The Fed took another step Wednesday on its path to slay inflation. As widely expected, the Fed increased rates by .75%. The next steps for the Fed likely include a 50bp increase in December and 25bp hikes in February and March. Currently, Fed Funds futures imply 5% Fed Funds by the spring of 2023. At that point, many, including Fed members, think the next step is to wait and see. As we have noted numerous times, the biggest risk with aggressive Fed hikes is the lag effect. Steps to raise interest rates last spring and early summer are just starting to take a bite out of inflation and economic activity.

Waiting and watching, aka pausing, allows for the 3.75% in hikes we have already witnessed, plus future rate hikes to get digested into the economy. Regardless of market narratives, pausing is not a pivot. A pivot, which the stock market anxiously awaits, starts with a Fed discussion of steps to lower rates and or reduce the amount of QT. That did not occur yesterday. A pause is also not on the immediate horizon. Per Powell: “it’s very premature to talk about pausing policy.”

What To Watch Today

Economy

- 7:30 a.m. ET: Challenger Job Cuts, year-over-year, October (67.6% prior)

- 8:30 a.m. ET: Trade Balance, September (-$72.3 billion expected, -$67.4 billion prior)

- 8:30 a.m. ET: Nonfarm Productivity, Q3 preliminary (0.5% expected, -4.1% prior)

- 8:30 a.m. ET: Unit Labor Costs, Q3 preliminary (4.0% expected, -10.2% prior)

- 8:30 a.m. ET: Initial Jobless Claims, week ended Oct. 29 (220,000 expected, 217,000 prior)

- 8:30 a.m. ET: Continuing Claims, week ended Oct. 22 (1.450 million expected, 1.438 million prior)

- 9:45 a.m. ET: S&P Global U.S. Services PMI, October final (46.6 expected, 46.6 prior)

- 9:45 a.m. ET: S&P Global U.S. Composite PMI, October final (47.3 expected, 47.3 prior)

- 10:00 a.m. ET: Factory Orders, September (0.3% expected, 0.0% prior)

- 10:00 a.m. ET: Factory Orders Excluding Transportation, September (0.2% prior)

- 10:00 a.m. ET: Durable Goods Orders, September final (0.4% expected, 0.4% prior)

- 10:00 a.m. ET: Durables Excluding Transportation, September final (-0.5% prior)

- 10:00 a.m. ET: Non-defense Capital Goods Orders Excluding aircraft, September final (-0.7% prior)

- 10:00 a.m. ET: Non-defense Capital Goods Shipments Excluding Aircraft, September final (-0.5% prior)

- 10:00 a.m. ET: ISM Services Index, October (55.4 expected, 56.7 prior)

