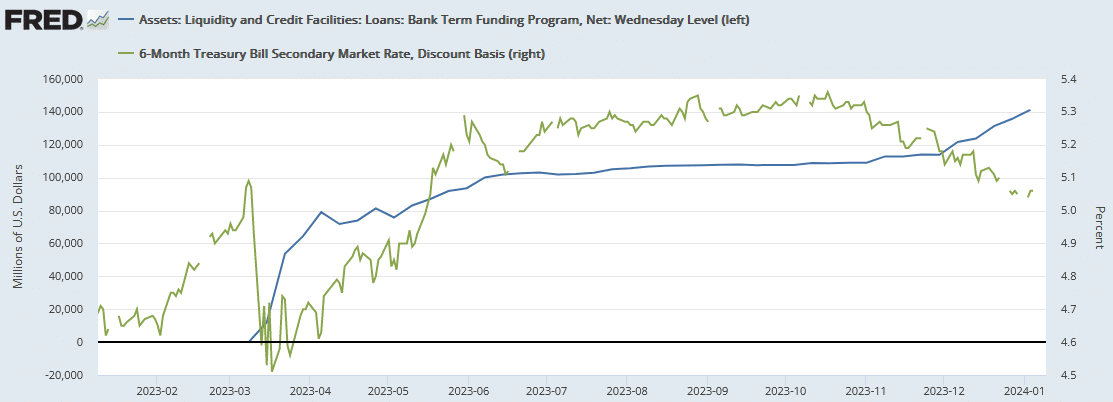

The Fed came to the banking sector’s rescue in March 2023 with the Bank Term Funding Program (BTFP). This latest bank rescue program allows banks to replace lost deposits with a Fed loan. Instead of having to sell underwater assets and take a loss, participating banks can replace deposits with a collateralized loan from the Fed. Within the program are two unusual benefits. The first benefit is that the loan amount is not based on the pledged collateral market value. Instead, its nominal value is used. In other words, a bond trading at 75 cents can be used to borrow $1.00. Secondly, and making headlines today, the interest rate on the loan is based on interest rate expectations.

Consequently, with the market now pricing in rate cuts, the rescue program has become a profit center for banks. Per the Wall Street Journal, “An emergency lending program the Federal Reserve created during the 2023 banking crisis has turned into easy money.” As shown below, usage of the BTFP increased at the same time rate expectations started to decline. The program’s borrowing rate is now lower than the rate at which they can reinvest those funds at the Federal Reserve. Simply, the Fed is providing banks a risk-free arbitrage. The bank “rescue” program is expected to end in March. We suspect that if extended, there will be new guidelines to eliminate the arbitrage.

