Valuations & Full Market Cycles

In this past weekend’s missive, “Visualizing 10-Reasons For Caution,” I presented a chart heavy analysis of why the current market is likely due for at least a short-term correction.

There is little doubt currently “exuberance” is running high following the election of Donald Trump. The hopes for stimulus, tax reform, and repatriation has “hope” springing that job and economic growth will follow. The problem, as I have discussed previously, is this optimism comes at a point in history diametrically opposed to when President Reagan instituted many of the same conservative policies.

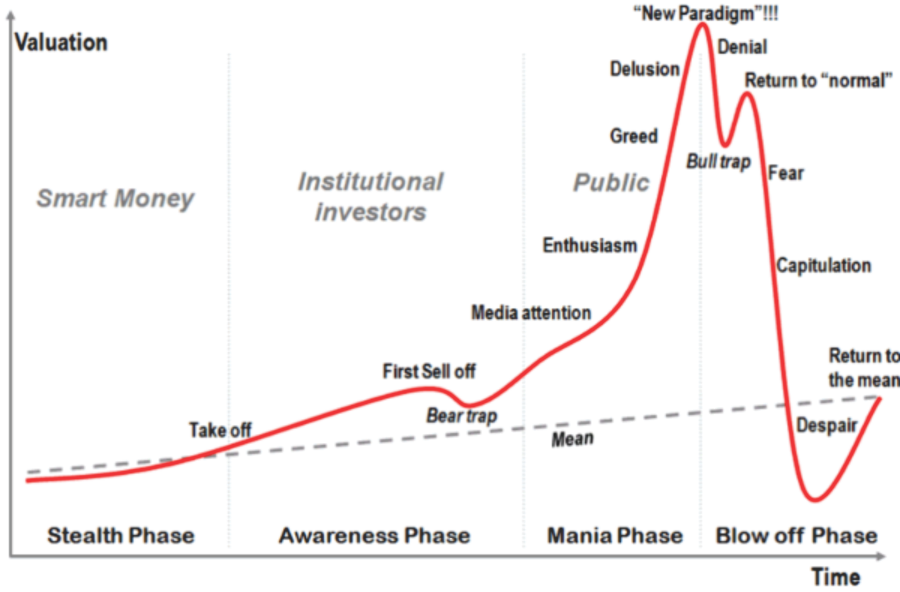

It is this exuberance that reminded me of the following “investor psychology” chart.

This chart is not new, and there are many variations similar to it, but the importance should not be lost on individuals as it is repeated throughout history. At each delusional peak, it was always uttered, in some shape, form or variation, “this time is different.”

Of course, to the detriment of those who fell prey to that belief, it was not.

As I was studying the chart, something struck me.

