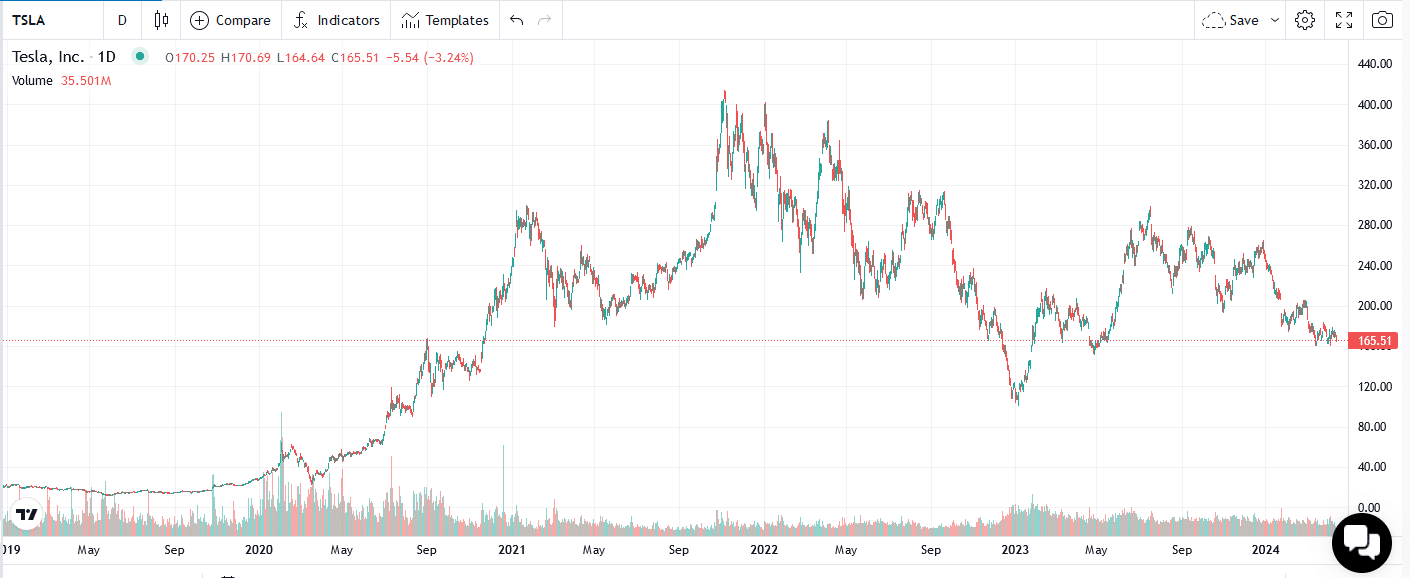

In our article Is Toyota The Next Tesla, we discuss recent trends in the automobile industry. In particular, EV sales growth has been declining as hybrid vehicles become more popular, and concerns specific to EVs are growing. With more competitors in the EV market and new hybrid models hitting the market, Tesla’s market share of total auto sales is at risk. In fact, its sales declined in the first quarter. To counteract the trend toward lower growth, Tesla has made some sacrifices. For starters, Tesla cut prices. Per Cox Automotive, “Tesla’s average transaction price was $52,315 in Q1, down roughly 13.5% year over year. However, lower prices did not generate higher volume.“

Since lower prices amid growing competition and waning demand aren’t spurring sales, Tesla announced it would cut 15,000 jobs or about 10% of its staff on Monday. As we wrote in our aforementioned article, EVs will gain market share but not likely at the pace they have, barring new technology. The Tesla job cuts and weakening sales greatly impact the producers of the metals used to make EVs. Consider the quote below from the Wall Street Journal.

Producers of lithium and nickel, which are used in lithium-ion batteries for EVs, have been stalling projects and closing mines to save cash after a painfully quick fall in commodity prices. Prices of lithium are down as much as 90% since the start of last year, while the price of nickel has roughly halved- The Boom In Battery Metals For EVs Is Turning To Bust

