The Fed’s two-day policy meeting kicks off this morning with expectations of a 75bps Fed Funds rate hike and a slight chance of 100bps. Currently, the odds of a 100bps rate hike stand at 20%. While inflation has stabilized, it is not coming down as quickly as the Fed was forecasting when they started fighting inflation earlier this year. Jerome Powell was incredibly hawkish at Jackson Hole. Raising by 100bps would further affirm Powell’s rhetoric and the Fed’s determination to beat inflation before it becomes persistent.

The graph below shows that October Fed Funds futures imply Fed Funds of 3.13% (100-96.87). Currently, Fed Funds are trading around 2.33%. A 75bps rate increase would bring it to 3.08%. Therefore, the market implies an additional 5bps. 5/25ths equates to a 20% chance of 100bps on Wednesday.

What To Watch Today

Economy

- 8:30 a.m. ET: Building permits, August (1.610 million expected, 1.674 million prior)

- 8:30 a.m. ET: Building permits, month-over-month, August (-4.8% expected, -1.3% prior)

- 8:30 a.m. ET: Housing Starts, August (1.445 million expected, 1.446 prior)

- 8:30 a.m. ET: Housing Starts, month-over-month, August (0.3% expected, -9.6% prior)

Earnings

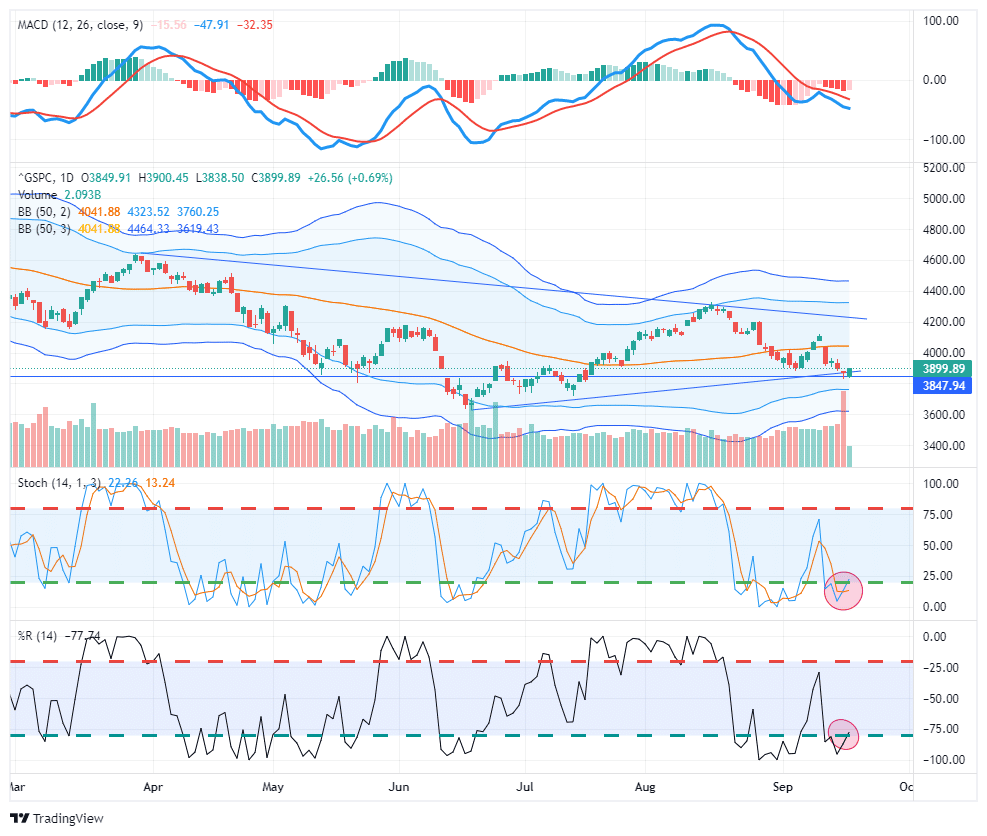

Market Trading Update

As noted in yesterday’s commentary:

“If you want to call it that, the good news is that Friday, which was options expiration, saw a massive surge in volume, suggesting a temporary low. The market also held vital support at the May lows (dotted red line). With the market oversold on a short-term basis, a reflexive rally next week is likely.”

Two pieces of positive action in yesterday’s reflex rally. First, the market bounced off that important support level from the May lows. Secondly, as shown, the market triggered a short-term Stochastics and Williams %R “buy signal.” While the market rally yesterday was weak, the market could have a bit more upside near term. We continue to suggest using any rally toward the 50-dma as an opportunity to reduce portfolio risk for now.