What To Watch Today

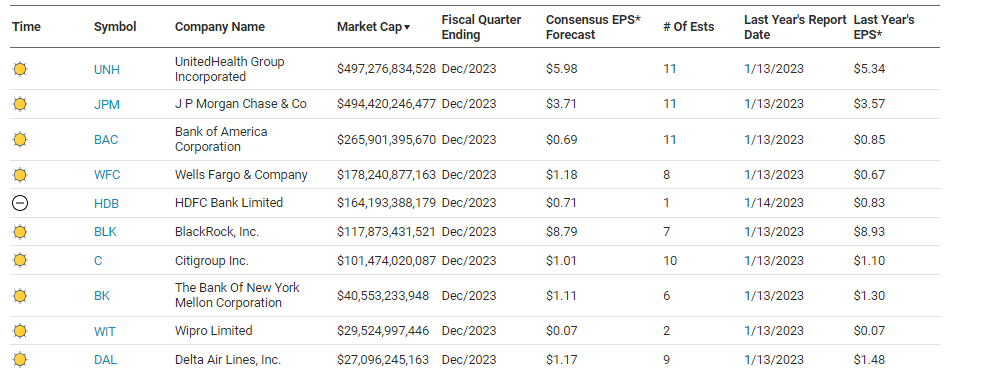

Earnings

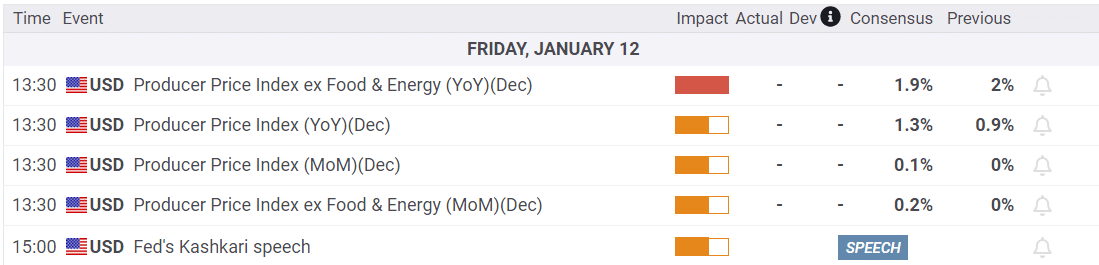

Economy

Investing Summit: Early Bird Registration Available Now

January 27th, we are hosting a live event featuring Greg Valliere to discuss investing in the 2024 presidential election. What will a new president mean for the markets, the risks, and where to invest through it all? Greg will be joined by Lance Roberts, Michael Lebowitz, and Adam Taggart for morning presentations covering everything you need to know for the New Year.

Register now, as there are only 150 seats. The session is a LIVE EVENT, and no recordings will be provided.

Market Trading Update

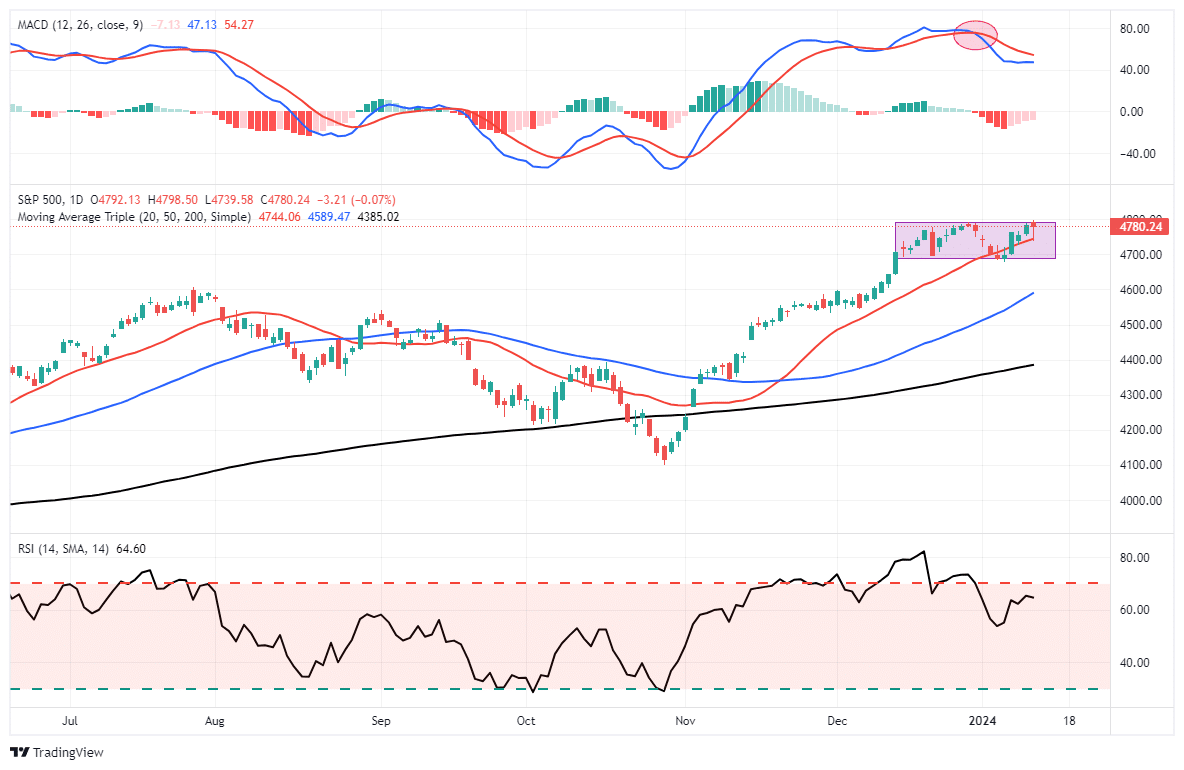

Stocks trading mixed yesterday, falling decently in early trade on the CPI inflation report, which showed increases in the index’s largest component – housing. As shown, the market tested and held the 20-DMA once again and recovered to break even by the close. Notably, technology stocks saved the afternoon from a more dismal outcome. The fact the market keeps recovering from early sell offs is bullish as it suggests there are buyers on dips. Such should keep the market afloat for now. However, as repeated over the last several weeks, the current MACD “sell signal” keeps a lid on prices for now. Hold cash until the market declares its next move, either higher or lower.

