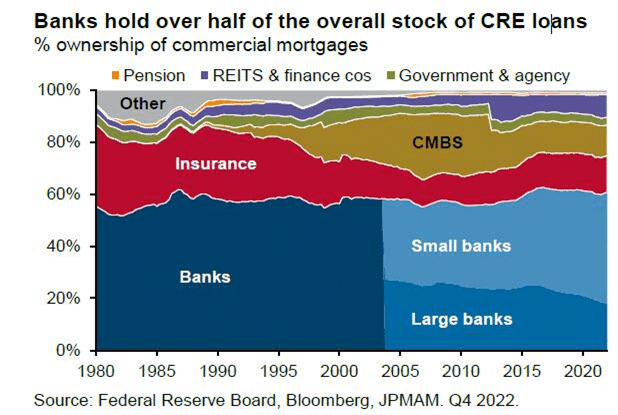

Regional bank woes have thus far been a function of interest rate risk, not credit risk. By this, we mean the banks made loans or bought debt assets with low-interest rates. As rates increased, the value of said loans declined. When deposits left these banks, the assets had to be sold, resulting in losses. With interest rates remaining high and depositors continuing to move money from banks to money market funds, interest rate risk remains a threat. As if that wasn’t enough risk for some banks, some will soon have to deal with the possibility of credit losses due to a record-high office vacancy rate.

The graph below shows that banks hold about 60% of commercial real estate (CRE), i.e., office space. Of that, smaller banks hold over two-thirds. The U.S. metro office space vacancy rate is now 18.7%, a new high. It has also been reported that rent is unpaid on approximately one-fifth of office space. With over $400 billion of CRE debt maturing between now through 2025, regional banks are increasingly at risk they will have to realize credit losses. A possible recession coupled with the work-from-home movement and increasing office vacancies could spell trouble for some banks.

What To Watch Today

Earnings

- No notable releases today.

Economy

Market Trading Update

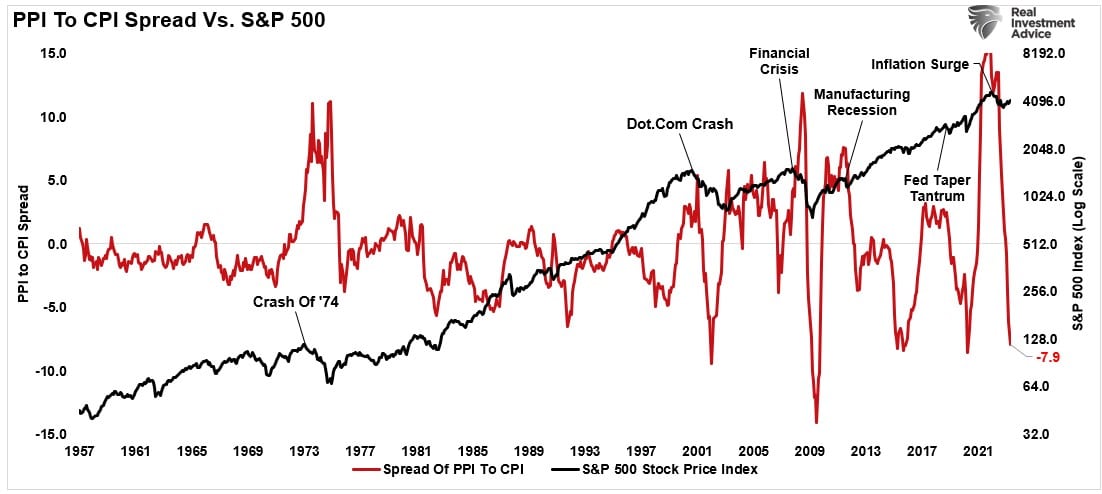

This week, both the CPI (consumer price index) and PPI (producer price index) showed inflation continues to decline as year-over-year comparisons become much easier. With the bulk of the high inflation rates caused by the shutdown behind us, inflation will continue to trend lower back to the long-term 2% target, which will align with lower economic growth rates in the future.

What was most notable was the massive collapse in the spread between CPI and PPI. That collapse has both bullish and bearish implications. From a bullish perspective, sharp declines in the spread have historically correlated to market lows, as expectations are that lower inflation will boost consumer spending. (Increasing spreads typically correlate with higher asset prices.)

