Inside This Week’s Bull Bear Report

- The Presidential Election Cometh

- How We Are Trading It

- Research Report –Buybacks: A Wolf In Sheep’s Clothing

- Youtube – Before The Bell

- Market Statistics

- Stock Screens

- Portfolio Trades This Week

One The Greatest Risk-Adjusted Returns…Ever

Last week, we discussed the break of the rising wedge pattern.

“Unsurprisingly, the market stumbled a bit this past week, breaking the “rising wedge” pattern to the downside. However, the market continues to find buyers at the 20-DMA as portfolio managers are unwilling to be “out of the market” currently.”

Such remained the case this week until it didn’t. On Thursday, the market cracked the 20-DMA and swiftly fell to retest the 50-DMA. There is an important lesson in this week’s action. Over the last several weeks, we have warned about the weakening of momentum and relative strength and the triggering of the MACD “sell signal.” However, many followers commented that the market kept rising despite my warnings and “this time was different.” The lesson is that while technical analysis is NOT perfect, the signals derived from the analysis are often a good process to follow. As always, “timing” is the most difficult challenge. The indicators told us that the market would likely “derisk” before the election, which is now evident.

As we have repeated, while the market was set up for a short-term correction, the backdrop remains bullish. Thus, we expect momentum to carry into year-end. However, here is an interesting data point from Goldman Sachs trader Brian Garrett, which was pointed out this past week.

“Between the lows of October 2023 and the highs of October 2024, the SPX rallied over 40%.What is almost unprecedented about this rally is that it was achieved on a realized volatility of ~12, yielding a “Dirty Sharpe” ratio above 3. Such has only happened previously in ’95, ’97, and pre “vol-mageddon” in 2018.“

To put that into layman’s terms, the last 12 months have been one of the greatest risk-adjusted yearly returns in market history.

What should be noted is that such low-volatility, exuberance-driven rallies eventually end. They lack the appropriate catalyst. As we concluded last week:

“There is currently little risk of a bigger near-term correction. However, some things could cause one, like a highly contested presidential election. In the current political environment, such is not a low-probability event. As such, while we remain allocated to the markets, we are closely monitoring the amount of risk we take.”

In other words, don’t forget to manage risk.

Let’s take a look at Q3 earnings and the upcoming election.

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

Earnings Were Okay…Not Great

As of Friday, about 80% of corporations have reported earnings. There are a few stragglers, like Nvidia (NVDA), which will report in late November, but overall, there is enough reporting to draw some conclusions.

Earnings season was broadly positive, with roughly 80% of reporting companies beating estimates. As noted, such would not be surprising given the sharp reduction in estimates heading into earnings season.

However, what is notable is that despite the high beat rate in earnings, the revenue beat rate has declined over the last three years. Since revenue happens at the “top-line of the income statement” and directly reflects consumer activity, the economy may be weaker than the headlines suggest.

As shown below, revenue is converted into reported earnings. Revenue is derived from actual economic activity. All of the expenses of operating the company and the cost of goods sold are subtracted from revenue. The remainder is the profit or earnings. What is most interesting is that since 2009, revenue (sales) per share has grown by 120%. Yet, after all expenses, reported earnings PER SHARE have surged by 606%. The surge in reported earnings per share has been the $11+ Trillion in corporate share buybacks, reducing the denominator of the equation.

The following chart is more telling. On an earnings-per-share basis, reported and operating earnings are only marginally higher than in 2021. Yet, the market is significantly higher in price.

Such is why valuations are rising dramatically on both a forward and trailing operating basis. Currently, the market has the highest valuations since 2021 and 1999. Following both of those periods was a valuation reversion.