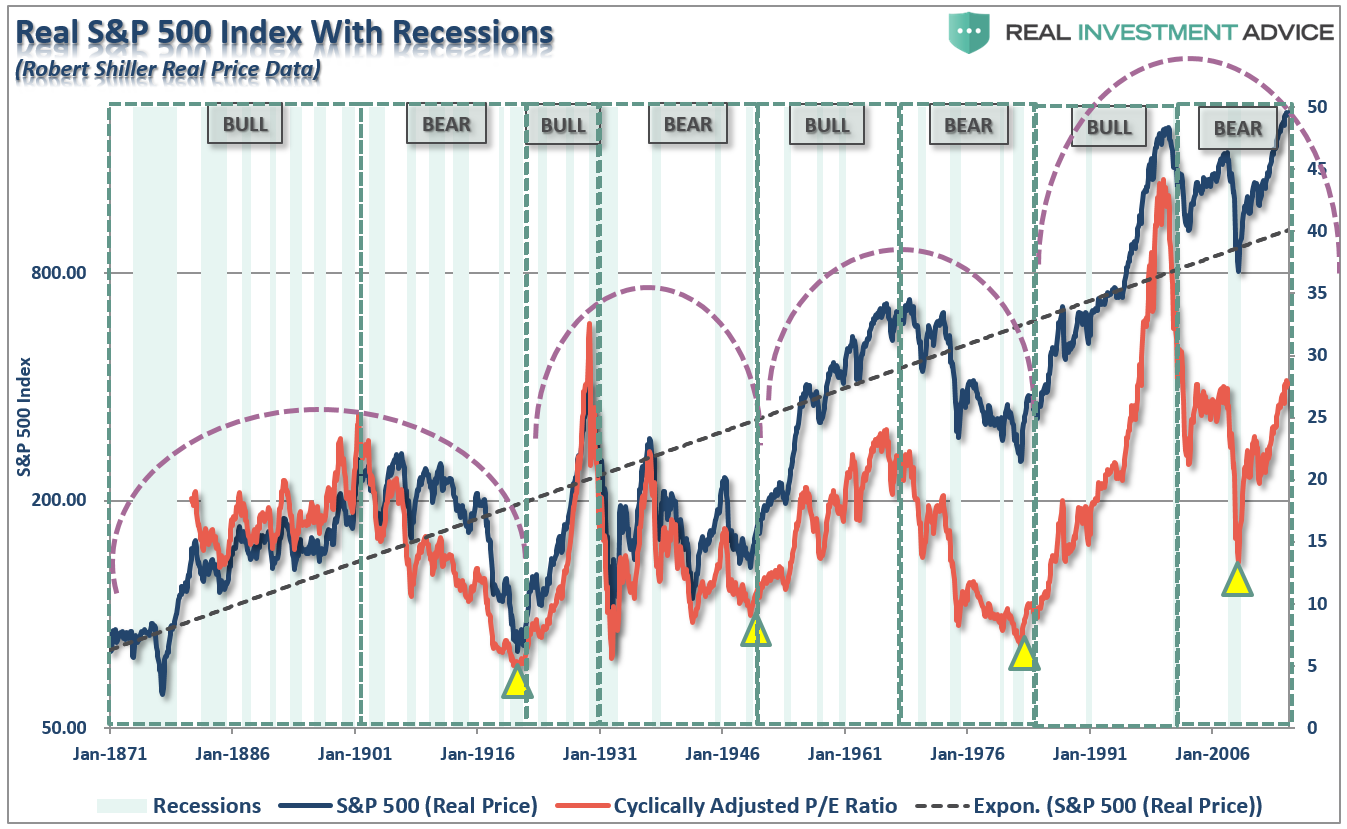

During my history of blogging and writing newsletters, I have often discussed the importance of full-market cycles.

“Long-term investment success depends more on the WHEN you start investing. This is clearly shown in the chart below of long-term secular full-market cycles.”

“Here is the critical point. The MAJORITY of the returns from investing came in just 4 of the 8 major market cycles since 1871. Every other period yielded a return that actually lost out to inflation during that time frame.”

By looking at each full-cycle period as two parts, bull and bear, I missed the importance of the “psychology” driven by the entirety of the cycle.

In other words, what if instead of there being 8-cycles, we look at them as only three?

This would, of course, suggest that based on the “psychological” cycle of the market, the bull market that began in 1980 is not yet complete.

Notice in the chart above the CAPE (cyclically adjusted P/E ratio) reverted well below the long-term in both prior full-market cycles. While valuations did, very briefly, dip below the long-term trend in 2008-2009, they have not reverted to levels either low or long enough to form the fundamental and psychological underpinnings seen at the beginning of the last two full-market cycles.

