Rumors were flying on Friday that a likely invasion of Kyiv by the Russians is imminent. PBS claims Russian President Putin has communicated invasion plans to his military. President Biden says a Russian invasion could come anytime. The early beneficiaries of a possible Russian invasion appear to be gold, bonds, and the dollar. Stocks languished on the news. Further weighing on stocks was the announcement of a special Fed meeting on Monday morning. Investors are concerned the Fed may raise rates before the March 16th meeting.

[dmc]

What To Watch Today

Economy

- No notable reports scheduled for release

Earnings

Pre-market

- TreeHouse Foods (THS) to report adjusted earnings of $0.10 on revenue of $1.12 billion

- Weber Inc. (WEBR) to report an adjusted loss of $0.07 on revenue of $310.71 million

Post-market

- Vornado Realty Trust (VNO) to report adjusted earnings of $0.75 on revenue of $1.8 billion

- Avis Budget Group (CAR ) to report adjusted earnings of $6.07 on revenue of $2.29 billion

- Arista Networks (ANET) to report adjusted earnings of $0.74 on revenue of $790.8 million

- Advance Auto Parts (AAP) to report adjusted earnings of $1.95 on revenue of $2.36 billion

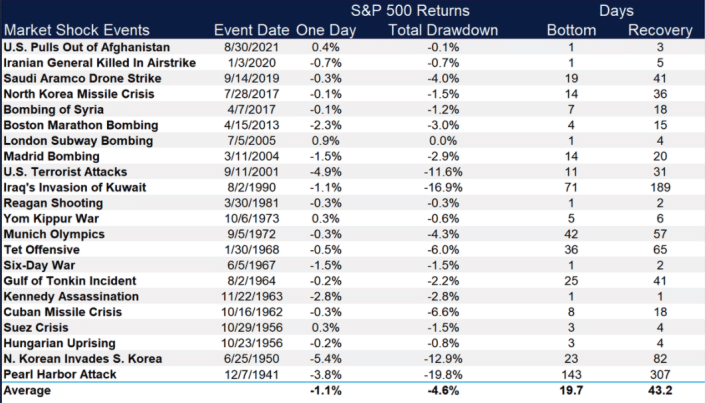

How Does The Market React To Geopolitical Events

The headlines over the Russian invasion will eventually be much to do about nothing. Russia has no real intention of invading the Ukraine and only really wants to ensure that the Ukraine does not become a member of NATO. In the meantime, while President Biden stumbles along in negotiations with Russia, the markets remain under duress.

“Over at LPL Financial, data cruncher Ryan Detrick highlights how the stock market has historically reacted to major geopolitical events such as the one that developed on Friday with Russia that sent stocks tanking. The takeaway: Stocks bounce back from these events.” – Yahoo Finance

The takeaway is not to let media-driven headlines deter you from your investment strategy.

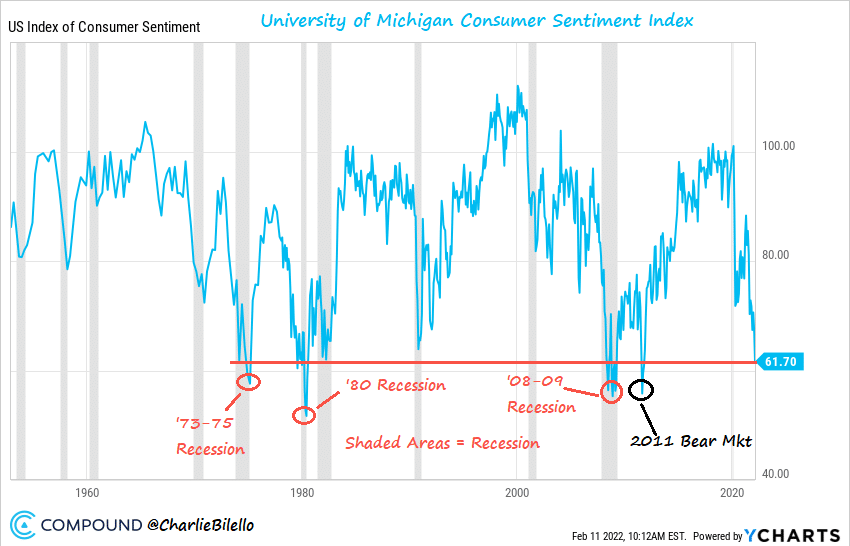

Consumer Sentiment Plummets

The University of Michigan consumer sentiment survey fell sharply to 61.7 from 67.2. It is now below March 2020 and at levels rarely seen in the last 50+ years. The index was expected to increase slightly. Inflation is likely weighing on consumers. The Michigan one-year inflation expectation index rose from 4.9% to 5%.

