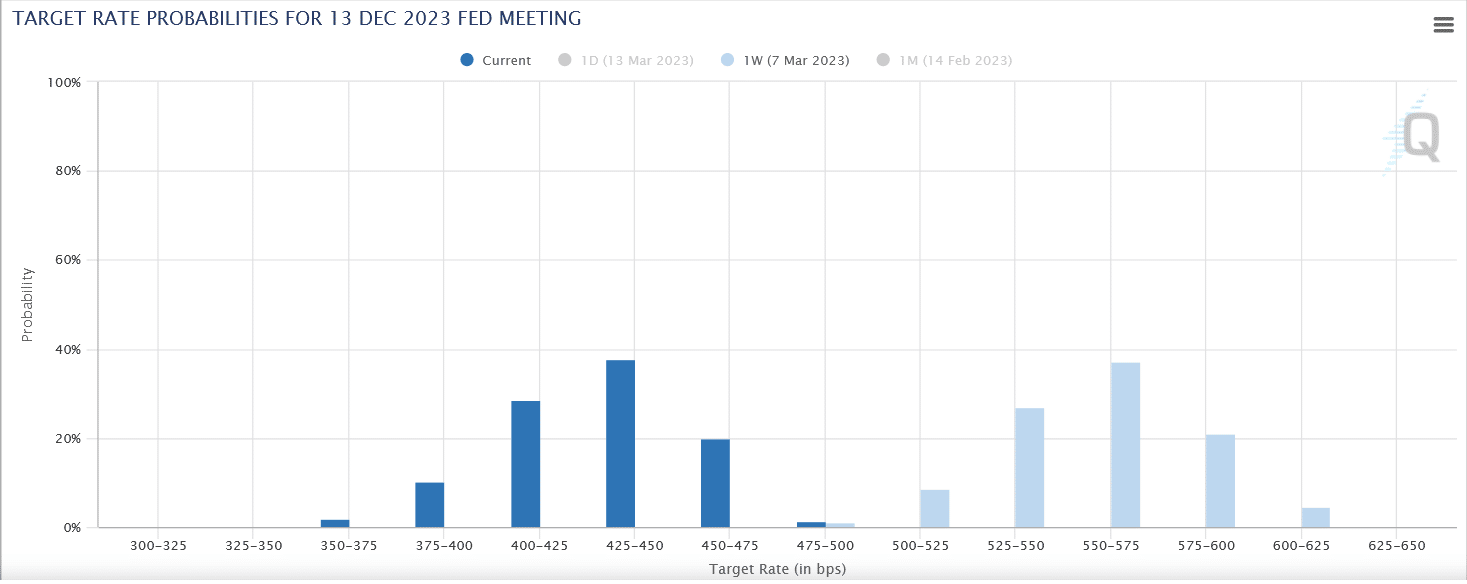

Less than a week after Jerome Powell was pounding the table on Capitol Hill, arguing the Fed must stay aggressive in its inflation fight, the market thinks the Fed is about to make an abrupt pivot and drop the Fed Funds rate rapidly. The graph below compares expectations for Fed Funds on March 7 (light blue) and today (dark blue). Remarkably, Fed Funds futures imply a pivot, with rates ending the year about 1.25% lower than expected seven days ago.

Markets are trying to figure out what the Fed now thinks. Will they agree that the banking crisis was a warning shot and they must pivot to lower interest rates to ensure the problems don’t multiply? If they were to take such action, would that destroy all credibility they have earned regarding being steadfast against high inflation? Also, if investors grow concerned that the Fed will not fight inflation, will the dollar sink, gold and commodities rise, and long-term yields increase? There are a lot of crucial questions that need to be addressed. We hope our visibility into Fed priorities clears up between now and the 3/22 Fed meeting. Until then, prudence is likely the best course of action.

