Bloomberg heralds “Nasdaq 100 Enters Bull Market as Bank Jitters Ease.” The Nasdaq is now up over 20% from recent lows, leading many media outlets like Bloomberg to declare the birth of a new bull market. Many investors seem to associate 20% declines with the start of bear markets and 20% increases with the beginning of bull markets. As investors, we must decide whether a simple rule of thumb is worth following.

We present two arguments for consideration. First, we do not believe the “bull market” since 2009 ended. Per our article, A 50% Decline will only be a Correction:

- A bull market is when the market price is trending higher over a long-term period.

- A bear market is when the previous positive trend breaks and prices trend lower.

The article questions whether the swoon in March 2020 was the start of a bear market. We state:

“The price decline in March 2020 was unusually swift using monthly closing data. However, that decline did not break the long-term bullish trend and quickly reversed to new highs, suggesting it was a “correction.”

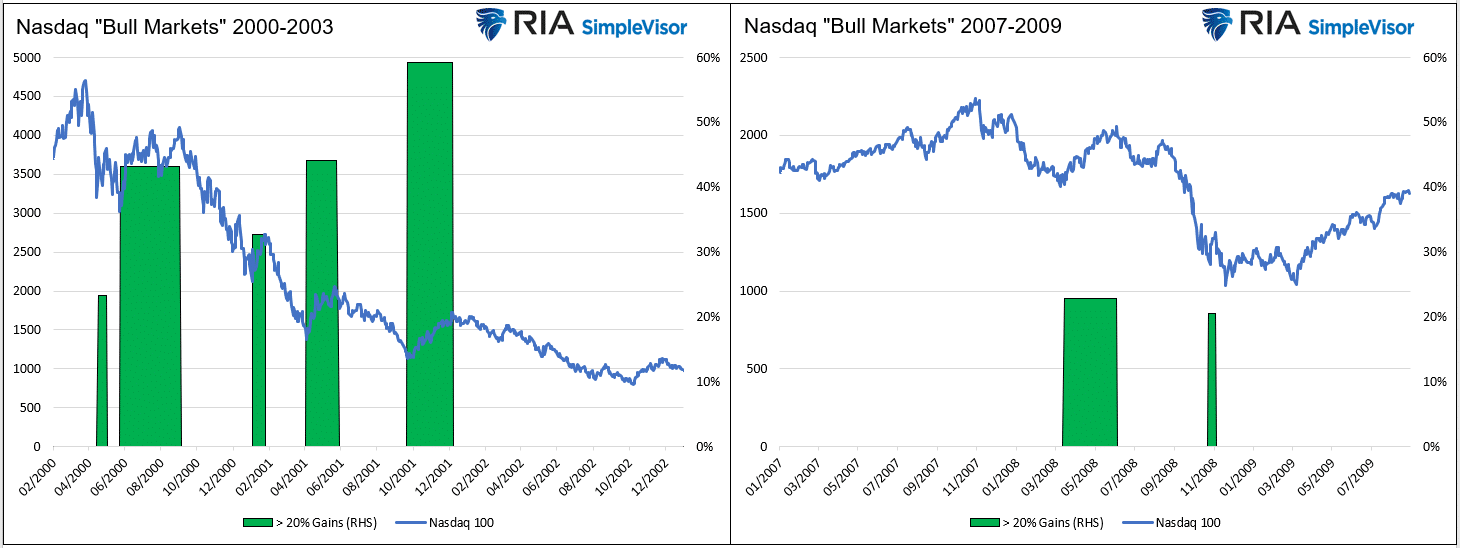

Second, as we share below, history doesn’t always agree that 20% increases signify the beginning of bull markets. The Nasdaq dot.com crash saw five “bull markets” until a bottom was found. There were two during the financial crisis.

