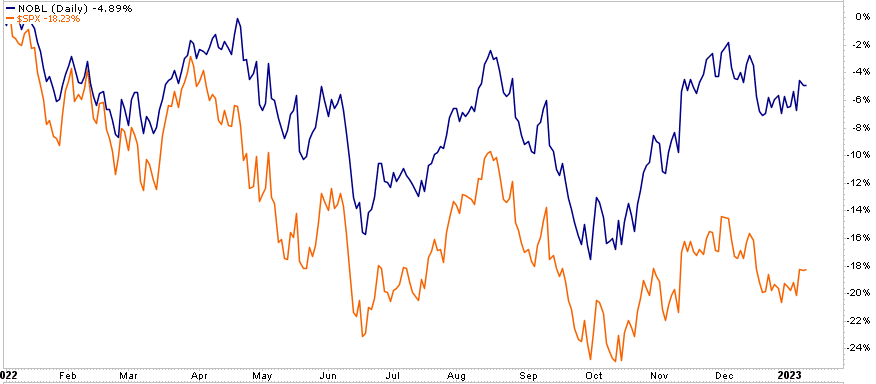

Last year, as the market trended lower, higher dividend stocks sheltered investors from the storm. Within higher dividend stocks are a special breed called dividend aristocrats. To be considered an aristocrat, stocks must pay a consistent dividend and continuously increase the size of their dividend payouts. The graph below shows the performance of NOBL (ProShares Dividend Aristocrat ETF) and the S&P 500. While the price gyrations are certainly correlated, the shelter from the market that NOBL provided was quite impressive.

The ability to provide shelter from market drawdowns results from both the higher dividend yield and quality of earnings. For a corporation to maintain a high dividend and consistently increase it, it must have earnings stability. Further, dividend aristocrats tend to have lower valuations, partly due to the fiscal conservatism they practice. During market drawdowns, this conservatism and low valuations provide a cushion, sheltering investors during tough times.

What To Watch Today

Economy

- 7:00 a.m. ET: MBA Mortgage Applications, week ended Jan. 6 (-10.3% prior)