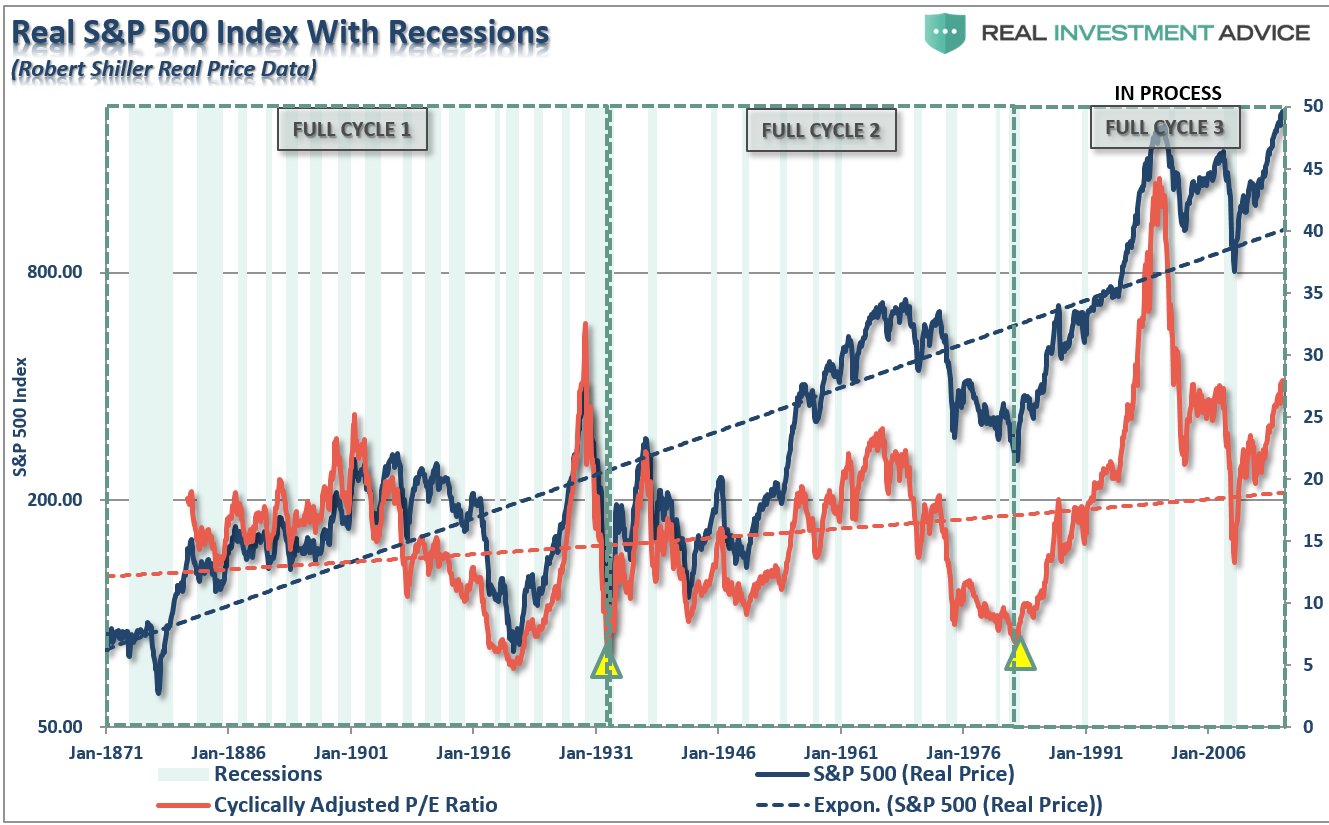

What If The 80’s Secular Bull Is Still Running?

It is from that basis, and historical time frames, that I have created the following thought experiment of examining the psychological cycle overlaid on each of the three full-cycle periods in the market.

