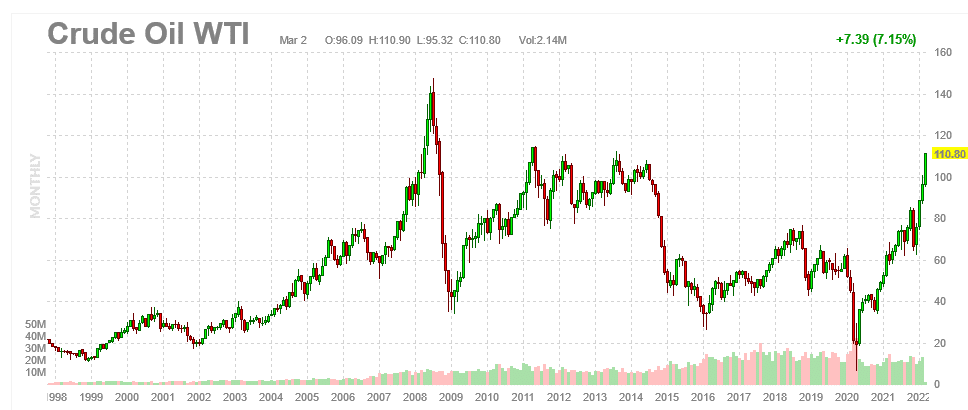

Stocks rebounded despite a somewhat hawkish Congressional testimony by Powell and soaring crude oil prices. The culprit behind yesterday’s soaring oil prices is OPEC. They decided not to increase production beyond the amounts they agreed upon months ago. As shown below, crude oil hit $110 a barrel on Tuesday. Jerome Powell testified to Congress on the state of monetary policy. For an excellent summary, check out Mish Shedlock’s review. Stocks were unphased by soaring oil prices and Powell’s hawkish testimony. Keep in mind; however, stocks are oversold technically. Further, investor sentiment is at historically low levels. The bounce may continue, but significant resistance lurks overhead.

[dmc]

What To Watch Today

Economy

- 7:30 a.m. ET: Challenger Job Cuts, year-over-year, February (-76.0% during prior month)

- 8:30 a.m. ET: Non-farm Productivity, fourth quarter final (6.6% expected, 6.6% prior)

- 8:30 a.m. ET: Unit Labor Costs, fourth quarter final (0.3% expected, 0.3% prior)

- 8:30 a.m. ET: Initial Jobless Claims, week ended Feb. 26 (225,000 expected, 232,000 during prior week)

- 8:30 a.m. ET: Continuing Claims, week ended Feb. 19 (1.4 million expected, 1.476 million during prior week)

- 9:45 a.m. ET: Markit US Services PMI, February final (56.7 expected, 56.7 prior)

- 9:45 a.m. ET: Markit US Composite PMI, February final (56 prior)

- 10:00 a.m. ET: ISM Services Index, February (61.1 expected, 59.9 during prior month)

- 8:30 a.m. ET: Durable Goods Orders, January final (1.6% prior)

- 8:30 a.m. ET: Durable Goods Orders Excluding Transportation, January final (0.7% prior)

- 8:30 a.m. ET: Capital Goods Orders Nondefense Excluding Aircrafts, January final (0.9% prior)

- 8:30 a.m. ET: Capital Goods Shipments Nondefense Excluding Aircrafts, January final (1.9%)

Earnings

Pre-market

- Toronto-Dominion Bank (TD) to report adjusted earnings of C$2.04 on revenue of C$10.17 billion

- BJ’s Wholesale Club (BJ) to report adjusted earnings of 76 cents on revenue of $4.42 billion

- Best Buy (BBY) to report adjusted earnings of $2.72 on revenue of $16.59 billion

- Kroger (KR) to report adjusted earnings of 72 cents on revenue of $32.98 billion

Post-market

- Marvell Technology (MRVL) to report adjusted earnings of 48 cents on revenue of $1.32 billion

- Broadcom (AVGO) to report adjusted earnings of $8.13 on revenue of $7.61 billion

- Costco (COST) to report adjusted earnings of $2.58 on revenue of $51.47 billion

- Gap (GPS) to report adjusted losses of 14 cents on revenue of $4.49 billion

- Vizio (VZIO) to report adjusted losses of 18 cents on revenue of $691.46 million

- Sweetgreen (SG) to report adjusted losses of 66 cents on revenue of $84.68 million

Market Update – Stocks Rally On Good News

As discussed over the last few days, the market rallied after the initial invasion of Ukraine. With the markets not overbought as of yet, and sentiment still bearish, the market rallied yesterday, even as oil soared, as Powell noted he would only increase rates by 0.25% at the next meeting. This softer stance, as expected, gave the markets room to run.