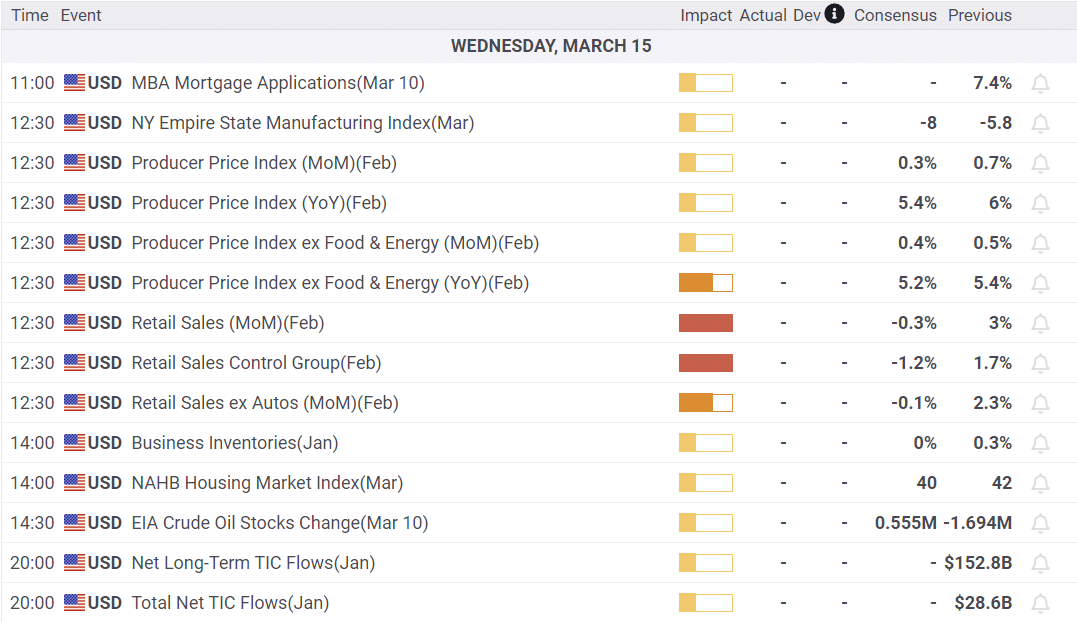

What To Watch Today

Economy

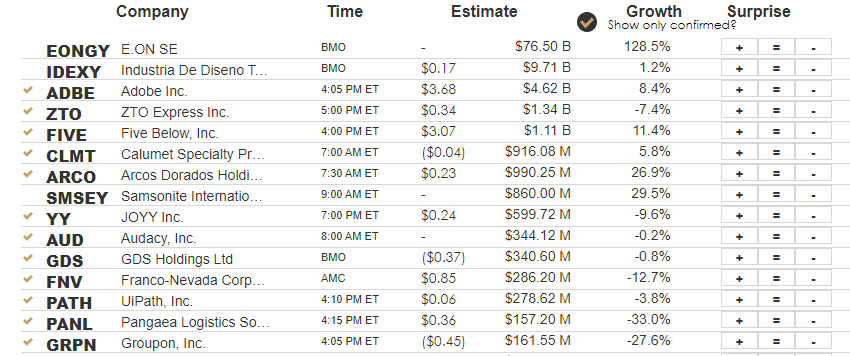

Earnings

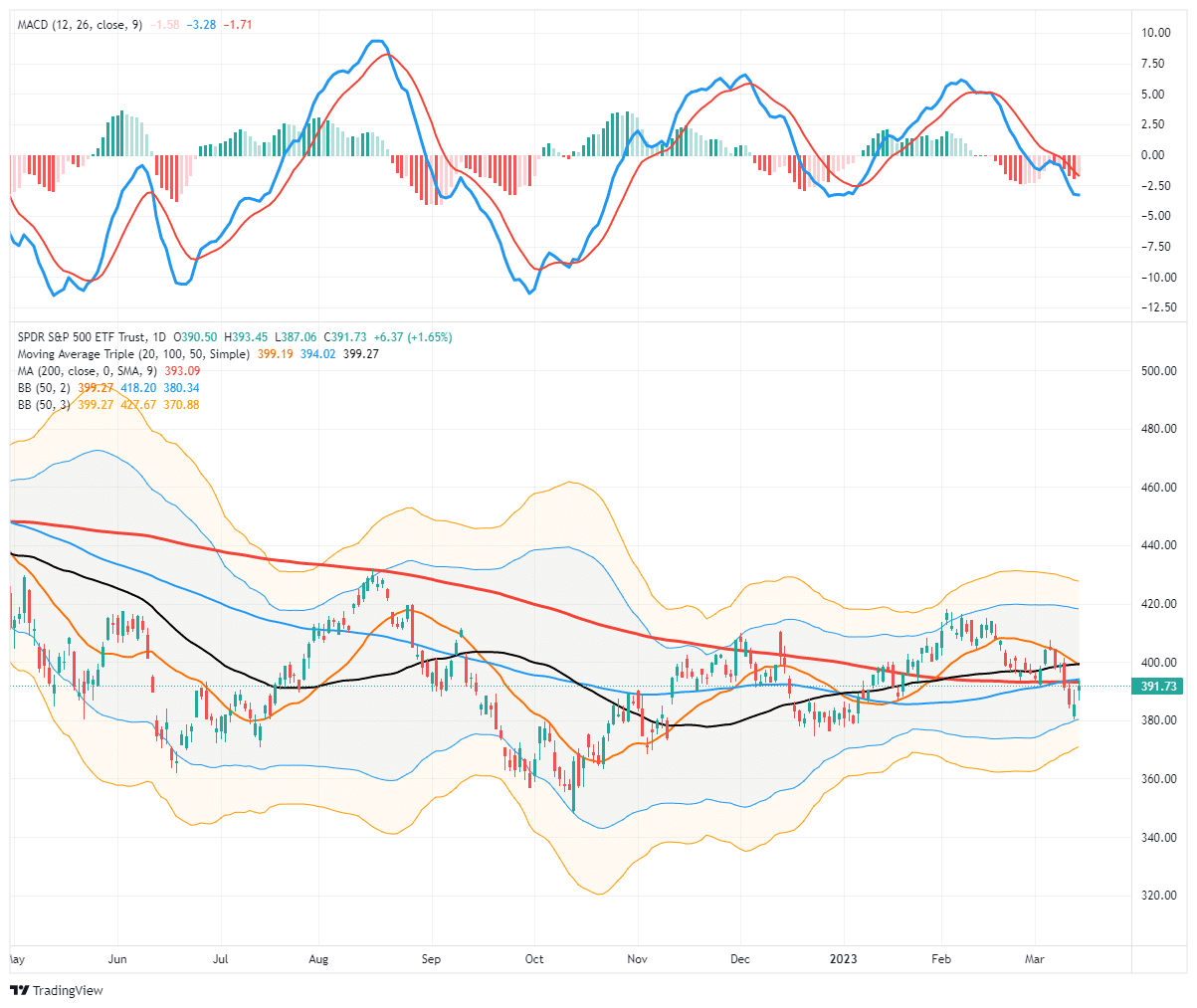

Market Trading Update

With the bailout pulling some of the stress off the financial sector, the market’s oversold condition allowed for a rally yesterday. The rally failed at the 200-DMA, its first attempt to reclaim broken support. Such initial failed attempts happen often, but the market must retake that resistance by the end of this trading week. A weekly close below the 200-DMA will suggest bears have regained control of the market short term.

We continue to suggest taking profits and reducing equity risk unless, or until, the market regains a more bullish footing. With next week’s Fed meeting, traders will likely remain cautious, limiting the upside for now. Also, our MACD “sell signal” remains firmly intact, suggesting that risk is to the downside.

