Yeah…But

Yeah… Barry Bonds, a Major League Baseball (MLB) player, put up some amazing stats in his career. What sets him apart from other players is that he got better in the later years of his career, a time when most players see their production rapidly decline.

Before the age of 30, Bonds hit a home run every 5.9% of the time he was at bat. After his 30th birthday, that rate almost doubled to over 10%. From age 36 to 39, he hit an astounding .351, well above his lifetime .298 batting average. Of all Major League baseball players over the age of 35, Bonds leads in home runs, slugging percentage, runs created, extra-base hits, and home runs per at bat. We would be remiss if we neglected to mention that Barry Bonds hit a record 762 homeruns in his MLB career and he also holds the MLB record for most home runs in a season with 73.

But… as we found out after those records were broken, Bond’s extraordinary statistics were not because of practice, a new batting stance, maturity, or other organic factors. It was his use of steroids. The same steroids that allowed Bonds to get stronger, heal quicker, and produce Hall of Fame statistics will also take a toll on his health in the years ahead.

Turn on CNBC or Bloomberg News, and you will inevitably hear the hosts and interviewees rave on and on about the booming markets, low unemployment, and the record economic expansion. To that, we say Yeah… As in the Barry Bonds story, there is also a “But…” that tells the whole story.

As we will discuss, the economy is not all roses when one considers the massive amount of monetary steroids stimulating growth. Further, as Bonds too will likely find out at some point in his future, there will be consequences for these performance-enhancing policies.

Wicksell’s Wisdom

Before a discussion of the abnormal fiscal and monetary policies responsible for surging financial asset prices and the record-long economic expansion, it is important to impart the wisdom of Knut Wicksell and a few paragraphs from a prior article we published entitled Wicksell’s Elegant Model.

“According to Wicksell, when the market rate (of interest) is below the natural rate, there is an incentive to borrow and reinvest in an economy at the higher natural rate. This normally leads to an economic boom until demand drives up the market rate and eventually chokes off demand. When the market rate exceeds the natural rate, borrowing slows along with economic activity eventually leading to a recession, and the market rate again falls back below the natural rate. Wicksell viewed the divergences between the natural rate and the market rate as the mechanism by which the economic cycle is determined. If a divergence between the natural rate and the market rate is abnormally sustained, it causes a severe misallocation of capital.

Per Wicksell, optimal policy should aim at keeping the natural rate and the market rate as closely aligned as possible to prevent misallocation. But when short-term market rates are below the natural rate, intelligent investors respond appropriately. They borrow heavily at the low rate and buy existing assets with somewhat predictable returns and shorter time horizons. Financial assets skyrocket in value while long-term, cash-flow driven investments with riskier prospects languish. The bottom line: existing assets rise in value but few new assets are added to the capital stock, which is decidedly bad for productivity and the structural growth of the economy.

Essentially, Wicksell warns that when interest rates are lower than they should be, speculation in financial assets is spurred and investment into the real economy suffers. The result is a boom in financial asset prices at the expense of future economic activity. Sound familiar?

But… Monetary Policy

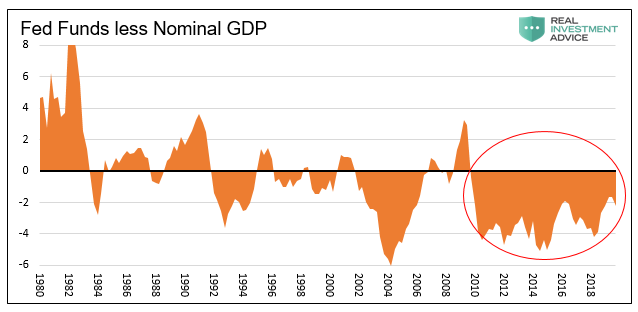

The Fed’s primary tool to manage economic growth and inflation is the Fed Funds rate. Fed Funds is the rate of interest that banks charge each other to borrow on an overnight basis. As the graph below shows, the Fed Funds rate has been pinned at least 2% below the rate of economic growth since the financial crisis. Such a low relative rate spanning such a long period is simply unprecedented, and in the words of Wicksell not “optimal policy.”

Until the financial crisis, managing the Fed Funds rate was the sole tool for setting monetary policy. As such, it was easy to assess how much, if any, stimulus the Fed was providing at any point in time. The advent of Quantitative Easing (QE) made this task less transparent at the same time the Fed was telling us they wanted to be more transparent.

Between 2008 and 2014, through three installations of QE, the Fed bought nearly $3.2 trillion of government, mortgage-backed, and agency securities in exchange for excess banking reserves. These excess reserves allowed banks to extend more loans than would be otherwise possible. In doing so, not only was economic activity generated, but the money supply rose which had a positive effect on the economy and financial markets.

Trying to quantifying the amount of stimulus offered by QE is not easy. However, in 2011, Fed Chairman Bernanke provided a simple rule in Congressional testimony to allow us to transform a dollar amount of QE into an interest rate equivalent. Bernanke suggested that every additional $6.6 to $10 billion of excess reserves, the byproduct of QE, has the effect of lowering interest rates by 0.01%. Therefore, every trillion dollars’ worth of new excess reserves is equivalent to lowering interest rates by 1.00% to 1.50% in Bernanke’s opinion. In the ensuing discussion, we use Bernanke’s more conservative estimate of $10 billion to produce a .01% decline in interest rates.