What To Watch Today

Earnings

Economy

Market Trading Update

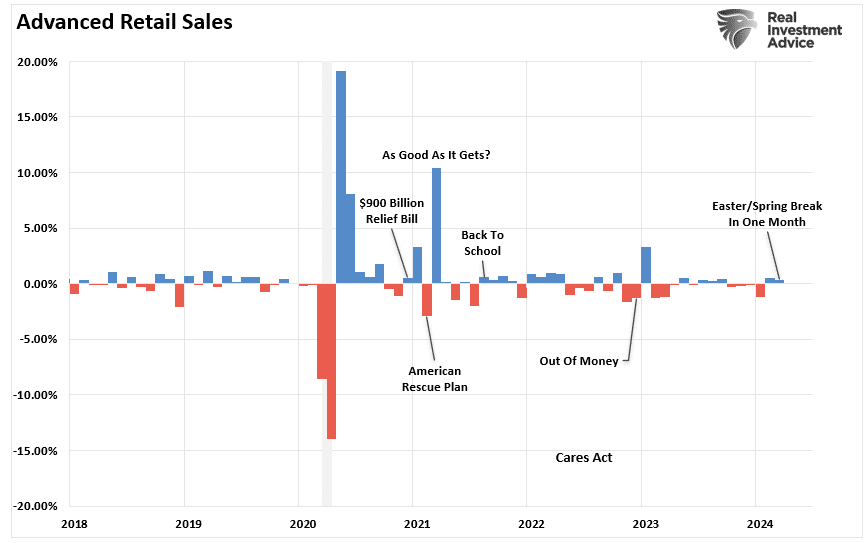

As discussed yesterday, the market is sitting on support at the 50-DMA and is oversold. Yesterday morning, the market opened up decently strong on cooling tensions between Iran and Israel, and stronger than expected retail sales data suggesting the consumer remains strong. However, it didn’t take long for the market to see through the sales data and realize that while sales were strong, it included Spring Break and Easter. Of course, both events require travel, hotels, food, and clothing. It is quite likely April will be substantially weaker as a payback for the pull-forward of spending in March. As shown, retail sales remain weak, and this is on a nominal basis, which is crucial as it means consumers are paying more for the same amount of goods.

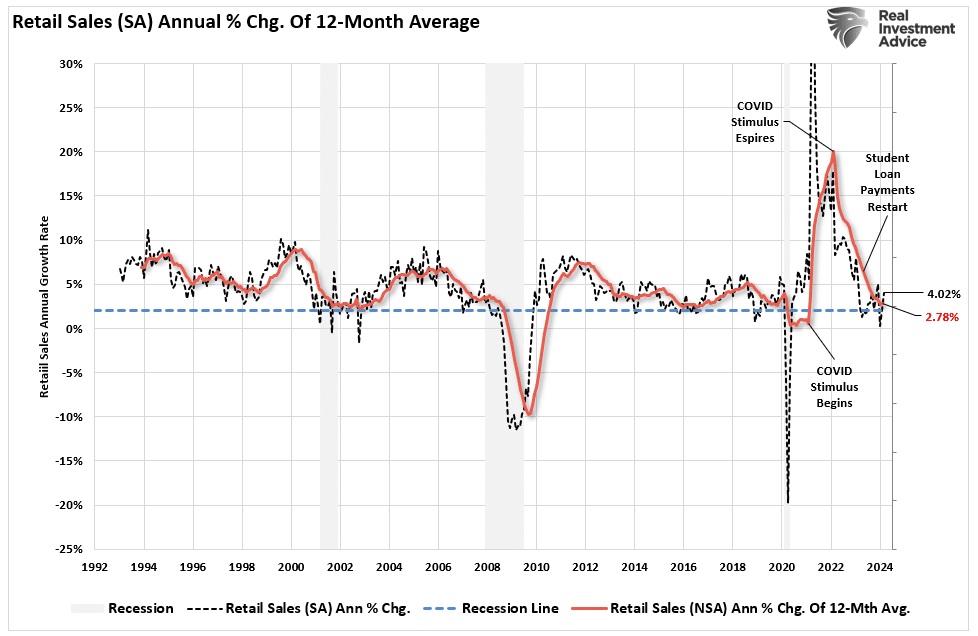

Furthermore, the 12-month average of the non-seasonally adjusted spending data should be examined, removing all the seasonal adjustments and manipulations. We find that retail sales growth is substantially weaker than reported. Given that the reported numbers follow the unadjusted average, we will likely see weaker sales numbers heading into summer.

