Last week, the S&P 500 volatility index (VIX) fell below 16 for the first time since November 2021. The VIX index uses options prices to imply how much future volatility the market expects. Typically, in upward-trending markets, the VIX trends below 20. Conversely, in bearish markets or shorter drawdowns, it lingers in the 20s but can peak above 50. Lower volatility, like the current reading of 16, implies the market is very comfortable with potential risks.

The graph below charts the S&P 500 and the VIX. We use two colors to highlight when the VIX is over 16 (orange) and under 16 (green). The VIX tends to reside under 16 during the beginning and middle stages of the rallies. Toward the latter stage, when valuations rise, and risks become more pronounced, volatility often perks up. Since 1990, the VIX has been below 16 a little more than a third of the time. Of these instances, the average daily gain has been 0.11%. Conversely, when the VIX is greater than 16, the average daily loss was -.013%. Bottom line: a VIX below 16 is bullish.

What To Watch Today

Economy

- No notable economic releases

Earnings

Bullish Buy Signals Are In

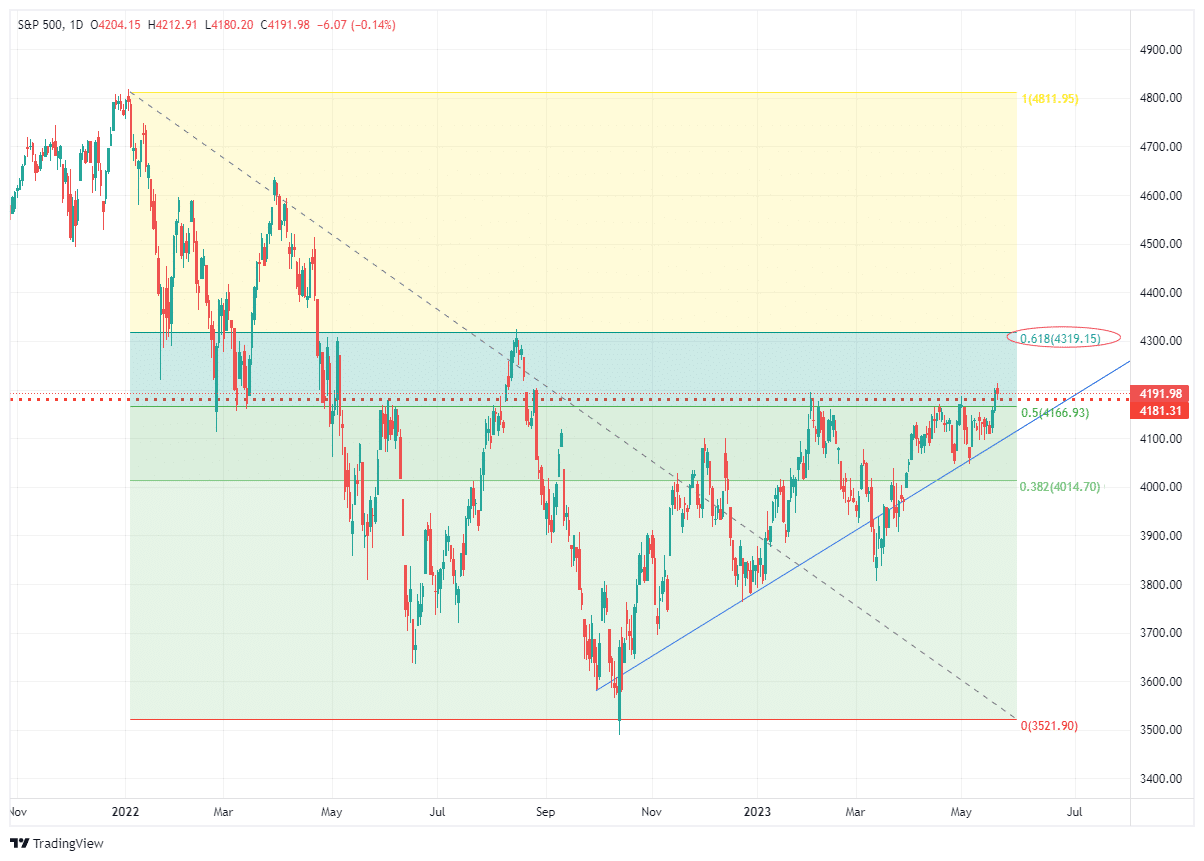

After 45 days of sideways action, the market broke decisively higher last week. While narrow in scope, that breakout allows the market to move higher. As I noted in Friday morning’s Daily Market Commentary:

“Following more good news from retailers, which further confirmed no imminent recession, stocks broke above the trading range that has contained markets since February. That breakout sparked massive short covering and a rush to buy into the technology sector index, with the mega-caps again leading the way, as we discussed in yesterday’s morning note.“

On Friday, the market pulled back and held the breakout level with the first test of the previous resistance. If that level holds next week, the market will have a new support level to build off of.

