With the latest round of inflation data in hand, it appears the Fed has two paths to consider. Nick Timiraos of the WSJ lays out the “bumpy” or “stuck” inflation scenarios the Fed faces in his latest article, Fed Rate Cuts Are Now A Matter Of If, Not Just When. Given Nick’s unique access to Jerome Powell and the Fed, his discussion of the most recent inflation data is essential in gauging what the Fed may or may not do.

The bumpy Fed path is the expectation that inflation is still trending lower but will do so in a bumpy manner. This bumpy but lower inflation theory is primarily based on prices of CPI shelter (rent). Rent prices constitute 40% of CPI. Rent is a lagging indicator that will decline; it’s just a question of when. The graph below from the article shows that core CPI is running below 2% without shelter prices. The other key point in the graph is that inflation is now concentrated and not as widespread as it was in 2022 and early 2023. The bumpy path entails the Fed will likely cut rates later in the year.

The second path is the stuck path. This case argues that inflation is stuck around 3% to 3.5%. Unless the economy slows and or the unemployment rate increases, the Fed may have to leave rates alone this year. Accordingly, this scenario makes it more difficult for the Fed to achieve a soft landing. They remain concerned that the lag effect will weigh on economic growth. If prices are indeed stuck, the Fed will find it more challenging to get ahead of a slowdown. Instead, they will have to wait for the slowdown to happen before they can react.

What To Watch Today

Earnings

Economy

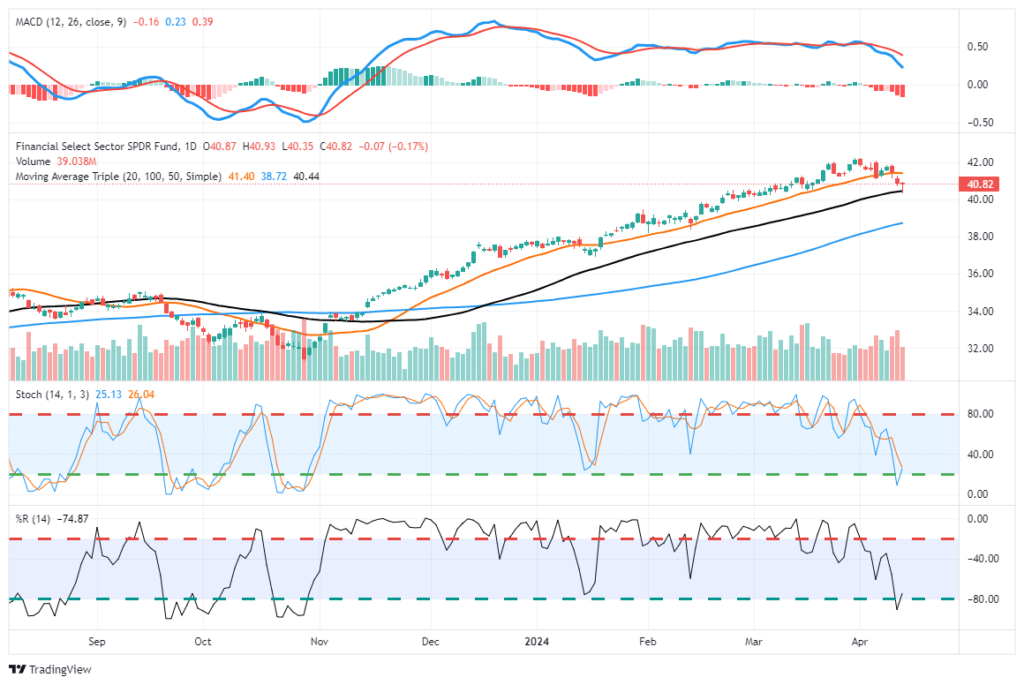

Market Trading Update

Welcome to the kick-off of #MillennialEarningsSeason, where everyone gets a trophy after dropping earnings estimates that are enough for everyone to clear the bar. The major banks are the first to report starting today. Like the overall market, the banking sector has been under selling pressure lately, bounced off the 50-DMA yesterday, and decently oversold. Given that the likes of $JPM, $WFC, and $BLK will likely report better-than-expected earnings, we would not be surprised to see a bit of a countertrend rally today.