Earnings

Market Trading Update

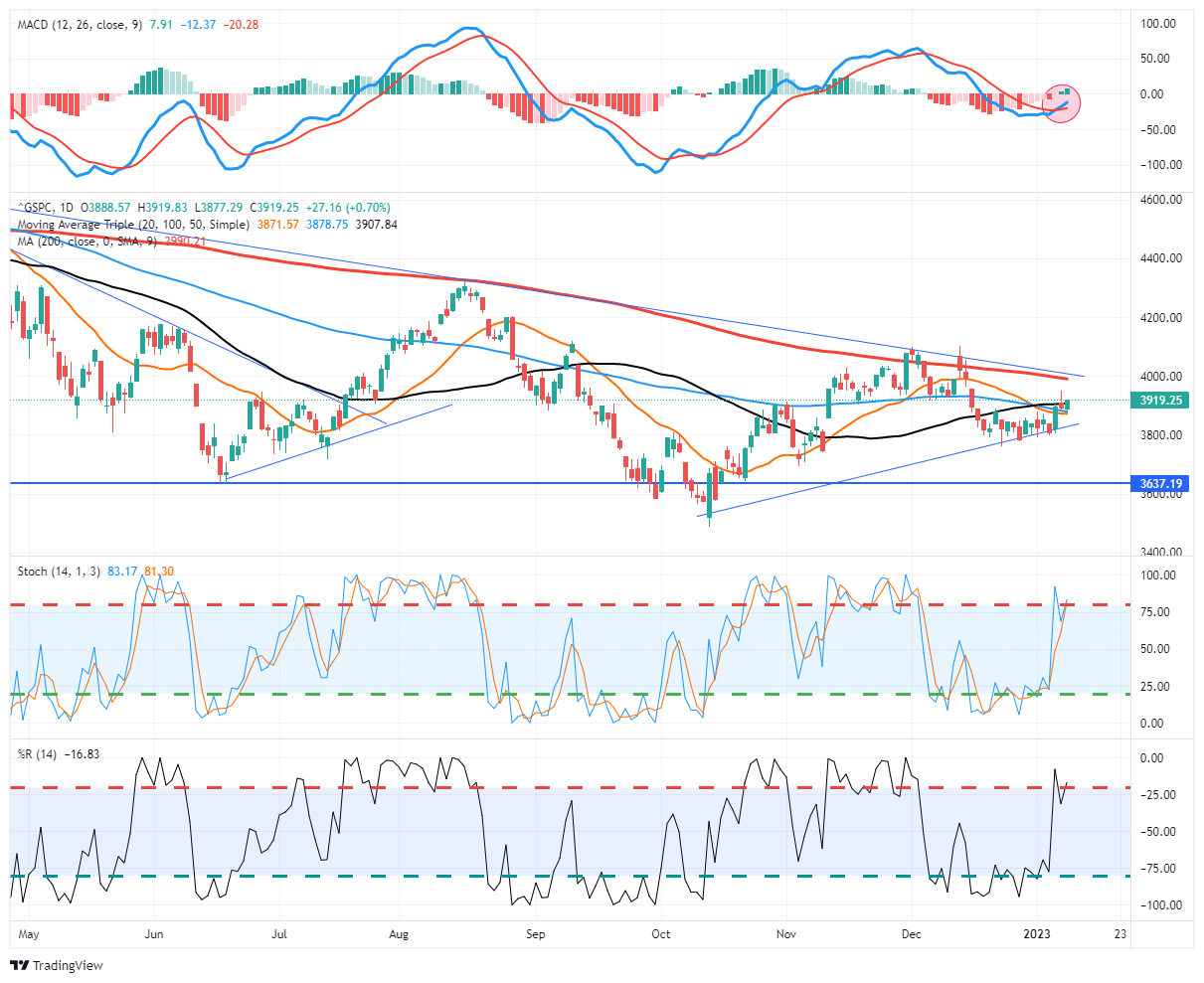

The market rallied yesterday following a “nothing burger” of a speech by Jerome Powell. The next big report is the highly anticipated December CPI report could send stocks soaring or sinking. There is currently a wide range of estimates, but a substantially weaker number will put “pivot” hopes back on the table.

With the MACD signal in place, we are adding some exposure. We would like to see a firm break above the 50-DMA to set up a stronger run to, and potentially above, the downtrend line from last year’s highs. A weak CPI report could give us the catalyst to add some of the “dividend aristocrats” to our portfolio and increase equity exposure for a trading opportunity.

Remain cautious, markets are overbought, and we are about to kick off a potentially weak earnings season. So volatility could pick up depending on the trend of reports. We will update this analysis tomorrow once we have the inflation report.

