“Liquidity” and “volatility” are constantly thrown around by the financial media and Wall Street as if everyone fully understands them and their importance. These terms are vital, but regrettably, not many investment professionals take the time to help investors fully appreciate them.

Mea culpa! We also use the terms extensively in our writings and podcasts, yet we fail to impress upon our followers their importance.

With volatility spiking and the Fed removing liquidity, we think it is an excellent time to discuss the two terms and their dependency on each other. We hope this broader understanding of volatility and liquidity may help you better appreciate risk conditions.

Liquidity

- “Fed Pumps $70.2 Billion in Short-Term Liquidity Into Markets.” – WSJ December 2019

- “Is this a Liquidity Crisis or a Solvency Crisis? It Matters to the Fed.” WSJ April 2020

- “Liquidity Shocks: Lessons Learned from the Global Financial Crisis.” NYT August 2021

Those headlines are just a few of the many ways the media use the word liquidity.

Liquidity is the fuel that keeps the financial market’s engine running. As such, without enough liquidity, the motor seizes, and financial crises erupt.

Liquidity refers to the amount of money investors are willing to use to buy and sell assets now. As you might surmise, the more investors willing to bid and offer assets, the more liquid the market. We cannot underline or highlight the word “AND” enough. Liquid markets must have both many willing bidders and offerors of an asset.

Let’s consider markets in which only one side of the market offered good liquidity.

In 2008, everyone was a seller of sub-prime mortgages, while buyers were few and far between. In late 2020 and early 2021, buyers of SPACs, meme stocks, cryptocurrencies, and an assortment of high-growth tech stocks dwarfed the number of sellers.

The 2008 example highlights a surplus of sellers with limited buyers. The more recent example is the opposite. In hindsight, we know how both illiquid conditions ultimately ended up. That is why it is vital for a liquid market to have ample buyers and sellers.

Liquidity is in the Eye of the Transactor

As we write this article, the price of Apple stock is 160.12. Currently, 350 shares are offered at 160.13, and 500 are bid at 160.11. Within five cents of the current price, well over 7,500 shares are bid and offered. Accordingly, for a retail investor looking to buy or sell 20 shares, the market for Apple is incredibly liquid. A 20-share transaction will occur at the market price and have no effect on the market.

Warren Buffett’s Berkshire Hathaway has approximately 1 billion shares of Apple. If Buffett has a hankering to sell even a small portion of his billion shares asap, he might have a different opinion of Apple’s liquidity.

The point of comparing these two opinions on liquidity is to stress the importance of assessing how current liquidity conditions affect your trading, but equally important to understand broader liquidity. The Warren Buffetts of the investment world dictates the price of Apple, not our 20-share trader! Therefore, if Mr. Buffett is desperate to sell, he will likely have to rely on bidders at lower prices. Then the amount of price concession is a function of how much liquidity exists.

Liquidity defines risk!

Volatility

Volatility is often quoted in two ways, realized and implied.

Realized, or historical, volatility is backward-looking. It is a statistical measure of an asset’s price movement over a prior period.

Implied volatility is derived from options prices. It is a measure of what investors think volatility will be in the future.

While calculated differently, the gauges quantify the movement of prices, past and expected. Further, and a story for another article, the difference between them can sometimes be telling.

More importantly, volatility is not just a mathematical calculation. Volatility measures liquidity! And liquidity defines risk.

Volatility Measures Liquidity

Liquidity is variable. Changes in sentiment or policies, for example, can quickly alter liquidity. When liquidity is high, many buyers and sellers are poised to act on prices at or very close to current market prices.

As we discussed in our earlier example, selling or buying 20 shares of Apple, even if done repeatedly, will have little to no effect on price. In such an environment, the price will move up and down as factors change, but the movement will be gradual.

Now consider a market in which each 20-share purchase of Apple moves the stock by a nickel or more. In this circumstance liquidity is weak, and prices are susceptible to a motivated buyer or seller. In such instances, daily price moves in Apple are much more elevated than in the liquid market example. Accordingly, Warren Buffett could easily introduce significant downside pressure in such a market.

This example shows how liquidity is the critical determinant of volatility.

Evidence

To help better cement the concept, we provide actual data.