Resistance is currently at the intersection of the downtrend line and the 200-dma. Above that is resistance at the declining 50-dma. We are still in correction mode which is why we are maintaining decreased equity exposures for now.

Employment – ADP

The ADP Employment Report was genuinely shocking as they revised January’s -301k number to +509k. For February, ADP reports that 475k additional new jobs. The robust jobs market is weighing on small companies. Per the report- “Small companies lost ground as they continue to struggle to keep pace with the wages and benefits needed to attract a limited pool of qualified workers.” To that end, “Private sector small business employment decreased by 96,000 jobs from January to February according to the February ADP Small Business Report.” The current estimate for Friday’s BLS jobs report is for a gain of 400k jobs, down from 467k last month but still incredibly strong.

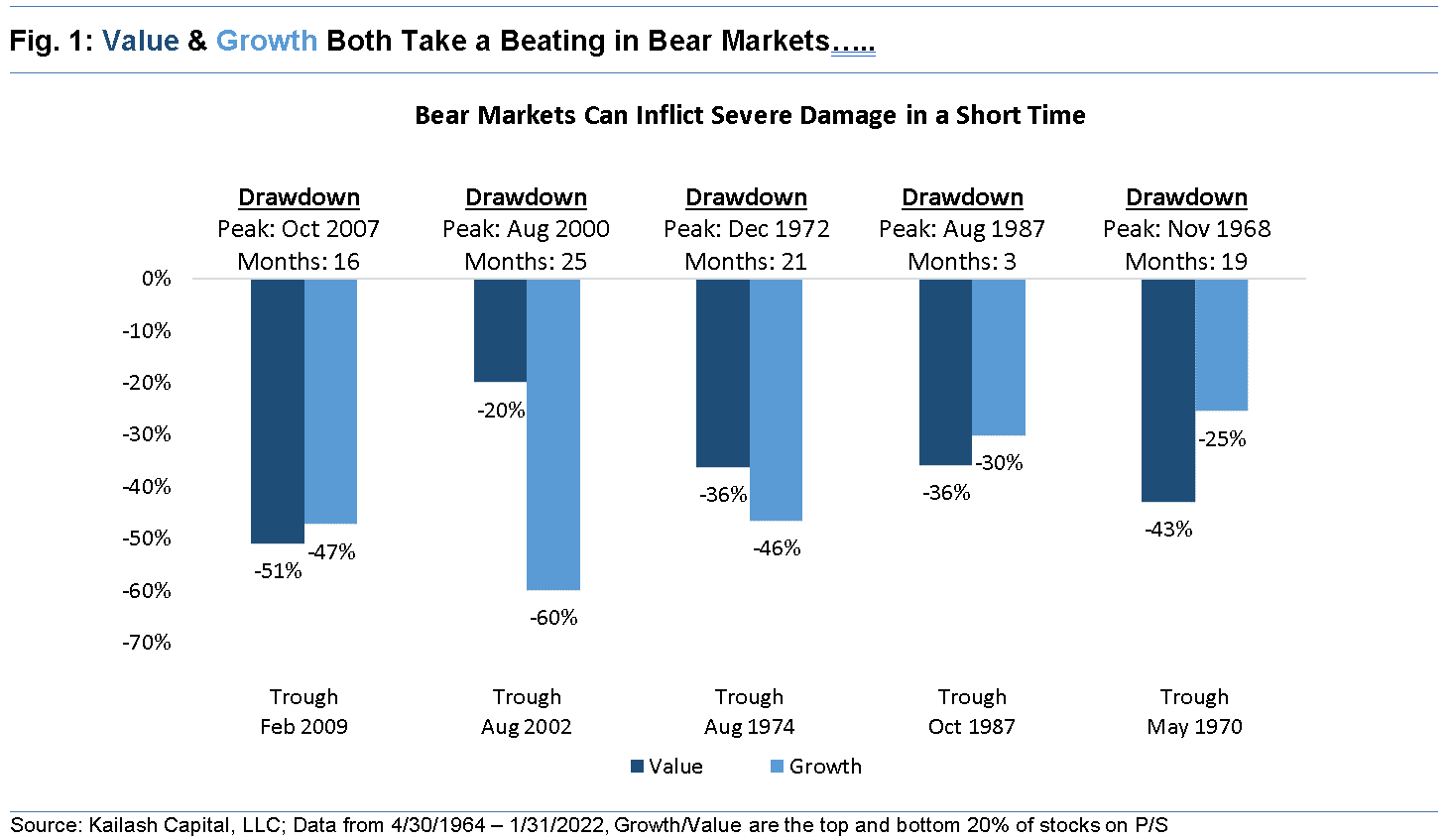

Value Vs Growth In Bear Markets – No Safe Place Hide

“To our knowledge, nobody can predict the frequency of bear markets, but we do know that all bull markets do eventually end. Our research has demonstrated that valuation levels today are at record highs. This problem is exacerbated by a dearth of safety and protection in fixed income markets.