The Week Ahead

This will be a busy week chock full of economic data. Another dose of inflation data comes Tuesday with the PPI report. Year over year PPI is expected to rise from 8.3% to 8.5%. Import and export prices along with retail sales will follow on Wednesday. We will get housing data, jobless claims, and the Philly Fed Index on Thursday. As the regional Fed surveys come out, much attention will be paid to their inflation sub-indexes.

Fed Presidents Waller and Williams will speak on Friday morning. Both have been very hawkish in prior speeches. Given the uptick in inflation, we suspect they will discuss raising rates by 50bps at the March meeting and starting QT very soon.

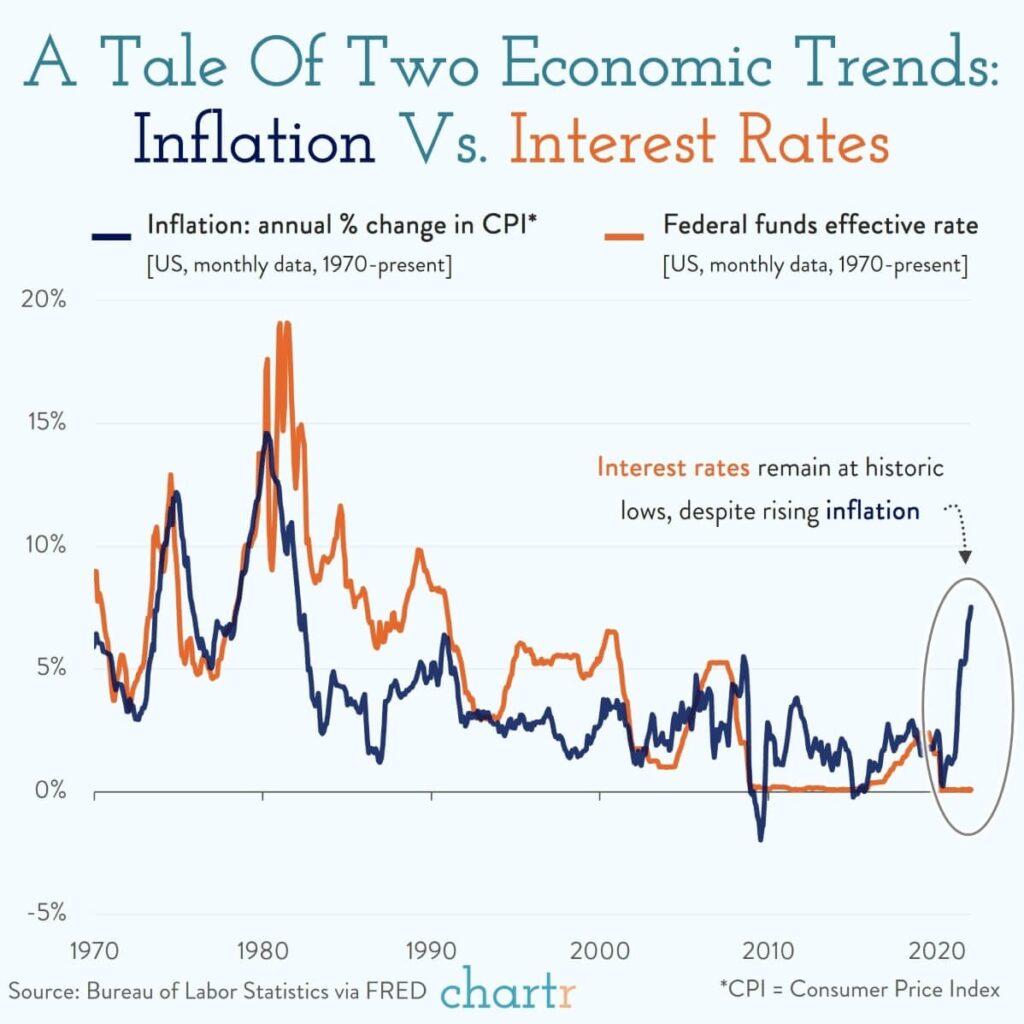

A Tale Of Two Trends

Yesterday the latest data hit the tape, with the Consumer Price Index up 7.5% on this time last year – another 40-year record jump.

