In the semi-annual Financial Stability Report, the Fed issued a stock market warning as elevated valuations are causing markets to be “vulnerable to significant declines”. To wit:

Prices of risky assets generally increased since the previous report, and, in some markets, prices are high compared with expected cash flows. House prices have increased rapidly since May, continuing to outstrip increases in rent. Nevertheless, despite rising housing valuations, little evidence exists of deteriorating credit standards or highly leveraged investment activity in the housing market. Asset prices remain vulnerable to significant declines should investor risk sentiment deteriorate, progress on containing the virus disappoint, or the economic recovery stall.

Is the Fed’s stock market warning justified?

The Fed is stating that valuations, as the prices of “risky” assets keep rising, make the stock market continually more vulnerable to a crash. It is the “stability/instability” paradox.

What could cause asset prices to crash? The Fed notes specifically:

- Another surge, or variant, of the COVID virus,

- A stalling of the economic recovery, or;

- Investor “risk-sentiment” deteriorates

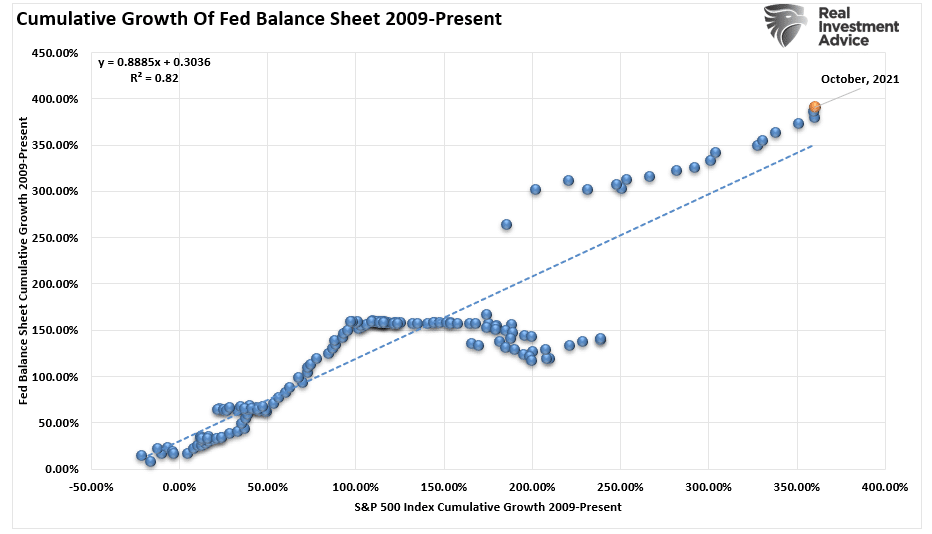

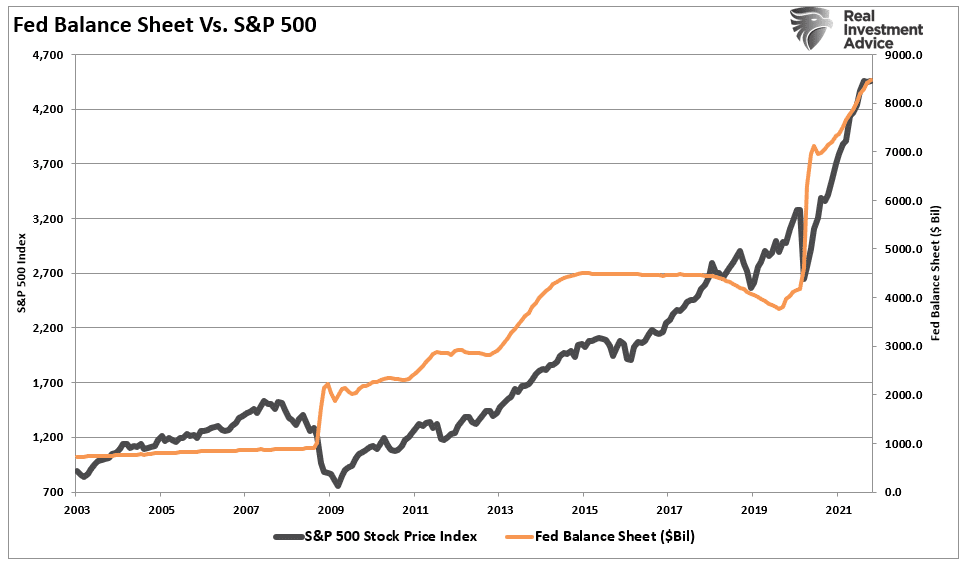

Given that Fed interventions boosted the stock market and “investor sentiment,” the withdrawal of that support could be problematic. As I discussed in “Bob Farrell’s Rules For A QE Market:”

“The high correlation between the financial markets and the Federal Reserve interventions is all you need to know to navigate the market.“

Those direct or psychological interventions are the basis for justifying all the speculative “risk” investors can muster.

