The Backward K and Coming Earnings Surprises

The broad economic shutdowns and psychological impacts of the pandemic, along with massive doses of fiscal stimulus doled out directly to consumers greatly altered consumer and business spending habits.

As we approach the second-quarter earnings season, we are likely to see a good number of surprises, especially on a year-over-year basis. In the second quarter of 2020, some companies were struggling to keep the lights on. Others were having trouble producing products fast enough to keep up with insatiable demand.

As our friend Peter Atwater correctly predicted in early 2020, the pandemic and its recovery would affect the economy in a K-shaped fashion. Essentially, there will be winners and losers.

With the pandemic abating and economic and consumer spending habits normalizing, some of those divergences from last year are reversing. Might we say the K is turning into a backward K?

This piece compares two companies to appreciate how and when the pandemic affected their revenues and stock price. It then looks forward to the question we face over the coming quarters; how and when earnings and share prices normalize. The analysis will allow you to prepare for earnings announcements from a host of greatly affected companies.

Graphing Distortions

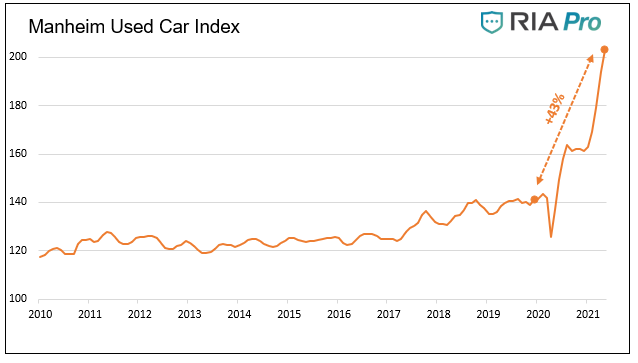

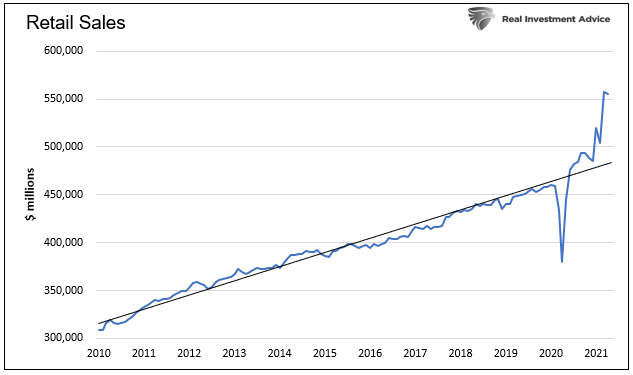

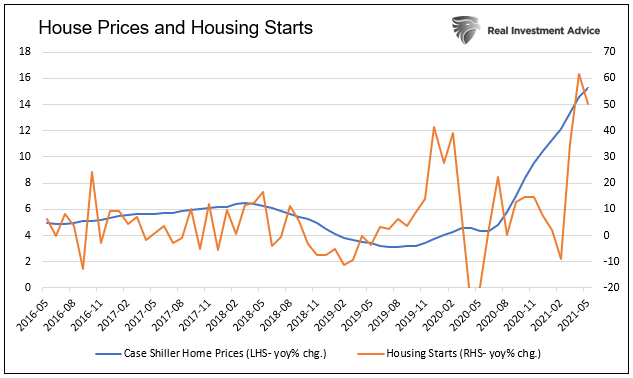

Before presenting the two companies, it is worth sharing a few graphs. While just the tip of the iceberg, the graphs highlight the massive distortions caused by the pandemic and stimulus. We separate the charts between the Haves and the Have Nots.

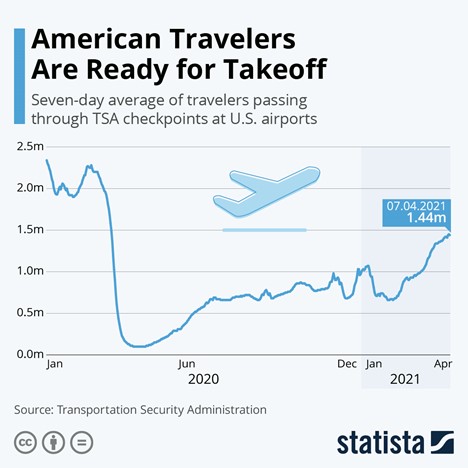

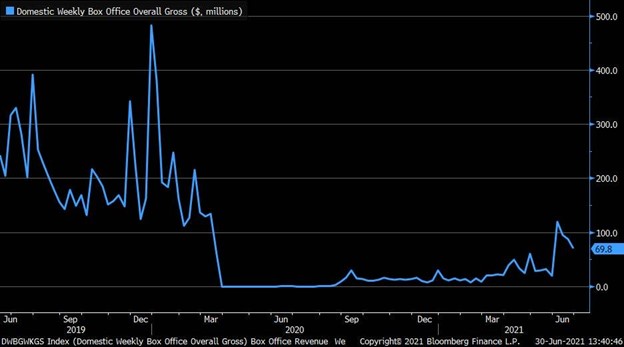

The Haves:

