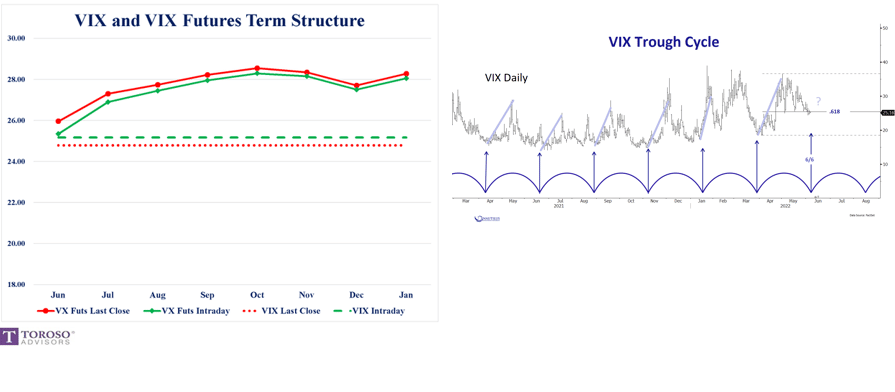

As measured by VIX, Volatility has been elevated throughout the current downward trend. Such is typical in bear markets. VIX measures the volatility or price movements implied by options on S&P 500 futures. Volatility is also a measure of liquidity. In Liquidity and Volatility- Decoding Market Jargon, we wrote: “More importantly, volatility is not just a mathematical calculation. Volatility measures liquidity! And liquidity defines risk.“

With that in mind, consider the two graphs below. The graph on the left shows that markets are currently implying that volatility will be higher in the future. Frequently, the curve is downward sloping, indicating less future risk. The graph on the right shows that VIX trading has formed a predictable cycle in which it peaks and troughs every 45 days. The cycle warns volatility will bottom shortly and start heading higher.

What To Watch Today

Economy

- 8:30 a.m. ET: Trade Balance, April (-$89.5 billion expected, $108.9 billion prior)

- 8:30 a.m. ET: Revisions: Trade Balance

- 3:00 p.m. ET: Consumer Credit, April ($35.000 billion expected, $52.435 billion prior)

Earnings

Pre-market

- JM Smucker Co (SJM) to report adjusted earnings of $1.85 on revenue of $1.98 billion

- Cracker Barrel (CBRL) to report adjusted earnings of $1.33 on revenue of $793. million

- Dave & Buster’s (PLAY) to report adjusted earnings of $1.17 on revenue of $445.33 million

Post-market

- No notable companies expected to report.

Market Goes Nowhere

The market went nowhere yesterday to speak of. The good news is that the market continues to hold its rally from last week. The bad news is that the longer the market takes to break above resistance there is an increasing likelihood of failure and a retest of lows. Remain cautious with exposures for the time being.

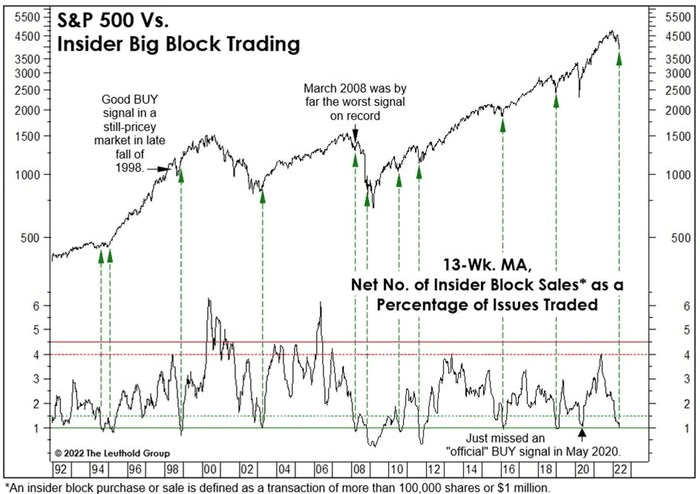

Corporate Insiders Signal the Potential for a Rally

The graph below from Callum Thomas shows the S&P 500 and an indicator of insider activity. It highlights the net number of insider sales as a percentage of volume has fallen to levels that were previously buying opportunities. If you notice, there was one time in the last 20 years the signal has failed investors. That occurrence was in March of 2008.

