For Part 1 on “Tariff Risk” read: Tariff Impact Not As Bearish As Predicted.

In “Trumpflation” we discussed why the tariff risk was not inflation. To wit:

“Today, globalization and technology give consumers vast choices in the products they buy. While instituting a tariff on a set of products from China may indeed raise the prices of those specific products, consumers have easy choices for substitution. A recent survey by Civic Science showed an excellent example of why tariffs won’t increase prices (always a function of supply and demand).”

Of course, if demand drops for products with tariffs, prices will fall, reducing inflationary pressures. Furthermore, the tariff risk is not a one-sided event. If Trump tariffs Chinese, European, or Canadian products, those countries tend to enact counter-balancing tariffs on U.S. products. Such slows demand for goods and services between all parties, again a deflationary process.

But therein lies the real tariff risk investors should focus on- the corporate profitability risk.

How We Got Here

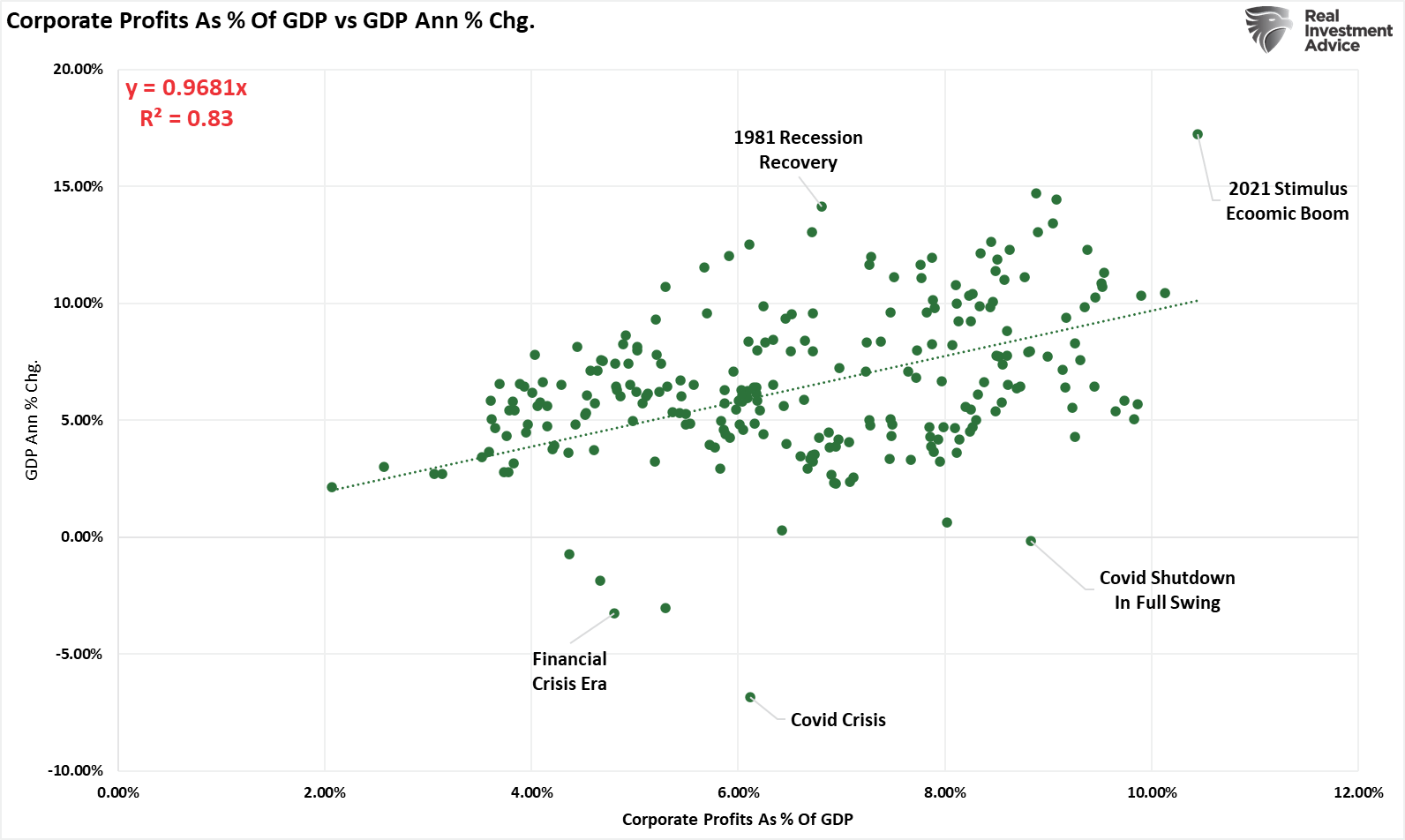

Corporate profit margins in the U.S. are at historic highs, with S&P 500 companies enjoying levels well above their long-term exponential growth trends.