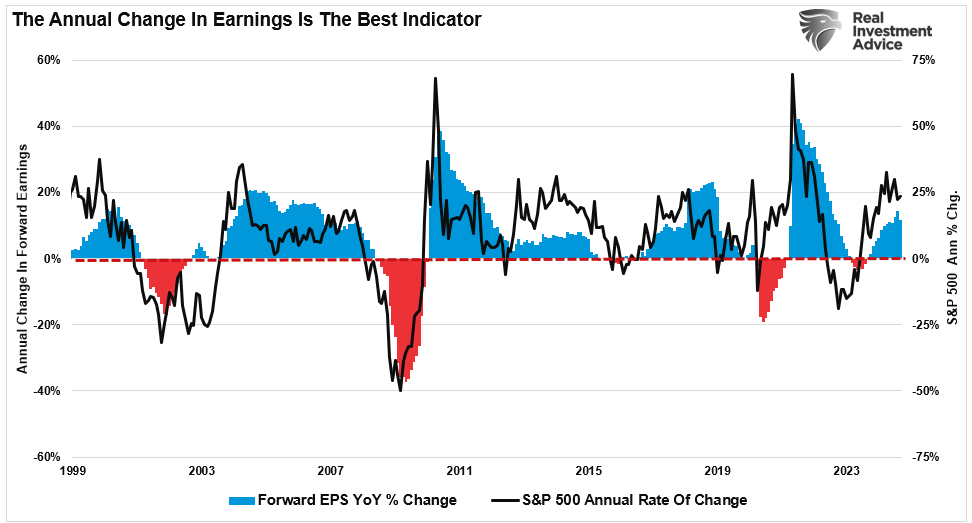

Lastly, while companies have beaten reduced earnings estimates this quarter, the annual rate of change has declined. Pay close attention to the chart below.

The reason is that the annual rate of change in earnings is the best indicator for understanding where the market will be. As shown, there is a decent correlation between the annual rate of change in earnings versus the annual rate of change in the market. Therefore, if the earnings growth rate continues to slow, which should be expected with a slowing economic growth rate, the market’s growth rate should also slow.

However, while we are watching earnings closely, the next week’s presidential election has the world’s attention.

The Presidential Election Cometh

The upcoming presidential election on Tuesday between Donald Trump and Kamala Harris has heightened uncertainty across financial markets. Both candidates present markedly different economic policies, so the stakes are high for investors. Historically, markets have experienced increased volatility preceding major elections. Such is particularly true in close elections where a potential winner is somewhat unclear.

The good news is that post-election returns remain broadly positive. As discussed in “Seasonal Buy Signal,” performance chasing, corporate share buybacks, and market sentiment will likely push markets higher into year-end.

However, while those are averages and some specific historical “close elections,” there is a risk of a “contested election.” Just recently, Greg Valliere noted the following:

“THIS UNFORGETTABLE ELECTION will end next week, but legions of lawyers are already plotting the appeals process, which could last into winter. There are three likely stages:”

- Within hours after the polls close, there will be inevitable calls for recounts. We anticipate about a dozen calls for recounts in the presidential race, with many more appeals in Congressional elections.

- There will be virtually instant allegations of irregularities — ballot boxes stuffed, dead people who voted, the usual stuff, which will be exaggerated on the internet.

- MOST IMPORTANT, the lawyers will unleash an avalanche of lawsuits, claiming fraud. These challenges may drag on into December.

Greg notes that both parties are preparing legal challenges in the event of an unfavorable outcome. Furthermore, if the race is close to a tie, which is entirely possible, both groups will likely make claims of fraud, Russian interference, collusion, etc. However, as Greg concludes:

“THIS WON’T LAST FOREVER, because a challenge could eventually wind up in the House. The Constitution stipulates that a new president must be sworn in by noon on Jan. 20. If this winds through the appeals process, one fact will stand out. The VERY CONSERVATIVE JUDICIARY, largely installed by Trump and Mitch McConnell, will call the shots. The Supreme Court — 6-to-3 conservative — unlimitedly may decide the outcome.”

The bad news about that outcome, while it follows the Constitutional architecture, will lead to a deep political divide in the country, demands for a restructuring of the Supreme Court, and potential civil unrest.

In other words, there is a more than small probability of a very difficult few weeks to a few months, regardless of who wins the election. The last time we had such a contested election was in 2000 between Al Gore and George Bush, when legal challenges over “hanging chads” delayed the presidential election outcome. Unsurprisingly, the market did not respond very positively.

So, what should you be doing?

I Am Not Doing Anything

Over the last few weeks, I have communicated with many concerned about the presidential election’s outcome. Rather than taking some action ahead of the event, their response is, “I am not doing anything.”

While there are times when doing “nothing” is a viable option, as noted above, there is a more than reasonable chance that waiting until after the presidential election results could be difficult. For example, in November 2000, when Gore and Bush were engaged in legal challenges, the market fell nearly 8%. For investors who did not prepare ahead of the election, they were caught potentially panic selling into the decline. This is why risk management is always important. Yes, implementing some risk measures today may limit the upside potential of portfolios. However, underperforming on the way up is far more preferable than outperforming on the way down.

The problem with worrying about individual events is also the behavioral problem of “loss aversion.” This dynamic is a psychological response to the need to avoid losses. For example, “I am worried about the presidential election. Therefore, I will not invest until I know the outcome.”

While I can certainly understand that sentiment, there is ALWAYS something to worry about. Once we get past the election on Tuesday, the Federal Reserve meeting will be held on Wednesday. Then, we have inflation reports, which could lead to concerns about inflation, etc. There is always a good reason NOT to invest.

