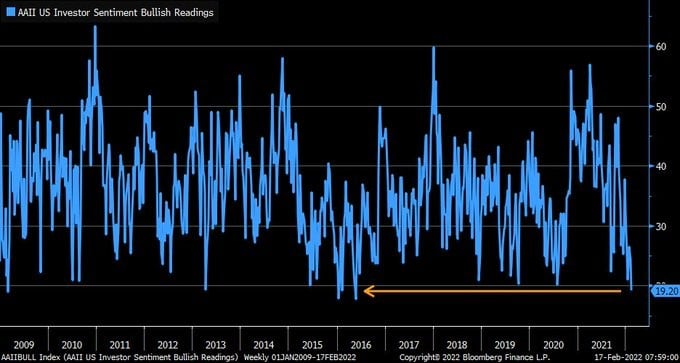

As we noted on Friday, the latest AAII Sentiment Survey reflects a decrease in bullish sentiment to levels last seen in early 2016. Bulls are dwindling as economic data continues to warrant a hawkish Fed. While last week’s FOMC minutes initially garnered a positive market reaction, reducing the implied odds of a 50bps hike in March, the message was nothing short of hawkish.

Russia-Ukraine tensions grabbed headlines once again on Friday, sending equities heading lower into the long weekend. On a positive note, Friday, the FOMC announced that it is adopting stricter trading rules for senior officials. Find the details HERE.

What To Watch Today

Markets are closed today for Presidents Day.

Weekly Market Wrap With Adam Taggart – Why We’re Buying Bonds

Every week, we do a market recap with Adam Taggart – we post it every Saturday at RealInvestmentAdvice.com.

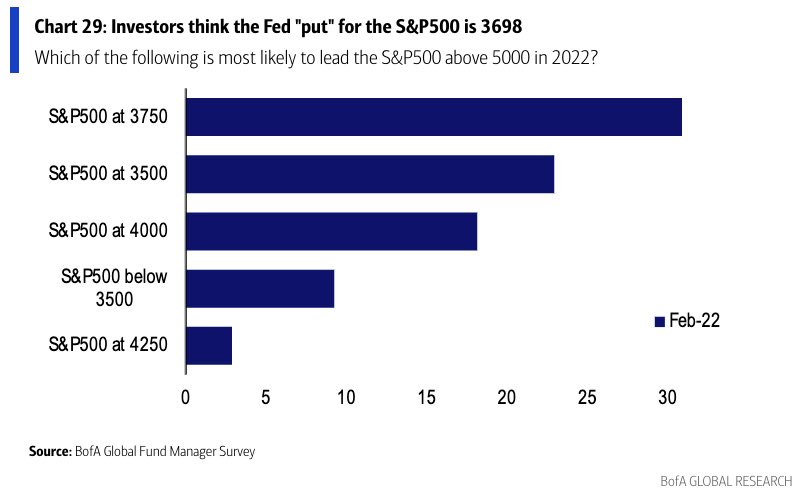

Where Is The Fed Put?

While the bulls are dwindling, the bulls are starting to ask the question “where is the Fed put?”

The “Fed put” is the level where the Federal Reserve will take action to begin supporting asset markets by reversing rate hikes and restarting quantitative easing (QE) programs. Recently, a BofA fund managers survey pegged 3750 as the level they thought the “Fed put” resides.

While the BofA fund managers may be correct, my targets are slightly different as they are a function of Fibonacci retracement levels from the March 2020 closing lows. From the peak close of the market, the targets are:

- 38.2% rally retracement = 3829 = 20% market decline (Fed likely worried)

- 50% rally retracement = 3523 = 27% market decline (Margin calls triggered. Fed likely acts.)

- 61.8% rally retracement = 3217 = 33% market decline (Fed put triggered)

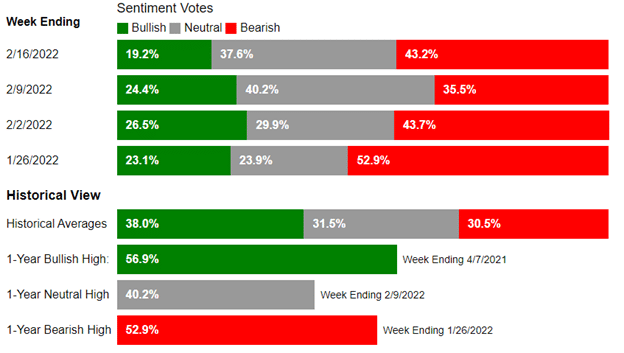

Bulls Are Becoming Increasingly Short in Supply

According to the most recent survey by the American Association of Institutional Investors, Bulls are dwindling. Bullish sentiment decreased to its lowest levels since 2016, while neutral and bearish sentiments are above norms. Peaks in bearish sentiment typically coincide with a good buying opportunity for equities. Although, with the S&P 500 down only 7% YTD, will it be the case this time too?

Margin Debt Has Peaked

As shown below in the chart courtesy of Tier1 Alpha, there is a significant correlation between YoY growth in margin debt and performance of the S&P 500 index. YoY growth in margin debt has peaked above 40% only three times since 2000. These peaks were followed by large liquidations and bear markets in two of the three instances, while the third was followed by liquidations and a period of lackluster returns. With margin debt recently having peaked at YoY growth well above 40%, the implications for index returns may not be terrible, but they clearly aren’t good.

The Week Ahead

The NYSE and Nasdaq will be closed today in observance of President’s Day. Normal trading hours will resume tomorrow, February 22nd.

The pipeline of economic data this week kicks off tomorrow with the S&P/Case-Shiller Home Price Index, Markit PMI Flash, and Consumer Confidence. Thursday, we will receive the second estimate of Q4 GDP growth, jobless claims, the Chicago Fed Index, and home sales data. Then, Durable Goods Orders, Personal Income and Outlays, and consumer sentiment data will come out on Friday.

We will hear from the Fed’s Bowman today. Then Bostic, Mester, and Waller will speak on Thursday.

The Intersection of Asset Prices and Inflation

Last Friday, we shared some comments from Zoltan Pozsar on the Fed’s options going forward. Our post can be found HERE. In economics, the “wealth effect” suggests that inflated asset prices make households feel better off, thus increasing aggregate demand. It could also reduce the labor supply in extreme cases, and we are currently facing labor shortages which add to inflation. Ultimately, Zoltan opines that the Fed may have to curb inflation by engineering a correction in asset prices due to political pressures.

Rabobank joined the conversation expressing similar views:

“All Fed choices are bad. There is no oasis ahead, as markets like to believe. There is no Fed ‘ master plan’ to stop inflation without stopping either the asset-price appreciation we’ve built markets on for decades or the faux appreciation for the working class we’ve built markets on the backs of for decades or both.”

Wall Street is confronting the intersection of asset prices and inflation, and this may help explain why bulls are dwindling.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

Also Read