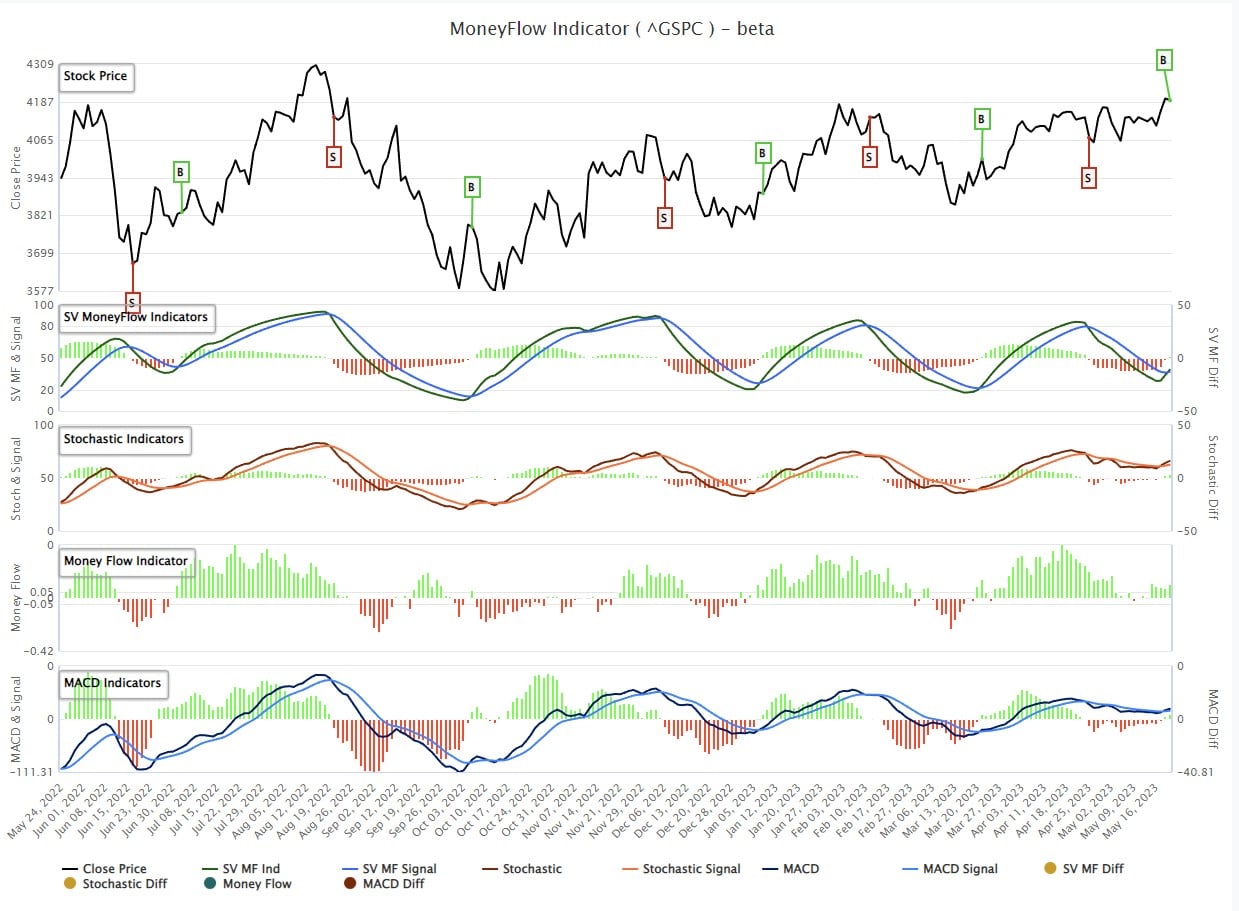

More importantly, as shown below, the MACD and the MoneyFlow “buy signals” confirmed that breakout. Such suggests that the most likely move for the market is higher for now.

The only “negative” to the market action is that the buy signals are triggering at fairly high levels from a historical basis, which will likely contain the upside of whatever rally the market provides. As noted in the chart above, the next target for the market near term is 4300. Any dips between the current market level and the rising trend line from the October lows, or the 50-DMA, should be used to increase equity exposure accordingly.

For now, there is absolutely no reason to be negative on the market as the bulls are clearly in control.

The Week Ahead

Heading into the Memorial Day weekend, there will be limited economic data and few earnings reports. Several housing numbers will be released this week, including pending home sales, building permits, and new home sales. On Friday, the Fed’s preferred inflation gauge, Core PCE, is expected to post a 0.3% monthly gain.

Like last week, many Fed members will share their views. Generally, they have been hawkish and in the “higher for longer” camp. Currently, the market assigns a 20% chance the Fed will increase rates at the mid-June meeting. The minutes from the Fed’s May meeting are due out on Wednesday. If the recent FOMO-like trading in the equity markets is of concern, they may mention it in the minutes. Other than that, the market is not expecting fireworks from the FOMC minutes.

