The Wisdom of Peter Fisher

“In recent years, numerous major central banks announced objectives of achieving more rapid rates of inflation as strategies for fostering higher standards of living. All of them have failed to achieve their objectives.” – Jerry Jordan, former Cleveland Federal Reserve Bank President

In March 2017, former Treasury and Federal Reserve (Fed) official, Peter R. Fisher, delivered a speech at the Grant’s Interest Rate Observer Spring Conference entitled Undoing Extraordinary Monetary Policy. It is one of the most insightful and compelling assessments of the Fed’s post-financial crisis policy actions available.

Now a professor at the Tuck School of Business at Dartmouth, Fisher is a true insider with experience in the government and private sector that affords him unique insight. Given the recent policy “pivot” by Chairman Powell and all members of the Fed, Fisher’s comments from two years ago take on fresh relevance worth revisiting.

In the past, when Fed leadership discussed normalizing the Fed’s post-crisis policy actions, they exuded confidence that it can and will be done smoothly and without any implications for the economy or markets. Specifically, in a Washington Post article from 2010, Bernanke stated, “We have made all necessary preparations, and we are confident that we have the tools to unwind these policies at the appropriate time.” More recently, Janet Yellen and others have echoed those sentiments. Current Fed Chairman Jerome Powell, tasked with normalizing policy, appears to be finding out differently.

Define “Normal”

Taking a step back, there are important issues at stake if the Fed truly wants to unshackle the market economy from the influences of extreme monetary policy and the harm it may be causing. To normalize policy, the Fed first needs to explicitly define “normal.”

For instance:

- The Fed should take steps to raise interest rates to what is considered “normal” levels. Normal can be characterized as a Federal Funds target rate in line with the average of the past 30 years or it might be a level that reflects sufficient “dry powder” were the Fed to need that policy tool in a future economic slowdown.

- The Fed should reduce the size of their balance sheet. In this case, normal under reasonable logic would be the size of the balance sheet before the financial crisis either in absolute terms or as a percentage of nominal gross domestic production (GDP). Despite some reductions, it is not close on either count.

The Fed consistently feeds investors’ guessing games about what they deem appropriate. There appears to be little rigor, debate, or transparency about the substance of those decisions. Neither Ben Bernanke nor Janet Yellen offered details about how they would accurately characterize “normal” in either context. The reason for this seems obvious enough. If they were to establish reasonable parameters that defined normal levels in either case, they would be held accountable for differences from their prescribed benchmarks. It might force them to take actions that, while productive and proper in the long-run, may be disruptive to the financial markets in the short run. How inconvenient.

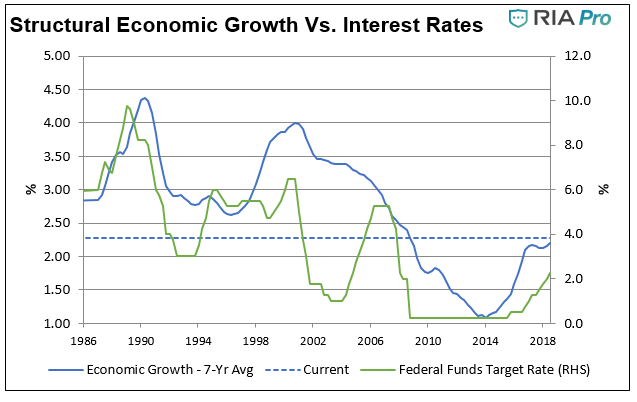

In most instances, normal is defined as something that conforms to a standard or that which has been common under historical experience. Begin by looking at the Fed Funds target rate. A Fed Funds rate of 0.0% for seven years is not normal, nor is the current rate range of 2.25-2.50%.

As illustrated in the chart below, in each of the past three recessions dating back to 1989, the Fed cut the fed funds rate by an average of 5.83%. In that context, and now resting at less than half the average historical pre-recession level, a Fed Funds rate of 2.25-2.50% is clearly abnormal and of greater concern, insufficient to combat a downturn.

Interest rates should mimic the structural growth rate of the economy. As we have illustrated in prior analysis and articles, particularly Wicksell’s Elegant Model, using a 7-year cycle for economic growth reflective of historical expansions, that time-frame should offer a reasonable proxy for “structural” economic growth. The issue of greater concern is that, contrary to the statement above, structural growth appears to be imitating the level of interest rates meaning the more the Fed suppresses interest rates, the more growth languishes.

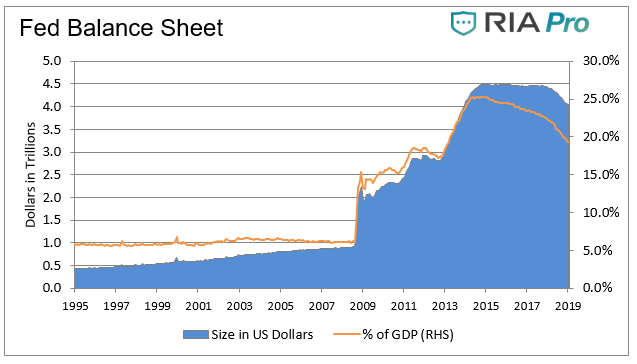

Next, let’s look at the Fed balance sheet. Quantitative tightening began in late 2017 gradually increasing as the Fed allowed their securities bought during QE to mature without replacing them. As shown in the blue shaded area in the chart below, QT reduced the Fed balance sheet by about $500 billion, but it remains absurdly high at nearly $4.0 trillion. As a percentage of GDP, it has dropped from a peak of 25.3% to 19%. Before the point at which QE was initiated in September 2008, the size of the Fed balance sheet was roughly $900 billion or 6% of nominal GDP and was in a tight range around that level for decades. Now, with the Fed halting any further reductions in the balance sheet, are we to assume 20% of GDP to be a normal level? If so, what is the basis for that conclusion?