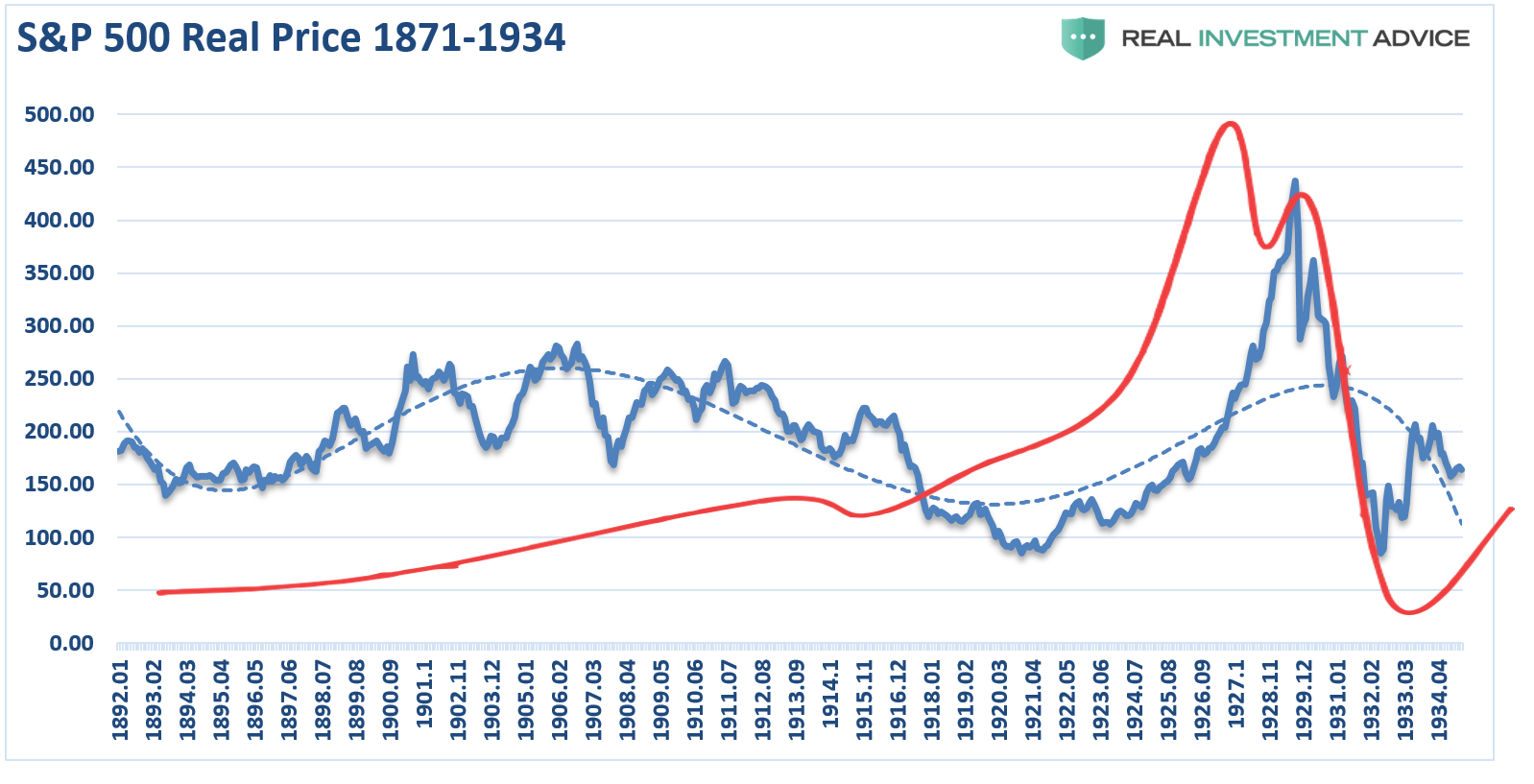

The first full-market cycle lasted 63-years from 1871 through 1934. This period ended with the crash of 1929 and the beginning of the “Great Depression.”

