Quick Take: The Great “Tesla” Hysteria Of 2020

“Let us see how high we can fly before the sun melts the wax in our wings.” – E. O. Wilson

Since January 1, 2020, Tesla’s (TSLA) stock price has risen by $462 or 110%. TSLA’s market cap now exceeds every automaker except for Toyota. In fact, it exceeds not only the combined value of the “big three” automakers GM, Ford, and Chrysler/Fiat, but also companies like Charles Schwab, Target, Deere, Eli Lily, and Marriot to name a few large companies.

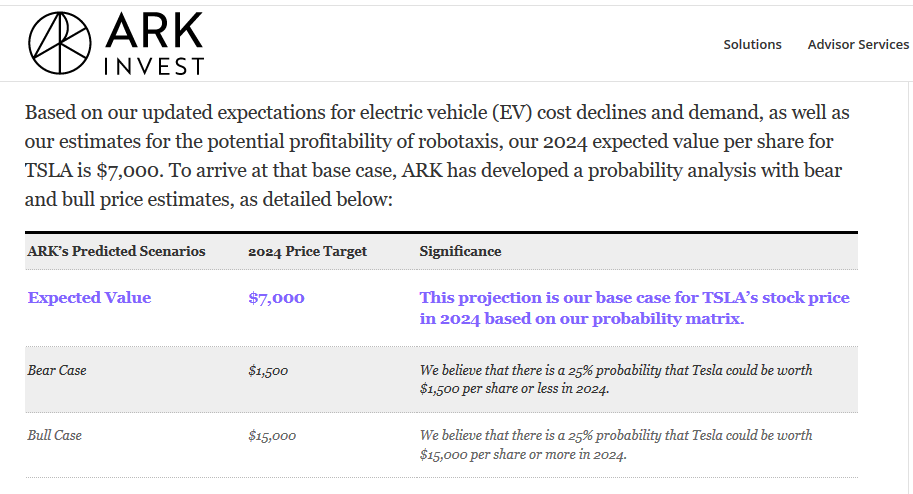

Seem crazy? Not as crazy as what comes next. Crazy are the expectations of Catherine Wood of ARK Invest. This well-known “disruptive innovation” based investor put out the following chart showing an expected price of $7,000 in 2024 with a $15,000 upside target.

Siren songs such as the one shown above encourage investors to chase the stock higher with reckless abandon, and maybe that is ARK’s intent. Given their large holding of TSLA, it certainly makes more sense than their price targets. Instead of taking her recommendations with blind faith, here are some statistics to illustrate what is required for TSLA to reach such lofty goals.

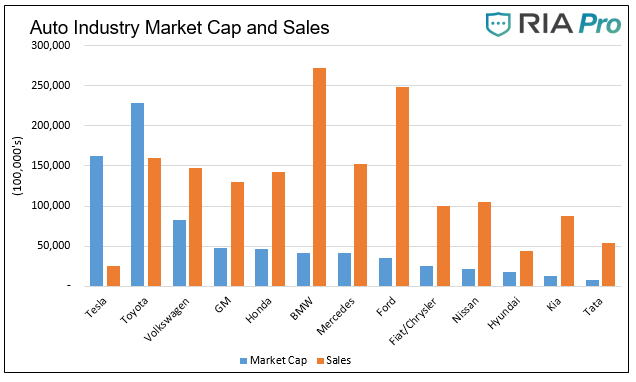

To start, let’s compare TSLA to their peer group, the auto industry. The chart below shows that TSLA has the second largest market cap in the auto industry, only behind Toyota. Despite the market cap, its sales are the lowest in the industry and by a lot. According to figures published on their website, TSLA sold 367,500 cars in 2019. General Motors sold 2.9 million and Ford sold 2.4 million.

Clearly investors are betting on the future, so let’s put ARK’s forecast into context.

If the TSLA share price were to rise to their baseline forecast of 7,000, the market cap would increase to $1.26 trillion. Currently, the auto industry, as shown above, and including TSLA, aggregates to $772 billion. At the upside scenario of 15,000, the market cap of TSLA ($2.7 trillion) would be almost four times the current market cap of the entire auto industry. More stunning, it would be greater than the combined value of Apple and Microsoft.

Even if we make the ridiculous assumption that TSLA will be the world’s only automaker, a price of 15,000 still implies a valuation that is three to four times the current industry average based on price to sales and price to earnings. At 7,000, its valuation would be 1.6 times the industry average. Again, and we stress, that is if TSLA is the world’s only automaker.

Summary

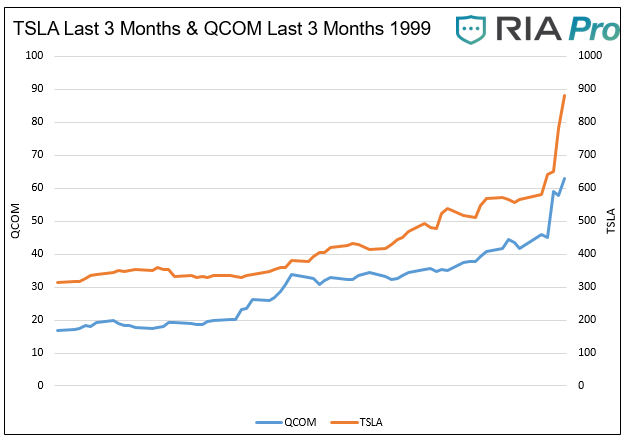

Tesla is one of a few poster children for the latest surge in the current bull market. That said, it’s worth remembering some examples from the past. For instance, Qualcomm (QCOM) was a poster child for the tech boom in the late 1990s. Below is a chart comparing the final surge in QCOM (Q4 1999) to the last three months of trading for TSLA.

In the last quarter of 1999, QCOM’s price rose by 277%. TSLA is only up 181% in the last three months and may catch up to QCOM’s meteoric rise. However, if history is any guide, QCOM likely offers what a textbook example of a blow-off top is. By 2003 QCOM lost 90% of its value and would not recapture the 1999 highs for 15 years.

Tesla may be the next great automaker and, in doing so, own a sizeable portion of market share. However, to have estimates as high as those proposed by ARK, they must be the only automaker and assume fantastic growth in the number of cars bought worldwide. Given their technology is replicable and given the enormous incentives for competitors, we not only find ARK’s wild forecast exceedingly optimistic, but we believe it is already trading near a best-case scenario level.

One final factor that ARK Invest also seems to have neglected is the risk of an economic downturn. Although they do highlight a “Bear Case” price target of $1,500, that too seems incoherent. Given that TSLA is still losing money and is also heavily indebted, an economic slowdown would raise the risk of their demise. In such an instance, TSLA would probably become the property of one of the major car companies for less than $50 per share.

TSLA’s stock may run higher. Its price is now a function of all the key speculative ingredients – momentum, greed, FOMO, and of course, short covering. The sky always seems to be the limit in the short run, but as Icarus found out, be careful aiming for the sun.

**As we published the article Tesla was up 20% on the day. The one day jump raised their market cap by an amount greater than the respective market caps of KIA, Hyundai, Nissan, and Fiat/Chrysler!!