The bottom line: simple analysis, straight-forward logic, and common sense dictate that monetary policy remains abnormal.

Fisher helps us understand why the Fed is so hesitant to normalize policy, despite their outward confidence in being able to do so.

Second-Order Effects

As Fisher stated in his remarks at the conference, “The challenge of normalizing policy will be to undo bad habits that have developed in how monetary policy is explained and understood.” This is a powerfully important statement highlighting second-order effects. He continues, “…the Fed will have to walk back from their early assurances that the “exit would be easy.” Prophetic indeed.

The “easy” part of getting rates and the balance sheet back to “normal” is now proving to be not so easy. What the Fed did not account for when they unleashed unprecedented policy was the habits and behaviors among governments, corporations, households, and investors. Modifying these behaviors will come at a debilitating cost.

Think of it like this: Nobody starts smoking cigarettes with a goal of smoking two packs a day for 30 years, but once introduced, it is difficult to stop. Furthermore, trying to stop smoking can be very painful and expensive. NOT stopping is medically and scientifically proven to be even more so.

Fisher goes on to explain in real-world terms how two households are impacted in an environment of extraordinary policy actions. One household possesses savings; the other does not. Consider their traditional liabilities such as mortgage and auto loans, “but also their future consumption expenditures, their liability to feed and clothe themselves in the future.” The family with savings may feel wealthier from gains in their invested savings and retirement accounts as a result of extraordinary policies pushing financial markets higher, but they also must endure an increase in the cost of living. In the final analysis, they end up where they started. “They may… perceive a wealth effect but, ultimately, there is only a wealth illusion.”

As for the family without savings, they had no investments to go up in value, so there is no wealth effect. This means that their cost of living rose and, wages largely stagnant, it occurred without any form of a commensurate rise in income. That can only mean their standard of living dropped. As Fisher states, given extraordinary policy imposed, “There was no wealth effect, not even a wealth illusion, just a cruel hoax.” He further adds, “…the next time you hear that the net-wealth of American households is at an all-time high, do spend a minute thinking about the present value of the unrecorded future consumption expenditures, particularly of households with no savings.”

What is remarkable about Fisher’s analysis is contrasting it with the statements of Fed officials who say they are acting in the best interest of all U.S. citizens. Quoting from George Orwell’s Animal Farm, “All animals are equal, but some animals are more equal than others.”

A man can easily drown crossing a stream that is on average 3 feet deep. Household wealth as a macro measure of monetary policy success in a period when wealth inequality is at such extremes perfectly illustrates this imperfection. As Fisher states, “Out of both humility and self-preservation, let’s hope the Fed finds a way to stop targeting the level of wealth.”

Linear Extrapolation

Fisher also addresses the issue of Fed forward guidance stating, “Implicit in forward guidance…is the idea that dampening short-term market uncertainty and volatility is a good thing. But removing uncertainty from our capital markets is not, in my view, an unambiguous blessing.”

Forward guidance, whereby the Fed provides expectations about future policy, targets an optimal level of volatility without being clear about what “optimal” means. How does the Fed know what is optimal? As we have stated before, a market made up of millions of buyers and sellers is a much better arbiter of prices, value, and the resulting volatility than is the small group of unelected officials at the Fed. Yet, they do indeed falsely portray an understanding of “optimal” by managing the prices of interest rates but theirs is a guess no better than yours or mine. Based upon their economic track record, we would argue their guess is far worse.

Fisher goes on to reference John Maynard Keynes on the subject of extrapolative expectations which is commonly used as a basis for asset pricing. Referring to it as the “conventional valuation” in his book The General Theory of Employment, Interest and Money, Keynes said this reflects investors’ assumptions “that the existing state of affairs will continue indefinitely, except in so far as we have specific reasons to expect a change.” Connecting those dots, Fisher states that “forward guidance is the process through which the Fed – through its more explicit influence on the expected rate of interest – becomes the much more explicit owner of the “conventional valuation” of asset prices… the Fed now has a heightened responsibility and sensitivity to asset pricing.”

That conclusion is critically important and clarifies the behavior we see coming out of the Eccles Building. In becoming the “explicit owner” of valuations in the stock market, the Fed now must adhere to a pattern of decisions and actions that will ultimately support the prices of risky assets under all circumstances. Far from rigorous scrutiny of doubts and assumptions, the Fed fails in every way to apply the scientific method of analyzing their actions before and after they take them. So desperate are they to manage the expectations of the public, their current posture leaves no latitude for uncertainty. As Fisher further points out, the last time we saw evidence of a similar stance was in 2007 when the Fed rejected the possibility of a nation-wide decline in house prices.

Summary

Fisher fittingly sums up by restating the point he made at the beginning:

“…the Fed and other central banks appear to have avoided being candid about the uncertainty (of extraordinary monetary policies) in order to maintain their credibility. But this is backwards. They cannot regain their credibility unless they are candid about the uncertainty and how they confront it.”

The power of Fisher’s perspectives is in his candor. Now at a time when the Fed is proving him correct on every count, it is worthwhile to refresh our memories. We would encourage investors to read the transcript in full. Given the clarity of the insights he shares, summarized here, their importance cannot be overstated.