Earnings

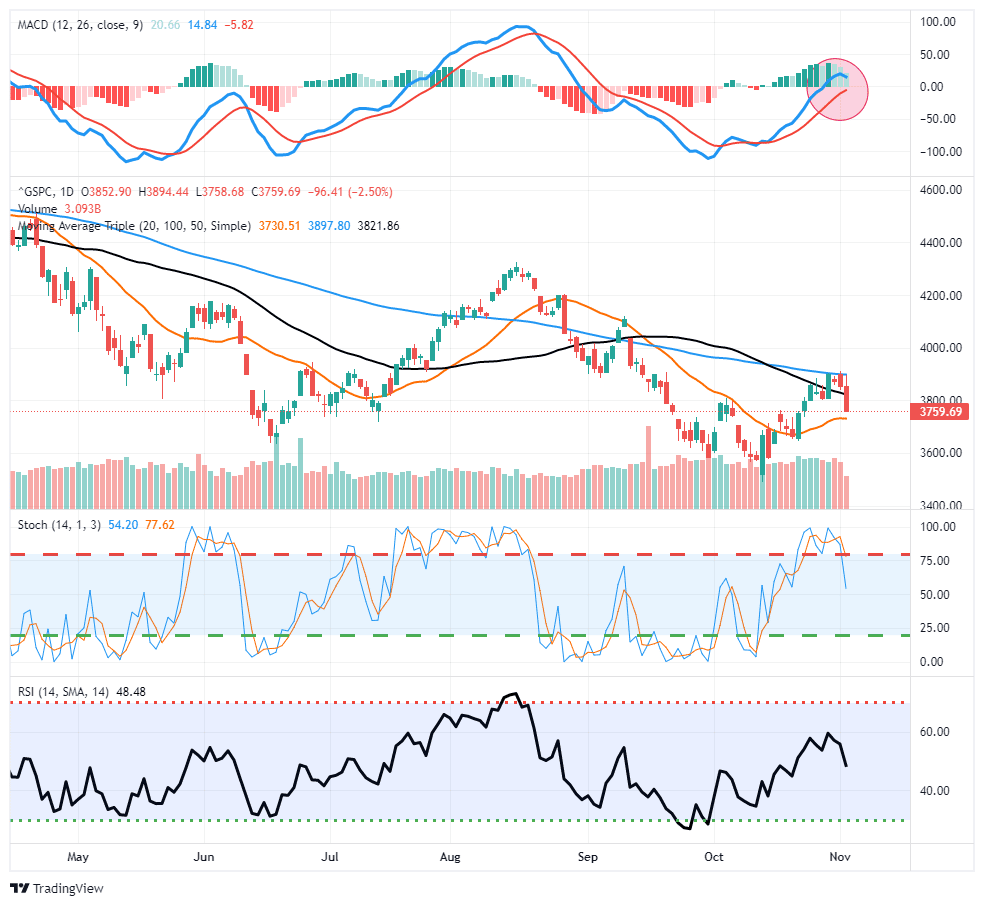

Market Trading Update

The market traded higher yesterday immediately after the FOMC rate announcement. However, it didn’t last long as “Super Hawk” Jerome Powell spoiled the party by stating the Fed had more work to do. To wit:

“The labor market continues to be out of balance, with demand substantially exceeding the supply of available workers” reinforces the notion that the Fed is looking at both employment and inflation as giving it plenty of reasons to keep tightening.“

He then reiterated previous comments that “at some point,” it will become “appropriate to slow the pace of increases.” The problem came as he most notably pointed out that there is “significant uncertainty” around that end-point which he indicated by stating, “we have some ways to go.”

However, just to make sure there were no questions about the Fed’s intentions, Powell said:

“The question of when to moderate the pace of increases is now much less important than the question of how high to raise rates and how long to keep monetary policy restrictive.”

That comment pushed terminal rate expectations above 5% and sank the market.

Yesterday’s sell-off took out important supports and pushed the market back below 3800. While there is some minor support at the closing levels, the main level to defend is the 20-dma which is just below the close. More importantly, short-term sell signals were triggered, and our primary MACD indicator turned lower. If that indicator triggers, such would indicate the current reflexive rally is over. The failure at the 100-dma is not a good position for the bulls and suggests the bears remain in control of the market for now.

A Path to a Pivot

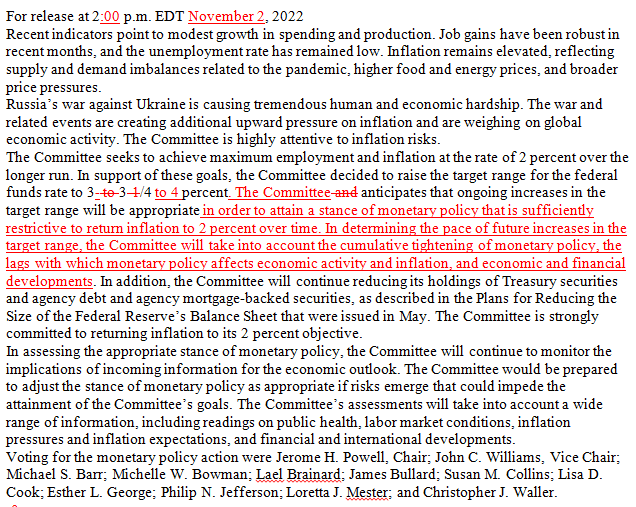

With Wednesday’s solid ADP employment report and Tuesday’s strong JOLTs data, the labor market is showing no signs of slowing down. Given the Fed’s concern that higher wages will keep prices higher for longer, the Fed is not relenting from its hawkish narrative. However, they are providing themselves an out, of-sorts. The following statement was added to the FOMC statement:

In determining the pace of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.