The chart below shows how value and growth stocks fared in the bear markets we referenced in Bear Traders. KCR believes the message is simple: even in the shortest bear market of 1987, the losses were severe.” – Kailash Concepts

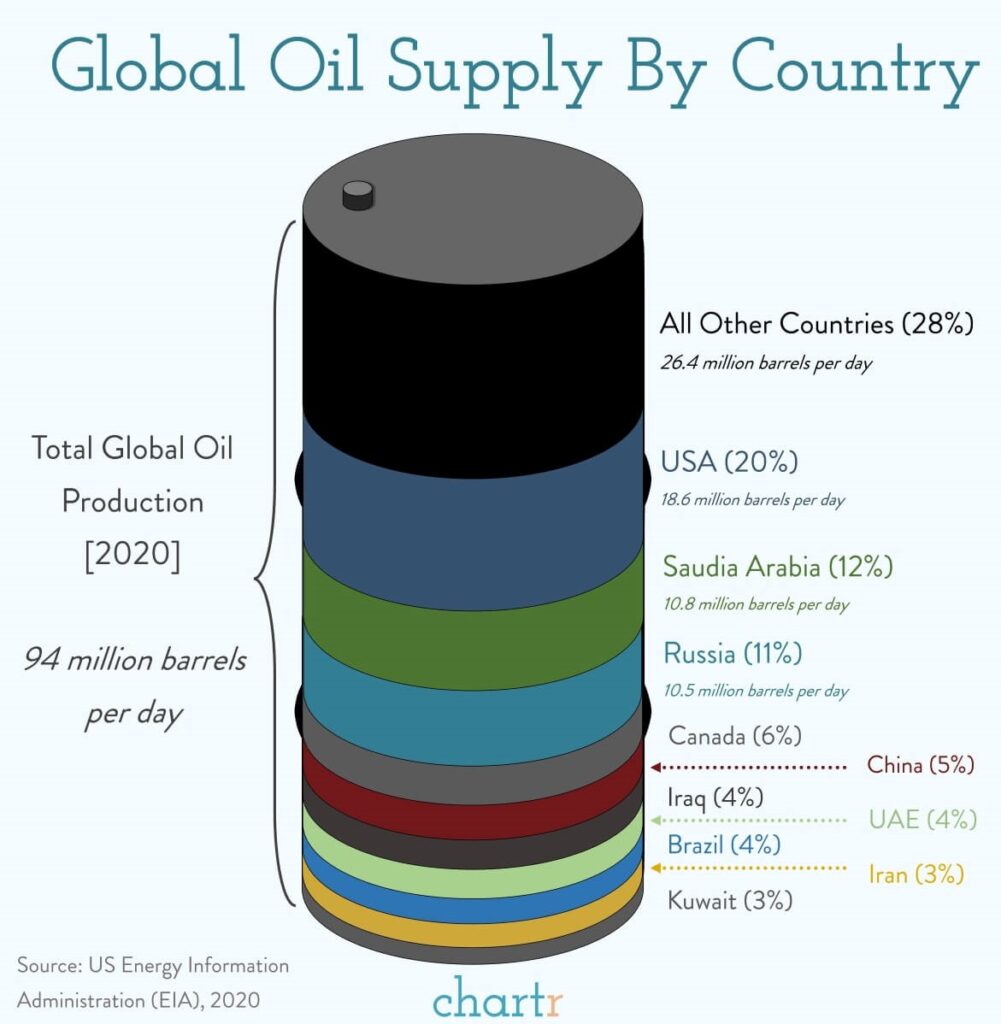

Global Oil Supply – Where Does it Come From

As oil soars, we thought this piece by Chartr showing the breakdown of oil supply was useful.

“The price of Brent crude oil, the widely-used global benchmark, spiked to more than $113 per barrel this week — its highest level in almost 7 years and a far cry from the (briefly) negative oil prices that we saw in April 2020.

Although the west has yet to target Russia’s enormous energy sector specifically, investors are now clearly expecting some kind of disruption to Russia’s significant production. In 2020 Russia produced more than 10 million barrels of oil per day, which is roughly 11% of global supply, only behind the US and Saudi Arabia.

