Three months ago, Congress and the President avoided a shutdown and default on government debt when they agreed to increase the Treasury’s spending cap. Unbeknownst to many, another potential government shutdown may come in less than a month. Lawmakers need to agree on the fiscal budget for 2024, which starts on October 1, 2023. A government shutdown is not nearly as problematic as the debt ceiling. Unlike the debt ceiling, the Treasury can still issue debt, so a default is not in the cards. However, hundreds of thousands of federal workers could be temporarily suspended from their jobs without pay. Consequently, many government services, some of which are critical, could be shut down.

Currently, both parties are confident they will reach an agreement. To avoid a government shutdown, Congress needs to pass twelve appropriations bills. Each bill funds a different part of the government. Or, they can pass an omnibus deal combining the twelve bills into one. Recently, Congress has gone with the omnibus approach. While both parties are hopeful, there are significant differences in their preferred spending targets. Further complicating matters, a large group of Republicans were not happy with the debt ceiling deal and may use this opportunity to push for much more aggressive cuts. Heading into an election year, the Democrats are likely to fight cuts. In 2018, Donald Trump and the House-led Democrats could not agree on funding. As a result, they shut down the government for 34 days in 2018. Despite the government shutdown, the market rallied over 10% during the fiasco.

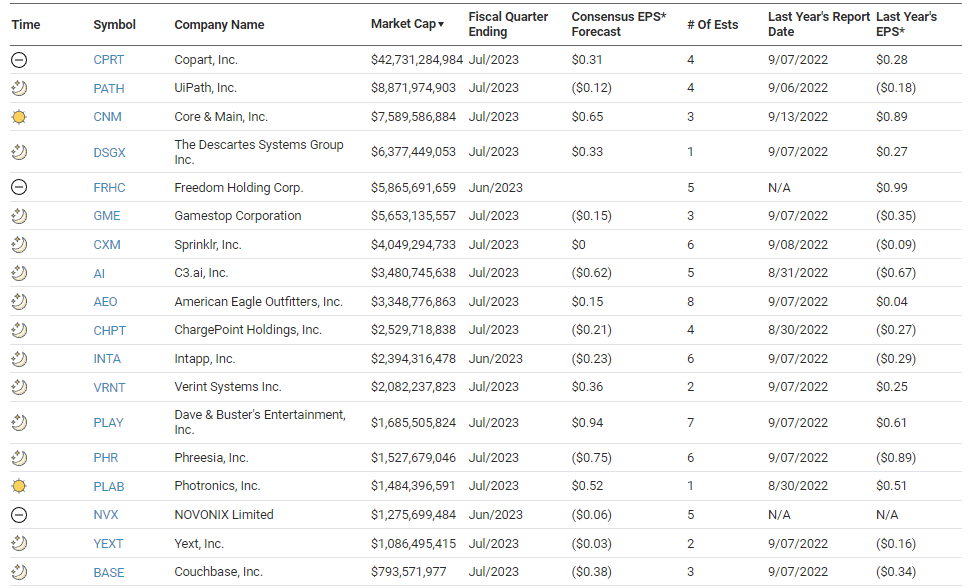

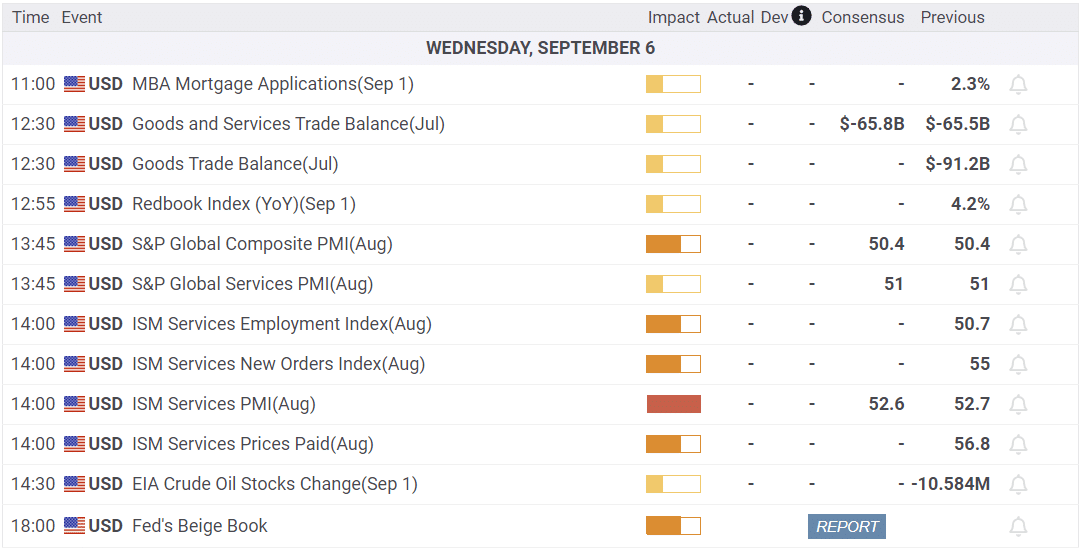

What To Watch Today

Earnings

Economy

Market Trading Update