Rising prices can be a scary self-perpetuating cycle. Prices go up, so firms raise prices in response, which makes other prices go up and so on and so forth. The big lever that the Federal Reserve has is the Federal Funds interest rate, which can help restrict, or expand, the amount of credit in the economy — but interest rates remain anchored to historic lows, just above zero.

That’s not going to be the case forever, and investors are quickly shifting their expectations. Investors have been expecting two, maybe three, rate hikes this year, but this latest data has investors wondering whether the Fed might do a “double hike” at the next meeting, which would raise interest rates by 0.5%, instead of the more usual 0.25% bump. The last time the Fed did a double hike? May 2000. – Chartr

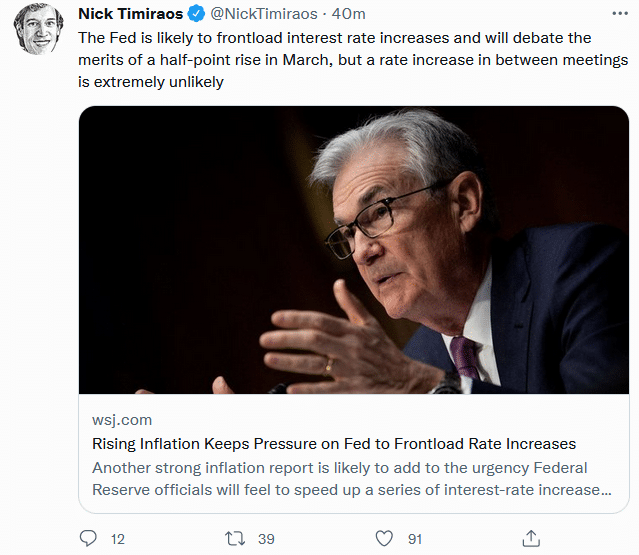

The Fed Quells Rumors of Intra-meeting Rate Hike

After Thursday’s bond debacle, rumors were flying the Fed would raise rates and end QE before the March 16th FOMC meeting. The day after, the Fed’s mouthpiece, Nick Timiraos of the Wall Street Journal, quelled such rumors in Rising Inflation Keeps Pressure on Fed to Frontload Rate Increases. As Nick tweets- “but a rate increase in between meetings is extremely unlikely.”

Interestingly, later that day, the Fed announced a special meeting for Today. The topic- “Review and determination by the Board of Governors of the advance and discount rates to be charged by the Federal Reserve Banks.” We are not sure what to make of it, but the stock market is getting anxious.

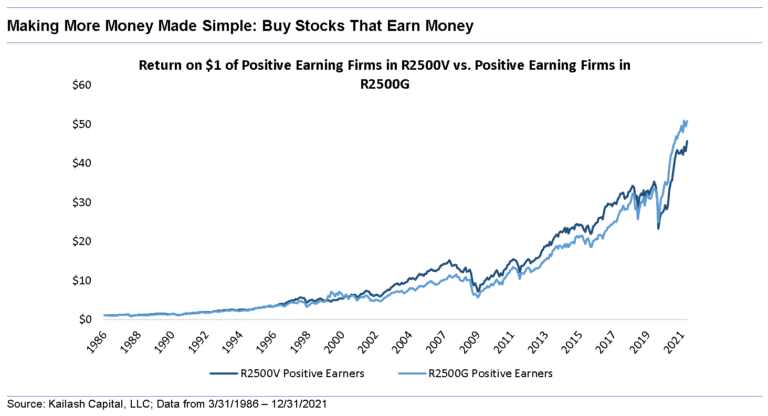

Want To Make Money, Buy Companies That Make Money

KCR’s research team recently wrote that Growth at a Reasonable Price had never looked more compelling than it does today. The core tenet of that research was identifying firms with increasing profitability at modest valuations.

The chart below shows the compound returns to merely buying the stocks in the R25G and R25V that are profitable over time. You can see that despite the recent explosive returns in the growth stocks, value is still tied with growth over the long haul. This is consistent with the conclusions from our research on how to find safe investments.

The data provides a powerful and simple message: when you buy a stock, does it make money? A simple “yes” is a surprisingly good starting place for any investment process!