Post-pandemic demand surges, supply chain disruptions, and massive fiscal and monetary interventions supported those elevated margins. As evidenced by the chart below, the correlation between economic growth rates and corporate profits is high. Note that outliers of the correlation are historically related to events such as the “Financial Crisis” and post-recession economic recoveries.

However, as the economic landscape shifts, several factors threaten to erode these profit margins, which should raise concerns for investors.

Pandemic-era stimulus measures played a critical role in boosting corporate profits. Trillions in fiscal and monetary support created robust demand, while low interest rates reduced borrowing costs. Businesses capitalized on supply chain disruptions, passing increased costs to consumers with little resistance. At the same time, industries like technology and healthcare benefited from market consolidation, strengthening their pricing power. Labor costs also lagged behind inflation during this period, helping businesses maintain wide margins.

However, these conditions are now waning. As economic growth slows, supply chains normalize, and inflation moderates, sustaining high profit margins will become more challenging.

Such is particularly the case when it comes to tariffs.

Tariff Risk On Corporate Profits

Corporations react to cost increases in their business (i.e., wages, benefits, commodities, utilities, etc.), which must be factored into the selling price to maintain profitability. Crucially, corporations can only pass on higher input costs to consumers if demand remains higher than the available supply of those goods or services.

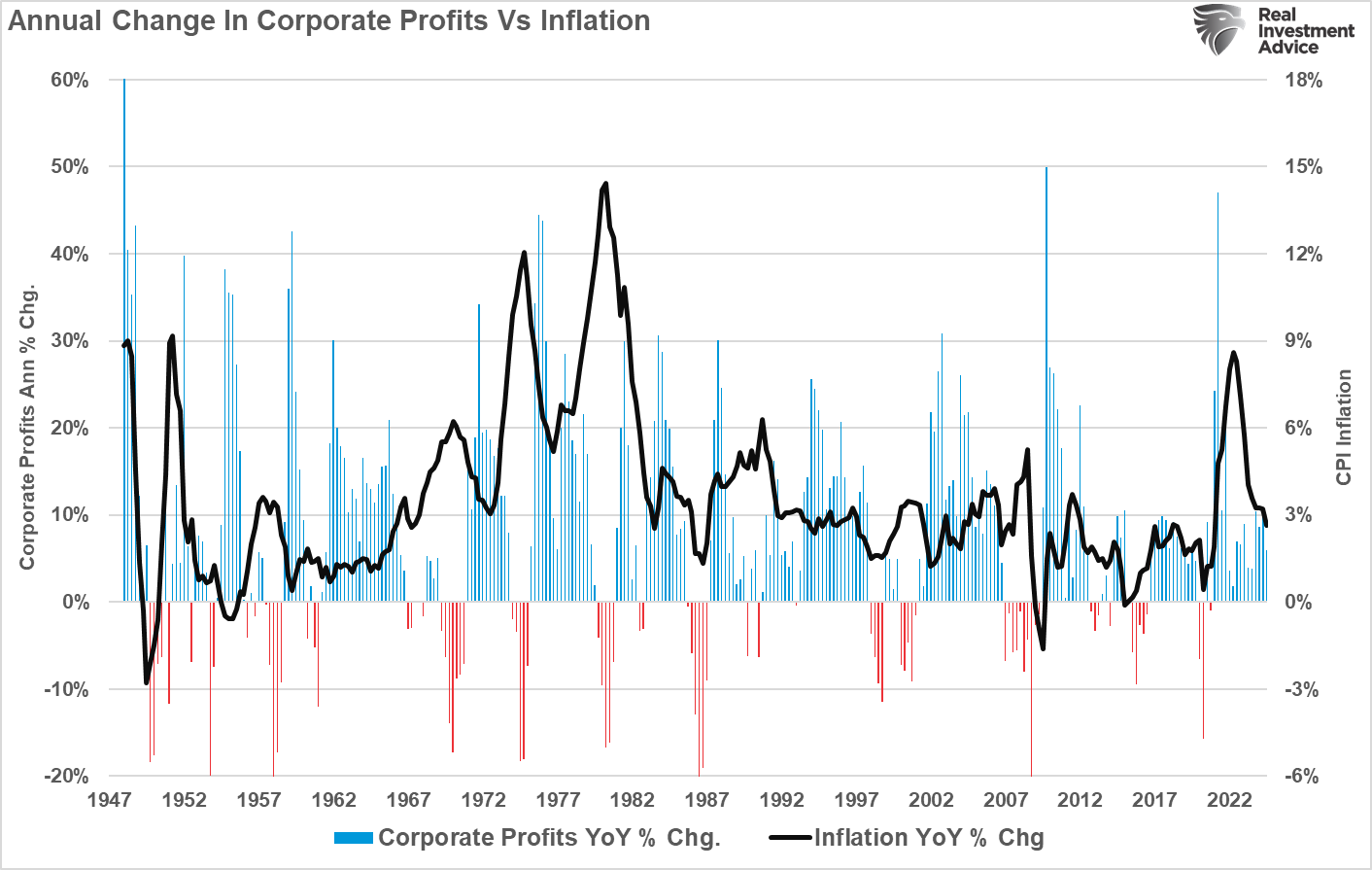

In 2020 and 2021, corporations could pass on most of the inflationary increase to consumers as they were willing to spend the Government’s money. However, as excess savings run out, inflation declines as consumers decrease spending; corporate profits weaken as the ability to pass on higher input costs to customers fades. As shown, as inflation declines, the rate of change in corporate profits also weakens.

We see the same if you use a two-year average of corporate profits minus inflation. Again, when inflation surged in 2020, corporations could pass on the bulk of the cost increases to consumers. Today, as inflation slows due to declining demand, corporations must absorb the inflation to sell products or services.

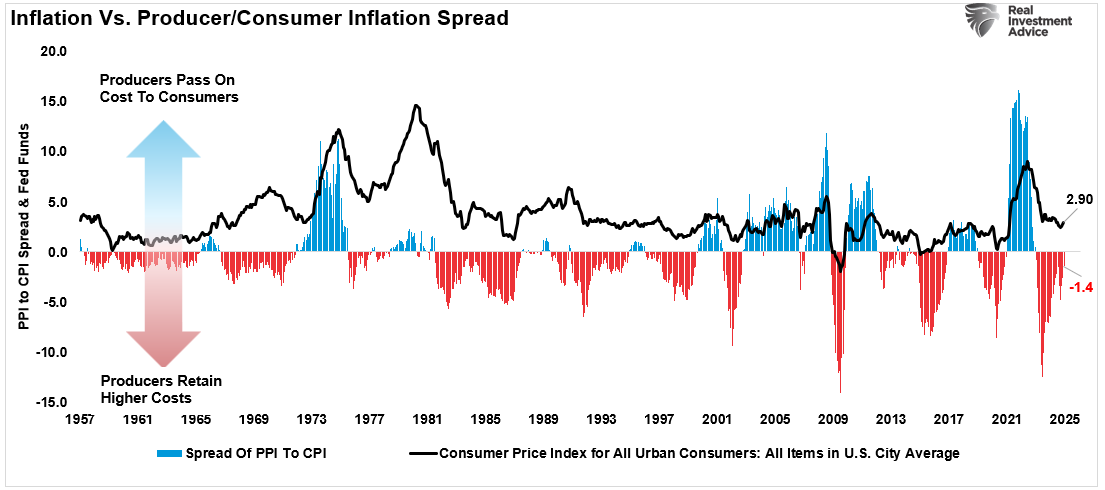

Another way to view this issue is by comparing the spread between the consumer price index (what consumers pay for goods and services) and the producer price index (what corporations pay). When inflation rises and consumer demand exceeds supply, corporations can pass higher input costs to consumers. However, when inflation declines, corporations must absorb higher input costs due to slower demand to sell products or services.

Here is the crucial point:

“Corporations don’t create inflation. They merely react to changes in demand and adjust pricing and supply to maintain profitability. When the consumer slows down, corporations cut prices to reduce supply.”

While many risks, such as high labor costs, increased borrowing costs, slowing economic growth, and tax policy risks, threaten corporate profitability over the next few years, tariff risk is often overlooked.

