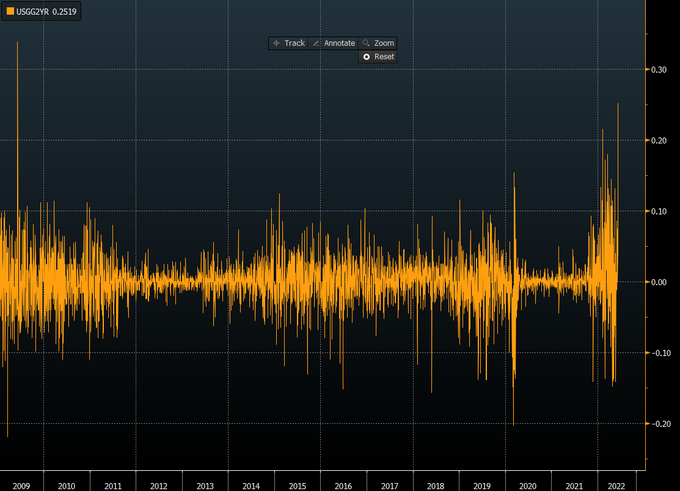

The graph below shows that 2yr Treasury yields rose 0.25% on Friday, the largest one-day change since 2009. On May 31, 2022, the 2yr Treasury yield was 2.54. Today the 2yr Treasury yield is approaching 3.35%. The bond market, especially the shorter maturities, is increasingly concerned that the Fed may raise rates by .75bps at tomorrow’s meeting and/or the one in July. Last Friday’s CPI report appears to be responsible for this disorderly sell-off.

For a brief moment on Monday morning, the 2yr Treasury yield curve was flat. Since then, it steepened but remains close to inverting. As we have noted, a yield curve inversion typically precedes a recession. However, the recession starts after the curve steepens out of an inverted state.

What To Watch Today

Economy

- NFIB Small Business Optimism, May (93.0 expected, 93.2 during prior month)

- PPI final demand, month-over-month, May (0.8% expected, 0.5% during prior month)

- PPI final demand, year-over-year, May (10.8% expected, 11.0% during prior month)

Earnings

Pre-market

- Core & Main (CNM) to report adjusted earnings of 35 cents on revenue of $1.38 billion

Post-market

- Sprinklr (CXM) to report adjusted losses of 6 cents on revenue of $141.00 million

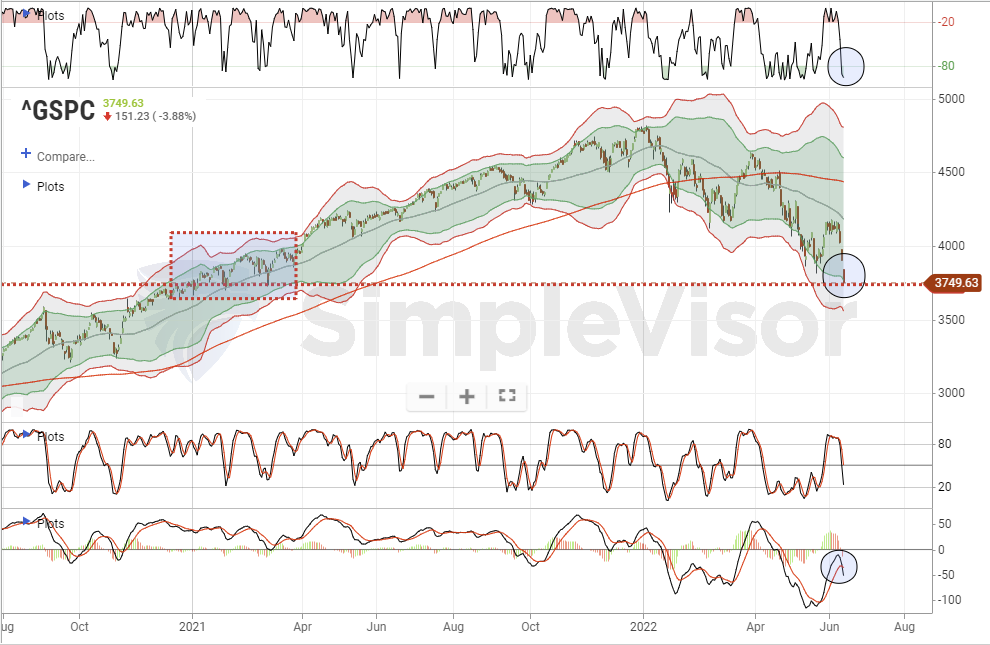

Market Tanks As Support Is Taken Out

The market tanked yesterday as the 2yr Treasury Yield soared spooking markets the Fed might be even more aggressive on Wednesday and hike 0.75%. More on that next. Technically, the market broke previous support lows and collapsed back to the previous market bottoms in early 2021 erasing the entirety of last year’s gains. With the market back on a MACD sell signal, there is a risk of more downward pressure. However, with the market short-term oversold and more than 2-standard deviations below the 50 dma, a bounce following the Fed meeting will not be surprising.