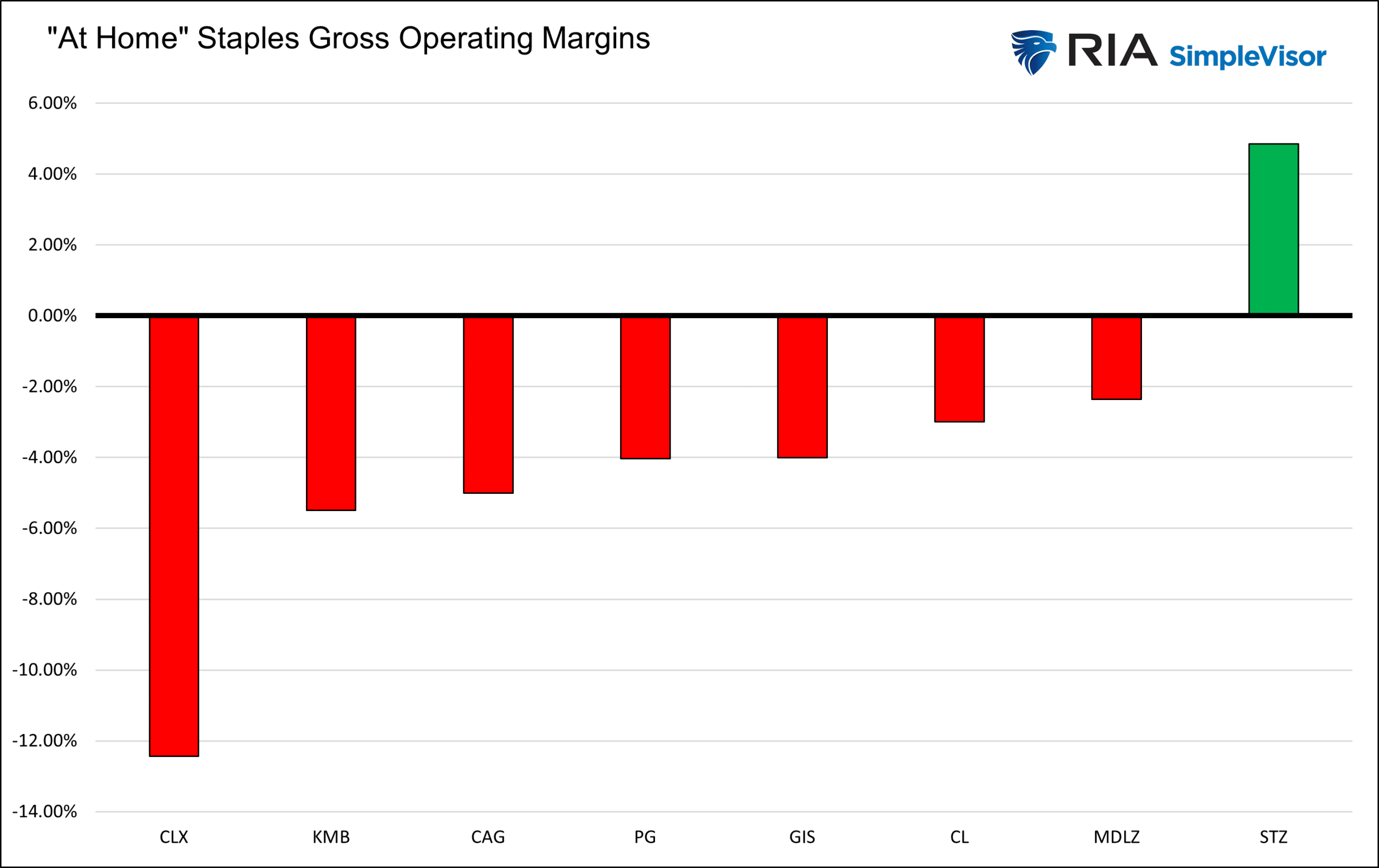

Can Consumer Staples Companies Pass On Inflation To Consumers?

Which companies can pass on inflation to their customers and keep profit margin intact? The Consumer Staples sector may be the most affected by inflation as they face sharply rising prices for many of their input goods. The graphs below show larger staples companies and the change in their gross operating profit margins from the most recent fourth quarter to the 2020 fourth quarter. Gross operating profit is simply sales/revenue less the cost of goods sold. The first graph below shows the year-over-year change in gross profit margin for the top holdings of XLP (Consumer Staples). The second graph hones in on companies that primarily sell directly to consumers. As shown, many companies that sell consumer goods have declining gross profit margins. We could not run the analysis on quite a few companies as they have not released Q4 earnings.

We will write an exhaustive report on most sectors and underlying companies once the earnings season is over.