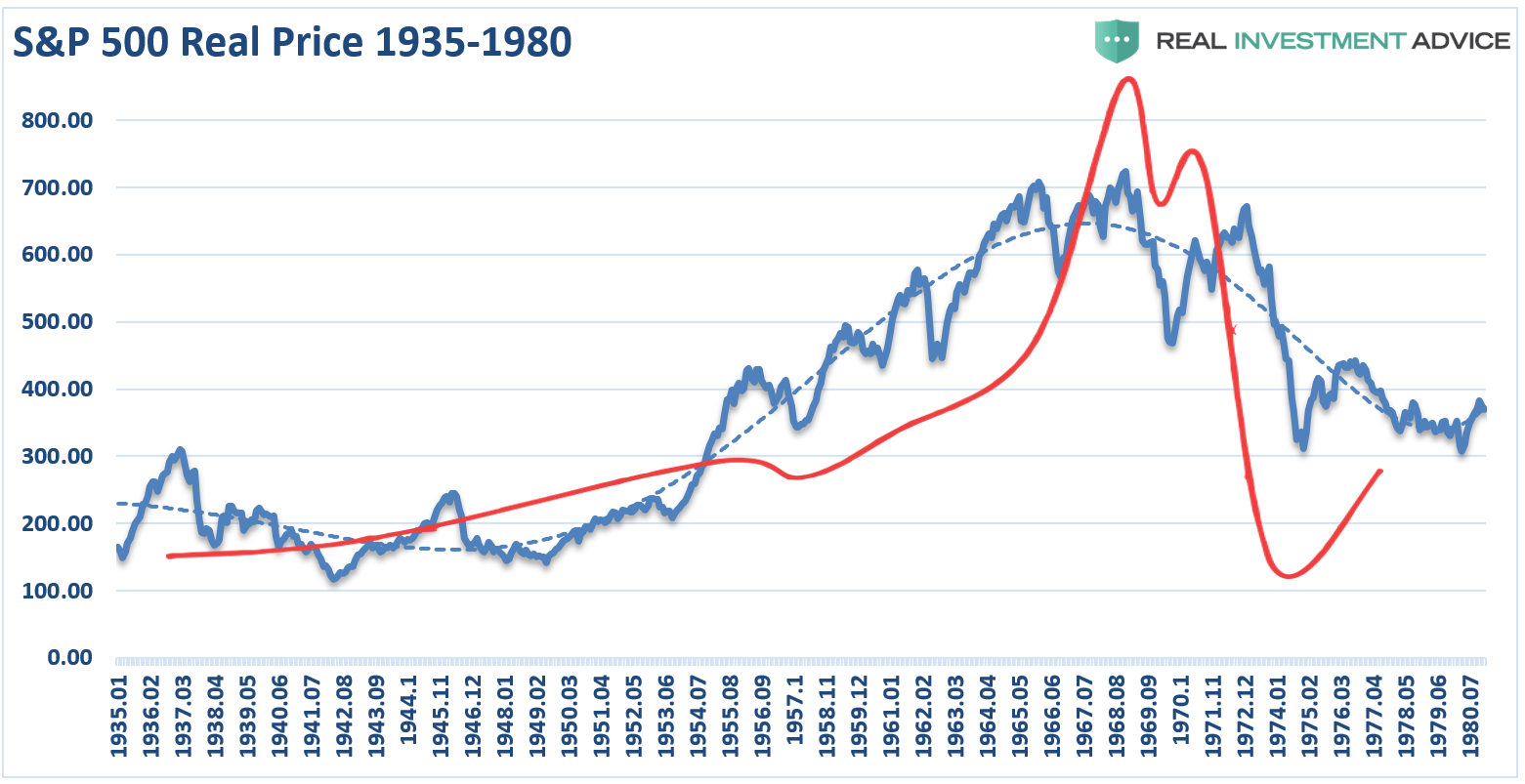

The second full-market cycle lasted 45-years from 1935-1980. This cycle ended with the demise of the “Nifty-Fifty” stocks and the “Black Bear Market” of 1974. While not as economically devastating to the overall economy as the 1929-crash, it did greatly impair the investment psychology of those in the market.