However, historically, regardless of who the president is, inflation, Federal Reserve policy, or economic data, the market tends to perform over time. As Fidelity recently noted, since 1950, US stocks have averaged returns of 9.1% in election years and 9% annually over all periods.

Furthermore, there is a decent probability that the House and Senate will be divided regardless of who wins the presidency. Such an outcome limits the aggressive political policy changes that could impact corporate earnings. Unsurprisingly, Wall Street likes such outcomes.

Like everyone else, I have no idea how the presidential election will turn out next week. Polls have an enormous historical tendency to be wrong, so we can understand that it can be tempting to “do nothing.” However, the financial markets have largely been unbothered by the presidential and midterm elections, and trying to avoid short-term losses could backfire.

Window dressing, performance chasing, and stock buybacks will drive the markets over the next two months. We also can’t negate the impact of further Fed rate cuts and continued decent economic data into year-end. In other words, elections tend to have less impact on the markets than many believe.

So, what should you do on Monday?

Monday Portfolio Strategy

While market sentiment reflects the tight race between Trump and Harris, the broader economic environment—marked by inflation, interest rates, and consumer behavior—significantly shapes the outlook. Regardless of the outcome, investors should be prepared for near-term volatility. Managing risk can provide critical protection in the uncertain days leading to and following Election Day.

However, as long-term investors, we should focus on broader economic fundamentals rather than short-term political shifts. Remaining calm, balanced, and well-diversified will help investors weather whatever outcomes unfold on Tuesday. This election is a pivotal moment, but the right preparation can help investors stay ahead of the uncertainty and position themselves for opportunities that may arise post-election.

Today is a good day to manage risk.

While we have discussed these simplistic rules over the last several weeks, we continue to reiterate the need to rebalance risk if you have an allocation to equities.

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against significant market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers

- Raise cash and rebalance portfolios to target weightings.

Keep moves small for now. As the markets confirm their next direction, we can continue adjusting accordingly.

If the market likes the election outcome, you may underperform. As we noted last week, risk management ensures that risk is controlled when the “sun shines.” Trying to find an umbrella after it starts raining does little good.

Continue to follow the rules and stick to your discipline. (Read our article on “What Is RIsk” for a complete list of rules)

Feel free to reach out if you want to navigate these uncertain waters with expert guidance. Our team specializes in helping clients make informed decisions in today’s volatile markets.

Have a great week.

Research Report

Subscribe To “Before The Bell” For Daily Trading Updates

We have set up a separate channel JUST for our short daily market updates. Please subscribe to THIS CHANNEL to receive daily notifications before the market opens.

Click Here And Then Click The SUBSCRIBE Button

Subscribe To Our YouTube Channel To Get Notified Of All Our Videos

Bull Bear Report Market Statistics & Screens

SimpleVisor Top & Bottom Performers By Sector

S&P 500 Weekly Tear Sheet

Relative Performance Analysis

Last week, we noted that the previous overbought/sold analysis on the bottom left showed the average and median stock was overbought, with the broad market and many sectors pushing for more extreme conditions. We suggested that such a setup allows the market to “rest” briefly before moving higher into year-end. Over the past two weeks, that correction has taken place, and now most markets and sectors are oversold heading into the election. This is the setup we were looking for to support a rally into year-end. Once we get through the election and the FOMC meeting next week, the market should start to find its footing as buybacks and performance chasing take precedence into year-end.

Technical Composite

The technical overbought/sold gauge comprises several price indicators (R.S.I., Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The market peaks when those readings are 80 or above, suggesting prudent profit-taking and risk management. The best buying opportunities exist when those readings are 20 or below.

The current reading is 70.20 out of a possible 100.

Portfolio Positioning “Fear / Greed” Gauge

The “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, the more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0 to 100. It is a rarity that it reaches levels above 90. The current reading is 66.55 out of a possible 100.

Relative Sector Analysis

Most Oversold Sector Analysis

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares the relative performance of each sector and market to the S&P 500 index.

- “MA XVER” (Moving Average Crossover) is determined by the short-term weekly moving average crossing positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- The table shows the price deviation above and below the weekly moving averages.

The risk/range report resets on the first trading day of the month. Therefore, we won’t have a risk analysis until next week. However, with the vast majority of sectors and markets on bullish buy signals, there is currently little to be concerned with.

Weekly SimpleVisor Stock Screens

We provide three stock screens each week from SimpleVisor.

This week, we are searching for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Fundamental & Technical Strength W/ Dividends

(Click Images To Enlarge)

RSI Screen

Momentum Screen

Fundamental & Technical Screen

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

No Trades This Week

Lance Roberts, C.I.O.

Have a great week!