Fed Driven “Irrational Exuberance”

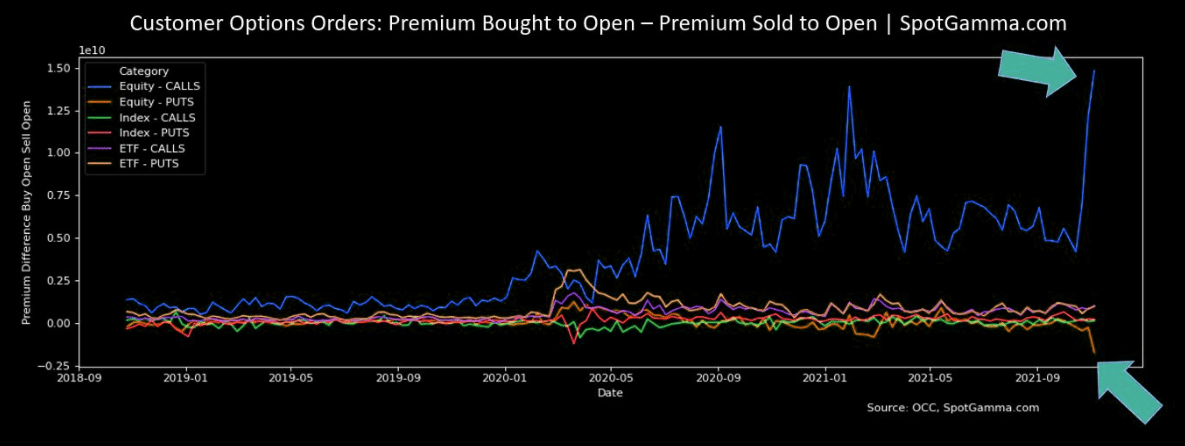

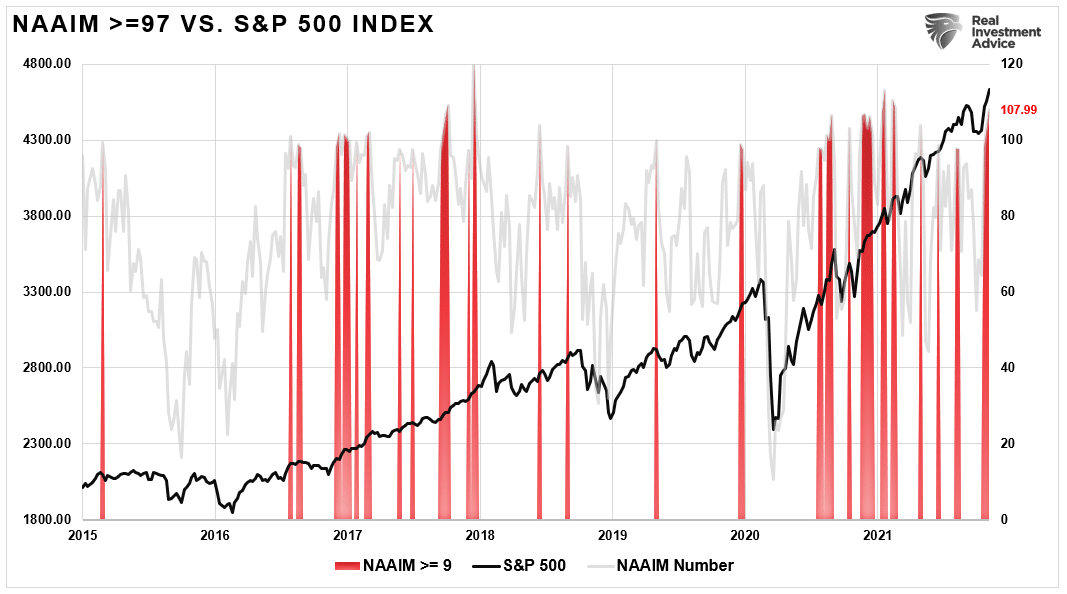

There is little doubt that “risky” assets are surging higher, driven by speculative investor confidence. That speculation appears throughout the market, from record call options to “meme” stocks surging in price.