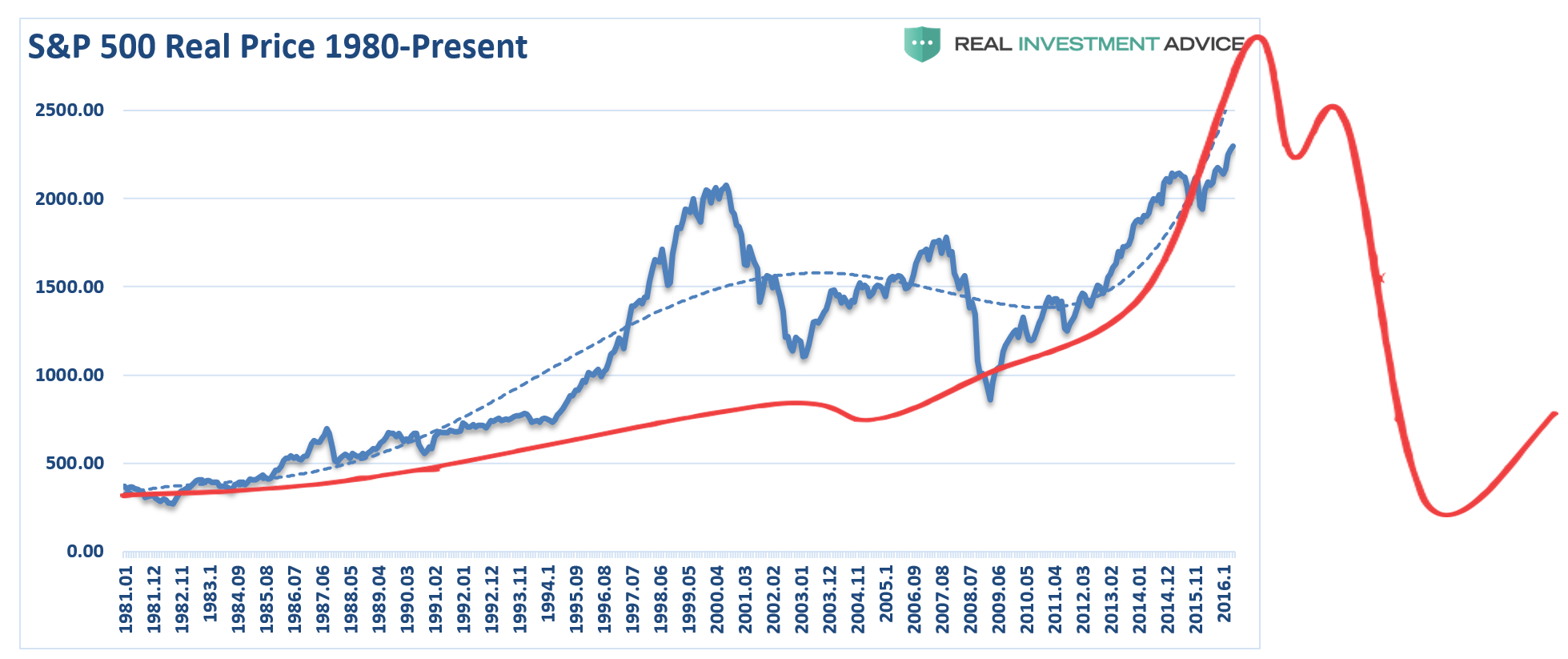

The current full-market cycle is only 37-years in the making. Given the 2nd highest valuation levels in history, corporate, consumer and margin debt near historical highs, and average economic growth rates running at historical lows, it is worth questioning whether the current full-market cycle has been completed or not.