Small Business Employment

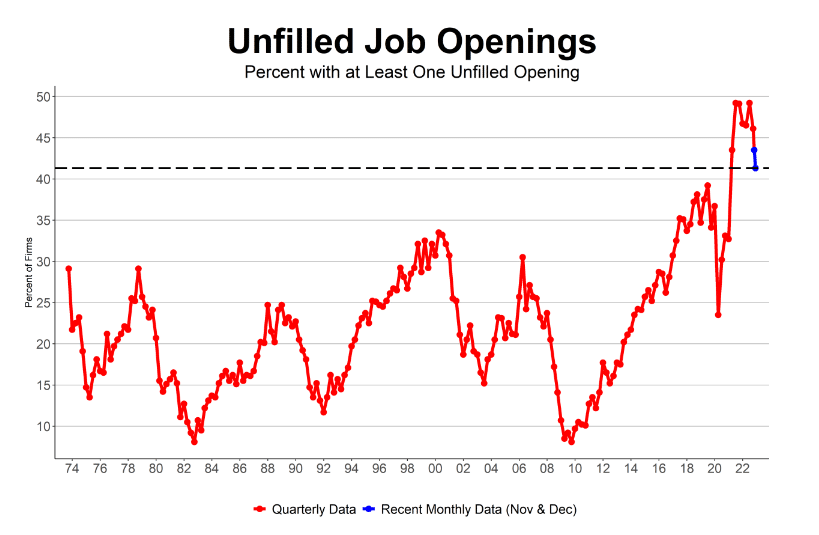

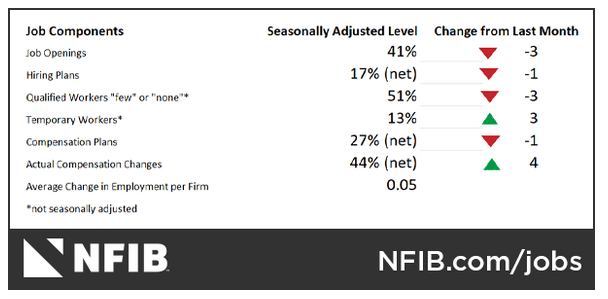

Last week’s payroll data showed that small businesses accounted for nearly all the new job growth in December. With the Fed trying to weaken the labor market to quell inflation, it’s worth focusing on small business employment to help us better assess what the Fed may do in 2023. The NFIB puts out a comprehensive monthly survey of small businesses. In its most recent labor market survey, they note:

Forty-one percent (seasonally adjusted) of all owners reported job openings they could not fill in the current period, down three points from November. The share of owners with unfilled job openings continues to exceed the 49-year historical average of 23% but 10 points below its record high of 51 percent last reached in July.

As shown below, the percentage of those surveyed reporting current job openings is off the 2022 peak but well above any other level since the mid-1970s.

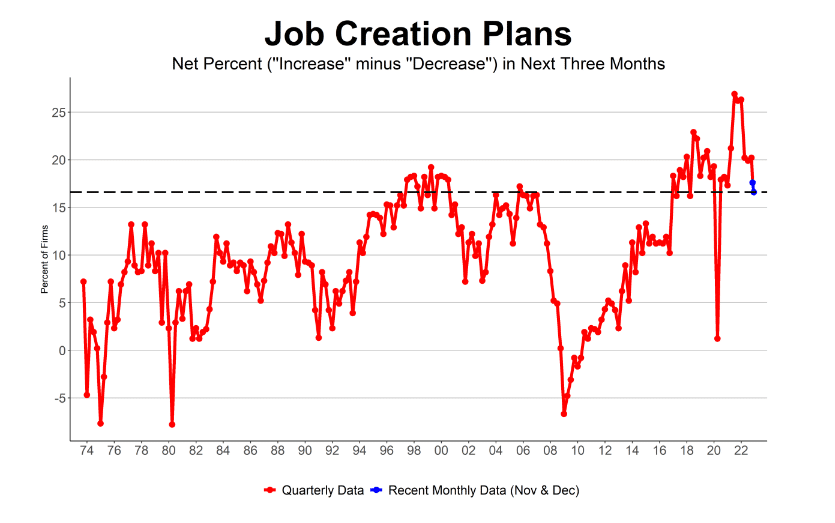

Job creation plans have also weakened but remain near the highest levels of the last fifty years.

Tightness in the labor market for small business owners does appear to be easing but make no mistake, the employment market remains exceedingly tight for small business owners. As such, pressure on small business owners to provide higher wages will likely continue, further hampering the Fed’s inflation goals.