CPI on the Screws

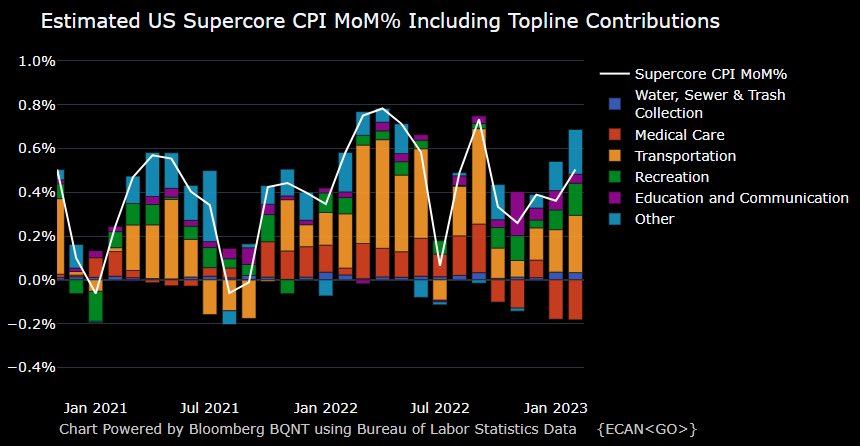

CPI came in largely as expected, with the monthly rate climbing 0.4% and the year-over-year rate falling from 6.4% to 6.0%. The monthly core CPI was .10% more than expectations and last month’s reading. At 0.5%, core CPI is running at a 6.0% annualized rate and appears sticky at current levels. Further supporting the stickiness of inflation theory are core service prices, excluding housing. The Fed has signaled that this indicator is their preferred gauge to determine the stickiness of prices. As shown below, the so-called Supercore CPI has risen three months in a row and shows no signs of ebbing.

The Fed claims they are “data dependent” in its monetary policy moves. The CPI data, on its own, provide no reason for the Fed to back off its hawkish stance. As such, how will they balance data dependency with the banking crisis? Last week wrote Speak Loudly Because You Carry A Small Stick to discuss the Fed’s predicament. Per the article:

Given the lag effect of prior rate hikes and the massive leverage embedded in the economy, we advise Jerome Powell to speak very loudly but take limited further action regarding rate hikes.

Our concern was the damage higher rates would do and the lack of ability to foresee economic or financial problems. As such, we advise the Fed to take it easy on rate hikes but be as hawkish as possible. Furthermore, with the new bank crisis, our advice is more important. At next week’s FOMC meeting, we expect the Fed to issue a strongly worded warning about the need to get inflation back to its target of 2%. At the same time, they may bring up pausing, so they don’t worsen the banking crisis. The situation is fluid, but as of today, we suspect they will increase by 25bps next week but emphasize flexibility.

Bank Runs

Seemingly out of nowhere, bank runs took down the nation’s 18th-largest bank and several smaller regional banks. Bank runs, even for the soundest bank, are always a risk. The simple fact is that banks run a Ponzi scheme of sorts. Lance Roberts explains why in his latest article- Bank Runs. The First Sign The Fed “Broke Something.” Per Lance:

“Bank runs” are problematic in today’s financial system due to fractional reserve banking. Under this system, only a fraction of a bank’s deposits must be available for withdrawal. In this system, banks only keep a specific amount of cash on hand and create loans from deposits it receives.

The problem facing banks is not one of trust, as is typical of a bank run. Instead, it’s customers can earn more yield elsewhere. Total banking deposits fell annually for the first time since 1948. Depositors are shifting money to money market funds and Treasury Bills to capture 4+% interest rates. This is just one of the unintended consequences of the Fed not tightening monetary in 2021 when the seeds of inflation were sown. As a result of acting too late, they had to raise rates higher than they might have. The bank run, and likely other economic and financial problems, are and will be the consequences.

Junk Bond Investors Finally See Risk

On February 24, 2023, and on a few other occasions, we wrote about low corporate bond market yields and our concern that poorer credit quality bond prices were not accurately reflecting enhanced risks. The February Commentary warned that corporate bond investors were “picking up pennies in front of a steam roller.” The graph below shows that the junk bond yield spreads versus U.S. Treasuries rose about 1% in the last few days. It appears a few investors hear the steamroller coming!

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.