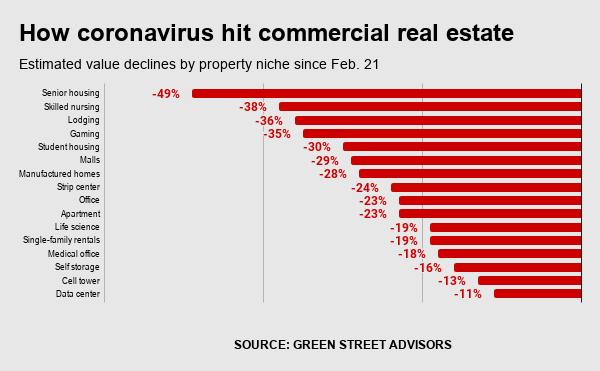

The Have Nots:

Clorox

Clorox started in 1913 as the Electro-Alkaline Company. The company sells a wide range of popular consumer products, focusing on cleaning and disinfecting products.

Clorox Wipes were worth their weight in gold during the early days of COVID. It was common to find empty shelves in the supermarkets where Wipes should have been. As a result of surging sales of Wipes and Bleach, and other disinfectant products, CLX stock price jumped in the spring of 2000.

Today store shelves are fully stocked, and concerns about getting COVID from surface-born germs are fading quickly. Per Lisah Burhan, CLX Investor Relations: “The lower shipments are a result of demand normalization in bleach and Pine-Sol relative to the year-ago period when consumers turned to these products given the persistent out-of-stocks in wipes and sprays at the onset of the pandemic.”

With the normalization process underway and pandemic conditions abating, we compare some fundamental data for CLX before the pandemic and during the pandemic. This analysis allows us better to evaluate CLX’s price and potential for earnings surprises.

Fundamentals CLX

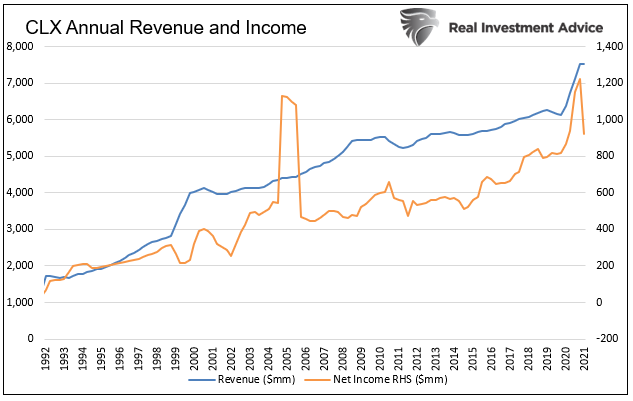

The graph below charts CLX revenue and income over the last 30 years. The pandemic-related spike in revenue and income is evident. From 2012-2019, revenue and income grew by 1.6% and 6.4%, respectively, on an average annualized basis. From 2020 through the first quarter of 2021, they rose 17.7% and 10.3% on an annualized basis. The pandemic was great for CLX’s bottom line.

The pandemic equally benefited shareholders. From January 2020 to August 2020, CLX shot up 60%. Compare that eight-month gain to the average annualized return of 8.4% for the three years before the pandemic.

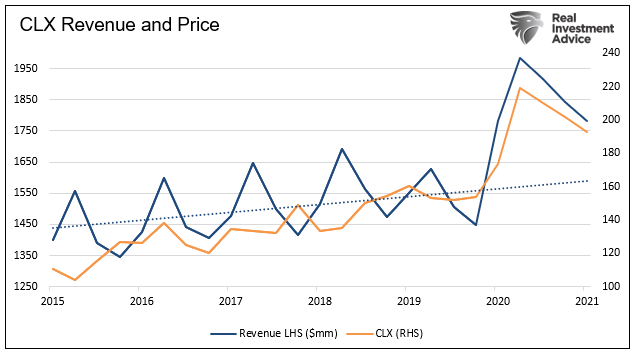

Because of the predictable trending nature of CLX’s sales, we compare its current share price to expected sales to help us arrive at a fair value. We can then value the stock assuming revenue and Price to Sales (P/S) ratio reverts to its pre-pandemic trend.

As shown below, the bump in quarterly revenue and stock price during 2020 and the partial normalization is clear. The dotted blue line indicates the revenue trend from 2015 through 2019.

CLX revenues will likely return to trend as the demand for their products normalizes. Accordingly, we should expect revenue to decline from $1,781 to $1,591. In the fourth quarter of 2019, its P/S ratio was 12.65. At its current price and trend revenue ($1,591), CLX has a P/S ratio of 14.06.

