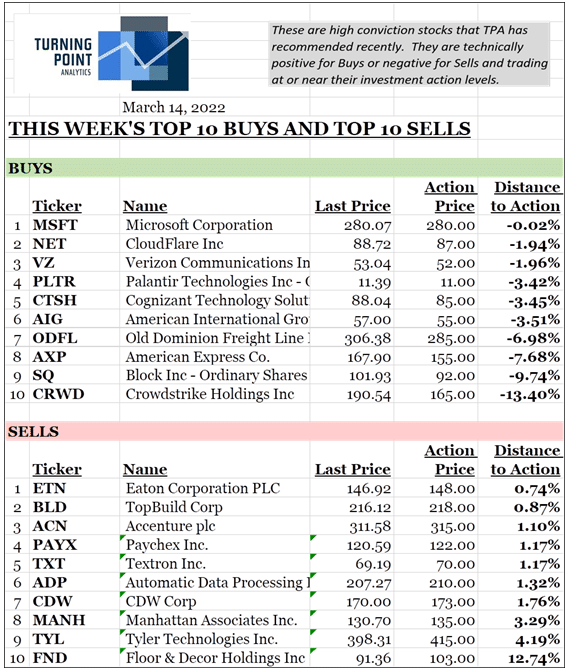

TPA Research – Top 10 Stocks To Buy And Sell

Click on RIAPro+ today to add TPA Research to your subscription for just $20/month.

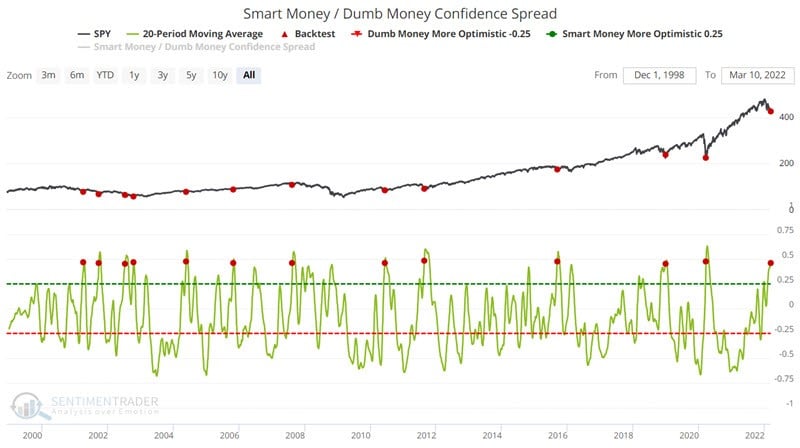

Dumb Money Suggests A Rally

The chart below displays each time the 20-day average for the Smart Money / Dumb Money Confidence Spread crossed above 0.45 for the first time in 21 days. As shown, retail investors tend to usually be on the wrong side of the trade. The current higher levels of bearishness by retail investors historically argue for better market days ahead. Of course, there is no guarantee.

The Week Ahead

This week’s big story is the Fed’s FOMC meeting and whether they hike rates by 25 or 50 basis points. Equally important, will they present a more dovish or hawkish tone than the markets are expecting. We think the Fed will use geopolitical concerns for cover to only raise rates by 25bps. If that is the case we will be interested to see if any voting members vote for 50bps and or reductions in the balance sheet. In his press conference, we expect Chairman Powell to address the future pace of rate hikes and balance sheet reductions.

On the heels of CPI last week, we will get another inflationary reminder with PPI on Tuesday. The current expectation is for a 10% increase year over year. In addition to the Fed on Wednesday, the Census Bureau will release Retail Sales. The data is for February. As such, the effects of the Russian invasion and spurt higher in gas prices will not factor into the number. The following Retail Sales number will probably be weak, reflecting the recent University of Michigan Consumer Sentiment survey.

Will Congress Stoke Inflation?