We will look to use bounces to add to our short-position further and reduce additional equity risk as needed.

Fed Meeting On Wednesday – .50% or 0.75% Bps?

“A string of troubling inflation reports in recent days is likely to lead Federal Reserve officials to consider surprising markets with a larger-than-expected 0.75-percentage-point interest rate increase at their meeting this week.

Before officials began their pre-meeting quiet period on June 4, they had signaled they were prepared to raise interest rates by a half percentage point this week and again at their meeting in July. But they also had said their outlook depended on the economy evolving as they expected. Last week’s inflation report from the Labor Department showed a bigger jump in prices in May than officials had anticipated.

Two consumer surveys have also shown households’ expectations of future inflation have increased in recent days. That data could alarm Fed officials because they believe such expectations can be self-fulfilling.” – Nick Timiraos

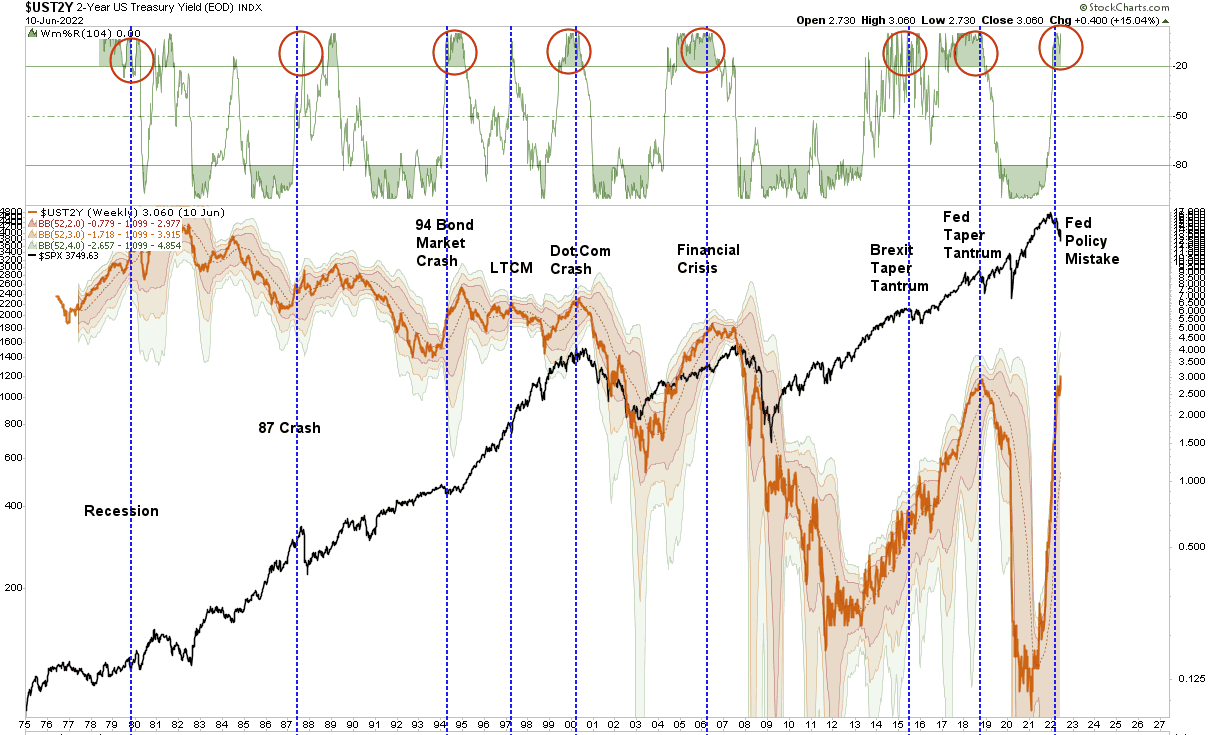

That potential for a 0.75% hike sent the 2yr Treasury Yields surging, nearly inverted the yield curve, and then crushed the long-end.

