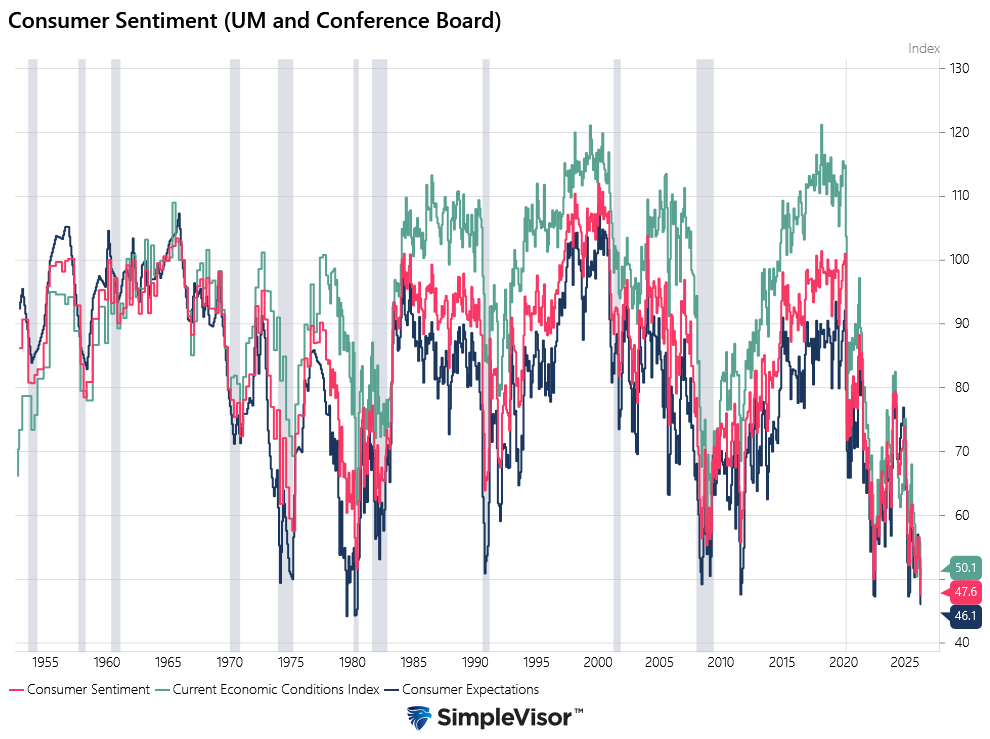

As shown in the graph below, the University of Michigan’s consumer sentiment gauges tells us that consumer confidence is now the worst its been since the survey began in 1952. Despite the confidence gauges being lower than during peak Covid shutdown, the GFC, and the 1970s oil crisis/inflation outbreak, the economy (GDP) and the employment situation have held up much better than one might expect. Unemployment sits below 4.5%, GDP continues to expand, albeit at 0.5% last quarter, and equity markets are at record highs despite the Iran conflict and $90 oil.

The concern, however, is forward-looking. Sentiment doesn’t just measure how people feel; at times it can shape how they spend. Recent data suggests the poor confidence feeling is slowly impacting consumerism. Real personal consumption expenditures, the broadest measure of what consumers buy, have quietly decelerated from roughly 3.5% year-over-year growth in early 2024 to under 2.5%. That’s not recessionary-like spending, but it’s a meaningful decline. Moreover, we are witnessing weakness concentrated in the categories most sensitive to confidence: discretionary retail, autos, and housing-adjacent spending like furniture and appliances.

The transmission lag is critical in predicting economic activity over the next few quarters. Historically, poor sentiment readings take three to six months to fully flow through into hard spending data. Which means the poor Michigan confidence survey is still only partially priced into the consumption data now being released. There may be more to come.