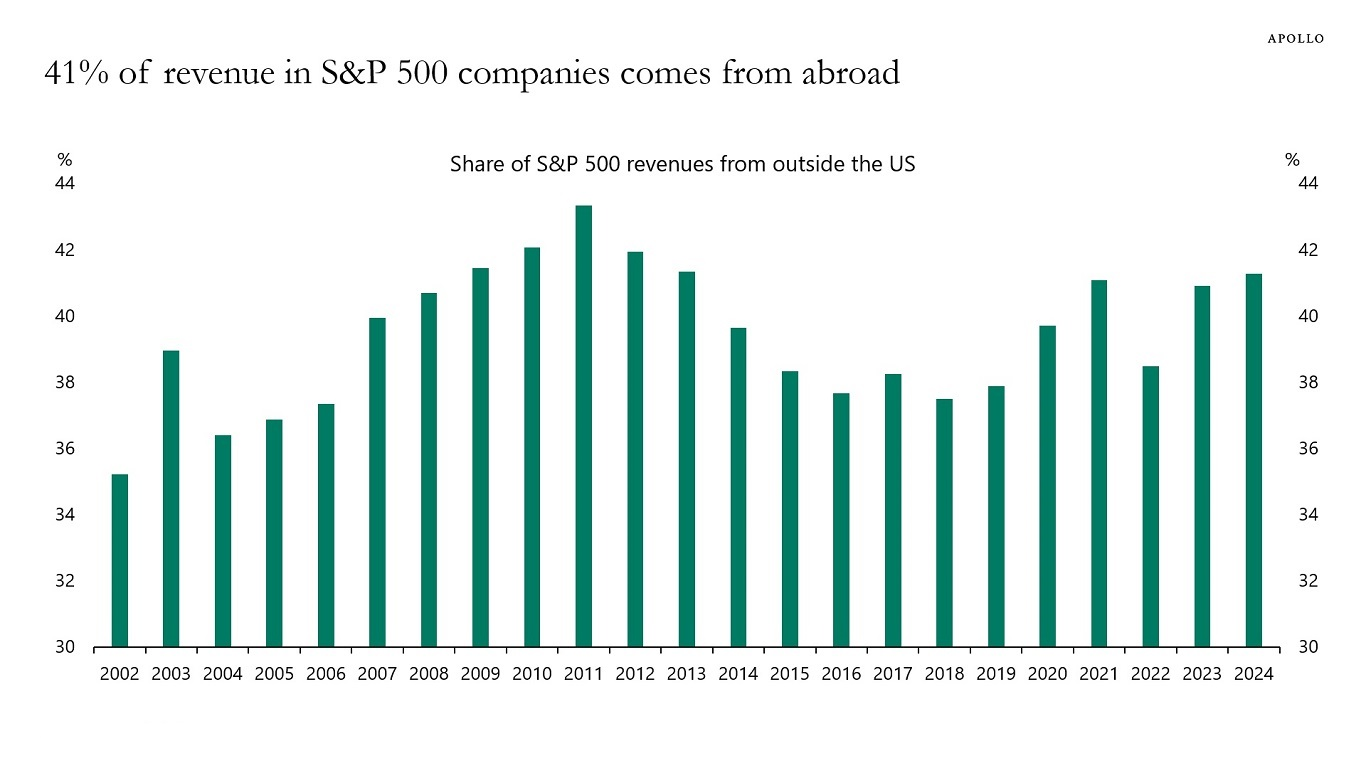

“The narrative in markets is that the outlook for the US is great, and the outlook for Europe, UK, and China is not good. For markets, the problem with this narrative is that 41% of revenues in the S&P 500 come from abroad. If we have a recession in Europe and a continued slowdown in China, it will have a significant negative impact on earnings for S&P 500 companies.” – Torsten Slok, Apollo Academy

One of the risks the Trump administration faces by imposing tariffs is the negative impact of tariffs on exports. Tariffs are an additional tax on imported goods, increasing the costs of those products. However, as noted above, tariffs are never in isolation, as the countries we impose tariffs on will likely impose tariffs back on the U.S. This “tit-for-tat” process threatens to raise costs on exports to countries already impacted by the purchasing power differential caused by a strong dollar. The chart below shows net corporate profit margins during the previous Trump-era tariff policy. Logically, given the high corporate revenue derived from international sales, investors should expect that any cost increase will immediately impact profitability.