Tech Valuations

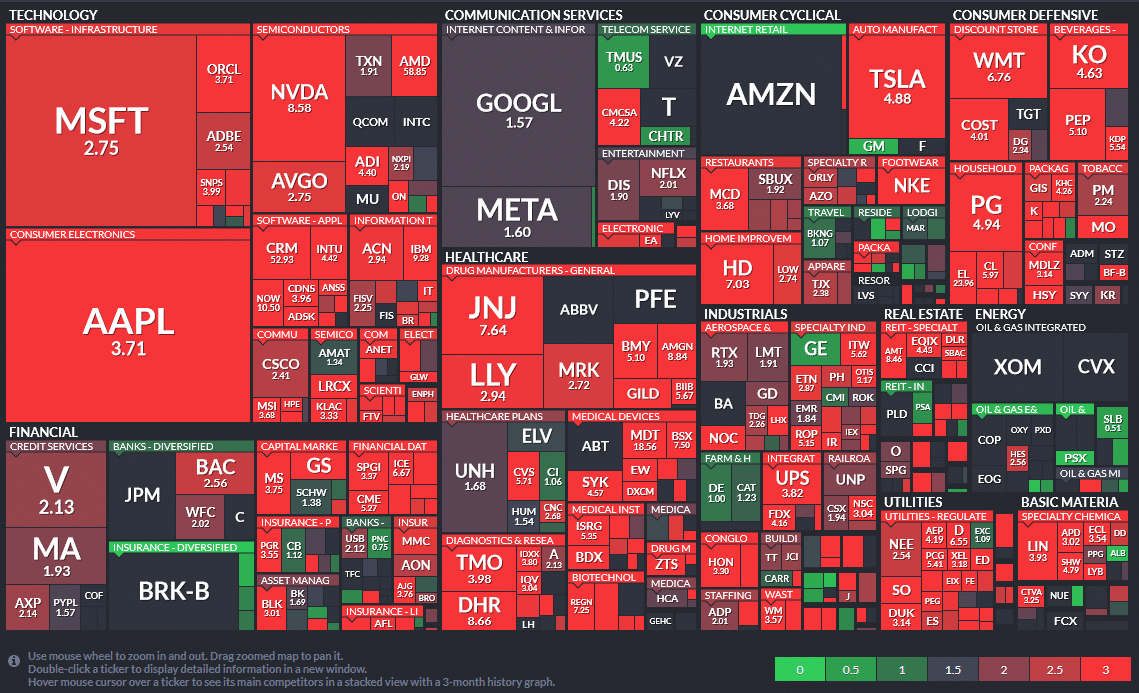

Much has been made about this year’s +26% run in the Nasdaq (QQQ). Yet, fewer are talking about the soaring valuations left in its wake. The FinViz heat maps below provide a few key valuation measures for each S&P 500 stock. A stock’s market cap determines the size of each block. Also, each stock is placed within its appropriate sector.

The first graph below shows that Forward P/Es are generally very high for the largest tech companies. However, GOOGL and META are still reasonable in the communications sector. The second chart shows that the price-to-sales ratios are very high for many tech, communications, and some sub-sectors within healthcare. Note that NVDA now has a price-to-sales ratio of 51 using last quarter’s data. Using the more reliable 12-month trailing sales, its ratio is lower but still a very hefty 29. Consider it stood at ten only seven months ago! Last is the PEG ratio, which is the P/E divided by growth. This is an excellent tool for normalizing valuations within sectors as growth rates differ. Again, large swaths of the chart are deep red, measuring high valuations.

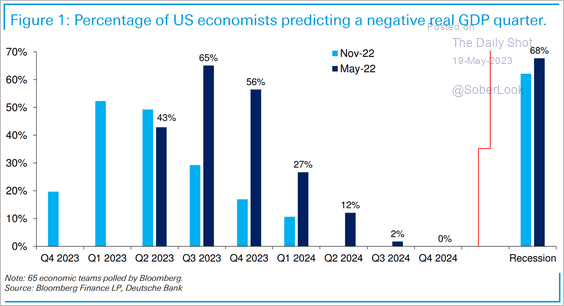

Recession Odds Delayed, But Not Going Away