More on HOPE

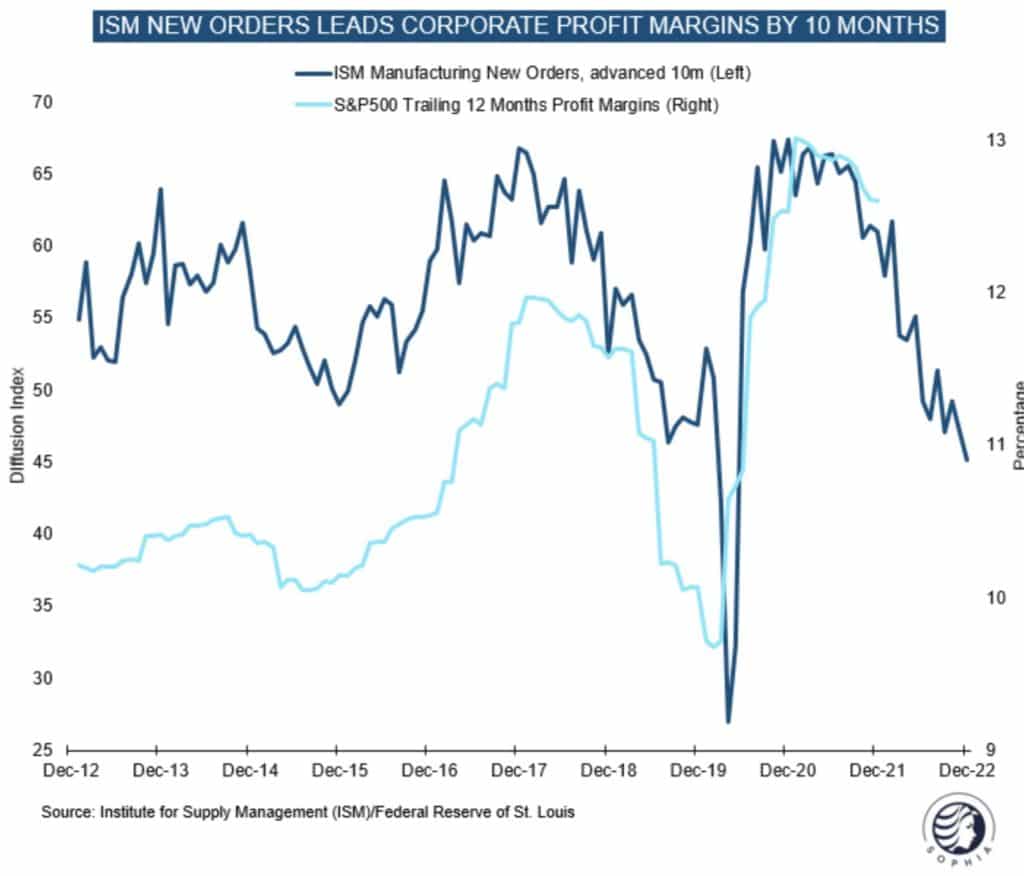

Tuesday’s Commentary presented Michael Kantro’s HOPE cycle. His cycle diagrams the order in which economic data typically deteriorates before a recession. The O, in HOPE, is New Orders from the ISM report. The P is corporate profits. The graph below shows that changes in new orders lead to changes in profit margins by about ten months. Based on the data below, we should expect profit margins to begin falling rapidly. Lower margins along with weakening sales, and higher inventories, will likely lead to lower-than-expected earnings in 2023. Ergo, estimates for 8% EPS growth in 2023 may be way off the mark. While the market has been lower over the last year, the market has yet to price in a recession and moderate decline in earnings. As we stated yesterday, 2022 was about inflation concerns. 2023 will likely be recession and earnings worries.