What To Watch Today

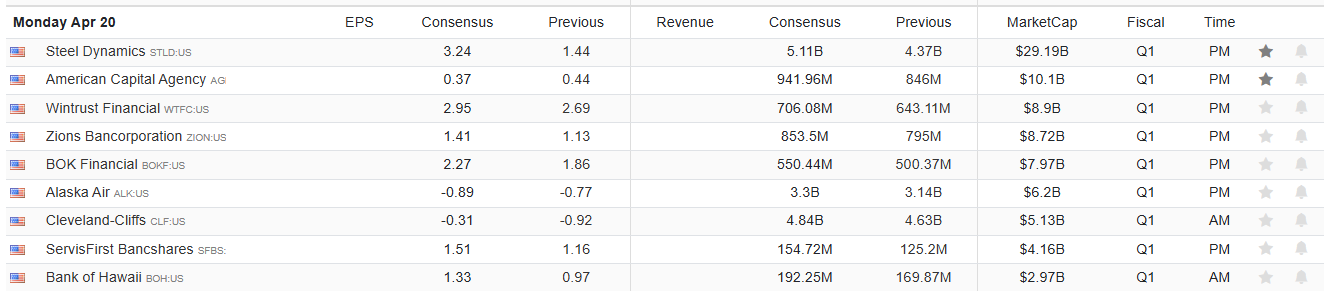

Earnings

Economy

- No economic reports to be released

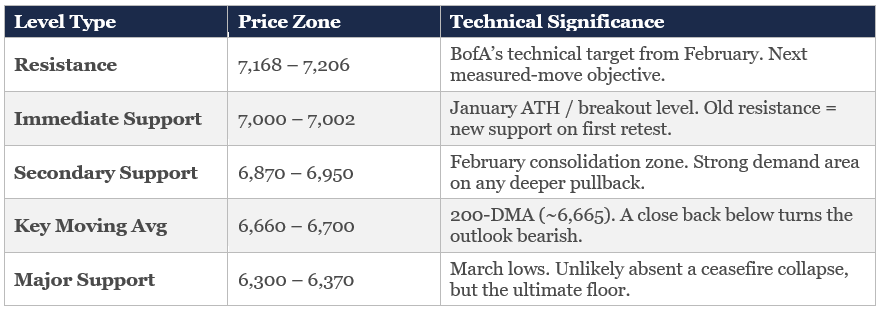

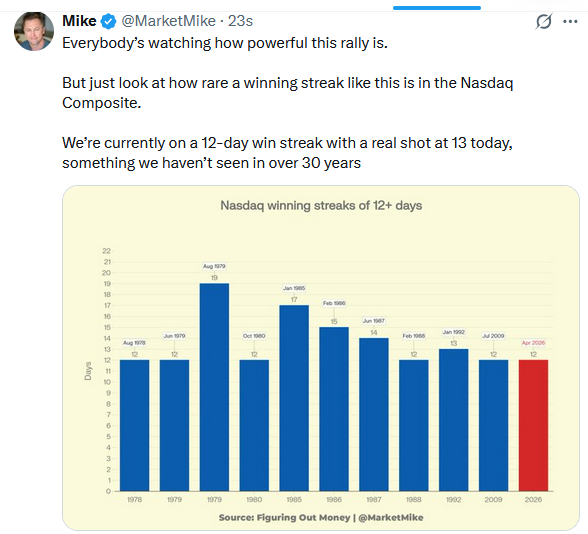

Market Trading Update

The S&P 500 closed Friday at a new all-time high of 7,125, extending 1.8% beyond January’s prior peak and capping a 13.1% rally from the March low in under three weeks. This is one of the sharpest V-shaped recoveries in the post-GFC era. The Nasdaq posted its 13th consecutive gain (its longest winning streak since 2009), the Russell 2000 hit a new all-time high, with 75% of its constituents advancing Friday, and the VIX collapsed from 31 to 17. Oil pulled back below $90 before closing at $94, with ships beginning to transit the Strait of Hormuz. This is exactly the durable-bottom signal we identified weeks ago: a rapid recovery above the 200-day moving average, improving breadth, and oil declining with the VIX below 20.

However, is this just a short-covering rally or the resumption of the bullish trend? The answer is that this is most likely the resumption of the bullish trend.

Two weeks ago, just 27.6% of S&P 500 constituents traded above their 50-DMA (12th percentile). That number has surged to roughly 71%, well above the 50% confirmation threshold we set as the dividing line between a reflexive bounce and a genuine trend reversal. The Russell 2000’s move to all-time highs is the single most bullish breadth signal: small caps confirm this is not merely a Mag 7 short-squeeze. JPMorgan’s flow data shows retail participation rising from the 10th to the 55th percentile. When breadth and flows confirm the move, the rally has a structural foundation that pure short-covering does not.

None of this means you should chase here. After a 13% move in three weeks, the market is stretched on every short-term measure. The RSI is pushing overbought above 70, price is extended 7% above the 200-DMA, and the Nasdaq’s 13-day streak has historically preceded 2–5% pullbacks within two weeks. Retail’s return is a yellow flag of sentiment as the “easy money” phase is behind us. On a pullback, the 7,000 level, January’s former all-time high, becomes first support under the classic “old resistance becomes new support” principle. Below that, the 6,870–6,950 zone (February’s consolidation range) should attract strong buying. The 200-DMA (~6,683) remains the line in the sand. A healthy 2–3% pullback to the 7,000–6,950 zone is the spot to add exposure, not up here at fresh highs.

This rally is the real thing, but treat it with caution. Reversals can be swift, particularly if the narrative supporting the rally fails. For now, stay long, stay patient, and let the market come to you.

Trade accordingly.

The Week Ahead

Retail Sales for March will be the key economic data point this week. This figure will be interesting as it will be the first piece of hard economic data released from the government since the Iran conflict started. Expectations are that the number will be +0.4%, down from +0.6% last month.