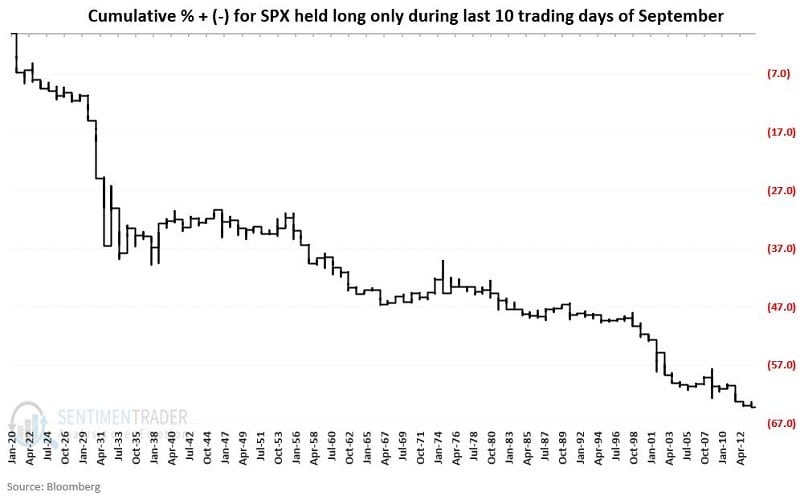

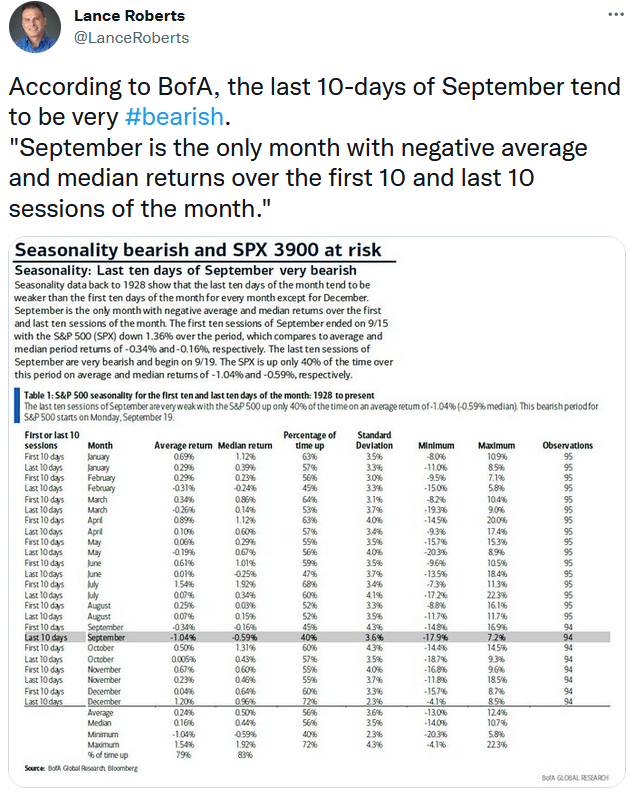

The Last Part Of September Sucks

While discussing the potential for a reflexive rally, it is worth noting that the last part of September tends to “suck” from a return perspective. This note from Sentiment Trader makes an excellent point:

“It is a mistake to assume that the stock market will decline simply because the calendar reads September. However, long-term results suggest that caution is clearly in order during September – particularly when we get to the last ten trading days of the month. For 2022, this particularly unfavorable period extends from the close on 2022-09-16 through the close on 2022-09-30.”

See more in my Tweet below on September stats.

The good news is that October begins the seasonally strong period of the year. So, hopefully, we will have some better trading days ahead.