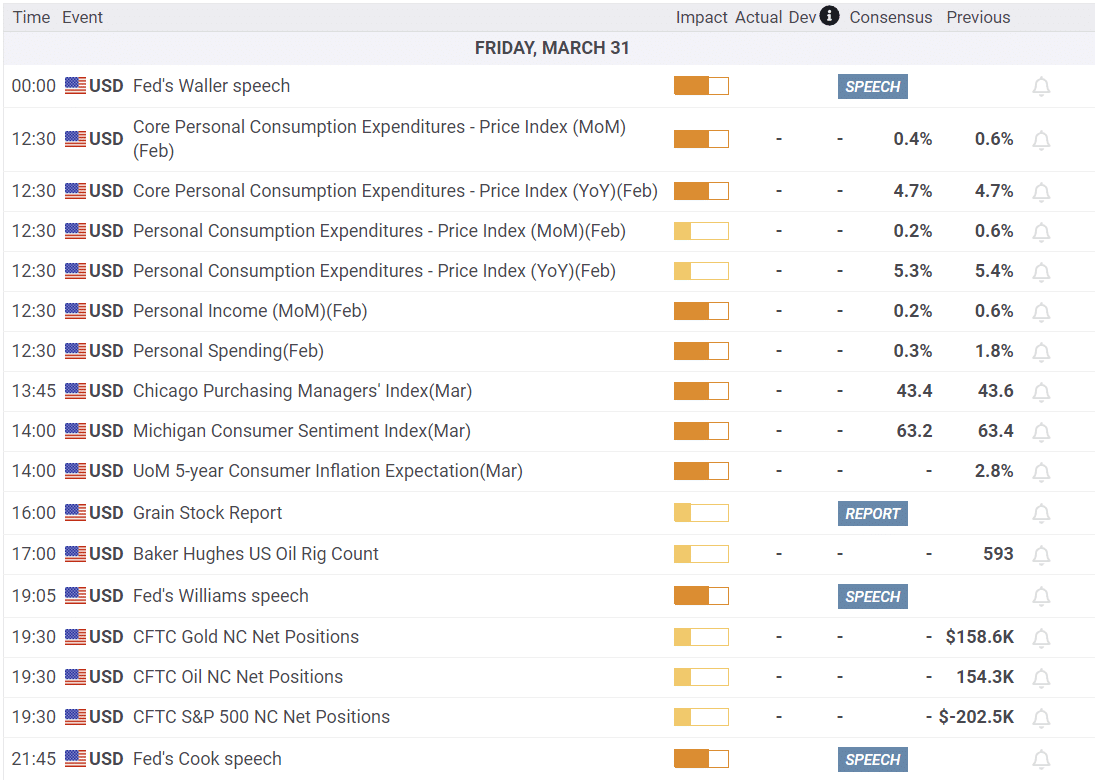

What To Watch Today

Earnings

- No significant releases today

Economy

Lots of Fed Speakers today, which may provide some clues on Fed policy for the next FOMC meeting.