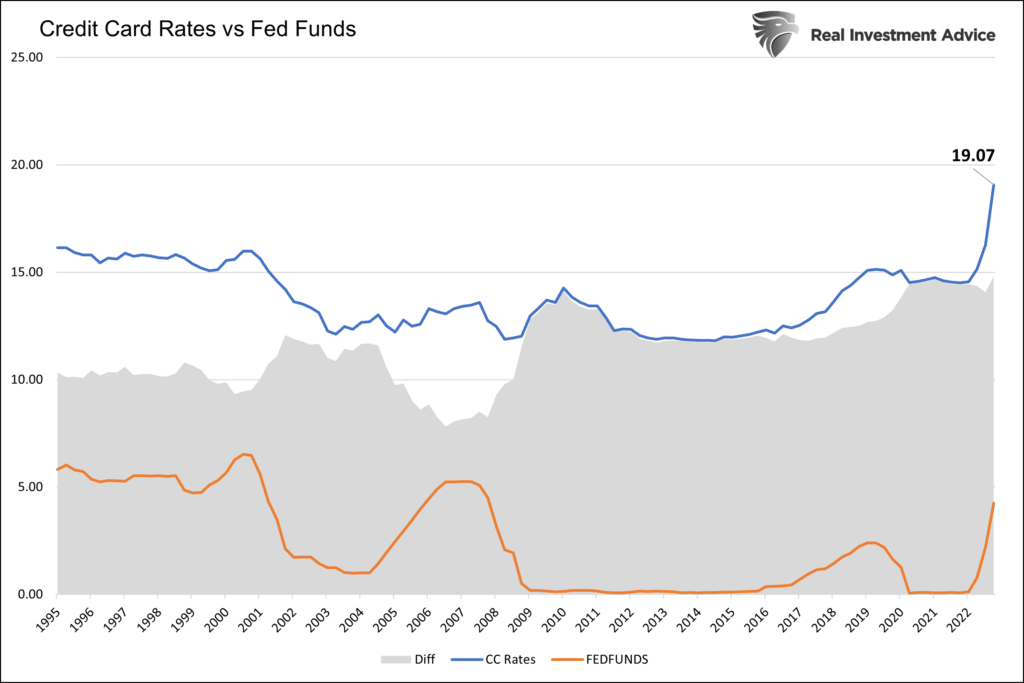

Credit Card Interest Rates Soar With Fed Funds

The Fed publically states it wants to curb consumer demand to quell inflation. Raising interest rates is a crucial tool they use to accomplish such a task. The graph below shows interest rates on credit cards at commercial banks have risen from 14.5% to over 19% since the Fed’s tightening campaign began. While the rate is exceptionally high, and some would argue it is a usurious rate, the difference between credit card rates and Fed Funds has remained constant over the last few years. That said, high-interest rates on credit cards will curtail spending.

The second graph shows the disturbing reality supporting consumption in 2022. The savings rate, at a mere 2.4%, is the lowest it has been since at least 1960. The amount of credit card debt outstanding is up over 15% in the last year. While debt and savings resulted in robust spending, we must ask where consumers will find the means to keep up such spending in 2023.

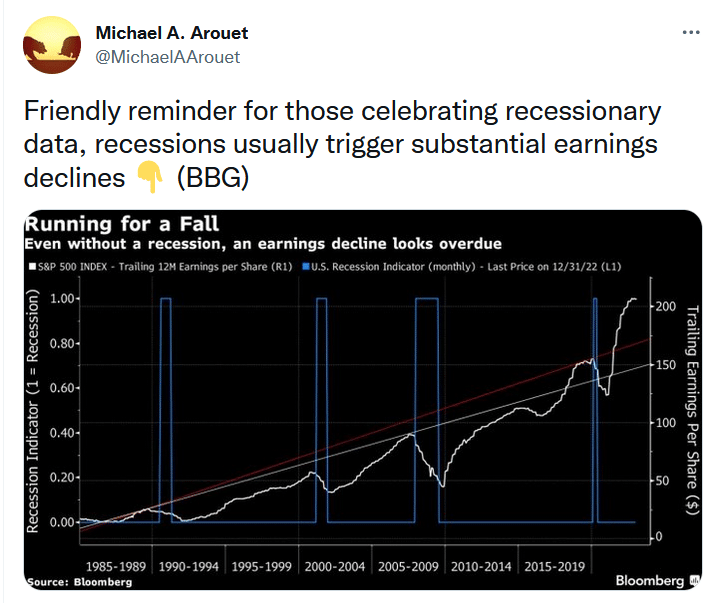

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.