S&P 500 futures are currently down 25 points in the overnight session and crude oil is over 3% lower at $63. 10-year UST yields are about 4bps lower at 1.23%. Other than the Fed minutes from yesterday there is little new news to blame for the sharp moves last night.

The Fed shed little new light in the July FOMC minutes in regards to the schedule and pace of Fed taper. While some Fed members seem eager to start tapering as soon as September, others voiced concern about downward inflation pressure and how the market may perceive tapering. We look to the Jackson Hole Fed conference late next week for more guidance.

Highlights from the Fed minutes from the July 28th FOMC meeting:

- “Most participants noted that, provided that the economy were to evolve broadly as they anticipated, they judged that it could be appropriate to start reducing the pace of asset purchases this year.”

- “They are worried that accelerating plans to wind down the asset purchases could lead investors to question whether the Fed is in a hurry to raise rates or less committed to achieving lower unemployment.”

- SOME PARTICIPANTS REMAINED CONCERNED ABOUT THE MEDIUM-TERM INFLATION FORECAST AND THE PROSPECT OF MAJOR DOWNWARD PRESSURE ON INFLATION RESURFACING.

- “Several others indicated, however, that a reduction in the pace of asset purchases was more likely to become appropriate early next year”

- “Most participants remarked that they saw benefits in reducing the pace of net purchases of Treasury securities and agency MBS proportionally in order to end both sets of purchases at the same time.”

- “The staff provided an update on its assessments of the stability of the financial system and, on balance, characterized the financial vulnerabilities of the U.S. financial system as notable. The staff judged that asset valuation pressures were elevated. In particular, the forward price-to-earnings ratio for the S&P 500 index stood at the upper end of its historical distribution; high-yield corporate bond spreads tightened further and were near the low end of their historical range; and house prices continued to increase rapidly, leaving valuation measures stretched.”

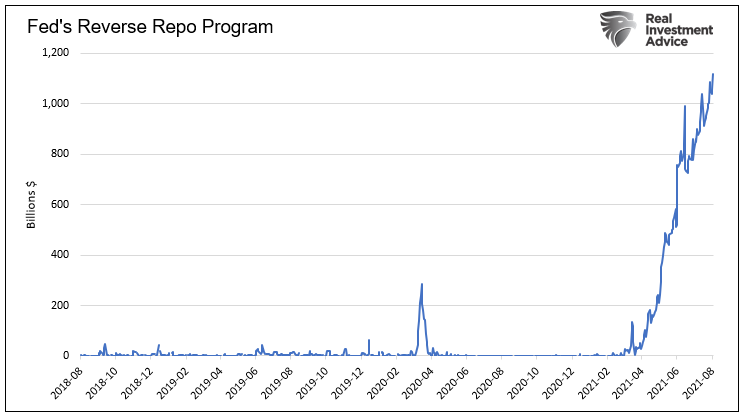

The Fed’s Reverse Repurchase Repo program set another new high at $1.116 trillion. The increasing trend points to the large and growing amount of cash being held at banks and money market funds. These massive balances are a green light of sorts for the Fed to taper. The large amount of cash on the sidelines will help offset the Fed buying less.

Housing Starts were weaker than expectations at 1.534 million annualized versus 1.643 million last month. Higher input prices and a growing reluctance to buy homes are likely causing home builders to scale back. Building permits were up slightly to 1.635 million. Given the increasing supply of existing homes, higher home prices, and weakening consumer sentiment we might find that some builders will reconsider and delay using the permits to build.

Hot Stocks We’re Watching

Since February, the Russell 2000 (IWM), tracking small-cap stocks, is little changed. Over the same period, the S&P 500 has risen by over 20%. The smaller graph below shows the underperformance of small caps to the S&P via the IWM: S&P price ratio. Many small-cap companies are feeling the negative effects of higher prices and are not able to offset inflation with lower interest rates to the degree large-cap companies can. Stripping the S&P 500 of the FANMG stocks and a few other leaders would leave the S&P 500 looking a lot like the Russell Index. This serves as a reminder of Bob Farrell’s investment rule #7: Markets are strongest when they are broad and weakest when they narrow to a handful of blue-chip names.

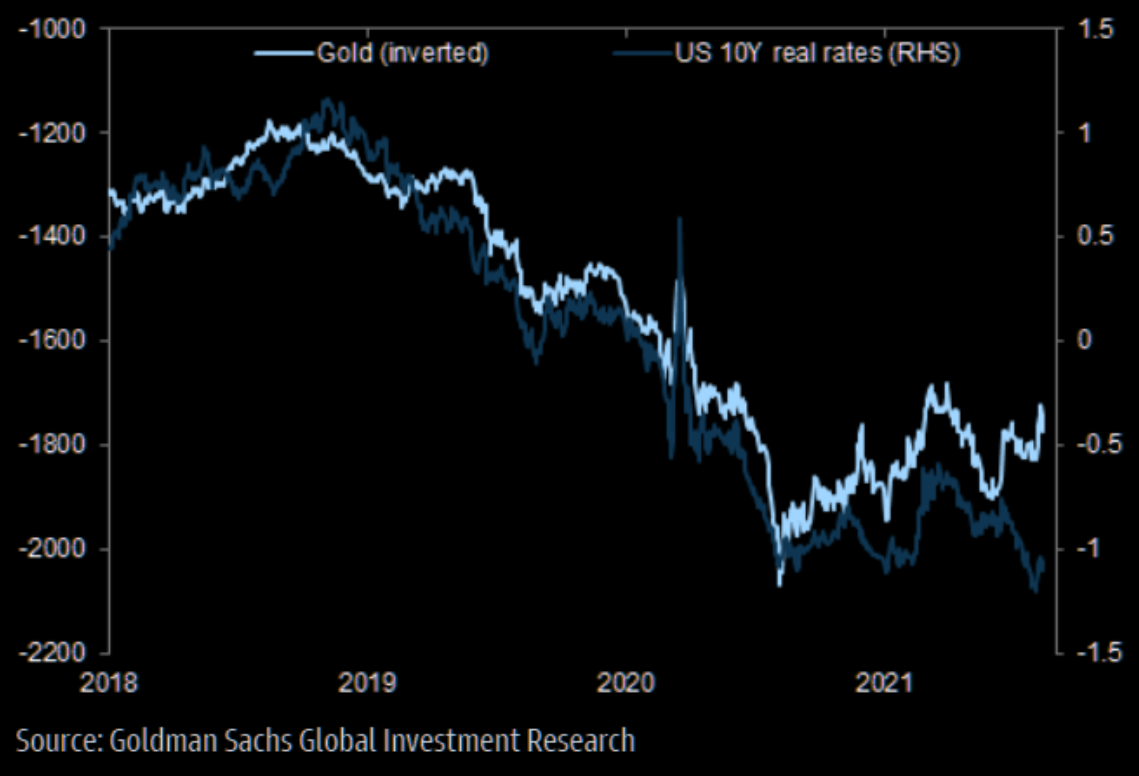

The graph below, courtesy of Goldman Sachs, shows the strong negative correlation between the price of gold to 10-year UST real rates. Recently, the correlation has failed. If the correlation regains its prior strength, the graph implies gold is underpriced by nearly $300, real rates are about to rise, or some combination of both. Real rates increase if Treasury yields rise and/or inflation expectations decline. We suspect it will be the latter.