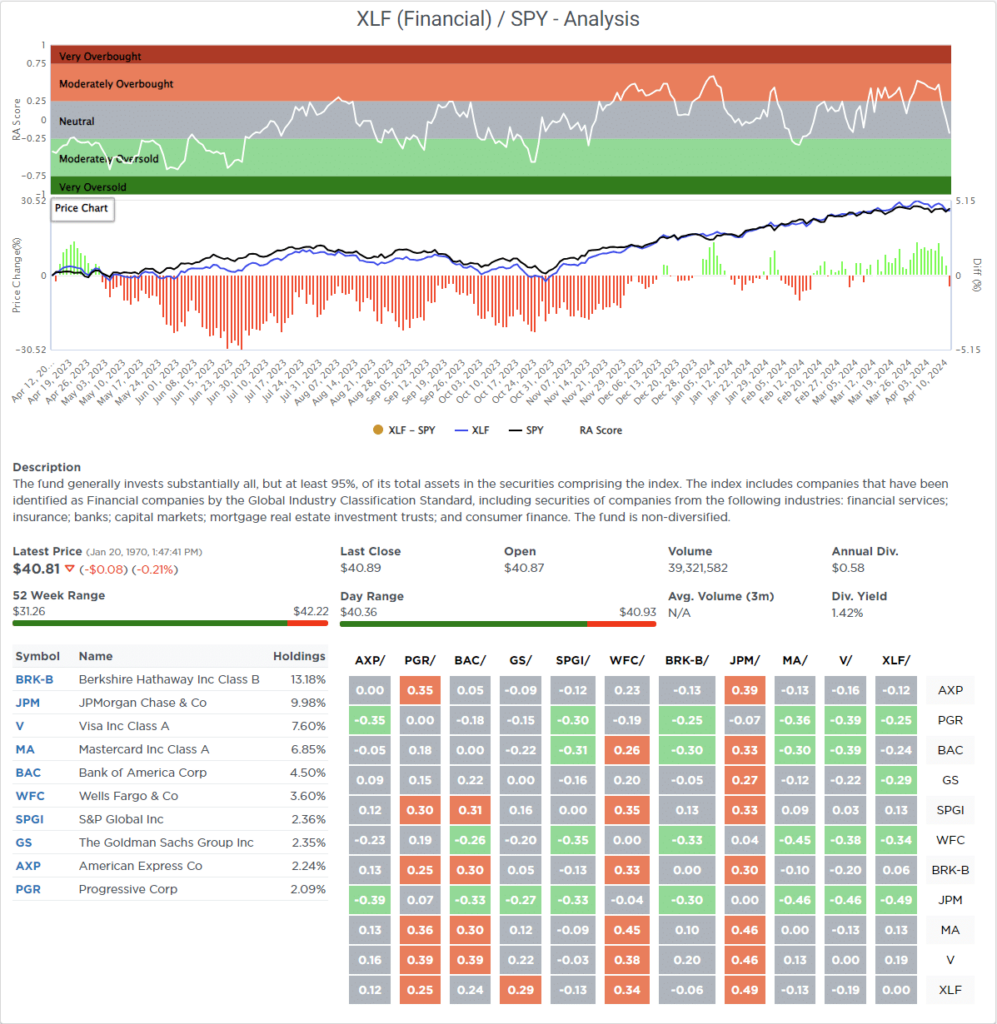

If we examine the top 10 holdings of the financial sector ETF (XLF), we find that relative to the ETF, $PGR, $GS, $WFC, and $JPM are the most overbought. Therefore, the upside may be somewhat limited in those issues. Still, we could see better potential performance from companies like $BAC, $BRK-B, $AXP, $MA, and $V, which are getting closer to oversold following recent corrections. While XLF may see some performance pickup relative to the broader market, investors may do better by being selective in their financial exposures.