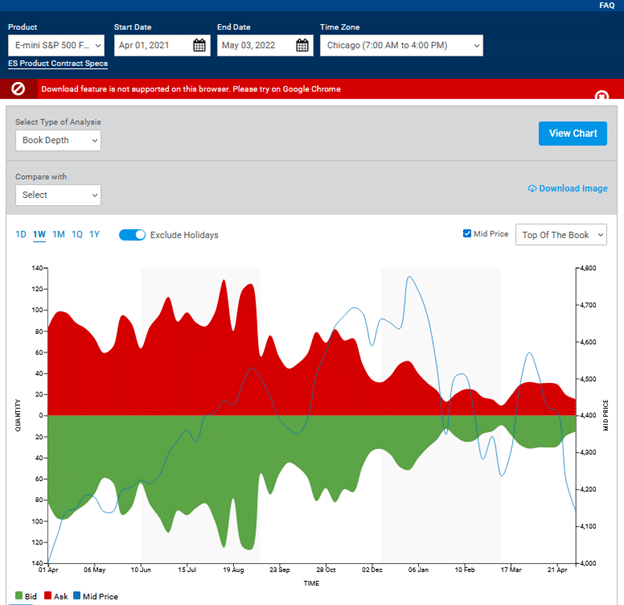

The graph below from the CME shows the S&P 500 E-mini futures contracts price (blue) and its book depth (red and green). Book depth measures how many bids and offers, on average, are available. As you see, when markets are rising, book depth is deeper. A deeper book implies investors are more comfortable, willing, and able to offer liquidity.

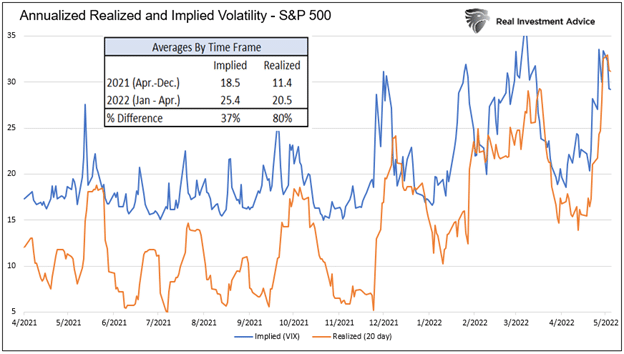

The second graph shows the bullish trend from April through December of 2021 had relatively low levels of realized and implied volatility. In January 2022, markets started falling, and liquidity gave way. During that period, book depth weakened, and the volatility readings rose.

Fed’s Liquidity Role

Liquidity comes from those investors that are willing and able to buy and sell. Therefore, sentiment, monetary and fiscal policy and a host of other factors affect the willingness and ability of investors. Over the past 20 years, the Fed has increasingly played a more prominent role in regulating liquidity.

The Federal Reserve does and doesn’t directly provide liquidity. As part of QE, the Fed purchases and sells bonds. In doing so, they add or remove securities available to markets. Removing assets increases liquidity as the amount of investable dollars chases fewer assets.

However, and equally important, is the Fed’s indirect influence on liquidity. This occurs via the perception that the Fed is adding or reducing liquidity and supporting or not supporting markets. Investors feel more comfortable knowing the Fed is adding liquidity. As we have repeatedly seen, Fed liquidity is an excellent backstop in many investors’ opinion. Conversely, as we see now, angst tends to occur when they remove liquidity.

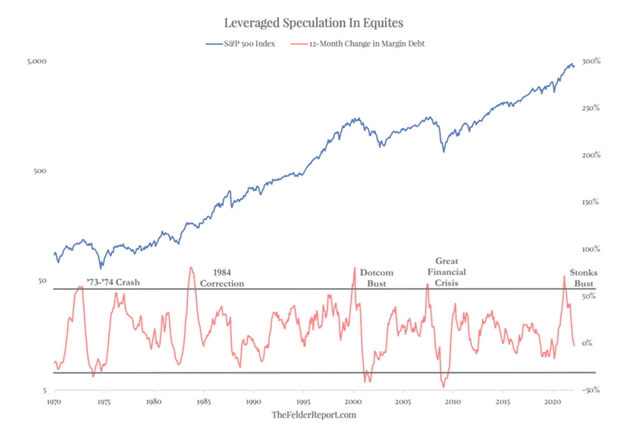

Raising and lowering interest rates is another way they affect liquidity. Trades using margin increase the purchasing power of buyers and sellers. Higher interest rates make it more costly to buy assets on margin and vice versa for lower rates. The graph below from Jesse Felder shows margin debt (leveraged speculation) tends to peak at market tops and troughs near market bottoms.

Lastly, the Fed regulates the banks. Accordingly, its rules and restrictions affect capital and collateral requirements, which directly influence the volume of financial market assets banks may own and or make loans against.

Summary- Don’t Fight The Fed

We often say, “don’t fight the Fed”. What we mean is that when the Fed is providing liquidity, do not fight them. It is likely the Fed’s liquidity will pacify investors and result in a less risky environment. Fed liquidity emboldens investors and adds liquidity, even when valuations are extreme.

Conversely and incredibly important today, when the Fed is removing liquidity, do not get in their way. Anxieties are increased, which results in reduced market depth and increased volatility.

There is no sign the Fed’s current quest to remove liquidity is close to ending. We recommend you carefully consider that liquidity is fading due to the Fed, and therefore, volatility is on the rise. Illiquid and volatile markets are not conducive to long-term wealth generation.