It’s hard to avoid a graph or statistic using time-tested correlations that aren’t forecasting a recession. Yet, despite the gloomy forecasts, the economy keeps humming along. To wit, the Atlanta Fed GDPNow pegs second quarter GDP growth at 2.9%, albeit the model only has one month of data. The graph below compares the percentage of economists predicting at least one negative quarter of growth today versus six months ago. In November 2022, over 50% of economists thought we would have a negative quarter in the first or second quarter of 2023. Now an even greater 65%, see a negative quarter in the third quarter.

Economists are more sure of a recession today versus six months ago but keep pushing the date it occurs to the future. In our opinion, they are rightfully concerned about higher interest rates and tightening financial standards but not putting enough emphasis on the continued strong demand from consumers. Such demand may slow, but unless the labor market weakens considerably, a soft landing, not a recession, becomes viable. That said, monetary policy and its lags will continue to be an increasing headwind toward growth.

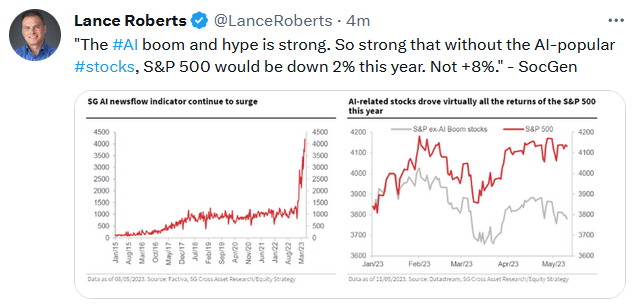

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.