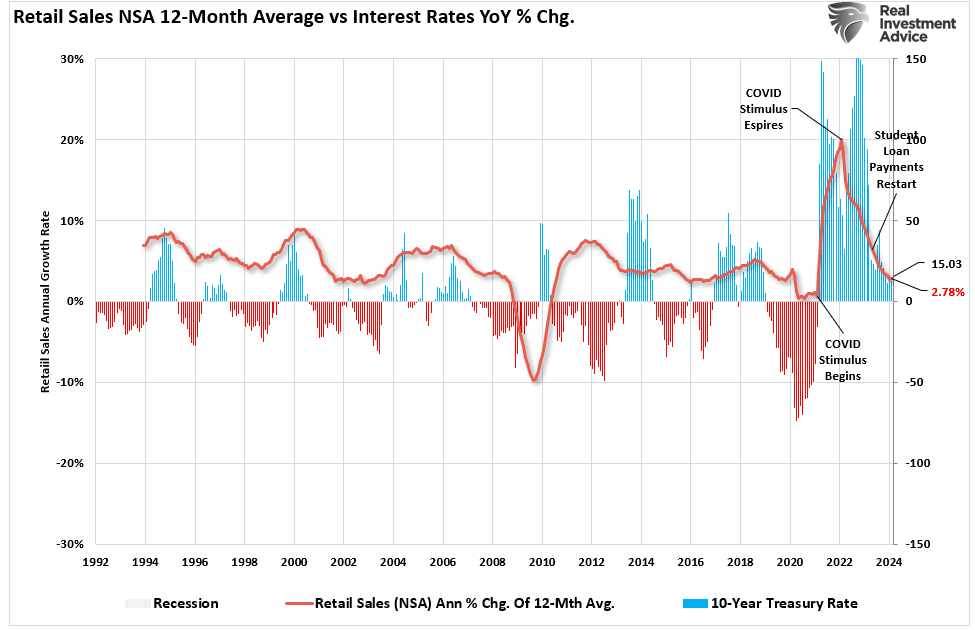

Notably, if retail sales slow down as they appear, interest rates will continue to follow. The chart below compares the 12-month average of retail sales to the annual change in interest rates. Over the months ahead, as retail sales and the overall economy continue to slow, interest rates will follow.

While interest rates are rising due to speculative market actions, the sustainability of higher rates is problematic for consumers and a heavily indebted economy.

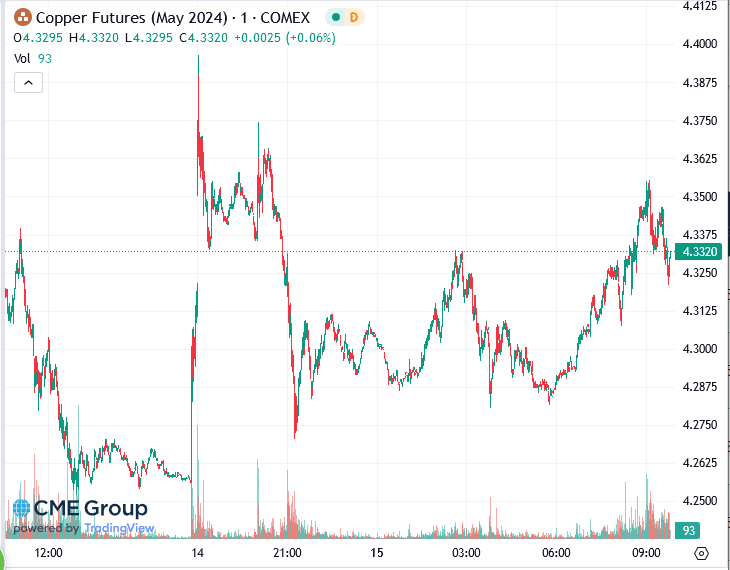

Industrial Metals Rally On Russian Sanctions

In further efforts to reduce Russia’s sources of military funding, the U.S. and British governments are banning Russian exports of nickel, aluminum, and copper. Further, the Chicago Mercantile Exchange (CME) and London Metal Exchange (LME) will make deliveries of the three metals produced by Russia ineligible for futures contracts. For context, Russia accounts for about 5% of the production of all three metals. On the margin, the ban may further add to price pressures. But keep in mind the markets for these metals are global. Therefore, China will buy more metals from Russia, while the U.S. and Britain buy more from other producers. Accordingly, the sanctions should have little effect on prices in the long run.

The prices of the metals spiked on the news but have since given back some of the gains. The graph below shows that Copper prices were up by about 4% when the news was released. However, it has retreated since then. Aluminum is up 2.5% but also down decently from Sunday night’s highs.