But it’s not just the retail investor piling into stocks, but even professional managers are now “all in” the equity risk pool.

Of course, such speculative appetite is no surprise as the Fed’s monetary policy created the “Pavlovian” response to “risk-taking.” Or, more commonly known as:

“Don’t fight the Fed.”

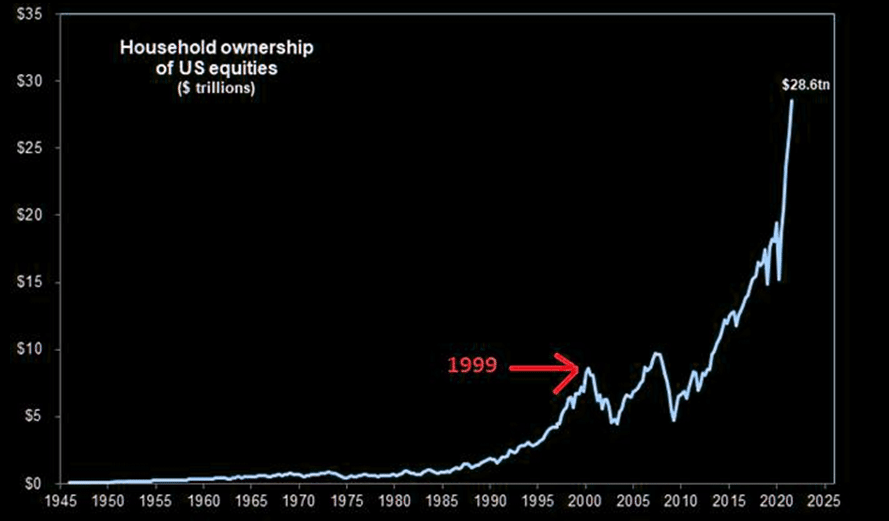

And “fight the Fed” retail investors did not. As shown below, household equity ownership is rocketing higher, towards $30 trillion.

Before you marvel at the feat of household equity ownership, you need to remember two crucial factors.

- The top 10% of income earners own 90% of those assets, and;

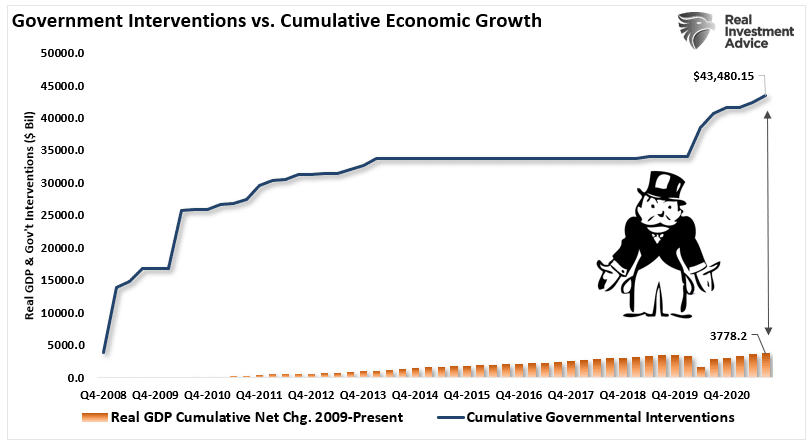

- It took $43.5 trillion dollars of liquidity to create that “wealth.”

Given the amount of “liquidity” thrown at the stock market, the Fed should take responsibility for investors’ “irrational exuberance.”

Valuations Are Extreme By Virtually Every Measure

“Across most asset classes, valuation measures are high relative to historical norms. Since the May 2021 Financial Stability Report, equity prices rose further.” – Federal Reserve

The description of valuations by the Fed is somewhat misleading. When saying something is high relative to historical norms, its meaning gets lost without some context. In this case, the context best comes from historical charts of various valuation measures.