CLX is trading at an 11% premium if we assume its revenue and P/S ratio return to pre-pandemic trends.

Sysco

Sysco (SYY) is an acronym for the Systems and Services Company. SYY is involved in the marketing and distribution of food products and kitchen equipment to restaurants and other institutional foodservice clients. Sysco is not as well known by the public as CLX as they predominately service businesses. Regardless, SYY has a market cap of $40 billion, about twice that of CLX.

Not surprisingly, SYY struggled during the pandemic. Many of its clients were either shut down or relegated to a fraction of their prior business. With people eating out again and offices opening back up, SYY is on the road to recovery.

CEO Kevin Hourican made the following comments during their latest earnings call in May of 2021: “We see tremendous pent-up demand in the food-away-from-home sector. Our data confirms that consumers are eager to eat at restaurants as soon as restrictions are reduced. Strong sales results and long wait times are common in restaurants operating within geographies that have limited restrictions. The third quarter can be aptly described is difficult at the beginning and robust at the end.”

As we did with CLX, let’s compare fundamental data for SYY before the pandemic and during the pandemic.

Fundamentals SYY

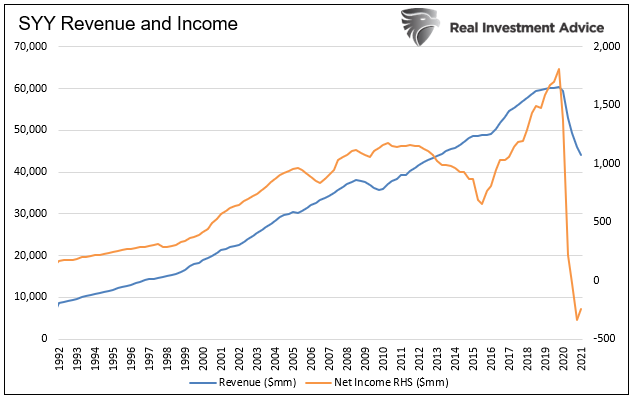

The graph below charts SYY revenue and income over the last 30 years. The pandemic-related reduction of revenue and income is startling. From 2012-2019, revenue and income grew by 5.4% and 4.8%, respectively, on an average annualized basis. From 2020 through the first quarter of 2021, revenue shrunk 22.4% on an annualized basis, and net income, which was running $6.7 billion per year, went negative.

The pandemic was painful for SYY shareholders. Between January and March of 2020, the stock price was cut in half, falling to a price last seen in early 2016. Before the pandemic, SYY was returning 15% per year on average.

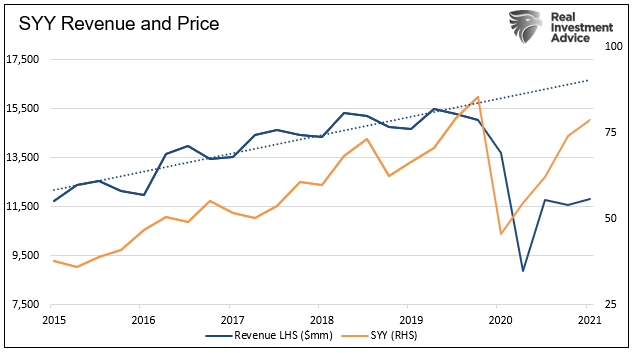

Like CLX, SYY is in a relatively stable and predictable business with dependable revenue trends. The reliable trending nature of their business allows us to do the same analysis we did with CLX.

The following graph zooms in on the data in this analysis. The drop in quarterly revenue and stock price during 2020 and the partial recovery are apparent. The dotted blue line is the revenue trend from 2015 through 2019.

If SYY sales return to normal, we should expect revenue to increase sharply from $11,824 to $16,278. In the final quarter of 2019, its P/S ratio was 3.27. At its current price and with trend revenue, its P/S ratio is 2.37.

SYY is trading at a 27% discount if we assume its business and valuations return to pre-pandemic trends.

Summary

SYY shares are about 10% below their value on 12/31/2019. At the same time, the S&P 500 Index is up about 25%. SYY’s revenue and income remain well off the levels of 2019. How and when SYY recovers is challenging to estimate. However, if they return to 2019 earnings levels more quickly than expected, the share price has significant upside potential. A strong earnings report will likely accompany a surge in the stock price.

Conversely, CLX will try to maintain higher revenue and sales despite what is likely a trend back to pre-pandemic norms. CLX share prices run the risk normalization occurs quicker than expected, and the pandemic premium vanishes in a short period.

SYY and CLX are just two examples of companies that can surprise investors with upcoming earnings announcements. The point is not to single out companies and make predictions but to highlight there are a host of companies with a potential for earnings surprises, positively and negatively. Economic activity a year ago was irregular and economic activity this last quarter is equally unusual.

Understanding what has transpired may open the door to several opportunities and a few stocks to stay away from.

Good luck in what is likely to be a widely divergent earnings season.