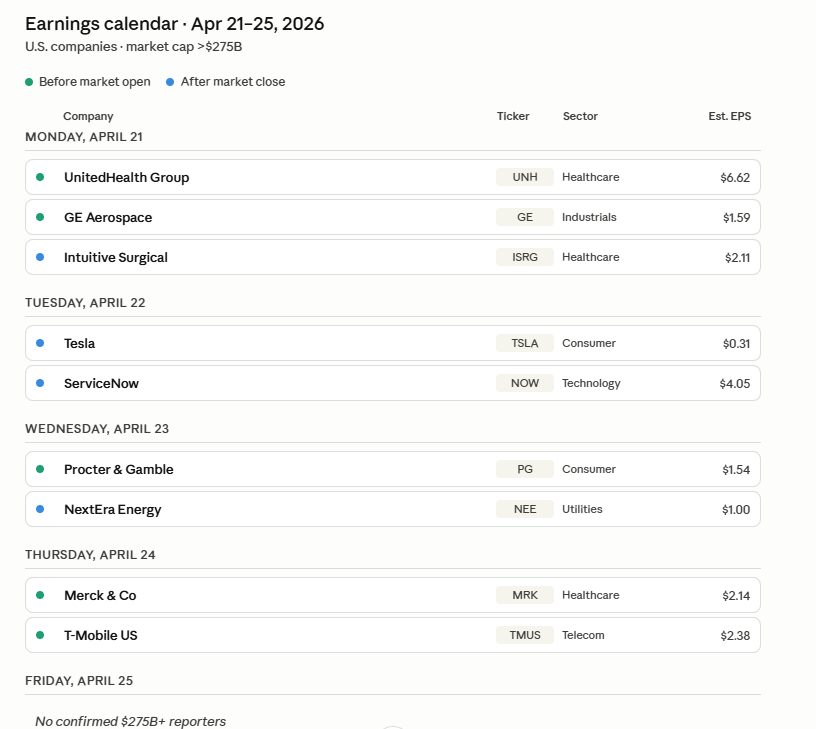

Earnings will kick into full speed this week as we share below. Pay attention to any forward guidance these companies may issue in regards to consumer spending trends.

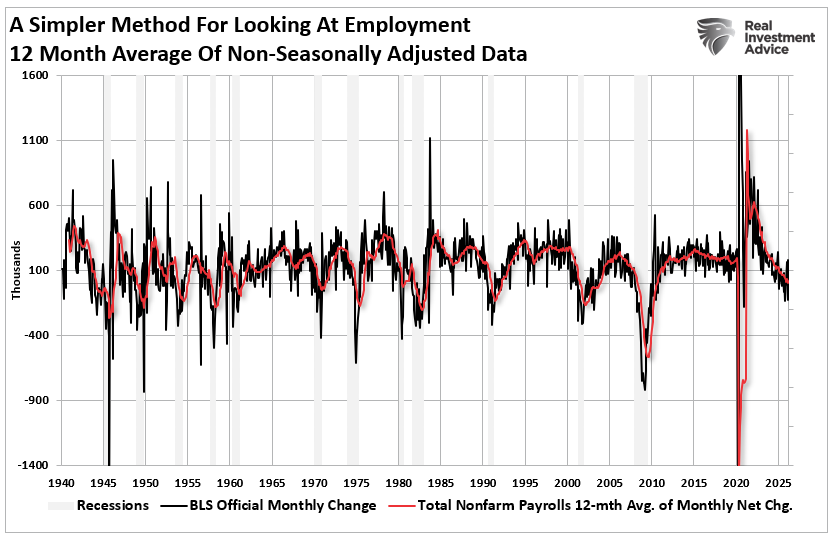

BLS Jobs Report: Is There A Better Measure?

“March’s 178,000 BLS jobs report came in nearly three times Wall Street’s 60,000 estimate. Markets celebrated. Almost nobody mentioned the entire beat traced back to doctors returning from a strike and weather rebounds. That’s not strength. That’s noise — and it’s a pattern we can no longer afford to ignore.“

Every time we see the BLS jobs report released, there are always problems with it. Over the years, I’ve come to accept that most government statistics are imperfect. Regardless, they are what markets pay attention to. However, it is increasingly clear that the BLS Jobs report over the last three years has been problematic. That report lands on the first Friday of every month and sends equity futures swinging before markets open. The problem is that the report has become so distorted by sampling failures, model-based imputations, and seasonal adjustments layered on top of more seasonal adjustments that the monthly print often tells us almost nothing reliable about the actual state of employment.

I realize that is a serious claim that borders on heresy, but let me back it up with the data. I want to show you what I believe is a simpler, more honest alternative. One that filters out the noise and reveals the employment trend that matters to investors and policymakers alike.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.