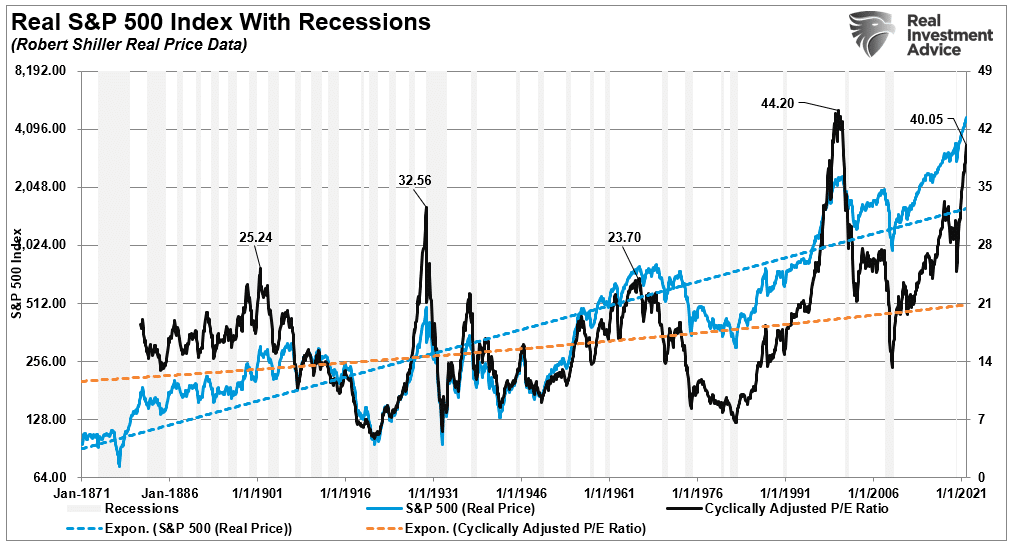

The most obvious is the Shiller CAPE ratio which takes current prices dividend by 10-years of earnings. This method smoothes out the volatility of earnings that can occur on an annual basis. At 40x trailing earnings, current valuations are higher at the peak of the market in 1999.

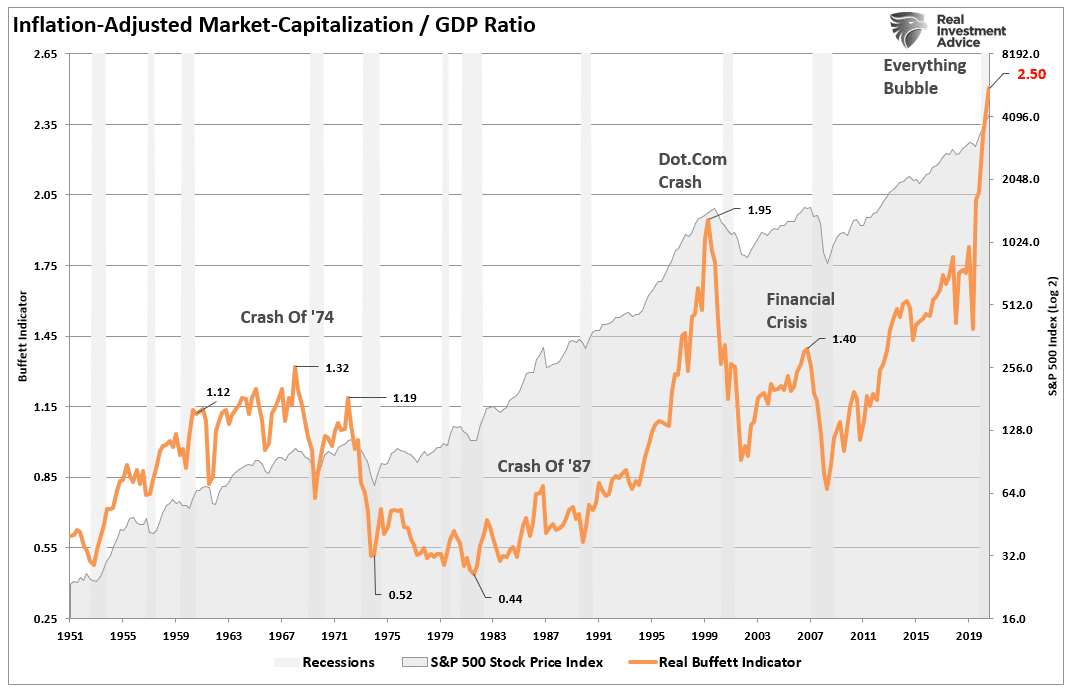

A look at market capitalization to the economy also gives you some sense of the “excess” in markets. Given that earnings and revenue come from economic activity, the market can not “outgrow” the economy long term.