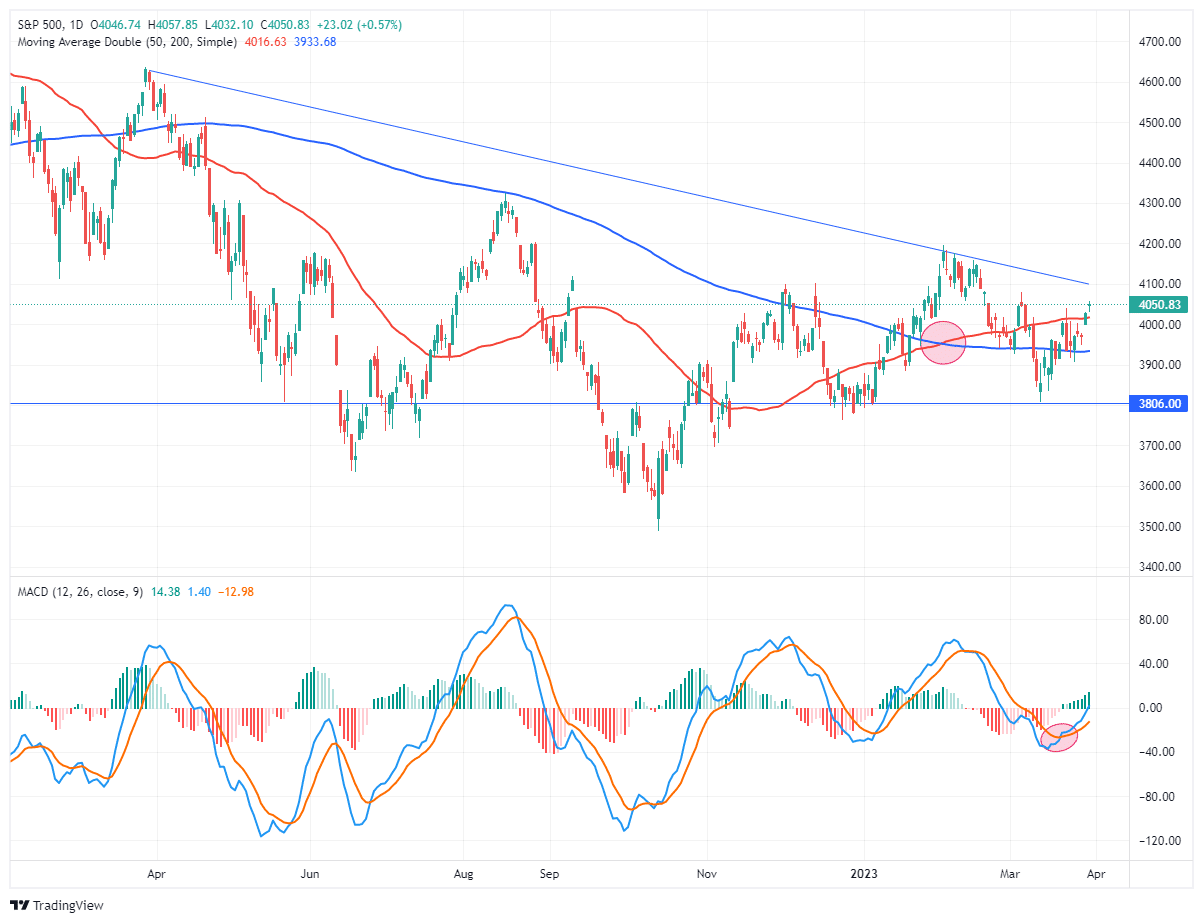

Market Trading Update

The market managed to maintain its rally footing yesterday after clearing the 50-DMA resistance on Wednesday. With the MACD still not nearly overbought, such suggests this rally could have a bit more to go. The first target for this rally is 4100 at the downtrend from the April peak. However, if the market can clear that resistance, then 4200-4300 is possible. Given we are moving into the last two seasonally strong months of the year, the “pain trade” remains higher as positioning and sentiment remain mostly negative.

Use pullbacks to the 50-DMA that holds support to add equity exposure as needed. However, once we move back into more overbought territory with our indicators, reverse that process and begin taking profits and reducing risk.

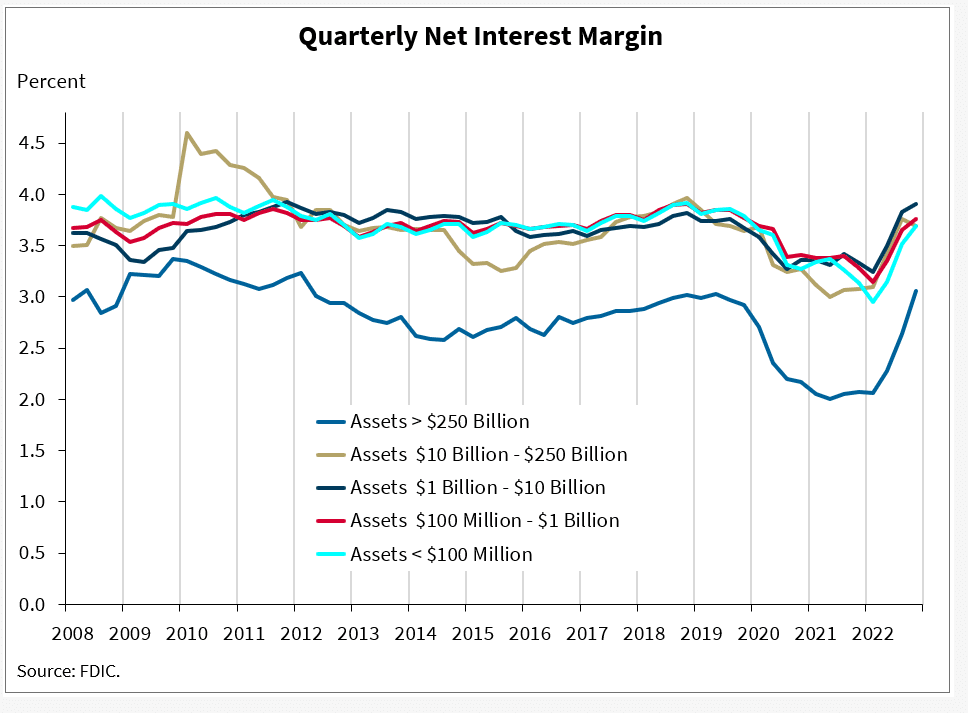

Regional Bank Margins and FDIC Fees

Regional Bank profit margins are under pressure as they replace lost deposits that pay well below 1% with 4% deposits from the Fed or other banks. The potential for a further weakening of margins doesn’t end there. The FDIC is set to propose a special assessment on banks to make up for the recent losses they endured. It is estimated the FDIC lost $20 billion on Silicon Valley Bank and $2.5 billion on Signature Bank. That is almost three times what the FDIC collected from banks in revenue in 2022. The FDIC last reported in late 2022 that it only held $128 billion in reserves, which is below its requirement. We presume the FDIC anticipates further losses and will want to get above its requirements and ensure they remain adequately funded if further losses occur.