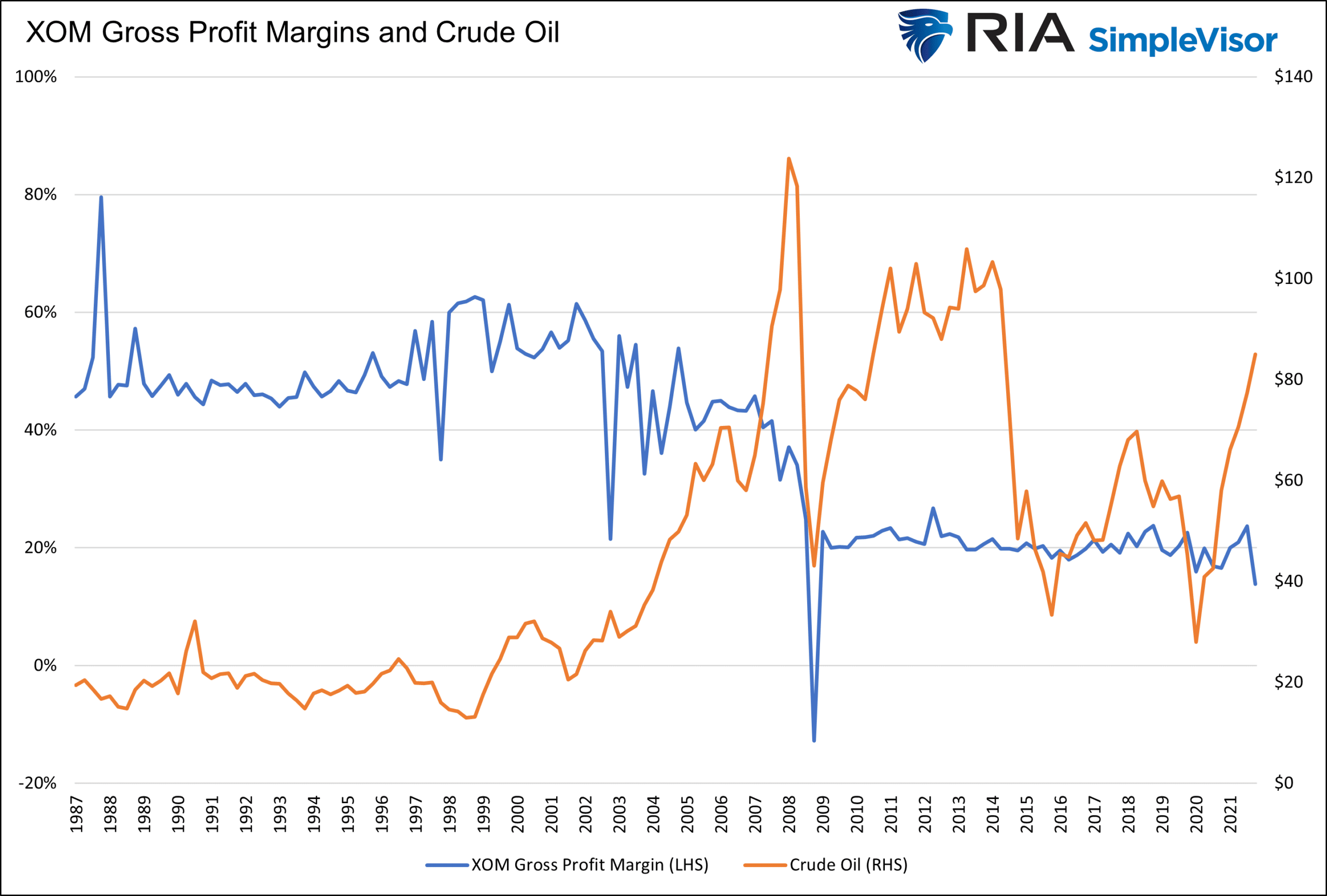

Legislators introduced the “Big Oil Windfall Profits Tax Act.” The bill’s objective is to tax the windfall profits of large oil companies at a 50% rate. The proceeds from the tax will go to consumers earning less than $75k through direct payments. From a purely macroeconomic perspective, this bill will likely further stoke inflation. For starters, the bill disincentivizes “big oil” to explore and drill for new oil wells. In some cases, oil companies may shut down wells that are not profitable enough with the tax. A limited supply of oil will undoubtedly push prices higher. Second, one of the primary reasons for the current bout of inflation is the massive fiscal stimulus programs and the extra demand generated by the checks to the public. As we saw in 2020 and 2021, checks to the public will get spent and increase demand for all kinds of products.

The other flaw with the bill is that there is no relationship between oil prices and profit margins, as some legislators contend. The graph below shows the relative stability of Exxon’s (XOM) gross profit margins versus the fluctuating price of crude oil. We will have more on this topic in an article on Wednesday.

Tightening Financial Conditions

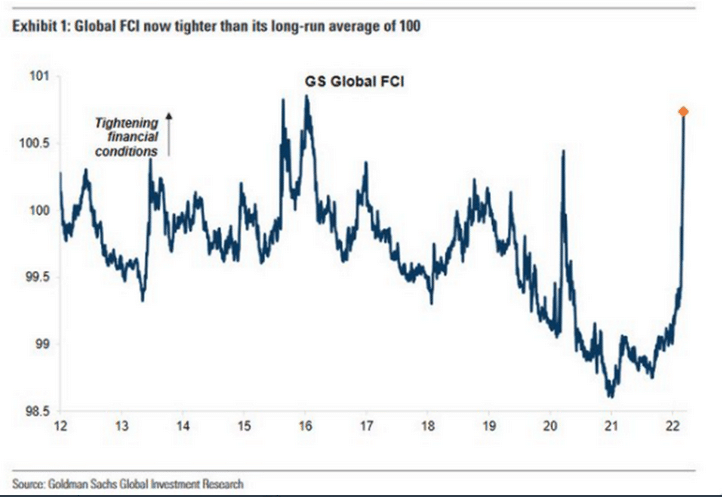

As we consider what the Fed may or may not do on Wednesday we must think about the graph below. The chart below, courtesy of Goldman Sachs, shows that financial conditions have tightened up considerably over the last month. They are now at five-year highs. Fighting inflation is likely top of mind for the Fed, but they will also consider financial stability. Financial stability is a function of the ease or difficulty with which borrowing and lending occur throughout the economy. When credit markets freeze up, the results can be disastrous, as we saw in 2008.

Second Order Financial Effects on the Financial Sector

The following from Almost Daily Grant’s shares an emerging problem facing emerging market investors, mutual funds, and ETFs that hold Russian assets. Per the commentary:

“The West’s comprehensive financial response to Russia’s invasion of Ukraine has rippled far and wide, as the Moscow Stock Exchange remains shut and investors remain unable to value their positions, let alone exit them. Yesterday, MSCI and FTSE Russell announced that they will cull Russian assets from benchmark indices, following suit from Stoxx’s decision a day earlier.”

“Second-order effects may be another story, as emerging market-focused managers unable to sell Russian assets were forced to raise cash elsewhere to meet redemptions. The Wall Street Journal reports today that some EM funds have weighed asking the Securities and Exchange Commission for a waiver on rules governing investor redemptions as well as the proportion of illiquid assets a fund can hold.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

Also Read