Are oil prices about to go surging higher? It’s possible with the technical backdrop improving after the recent decline. However, oil prices are getting fairly extended in the short term, with more extreme overbought readings, so a pullback should be expected. However, with the MACD “buy signal” triggered, we could see higher prices heading into October. xl

However, energy stock prices, as represented by XLE, did not fall with the decline in oil prices. The divergence from the long-term historical correlation will likely be filled at some point.

For now, energy stocks are also extremely extended after the recent move higher, so a correction in those stocks should be expected when oil prices eventually revert. The trend and the overall backdrop remains positive for both oil and energy stocks near term, however, the onset of a recessionary environment will ultimately realign energy stock and oil prices.

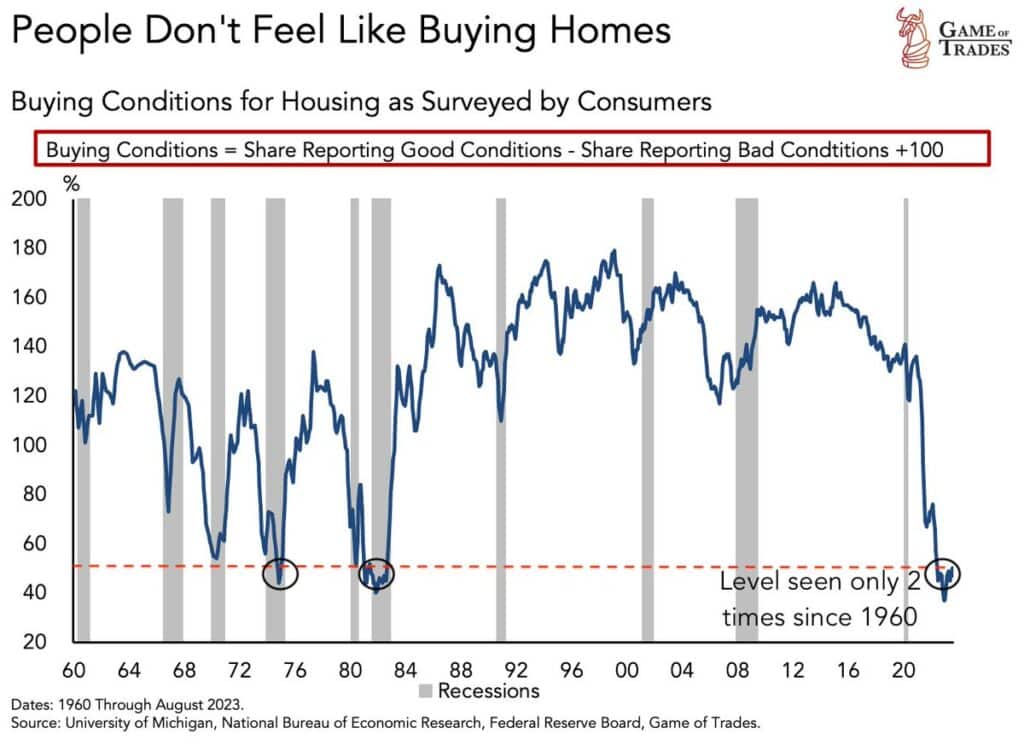

People Do Not Feel Like Buying Homes

As a result of house price inflation and the highest mortgage rates in 15-year highs, buying conditions for home buyers have deteriorated. Per the chart below, courtesy of Game of Trades, buying conditions are at levels only seen twice since 1960. While the existing home sale market is essentially frozen, as most buyers are unwilling to take on a high mortgage rate for a relatively expensive house, new home builders are doing well. For one, the inventory of new homes is comparatively robust versus existing homes. Second, and more importantly, new home builders can offer discounts in the form of lower mortgage rates. We suspect that as long as “people don’t feel like buying homes,” the homebuilders will continue to take an above-average percentage of total house sales.