The graph below, through 2022, shows an uptick in margins last year, resulting from the growing spread difference between very low deposit rates and higher-yielding loans.

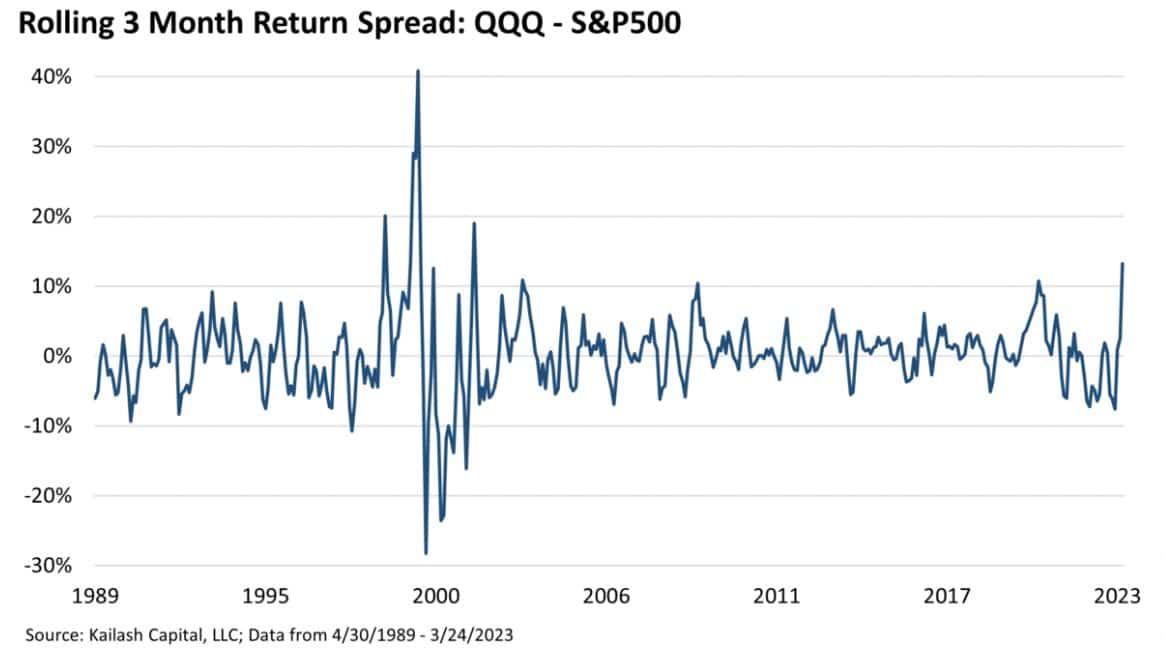

Another Take on the Nasdaq 100 Bull Market

Our friends at Kailash Concepts Research wrote a thoughtful piece putting the current Nasdaq “bull market” in context. We share the following paragraphs and graphs from their latest article, Rank Speculation Returns: A Crisis of Concentration.

Look where we are today. Only into the very peak of the DotCom bubble has the Nasdaq 100 done better over a rolling 90-day period than it has in the last 3 months. And we just showed you that this most recent run was driven entirely by just 28 stocks.