In a recent article, entitled Bear Stearns: A Lesson in Bear Market Bounces, we discussed the market in March 2008. as we wrote:

Wall Street was in the early rounds of a bout with unprecedented financial instability, and the economy would soon follow. Investors were relieved Bear Stearns avoided bankruptcy in spite of the ominous clouds on the horizon and recent financial instability. Within hours of the market opening following the Bear Stearns takeover, stocks started rising and didn’t look back for a month.

While the market didn’t regain its October 2007 peak, animal spirits were rekindled for a brief while.

The question facing investors today is whether insiders fully appreciate the underlying economic and Fed dynamics? Executives have been right many times and may very well be correct again. However, the Fed is rapidly removing liquidity despite signs of economic weakening.

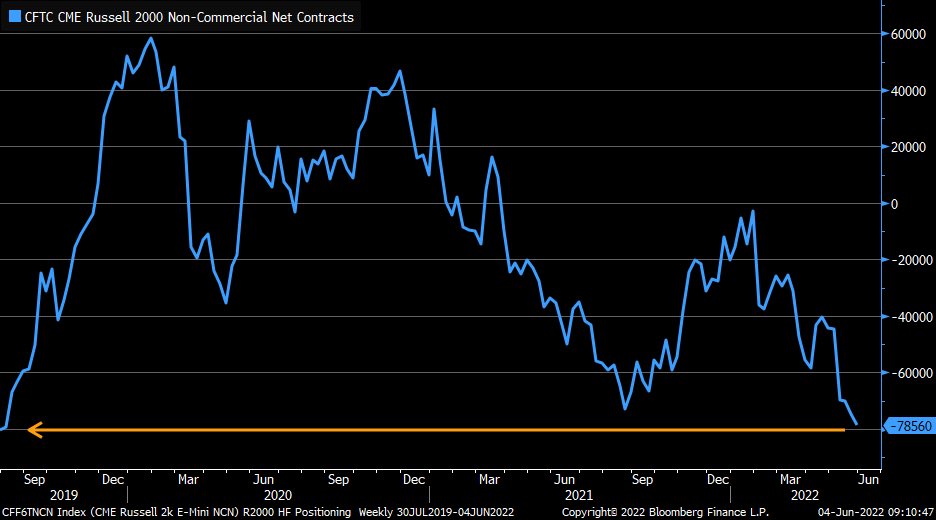

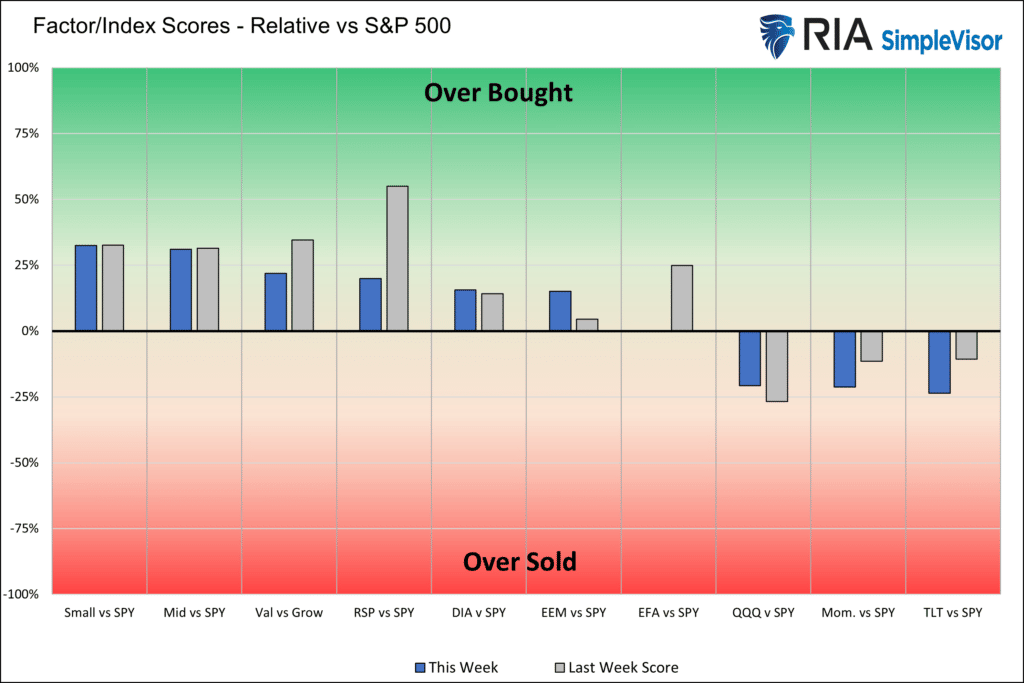

Are Small Caps Ready to Rally?

The graph below shows that professional traders are now as short the Russell 2000 futures contract as they have been in three years. Professional traders include many types of speculative investors, including hedge funds. The second graph below shows our proprietary model which measures the technical situation of various factors and indexes versus the S&P 500. As it shows, Small Cap and Mid Cap Stocks are the two most overbought sectors relative to the S&P 500. Their level of overboughtness is not extreme and could easily become more overbought. Short covering from speculative futures traders could spark such a rally.

Downgrade Cycles Take Time

“Mike Wilson highlights that US EPS revisions are now negative, but downgrade cycles take time. This time should be no different, which means stocks can hang around at current levels until 2Q earnings season when the next leg lower is likely to begin and end.” – TheMarketEar