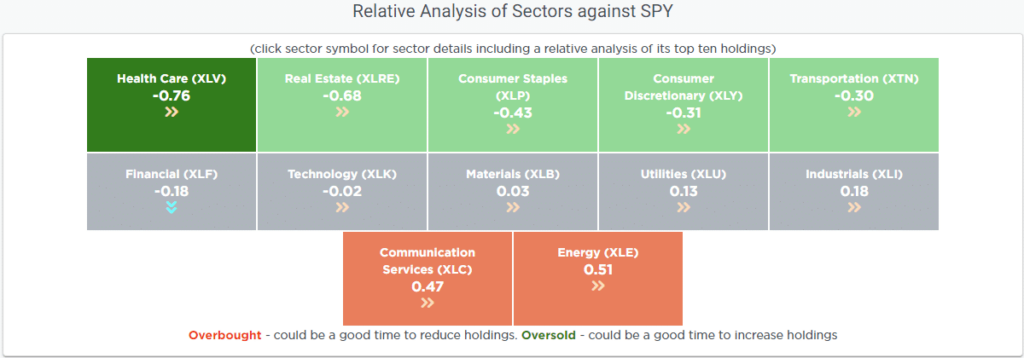

However, while Financials are kicking off the reporting season today, the Healthcare sector currently has our attention. Given its broad decline in recent weeks and the strong fundamentals of the underlying companies, there appears to be a good bit of value developing in that sector. We are starting to dig in, looking for opportunities.

PPI Bodes Well For PCE

The second round of inflation data, PPI, was more market-friendly than CPI. Headline and core PPI were .10% below expectations at 0.2% and below last month’s readings of 0.6% and 0.3%, respectively.

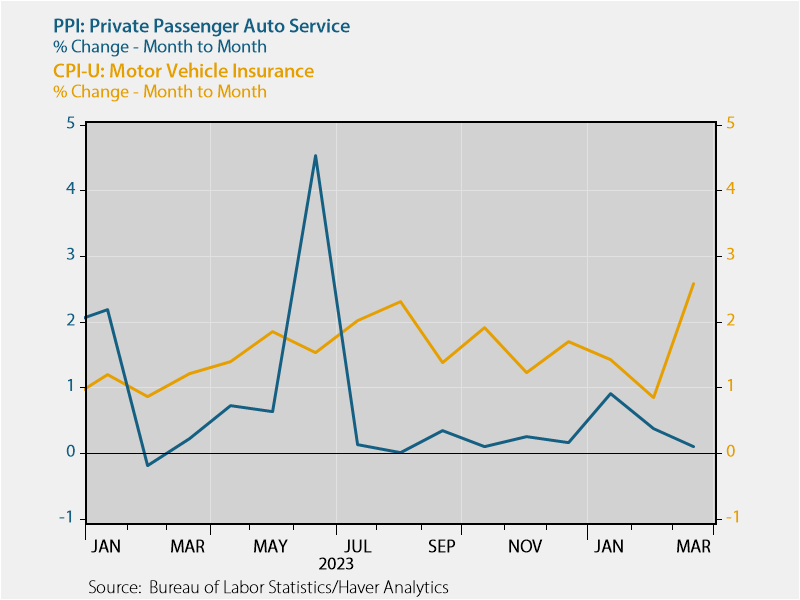

You may be confused about why PPI and CPI send different signals. The important thing to consider is that the Fed prefers PCE prices over both measures. In that light, consider that the surge in motor vehicle insurance single-handedly boosted yesterday’s CPI number above expectations. However, auto insurance within the PPI report came in much cooler at 0.1% versus CPI’s 2.6%. Most importantly, PCE uses the PPI motor vehicle insurance figure, not the one in the CPI report. The graph below, courtesy of Ernie Tedeschi, shows the divergence between the two measures. Further, shelter prices have less of a weighting in PCE than CPI. As a result of just PPI auto insurance and the lesser contribution of shelter prices, PCE will likely be 0.2% below CPI.

The Fed Signals A Reduction In QT

Wednesday’s release of the Fed minutes implies the Fed will likely reduce the amount of QT as early as their next meeting. Currently, the Fed lets $60 billion of U.S. Treasury securities and $35 billion in mortgage-backed securities roll off their books each month. The minutes indicate that most officials favor reducing the Treasury rolloff amount by “roughly half.” Further, “the vast majority of participants judged that it would be prudent to begin slowing the pace of runoff fairly soon.”

The reduction would serve two purposes. The first is to help stem the recent increase in interest rates. If investors have less Fed supply to absorb, they can take more supply from the market. Second, the Fed is concerned that the level of reserves in the banking system is getting close to “ample.” Sub-ample reserves could result in a liquidity crisis, as we saw in 2019, which followed QT in 2018 and early 2019. At that time, they reduced their balance sheet by about $.5 trillion before sparking problems. The balance sheet has fallen by $1.5 trillion since QT started in 2022.

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.