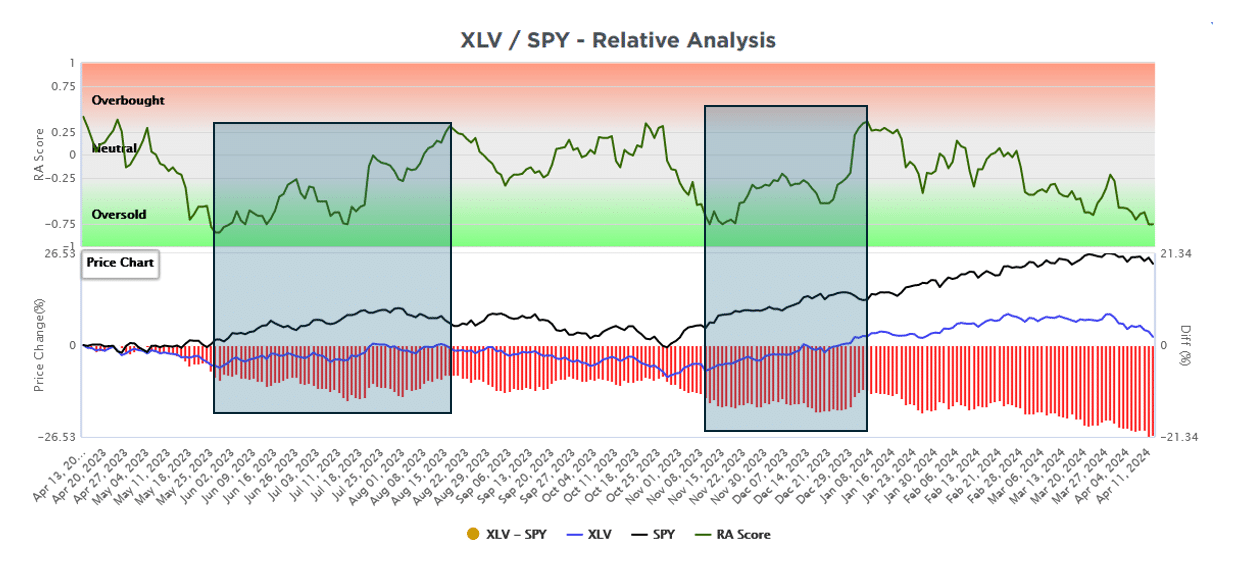

Healthcare Stocks Are Very Oversold, But…

The SimpleVisor graph below shows our proprietary SimpleVisor relative technical score (green line) for the healthcare sector (XLV). The black and blue lines in the lower chart show the prices of XLV and SPY. The red bars show XLV’s relative performance. The top chart highlights the two prior instances when XLV was as oversold as it is today versus the S&P 500.

Given the significant oversold level, is it worth adding to healthcare on a relative basis?

The answer is maybe. The boxes show that the prior deeply oversold periods only produced marginal relative outperformance. These periods of consolidation of the XLV/SPY ratio allowed the technical gauges to become more balanced. If this instance marks an actual trend change and not a consolidation in a lower trend, we may be nearing a period to buy XLV versus SPY. Breaking into overbought territory might signal such a trend change.

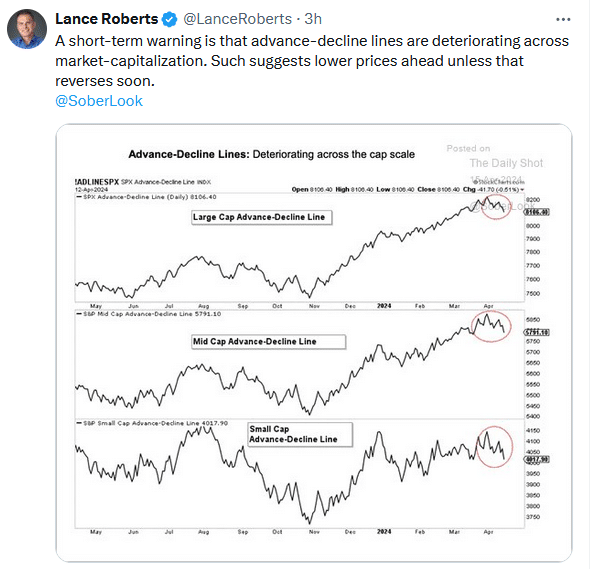

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.