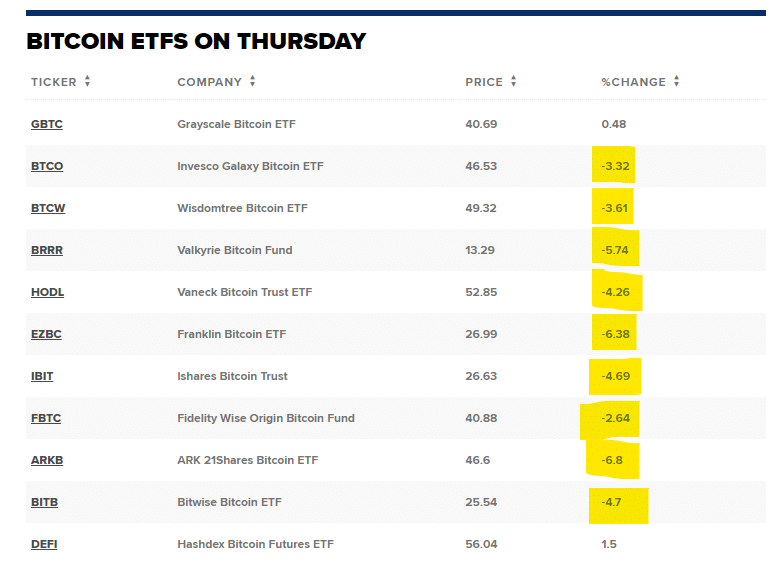

More interesting yesterday came from the ETF sector. After a decade-long fight to launch a “Spot Bitcoin ETF,” such was finally achieved with great fanfare yesterday as roughly a dozen new ETFs launched for investors to speculate with. The outcome was less than desirable, with most of the ETFs ending in the red for the day. The only two that didn’t were pre-existing non-spot ETFs that are in the process of converting. Unfortunately, Cathy Wood’s new ARK Bitcoin ETF was the biggest loser yesterday.

While these ETFs provide a new way to speculate in portfolios on the direction of cryptocurrency, we would suggest waiting for a bit until the market dynamics smooth themselves out somewhat. Once time passes, and there is some historical price action in these products, you can then use some basic technical analysis to better risk manage your position.

Wage Growth In A New Light

If you recall, in 2022 and early 2023, Jerome Powell was constantly harkening back to the 1970s, recalling how the circular relationship between prices and wages fed inflation. Such a feedback loop between prices and wages is called a price-wage spiral. Powell aimed to kill inflation before such a loop could amplify inflationary pressures. Consequently, Fed concerns over a price-wage spiral drove the Fed’s aggressive monetary policy.

The latest Atlanta Fed wage growth tracker has been at +5.2% for the past three months. Such is above the 3.00-3.50% range existing before the pandemic but nicely below the pandemic peak.

For more on this index, we share the work of Parker Ross. He recalculated the index to account for seasonal wage pressures. Per Parker Ross:

However, if you transform the y/y data into an index and seasonally adjust that index, we can get a better read on the shorter-term trends, and dare I say they look almost “normal.” Based on this transformation, the 6m seasonally adjusted annualized median wage growth was 3.6% in Dec ’23, up from 3.2% in Nov ’23. Looking at a more smoothed version, given the volatility of this data, the 6m avg annualized growth was 4.1%, down from a peak of 6.9% back in June ’22. The current pace of typical wage growth is below the late ’90s, in-line with the early 2000s, and just a hair above the years immediately preceding the pandemic. There is no wage-price spiral to fear.

Parker’s graph below shows the long-term trend of higher wages on a non-seasonally adjusted basis. What stands out in this graph is the monthly variations in the index. Therefore, stripping out these variations leads Parker to believe the wage growth is already back to pre-pandemic levels.