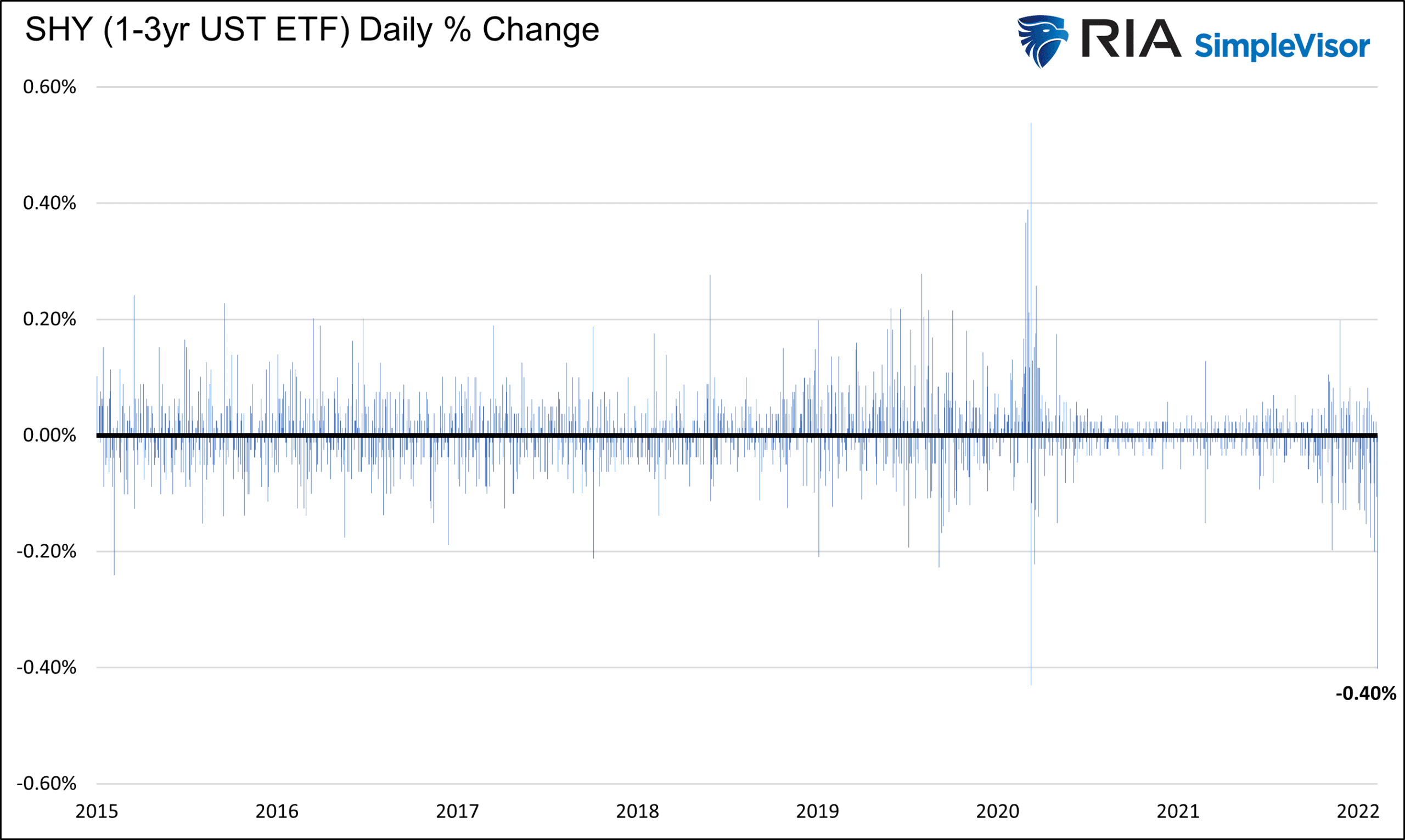

The 100-Year Storm Hits Bonds Again

The graph below showing the daily percentage gains and losses in bonds highlights the magnitude of Friday’s 25bps yield increase in short-term Treasury bonds. As shown, our proxy for short-term bonds, SHY (1-3 year UST ETF), lost .40% yesterday. The only other time it had such a loss in the last five years was during the early days of the Pandemic. Based on price data going back 20 years, the percentage change was a 4.5 standard deviation move. Statistically, such a move should occur once every 135 years. Since 2002, SHY has declined by more than .40% eleven times.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.