With this potential tariff risk in mind, what are the implications for investors in 2025?

Implications for Investors

As always, the problem facing investors is the timing of when the impacts of economic, political, or regulatory changes occur. Sometimes, those impacts can be immediate, such as a reduction in corporate tax rates; other times, the effect of a political or regulatory change can take much longer to manifest.

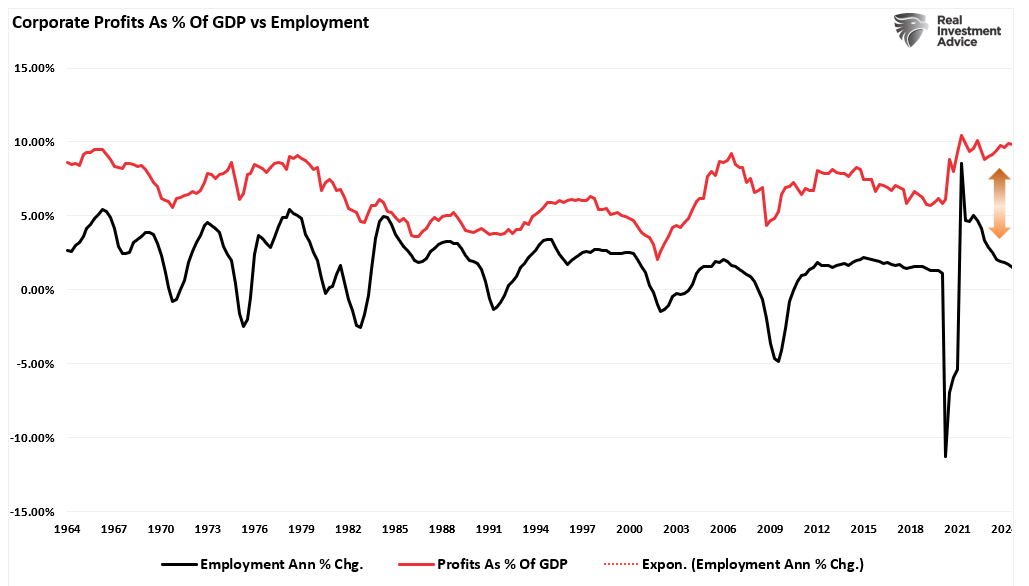

However, given the exceptionally high profit margin levels in an environment where employment growth is declining, tariff risks are increasing, and economic growth is slowing, being somewhat cautious about specific market exposures may make sense. The chart below shows the long-term relationship between employment growth (where wages and economic demand come from) and corporate profitability as a percentage of the economy.

So, what should investors do? One step would be to monitor portfolio holdings with an exceptionally large foreign revenue exposure. Below is a table of notable S&P 500 companies with substantial international revenue exposure. (Note: The percentages of revenue from international sales are approximate and based on available data as of 2023. Current P/S and P/E ratios are subject to change based on market conditions and company performance.)

Furthermore, investors should adopt a proactive and diversified strategy. The following steps can help mitigate these risks:

- Focus on Resilient Sectors: Certain industries, such as utilities, consumer staples, and healthcare, are less sensitive to tariff risks due to consistent demand. Allocating a portion of the portfolio to these sectors can help offset volatility in other areas.

- Evaluate Profit Margin Trends: Rising costs, slowing demand, and tariff risks pressure high corporate profit margins. Investors should analyze companies’ ability to maintain profitability amid these challenges. Companies with efficient cost structures and strong pricing power are better positioned to weather such conditions.

- Hedge Against Currency Risks: A strong dollar can compound the negative effects of tariffs by making U.S. goods more expensive abroad. Investors can consider hedging strategies or exposure to companies that benefit from a strong dollar.

- Adopt a Long-Term View: While tariff policies may create near-term uncertainty, investors should focus on long-term fundamentals. Maintaining a disciplined investment strategy and avoiding reactive decisions based on short-term market volatility can lead to better outcomes.

While I have no idea whether tariff risk will threaten corporate profit margins with certainty, the data suggest that risks exist. As we proceed into 2025, the risk of markets reversing to realign prices with valuations seems increasingly likely.

We suggest that becoming more cautious may pay more significant dividends later this year.

For deeper insights into managing your investments in today’s volatile market, visit RealInvestmentAdvice.com for expert guidance and actionable strategies.