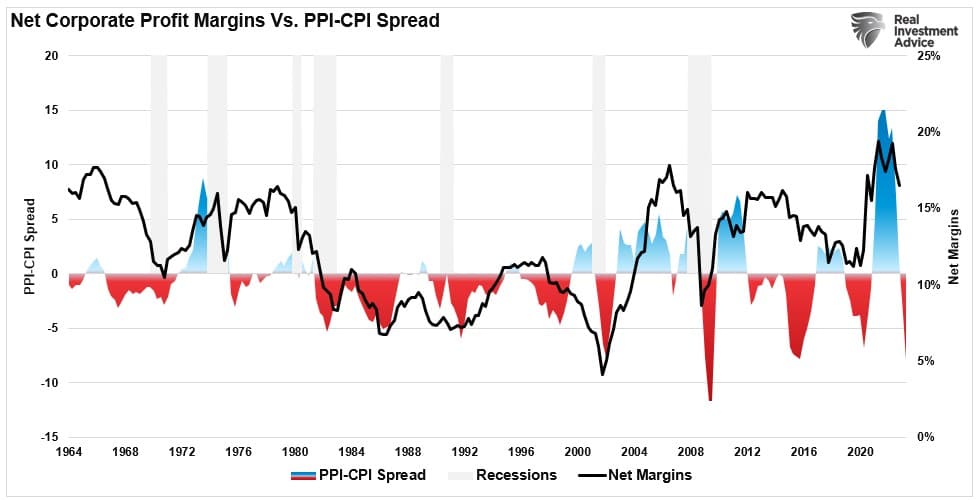

The bearish side of the collapse is that it suggests that companies’ net profit margins will likely remain under pressure as the ability to pass on higher costs will become more challenging.

We have not fully resolved the inflation issue yet, so the market’s upside will likely remain unchanged. Of course, such aligns with our comments from last week’s newsletter. To wit:

The market remains on a “sell signal” and again tested and held critical support at the 50-DMA and the downtrend support line from the April highs. The consistent test and holding of support remain bullish overall, and unless or until that is broken, the more bearish concerns are secondary.

With our sell signals still intact, we remain cautious for now. We noted last week that the “upside may be somewhat limited,” which was the case. However, we are now approaching more oversold levels with technically strong support. If we see an improvement in the price action, we suggest increasing exposure again accordingly. However, for now, that is not the case.”

Last week, such was the case as the market again struggled within a relatively tight trading range. Despite many bearish headlines, from more potential bank failures to weaker economic data, the market continues to trade bullishly. With moving averages sloping higher and downtrend support levels holding, we continue to grind away our current sell signal. It is important to remember that a market can correct excesses in two ways. The first is by declining in price. The second is by consolidating sideways.

So far, the correction has come as a consolidation, with the market continuing to cling to support at the 20-DMA. The rising trend line from the October lows is apparent as buyers step in on dips.

The Week Ahead

This will be a relatively quiet week, with Q1 earnings reports mainly behind us and inflation and unemployment data for April reported. The week’s big economic data point is retail sales on Wednesday. The market currently expects retail sales to increase by 0.6%. As discussed in the next section, it will be interesting to see if eroding consumer confidence reduces consumption.

Also of note this week, Chairman Powell will be speaking on Friday. Investors will want to see if his view from the last FOMC press conference has changed. If so, is he more dovish or hawkish?