As the redlined statement shows, the only edits of note were the addition of this caveat of sorts.

The Fed is not pivoting, but they are telling us that stopping rate hikes at some will be appropriate due to the effects of “cumulative tightening” and “the lags with which monetary policy affects economic activity and inflation.” Equally important, they acknowledge that “financial developments” will also factor into policy decisions. Prior to the statement, the Fed seemed to ignore liquidity issues in the U.S. Treasury market and weaker stock prices. At some point, a crisis here or abroad may be cause for a Fed pivot.

In our opinion, the Fed is not breaking new ground. By default, with each rate hike, they are closer to the terminal rate. We also knew the Fed would come to the rescue if financial conditions worsened. Lastly, of course, a sharp slowdown in the economy which will drive inflation much lower, will get them to rethink policy.

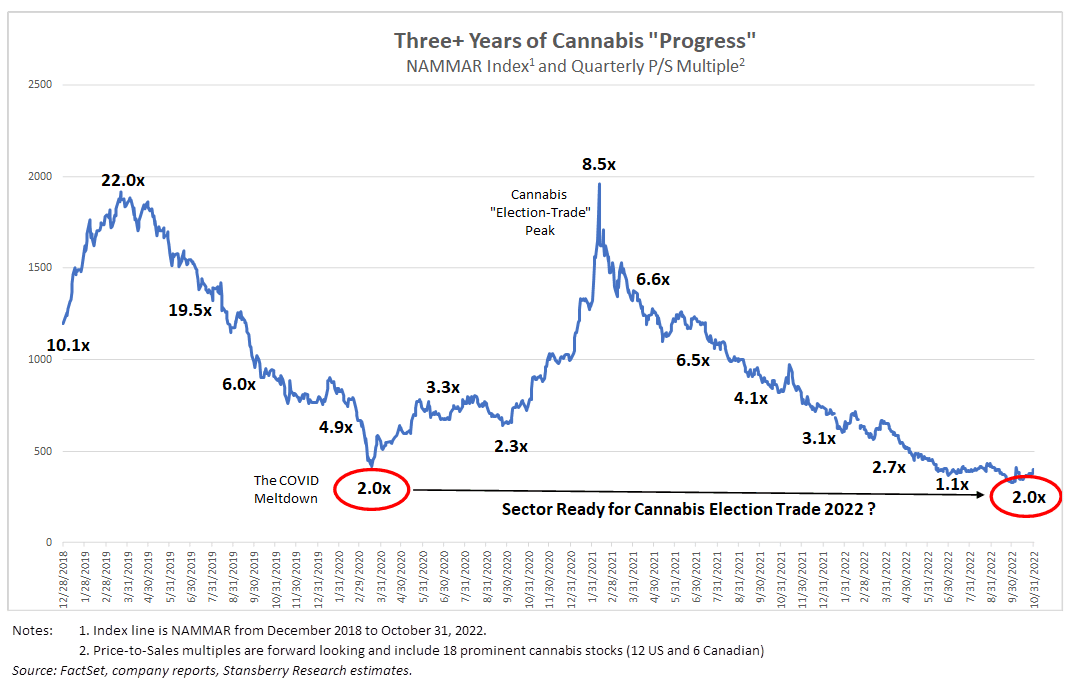

Alternative Idea- Cannabis Stocks

Biden recently took action to remove the Schedule I classification that Cannabis currently falls under. While his actions do not Federally legalize it, they make it much easier and more profitable to operate cannabis businesses. 37 states have legalized medical marijuana, and 19 have legalized the recreational use of marijuana. Further, 5 states are voting on recreational use at this year’s elections.

Despite the consistent progress toward legalization and increasing accessibility at the state level, cannabis companies and valuations have faltered. AdvisorShares Pure US Cannabis ETF- MSOS is down 80% since February 2021. The fund’s largest holding, Green Thumb Industries, is nearing five-year lows. The graph below shows that Price to Sales multiples for the industry is back to the lowest level in at least four years. With valuations relatively cheap and the rising odds for strong growth, Cannabis stocks may be a sector worth following.