“Over the past several months, we’ve been highlighting the declining trend in earnings revision breadth. We thought it would turn outright negative during Q1 earnings season and that’s where we are. However, it’s been a slow bleed toward 0%. This is why forward 12-month EPS estimates continue to grind higher for the S&P 500.” – Mike Wison

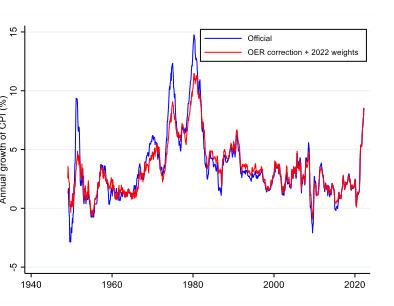

Inflation Today versus the 1970s/80s

Many, including ourselves, claim that official inflation figures are lower than what is occurring. Accordingly, the current bout of inflation may be on par with the 70s and 80s. One reason for our doubt is how the BLS treats rent and home prices. Housing constitutes about a third of CPI. Market measures of rents and home prices are up approximately 20% over the last year. Yet, the CPI-Shelter component is only up about 5%.

Lawrence Summers and others recently published a white paper. In it, they agree with us that inflation today and that of 40+ years ago may be more similar than CPI statistics show. However, Summers and co-authors take a different approach. They recalculate prior CPI data based on today’s methodology and weightings. The graph below shows their results. Looking at the two surges of inflation, we see the new estimates (red) are lower than previously thought and in line with current levels. The paper ends with two conclusions as follows:

- First, our observations imply that the current inflation regime is closer to that of the late 1970s than it may at first appear. In particular, the rate of CPI disinflation engineered in the Volcker-era is significantly less when measured using today’s treatment of housing. In order to return to 2 percent core CPI today, we need nearly the same five percentage points of disinflation that Volcker achieved.

- Second, our estimates suggest that past inflation cycles were more volatile than today’s due to the greater weight of transitory goods components in past indices.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.