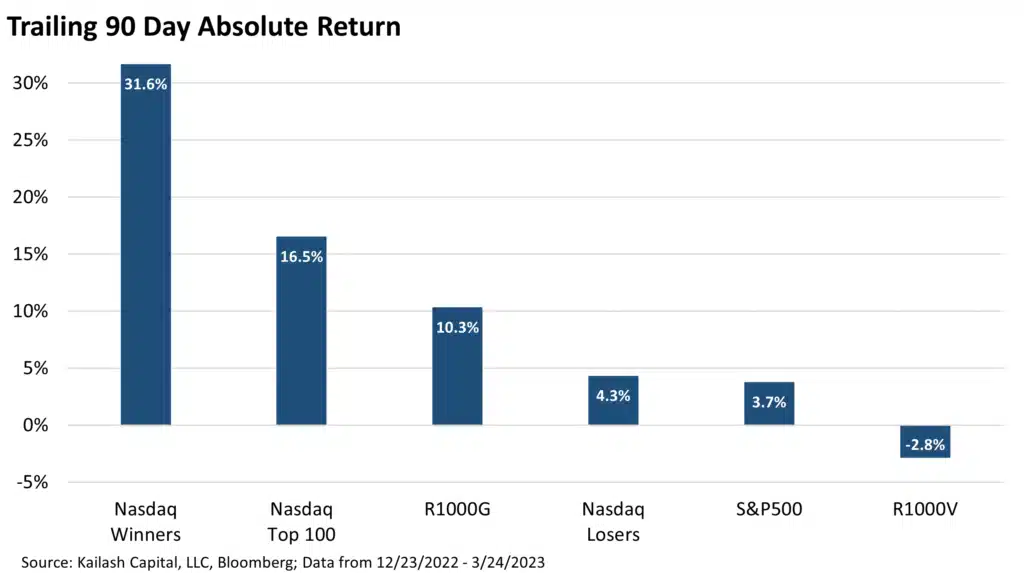

The chart below shows the 90-day performance of the following six groups of stocks, from left to right:

- The largest 100 stocks in the Nasdaq that outperformed the index rose 31.6% in the last 90 days

- The 100 largest stocks in the Nasdaq were up 16.5% over the last 90 days

- The Russell 1000 growth index rose 10.3% over the last 90 days

- The Nasdaq 100’s largest stocks that underperformed the index rose only 4.3% in the last 90 days

- The S&P 500 rose 3.7% over the last 90 days

- The Russell 1000 value index fell -2.8% over the last 90 days

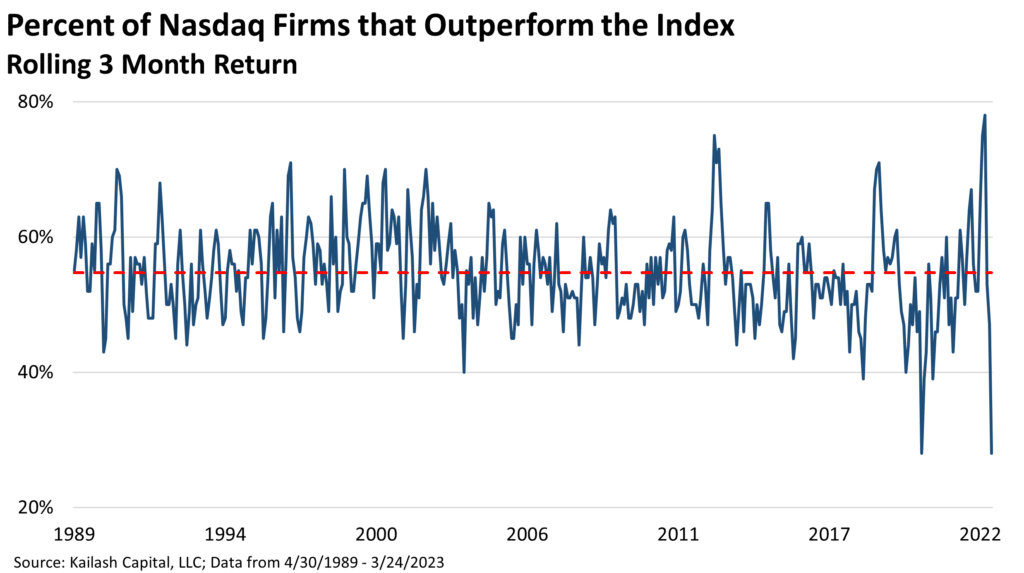

The dashed red line shows that over history, roughly 55% of the stocks in the Nasdaq 100 perform equal to or better than the 100 largest Nasdaq stocks (QQQs). Yet in the last 90 days, only 28% of the stocks in the index outperformed the broader benchmark’s 16.5% return.

This is an anomaly seen only once before in history. To be precise, it last occurred in the period ending on August 31, 2020, as the speculative fury of Covid stimulus sent a small slice of the market’s most speculative names soaring. We are, apparently, watching a near-perfect repeat of that behavior today.

More on Cash on the Sidelines

In yesterday’s Commentary, we discussed how money market fund assets were proliferating and questioned whether it represented cash on the sidelines, which could drive equities higher in the future. Some readers asked us to clarify that point. They, like us, realize there is truly no such thing as cash on the sidelines.

For every buyer, there is always a seller. Therefore, the buyer’s cash “on the sideline” is invested when a transaction occurs. However, the cash the seller receives moves to the sidelines. Investing is a zero-sum game. Consequently, the motivation of the sellers and the buyers drive prices. If sellers are very motivated to sell and there is little interest from buyers, prices will fall. Conversely, when markets run hot, everyone wants in, and few investors want to sell, prices will rise.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.