Sentiment Erodes as Inflation Worries Heat Back Up

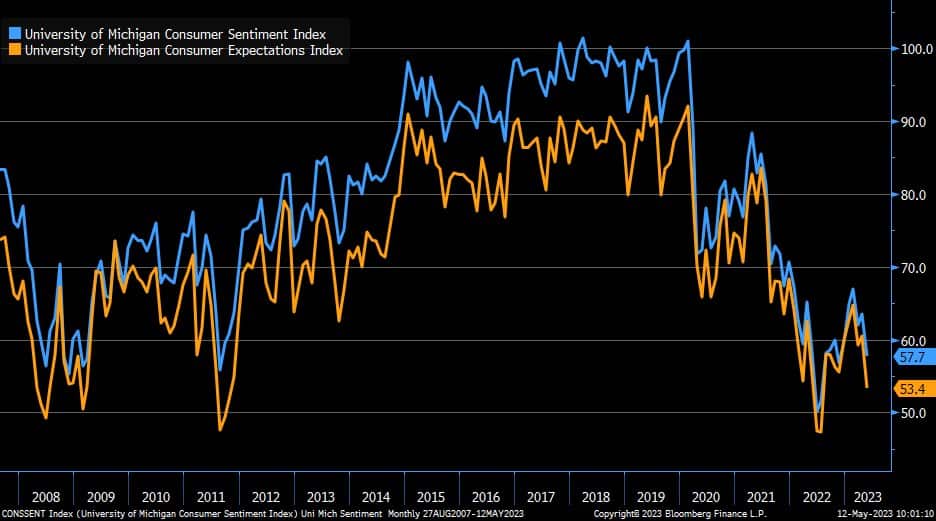

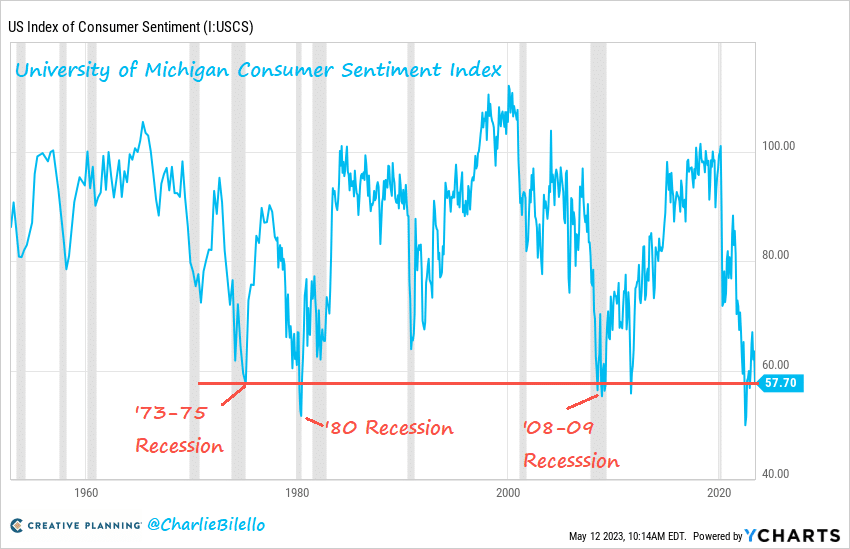

The University of Michigan Consumer Sentiment Survey fell sharply to 57.7 from 63.5. The likely culprit is a decent pickup in longer-term inflation expectations, not the regional banking crisis captured in last month’s survey. One-year inflation expectations were constant at 4.5%, but 5-10 year expectations jumped from 2.9% to 3.2%. The first graph below shows that current and expected conditions fell this month. The second graph puts the data in context. As Charlie Bilello shows, the current poor sentiment level is on par with the financial crisis but lower than 7 of the last 11 recessions. The findings should correlate with a decent decline in consumer spending. However, the sentiment index has been muddling at pessimistic levels, and we haven’t seen a material decrease in consumption yet.

On numerous occasions, Jerome Powell has referenced this survey as important to help the Fed assess inflation expectations. The Fed believes expectations tend to predict inflation. As such, the Fed Funds market may increase the odds of a hike rate hike in June. Currently, the market implies a 12% chance of a hike.

The second lesson is that the public’s expectations about future inflation can play an important role in setting the path of inflation over time. – Jerome Powell August 2022