Interestingly, according to analysts at Commerzbank, Russia’s Urals oil grade is now trading at an $18 per barrel discount to Brent crude oil as buyers skip Russian oil in favor of other exporters, for fear of future sanctions.” – Chartr

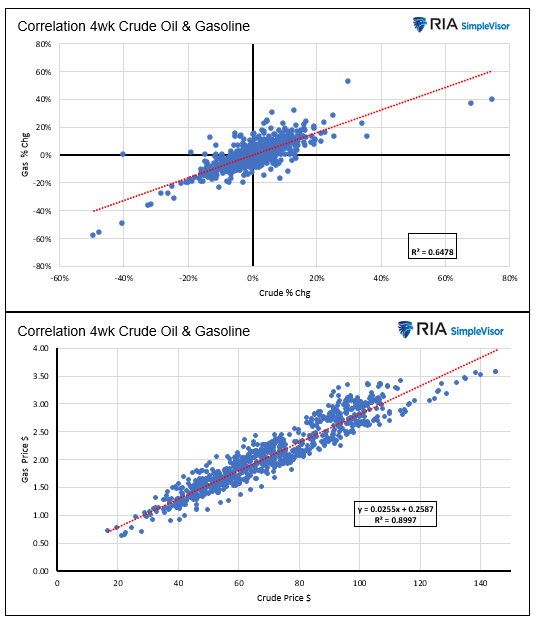

Crude Oil and Gasoline

The graphs below show the strong correlation between crude oil and gasoline futures. Based on the trendline in the second graph, each $1 increase in the price of crude oil should result in a 2.5 cent increase in the price of gasoline futures. Keep in mind the charts use gasoline futures which is not the price we pay at the pump. Storage, transportation, taxes, and profit margins add to the retail price. Since 2006, the average difference between gas futures and retail prices has been 75 cents. With gasoline futures trading at $3.25, most of us should expect gas prices to eclipse $4 shortly. The last time consumers grappled with $4 gas was in mid-2008 when crude oil reached $150, and the economy was in a recession.

Lower Inflation Coming?

The graph below provides a little optimism that the supply line problems and shortages that plagued the economy for over a year and drove up prices may be coming to an end. Keep in mind the supply line problems are abating as demand is waning, potentially providing a one-two punch to inflation. We would be remiss, however, if we didn’t mention the inflationary elephant in the room, that is the Russian invasion and the soaring price of oil.

Rut Roh!

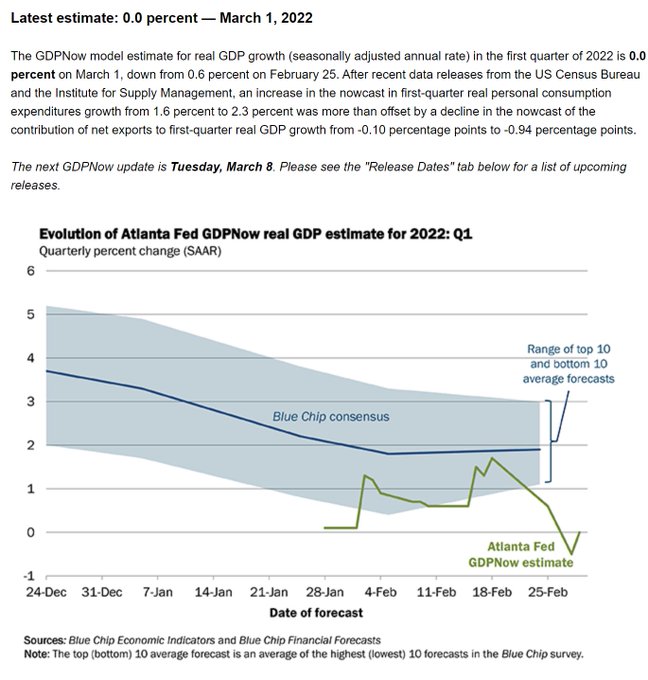

As shown below, the Atlanta Fed GDPNow forecast now calls for 0% economic growth in the first quarter. The troubling part is that the forecast comes largely from January data. Most February data, other than some manufacturing indexes, is not out yet. As such, the economic effect of soaring $100+ oil prices and additional Russian invasion-related inflation is not incorporated into economic data. Consumer Sentiment is likely to slip throughout the quarter due to gas prices and inflation.

The other important consideration for investors is the Fed will likely raise rates as the economy potentially slips into a recession. The combination of high inflation, weak economic growth, and a hawkish Fed has not been witnessed in this country for over 40 years! This time is different. As such, you may want to prepare in case the bull market of the last decade-plus falters. Our latest article walks readers through the bear markets of 2000-03 and 2008-09 to better appreciate how bear markets differ from bull markets. Bear Market Strategies- Are You Ready?

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.