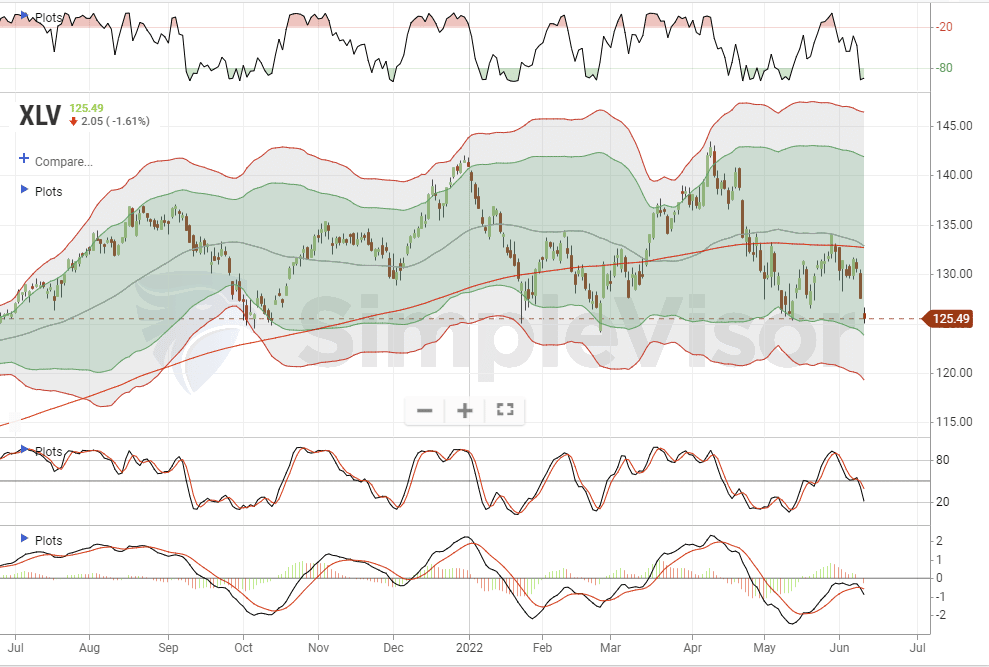

Healthcare on Critical Support

The graph and commentary below come from a feature we do in SimpleVisor every Monday. Yesterday’s Market Sector Buy-Sell Review shows that XLV (healthcare) is sitting on critical support. Many other sectors have similar-looking graphs and, as such, are in similar predicaments. Per the commentary:

- So goes the economy, so goes transportation. As the economy is showing signs of slowing, Transportation has come under pressure, adding to downward pressure from a declining 50-dma.

- Currently, the sell signal has triggered and is adding to the downward pressure. (bottom panel)

- Transportation is approaching oversold on a short-term basis. (top panel)

- Short-Term Positioning: Bearish

- Sell current positions on any rally to $75-78

- Stop-loss is currently broken.

- Long-Term Positioning: Bearish

Financial Instability

Price stability and maximum sustainable employment are the Federal Reserve’s Congressionally chartered dual mandates. These objectives are supposed to dictate monetary policy and the Fed’s longer-run goals and strategies. Recent experiences, however, assert that financial instability trumps Congress’s mandates. Given that inflation is surging and the unemployment rate is below average, will financial instability cause the Fed to reverse its hawkish tone?

The graph below says not yet. The orange line shows that IEI, the 3-7 year UST ETF, has fallen almost 10% since the start of the year. Over this period, the 5-year yield has risen from .75% to nearly 3.25%. Typically such a sharp increase in yields would trouble the credit markets. The graph below shows that is not the case. The ratio of the price of JNK to LQD (junk to investment-grade corporate bonds) has been relatively stable. In fact, JNK has slightly outperformed over the last few days despite yields rising appreciably. This one measure of financial stability shows no signs of problems.

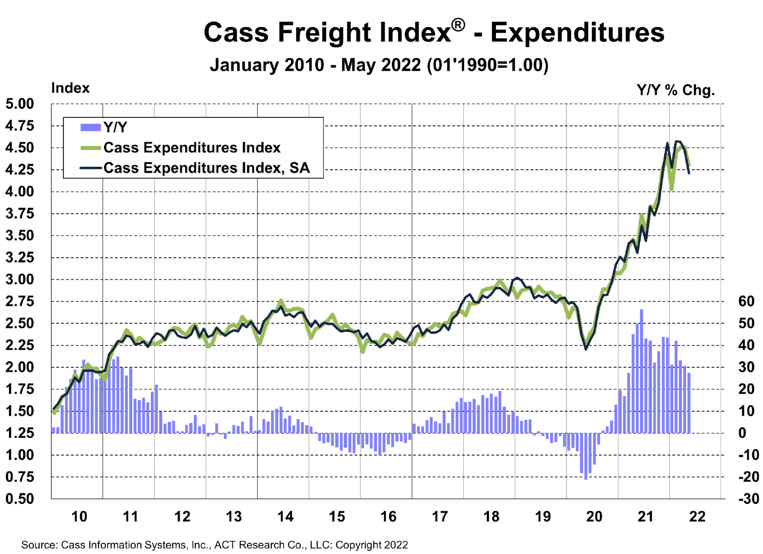

Cass Uses The “D” Word

Cass Systems helps companies manage freight/logistic expenses. They also put out a well-followed index on global freight costs. Per Cass, the demand-supply imbalance over the last year has resulted in soaring shipping costs, as we share below. This may be coming to an end, and per Cass, deflation in shipping costs is coming.

After nearly a two-year cycle of surging freight volumes, two key drivers of growth for the freight cycle– goods consumption and inventory restocking are faltering. Combined with a major improvement in driver availability (27,300 new jobs added in the past two months), all signs continue to point to a change in the trajectory of (shipping) rates in the coming months.

While this is welcome news on the inflation front, it does point to much slower economic growth ahead.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read