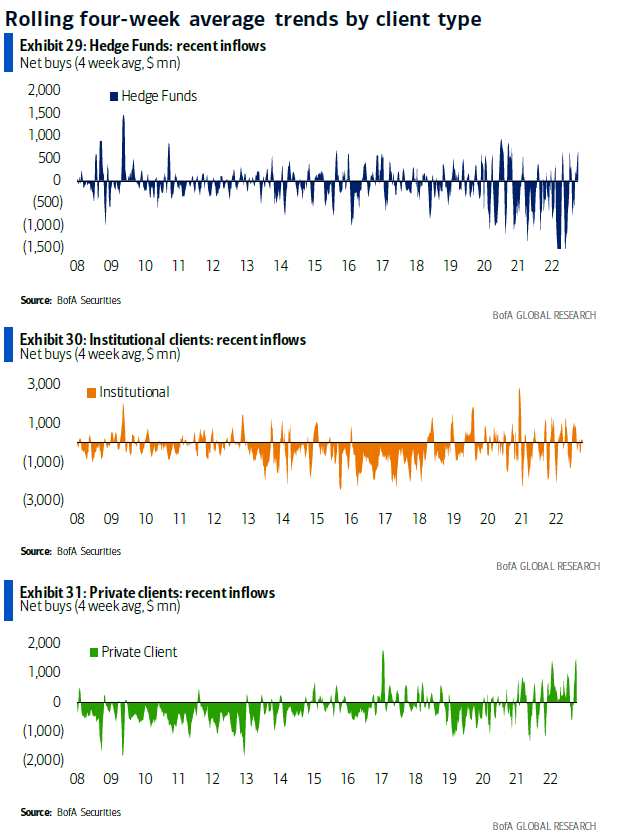

Who’s Buying and Who’s Selling?

The media often claims that either sellers or buyers drove the market’s direction. The truth is that every time a stock trades, there is a buyer and seller. By understanding that simple fact, we can gain an edge by distinguishing what type of investors are buying or selling.

It is often said retail investors are dumb money and institutional and hedge funds are smart money. The table below from AEI argues otherwise. Per AEI- “The S&P 500 Index Out-performed Hedge Funds over the Last 10 Years. And It Wasn’t Even Close!” Given the significant popularity of passive investment strategies that buy the major indexes, it’s fair to say a good number of retail accounts and 401ks have beaten hedge funds over the last decade.

The second graph highlights how retail and hedge fund investors are currently positioning themselves. As it shows, retail investors (private clients) have been buying throughout the year. Right now, they do not seem very smart. Our concern is that the traditional “smart money,” the hedge funds, which have been aggressively selling, are correct. That said, hedge funds have been buying recently, which may be a good sign if it continues. If retail becomes net sellers in 2023 and hedge funds large buyers, we may see active investment strategies beat out passive ones. Such would prove worrisome for the FAANG stocks and other mega-cap stocks. Small and mid caps, which are not well represented in passive funds, may outperform in such an environment.

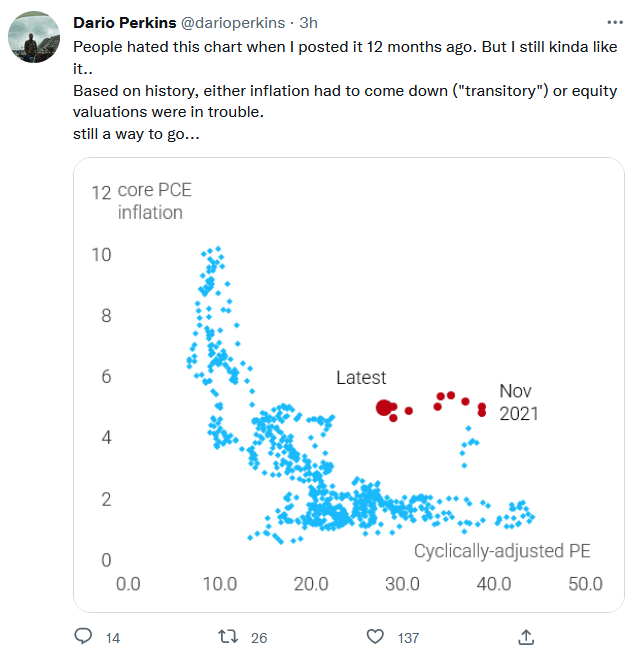

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read