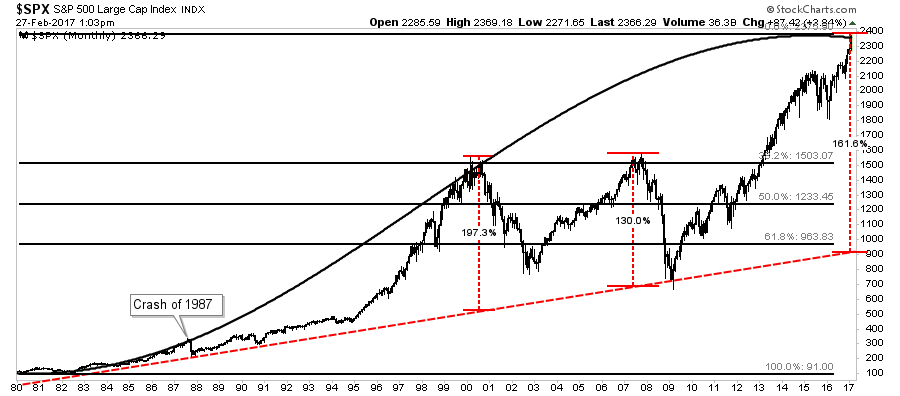

The idea the “bull market” which begin in 1980 is still intact is not a new one. As shown below a chart of the market from 1980 to present, suggests the same.

The long-term bullish trend line remains and the cycle-oscillator is only half-way through a long-term cycle. Furthermore, on a Fibonacci-retracement basis, a 61.8% retracement would current intersect with the long-term bullish trend-line around 1000 suggesting the next downturn could indeed be a nasty one. But again, this is only based on the assumption the long-term full market cycle has not been completed as of yet.

I am NOT suggesting this is the case. This is just a thought-experiment about the potential outcome from the collision of weak economics, high levels of debt, and valuations and “irrational exuberance.”

Yes, this time could entirely be different.

It just never has been before.

Indexing Realities

Daniel Drew had a very interesting post this past week discussing the realities of indexing. To wit:

“Warren Buffett released his annual letter over the weekend, in which he praised Jack Bogle as his ‘hero’ for promoting index investing. The irony is that investors would have been better off buying Berkshire shares. Over the last 10 years, Berkshire stock is up 139% while the S&P 500 is up 71%.

Buffett is doing something every skilled salesman does: managing expectations. Buffett’s own performance is compared against the S&P 500, and what better way to win that game than by putting a floor under the Berkshire price with the promise of share buybacks and then putting a ceiling on the stock by promoting index investing? The real secret is Buffett is talking his book by not talking it: Rather than tell investors to buy Berkshire at any price, he tells people to invest passively through an index, which leads to the very market inefficiencies that he profits from.

The great appeal of index investing is its low fees, but like buying a cheap pair of shoes that falls apart after 6 months, investors will find that index investing is the most expensive thing they ever did.

Vanguard promotes its rock-bottom expense ratios, but what is not published is market impact costs that are incurred when the fund rebalances. Since these rebalances are often announced ahead of time, they are extremely vulnerable to front running. Christophe Bernard, Ph.D. Senior Scientist at Winton Capital Management, estimates that front running costs index investors 0.20% per year. That’s 4 times the official expense ratio of Vanguard’s S&P 500 ETF.

In his latest research, finance professor Hendrik Bessembinder discovered that 58% of stocks don’t even outperform a Treasury bill. This study was based on 26,000 stocks from 1926 to 2015. Just 4% of stocks accounted for all of the $31.8 trillion in gains during this period. That means 96% of stocks were complete garbage. Even worse, shares of unprofitable companies outperform their profitable counterparts, which is why you have a marketplace that is dominated by Twitters and Teslas.

Index investing means buying a box of garbage stocks sprinkled with a few hope and glamor stocks whose price gains are solely a result of underperforming fund managers grasping for quarterly bonuses and retail investors juicing up their portfolios in a doomed attempt to catch up on their retirement targets.

While mom and pop buy a Vanguard index with their $500,000 and get front run all day by proprietary traders, the capitalist televangelist Warren Buffett will continue to actively trade billions while preaching the miracle of buy and hold investing.”

Just something to think about.

Also Read