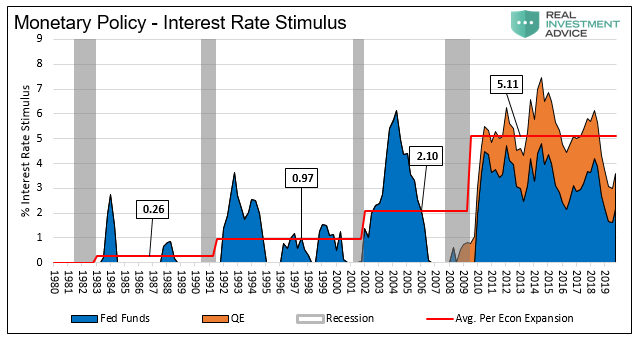

The graph below aggregates the two forms of monetary stimulus (Fed Funds and QE) to gauge how much effective interest rates are below the rate of economic growth. The blue area uses the Fed Funds – GDP data from the first graph. The orange area representing QE is based on Bernanke’s formula.

Since the financial crisis, the Fed has effectively kept interest rates 5.11% below the rate of economic growth on average. Looking back in time, one can see that the current policy prescription is vastly different from the prior three recessions and ensuing expansions. Following the three recessions before the financial crisis, the Fed kept interest rates lower than the GDP rate to help foster recovery. The stimulus was limited in duration and removed entirely during the expansion. Before comparing these periods to the current expansion, it is worth noting that the amount of stimulus increased during each expansion. This is a function of the growth of debt in the economy beyond the economy’s growth rate and the increasing reliance on debt to generate economic growth.

The current expansion is being promoted by significantly more stimulus and at much more consistent levels. Effectively the Fed is keeping rates 5.11% below normal, which is about five times the stimulus applied to the average of the prior three recessions.

Simply the Fed has gone from periodic use of stimulus to heal the economy following recessions to a constant intravenous drip of stimulus to support the economy.

Moar

Starting in late 2015, the Fed tried to wean the economy from the stimulus. Between December of 2015 and December of 2018, the Fed increased the Fed Funds rates by 2.50%. They stepped up those efforts in 2018 as they also reduced the size of their balance sheet (via Quantitative Tightening, “QT”) from $4.4 trillion to $3.7 trillion.

The Fed hoped the economic patient was finally healing from the crisis and they could remove the exorbitant amount of stimulus applied to the economy and the markets. What they discovered is their imprudent policies of the post-crisis era made the patient hopelessly addicted to monetary drugs.

Beginning in July 2019, the Fed cut the target for the Fed Funds rate three times by a cumulative 0.75%. A month after the first rate cut they abruptly halted QT and started increasing their balance sheet through a series of repo operations and QE. Since then, the Fed’s balance sheet has reversed much of the QT related decrease and is growing at a pace that rivals what we saw immediately following the crisis. It is now up almost a half a trillion dollars from the lows and only $200 billion from the high watermark. The Fed is scheduled to add $60 billion more per month to its balance sheet through April. Even more may be added if repo operations expand.

The economy was slowing, and markets were turbulent in late 2018. Despite the massive stimulus still in place, the removal of a relatively small amount of stimulus proved too volatility-inducing for the Fed and the markets to bear.

Summary

Wicksell warned that lower than normal rates lead to speculation in financial assets and less investment into the real economy. Is it any wonder that risk assets have zoomed higher over the last five years despite tepid economic growth and flat corporate earnings (NIPA data Bureau of Economic Analysis -BEA)?

When someone tells you the economy is doing fine, remind them that Barry Bonds was a very good player but the statistics don’t tell the whole story.

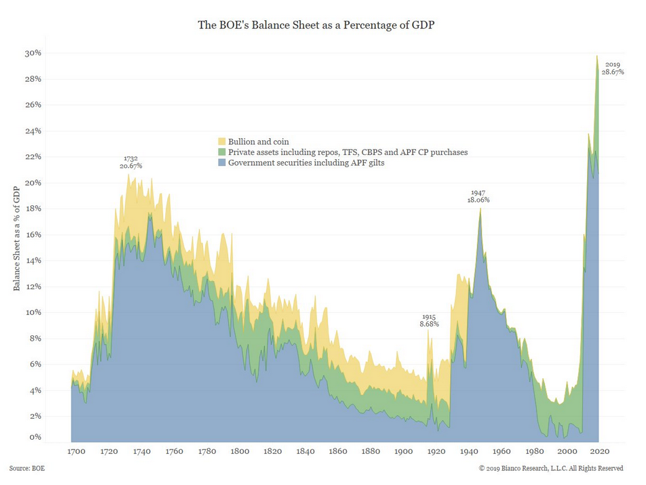

To provide further context on the extremity of monetary policy in America and around the world, we present an incredible graph courtesy of Bianco Research. The graph shows the Bank of England’s balance sheet as a percentage of GDP since 1700. If we focus on the past 100 years, notice the only period comparable to today was during World War II. England was in a life or death battle at the time. What is the rationalization today? Central banker inconvenience?

While most major countries cannot produce similar data going back that far, they have all experienced the same unprecedented surge in their central bank’s balance sheet.

Assuming today’s environment is normal without considering the but…. is a big mistake. And like Barry Bonds, who will never know when the consequences of his actions will bring regret, neither do the central bankers or the markets.