CPI Update

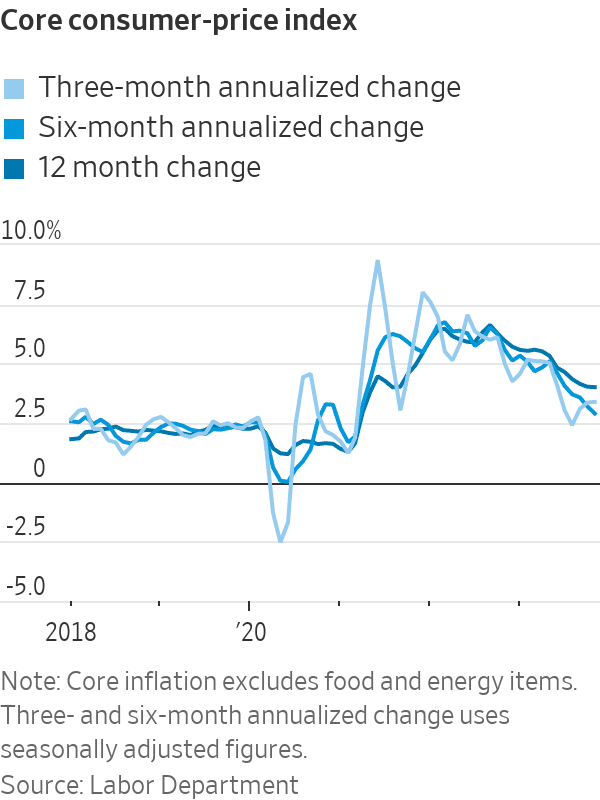

Headline CPI was a little hotter than expected at +0.3%, while the core rate met expectations and also rose by 0.3%. The core annual rate is now 3.9%, down a tenth of a percent from last month and well below the +6.3% last January. While the inflation data was slightly higher than expected, it is not likely to cause alarm at the Fed. The trend lower, as we show below, is still intact.

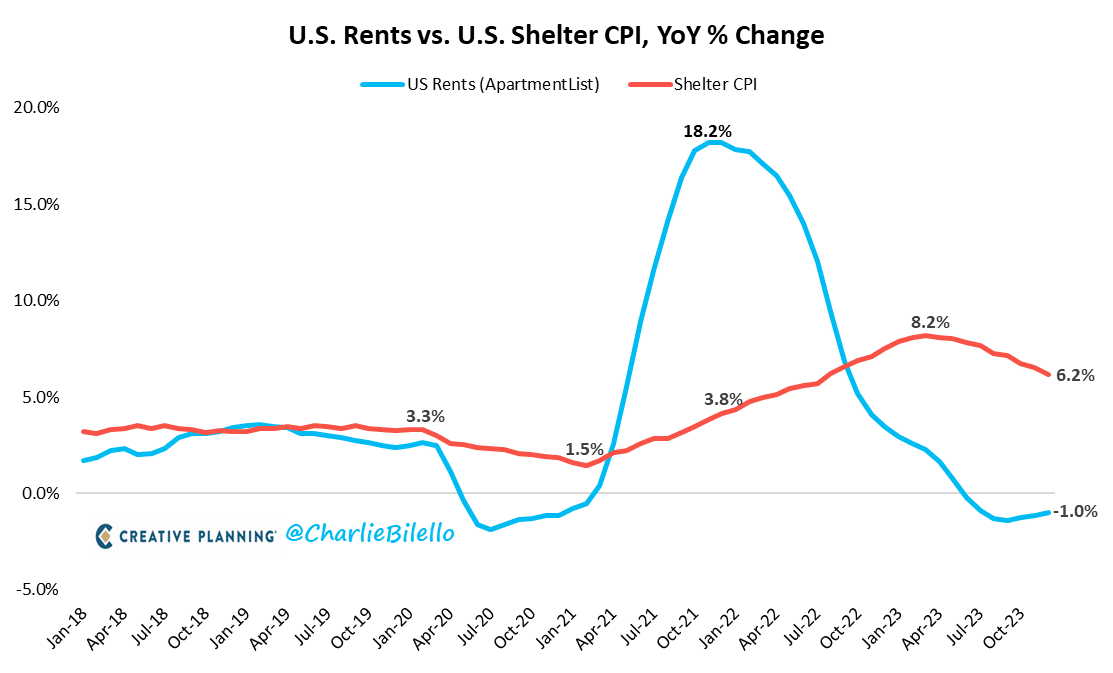

The shelter component, accounting for nearly 40% of the CPI calculation, continues to run much higher than what is being experienced in the economy. This significant lag between CPI and real-time data is well-known by the Fed. In the CPI report, shelter rose by 0.5%, with the three components of shelter increasing as follows:

- Owners equivalent rent: +0.5%

- Rent +0.5%

- Lodging away from home: +0.4%

The shelter index was +6.2% year over year, accounting for over two-thirds of the total increase in the core CPI. The graph below, courtesy of Charles Bilello, highlights why we should expect shelter prices to ease in the coming months and pressure CPI lower. Rent prices are declining on a year-over-year basis, yet the shelter index is still rising by 6.2%. The lag between real shelter prices and CPI prices is at least a year. Conservatively, we think shelter prices stabilize closer to 2-3%. Therefore, assuming all other inflation measures do not change, which is a big assumption, inflation should fall below the Fed’s target over the next year.

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read