Higher Crude Prices Dragging Bond Yields Higher

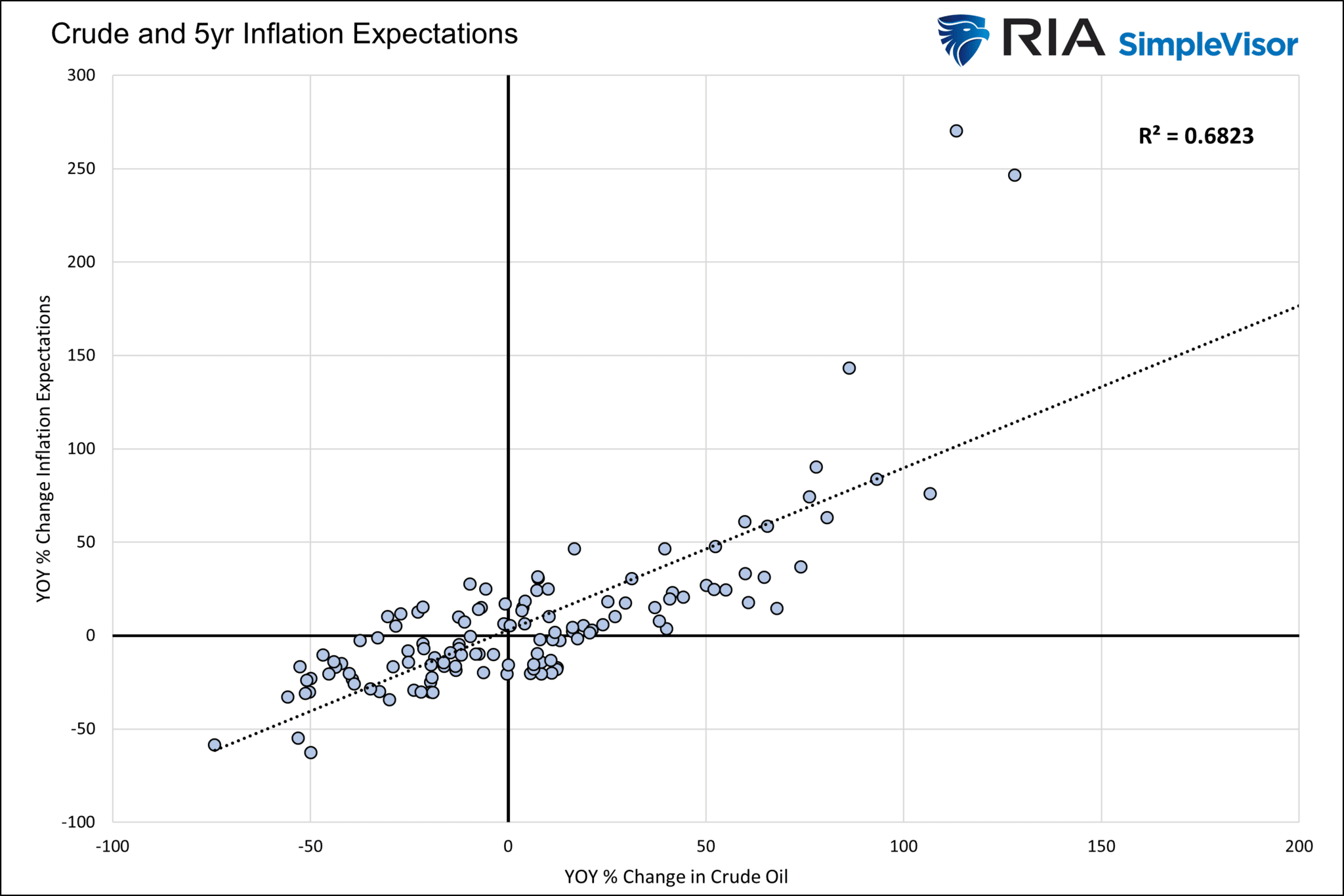

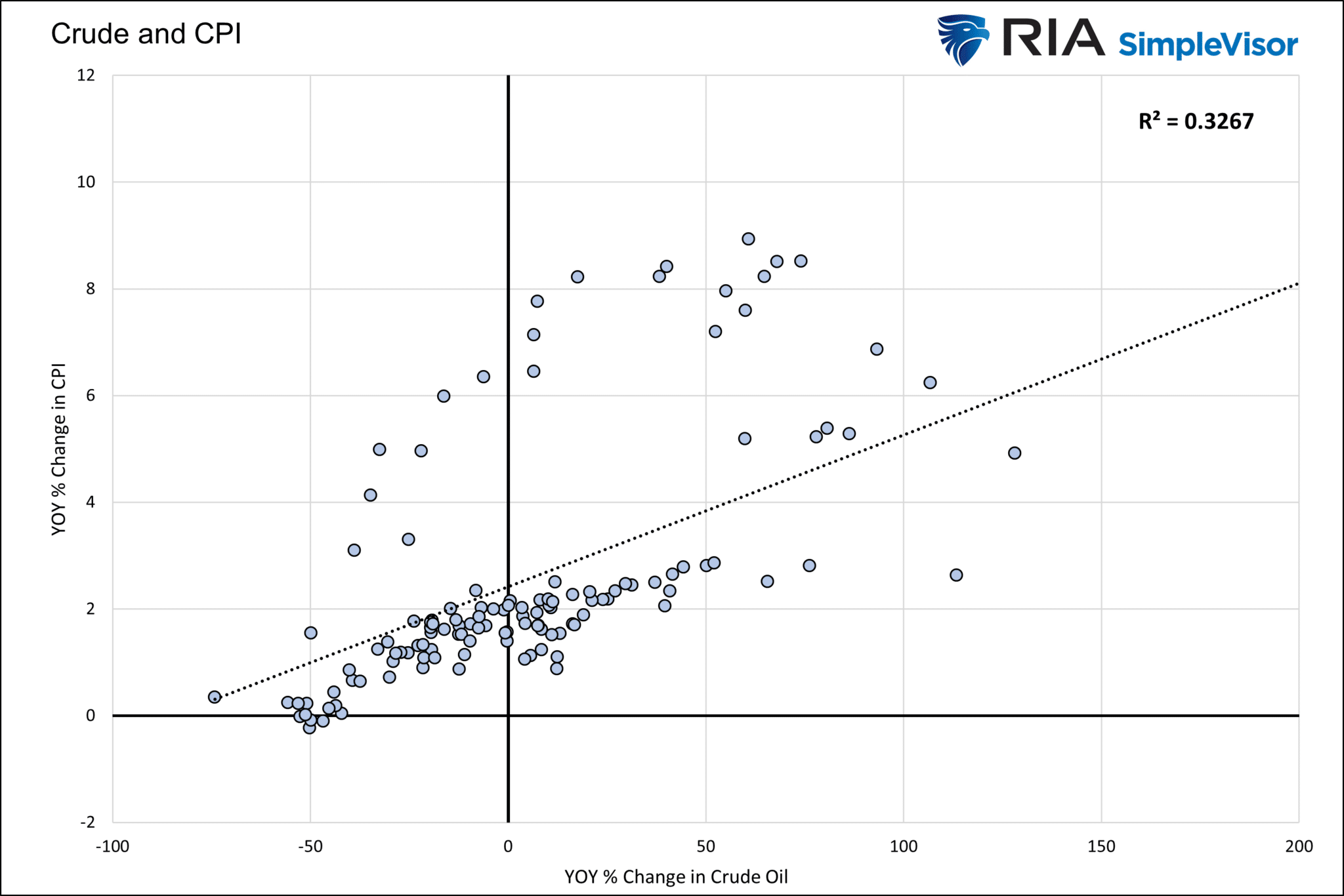

Since July, crude oil prices have risen from $70 a barrel to over $85. Prices at the pumps are now approaching $4 in many locations. At the same time, bond yields are rising as bond traders are concerned that higher oil and gas prices will generate more inflation. While such a correlation between crude and inflation expectations is the norm, the correlation between CPI and crude is less robust. As we show below, crude oil prices have much less of an impact on inflation than traders expect. That said, markets run on expectations, so higher crude may temporarily push yields higher.

The first graph below shows the strong relationship between crude oil and 5-year inflation expectations. The second graph shows the relationship is strong when inflation is low, but it vanishes when CPI is above the Fed’s 2% target, as we have today.

It’s worth adding the Fed prefers to gauge inflation with core measures that strip out food and energy prices. As such, the recent rise in crude prices may not overly concern the Fed as much as the bond market.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.