Trading With Mixed Views

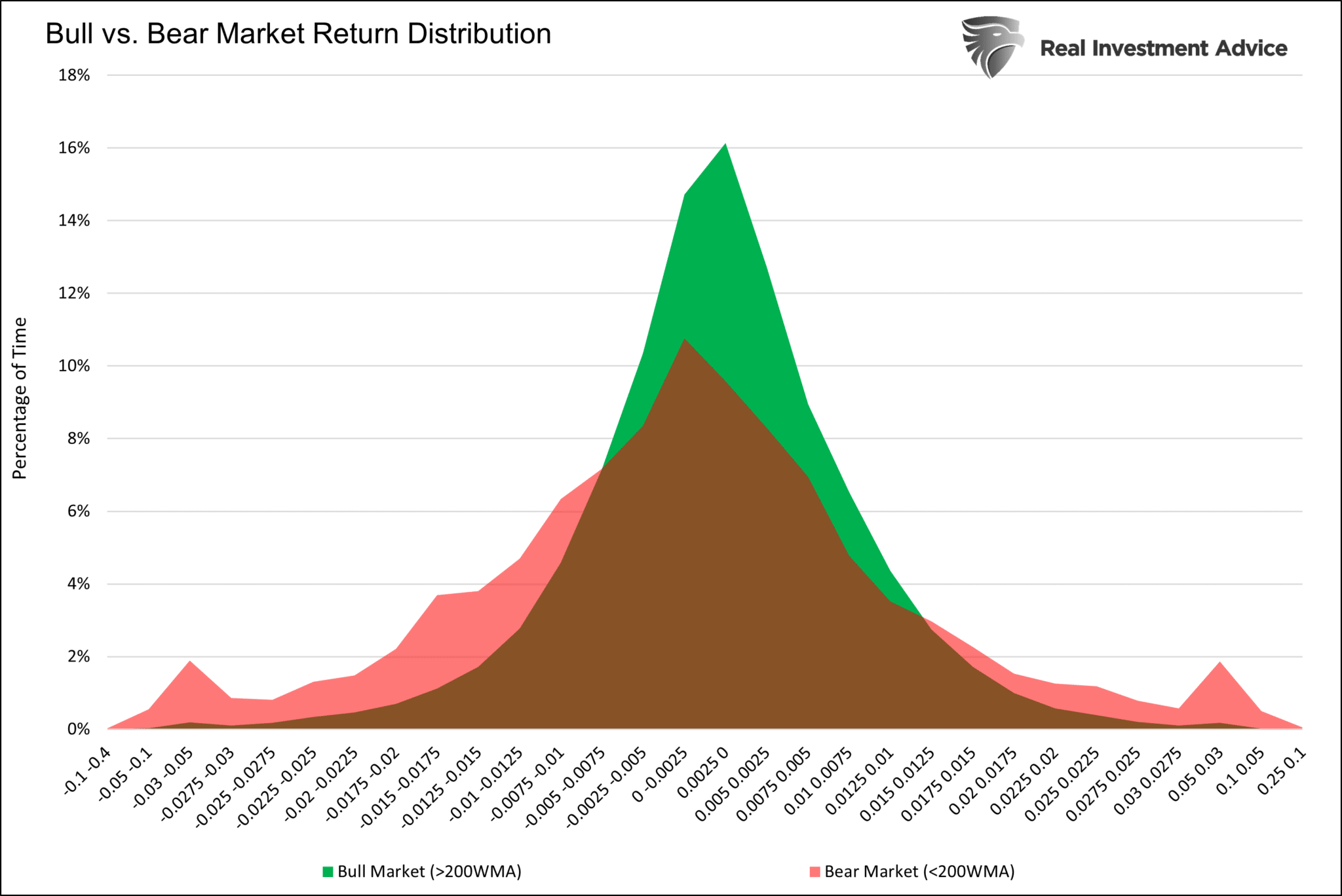

Technical studies on the S&P 500 are generally bullish, as we have regularly shared in the market trading update section of the commentary. That said, many reliable indicators are pointing to a recession. The discrepancy in potential outcomes is paralyzing for many investors. Our recent piece, Risk and Return Imaging, provides advice. The article uses statistics to help investors appreciate the risk and reward possibilities in various market environments.

One of the environments we studied was bull versus bear markets. We used a simple rule to define bull and bear markets, thus allowing us to quantify risk and return. If the daily S&P 500 was above its 200-day moving average (dma) we deemed it bullish and vice versa when below the 200dma. The first graph below shows how favorable daily returns occur more often in bull markets than bear markets. Conversely, bear markets have fatter tails. This means the instances of outsized gains or losses are larger than in a bull market. Most telling, the average annualized return in bull markets is 25.45%. In bear markets, the return is -22.29%. Volatility is almost twice as high in bear markets compared to bull markets. The second table shares more statistics.

This leaves us with advice. Own the market above the 200dma and trade with caution below it. The rule is most tricky when the market is near the 200 dma as it is today.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.