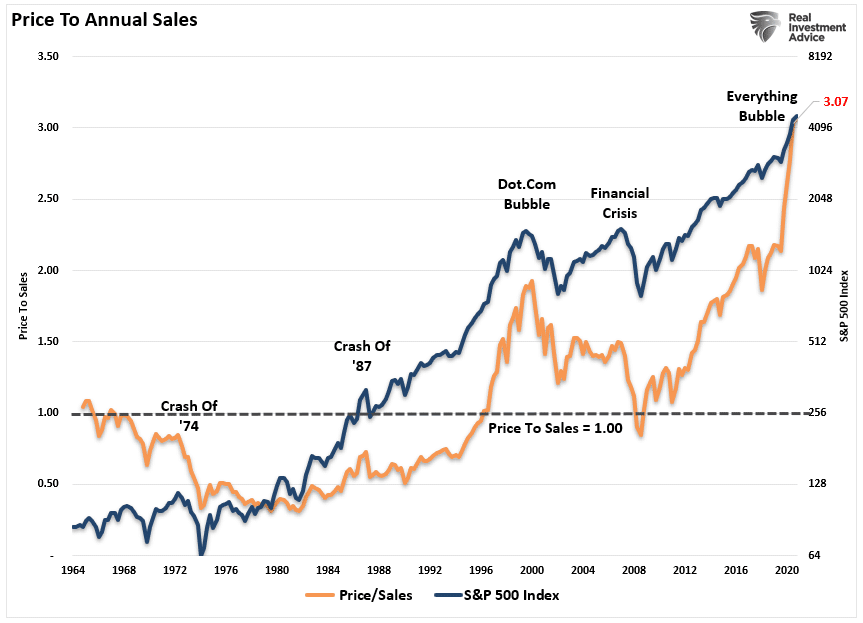

Lastly, price-to-sales (what happens at the top line of the income statement) is also exceedingly stretched.

While stock prices can advance, earnings are ultimately a function of economic growth and sales. Therefore, when excesses occur, an eventual reversion must, and will, occur.

The only question is the timing and the catalyst.

Hoping For A “Soft Landing”

In the Fed notes, valuations are elevated; in the stock market warning report, they identify several risks to the stock market.

The Fed report, highlighting the most salient risks that could undermine the financial system, flagged many previously stated concerns. Those included “structural vulnerabilities” in money market funds. “stable coins,” which the central bank now uses as a generic warning about risks associated with cryptocurrency adoption, inflation, and fading fiscal support.

But, as always, the Fed hopes they can orchestrate a “soft-landing” for the stock market.

Unfortunately, the Fed has a miserable track record of such outcomes.

Richard Thaler, the famous University of Chicago professor who won the Nobel Prize in economics, stated:

“We seem to be living in the riskiest moment of our lives, and yet the stock market seems to be napping. I admit to not understanding it.

I don’t know about you, but I’m nervous, and it seems like when investors are nervous, they’re prone to being spooked. Nothing seems to spook the market.”

Such is always the case, just before something does.

History Always Rhymes

While the Fed notes valuations are elevated, the crucial message to investors gets obfuscated. From current valuation levels, the expected rate of return for investors over the next decade will be low.

There is a large community of individuals who suggest differently. They rationalize a case this “bull market” can continue for years longer. But, unfortunately, any measure of valuation does not support that claim.

Such does not mean that markets will produce single-digit rates of return each year for the next decade. The reality is there will be some great years to get invested. Unfortunately, there will likely also be a couple of tough years in between.

That is the nature of investing. It is just part of the full-market cycle.

The economic cycle, demographics, debt, and deficit also suggest optimistic views are unlikely.

“History doesn’t repeat itself, but it often rhymes.” – Mark Twain

Unfortunately, despite the Fed’s stock market warning, the market will ultimately deal with “irrational exuberance,” just as it has done every time previously.