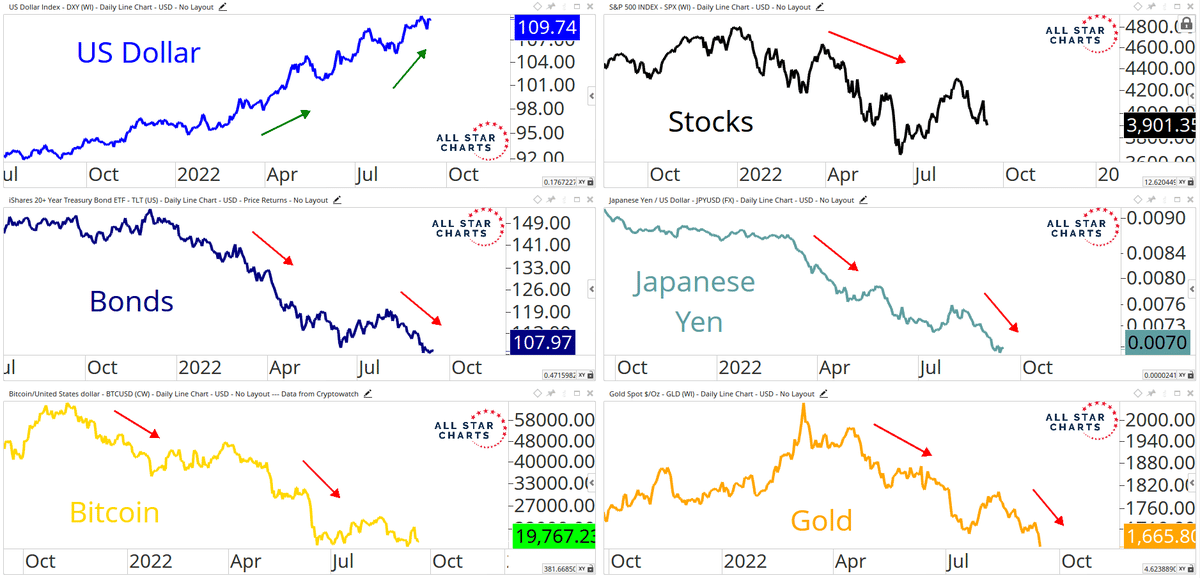

Don’t Fight The Trend

1. The Trend is Your Friend?

They say “don’t fight the Fed,” but another key market aphorism is **don’t fight the trend** (which is kind of in many ways driven by the Fed). But either way, as the chart shows, there are clear trends at play across assets as the liquidity tides go out and the cycle progresses…

The comment comes from Callum Thomas and is accompanied by the graph below. Regardless of asset class, one of the most critical market indicators today is the dollar. As we discuss in the next section, when will the world’s central banks say enough is enough regarding recent dollar strength? When or if they take forceful action to stop the dollar, the world’s risk markets may get a little relief.

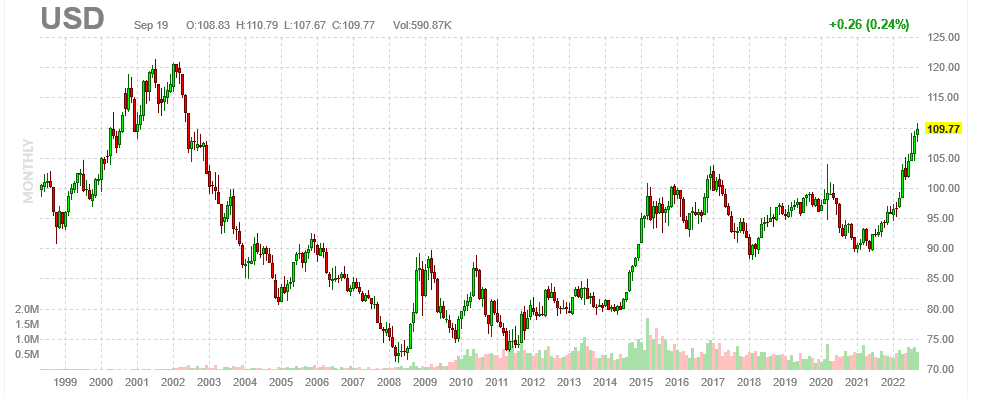

Currency Intervention

DOLLAR’S STRENGTH COULD INDUCE MORE COUNTRIES TO INTERVENE IN CURRENCY MARKETS- BIS.

The following headline scrolled across the screens on Monday. Remember that the BIS is often referred to as the “central banker’s bank.” They are a powerful player coordinating central bankers’ actions and policies. Its warning is likely a foreshadowing of aggressive actions soon to occur. In Yields Are Defying Yesterday’s Logic, we noted the likelihood of currency intervention. To wit:

Given soaring inflation rates, especially energy prices, this instance of a stronger dollar is wreaking havoc on Europe and Japan.

Making matters worse, many foreign borrowers borrow in dollars. If they don’t hedge the currency risk, as many do not, a strong dollar results in higher interest and principal payments. Simply, they must acquire more expensive dollars to pay interest and principal. As such, a strong dollar is a de facto tightening of global monetary policy.

Europe is doing everything possible to solve its energy crisis, but its options are limited as it is primarily a supply problem. While alleviating supply challenges is difficult, they can reduce the cost with a stronger currency.

We suspect that the ECB and BOJ have been selling dollar assets, predominately Treasury bonds, to prop up their currencies.

Amazon versus FedEx

On Monday, we commented on FedEx’s poor earnings and forward guidance. Ourselves and others warned that what ills FedEx is problematic as they are representative of the broad economy. We still think FedEx and its competitors are well correlated with economic activity. However, some of FedEx’s problems may also be market share related. Amazon is now a larger carrier than FedEx and closing in on UPS.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read