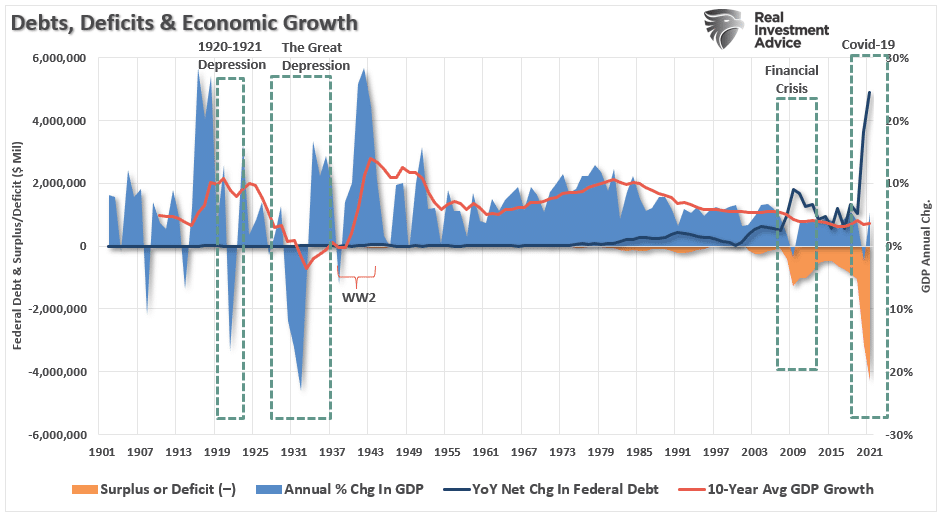

This morning, market futures surged on hopes of a “continuing resolution” to avert a “shutdown.” Last night the Democrats appeared to buckle under the pressure of a looming “shutdown” with Chuck Schumer, Senate Majority Leader, suggesting a vote on a “Continuing Resolution (C.R.)” is forthcoming. The C.R., a stop-gap measure in place of a budget, will provide funding for the government through December 3rd. At that point, another C.R. will have to get passed to fund the rest of the fiscal year.

For the unfamiliar, before 2008, Congress would pass an actual budget itemizing spending needs that would get passed and funded. However, starting with the Obama administration, such arcane methods of managing government got dropped for the use of C.R.’s instead, which take last year’s spending and adds 8% to it. Such is why debts and deficits started to increase beginning in 2008 and continues today.

The good news is that with the threat of a “debt default” and “shutdown” removed, stocks look to rally sharply this morning.

[dmc]

What To Watch Today

Economy

- 8:30 a.m. ET: Initial jobless claims, week ended September 25 (330,000 expected, 351,000 during prior week)

- 8:30 a.m. ET: Continuing claims, week ended September 18 (2.800 million expected; 2.845 million during prior week)

- 8:30 a.m. ET: GDP annualized, quarter-over-quarter, second-quarter third estimate (6.6% expected, 6.6% in prior estimate)

- 8:30 a.m. ET: Personal consumption, second-quarter third estimate (11.9% in prior estimate)

- 8:30 a.m. ET: Core personal consumption expenditures, second quarter third estimate (6.1% in prior estimate)

- 9:45 a.m. ET: MNI Chicago PMI, September (65.0 expected, 66.8 in August)

Earnings

Pre-market

- 6:50 a.m. ET: CarMax (KMX) is expected to report adjusted earnings of $1.87 per share on revenue of $6.88 billion

- 7:45 a.m. ET: Bed Bath & Beyond (BBBY) is expected to report adjusted earnings of 52 cents per share on revenue of $2.06 billion

Post-market

- 4:15 p.m. ET: Jefferies (JEF) is expected to report adjusted earnings of 99 cents per share on revenue of $1.74 billion

Politics

- Lawmakers appear to have a way to prevent the U.S. government from shutting down at 12:01 a.m. ET. Senate Majority Leader Chuck Schumer announced that the Senate will vote by midday on a bill to fund the government until Dec. 3. The U.S. House of Representatives will follow and — hopefully before the deadline — the measure will be sent to President Biden for his signature.

- Secretary of the Treasury Janet Yellen and Federal Reserve Chairman Jerome Powell will appear before Congress today for the second time this week. On Tuesday, Yellen warned of “catastrophic economic consequences” if the debt ceiling is not raised by Oct. 18.

Courtesy of Yahoo

Stocks Holding Support At 100-dma

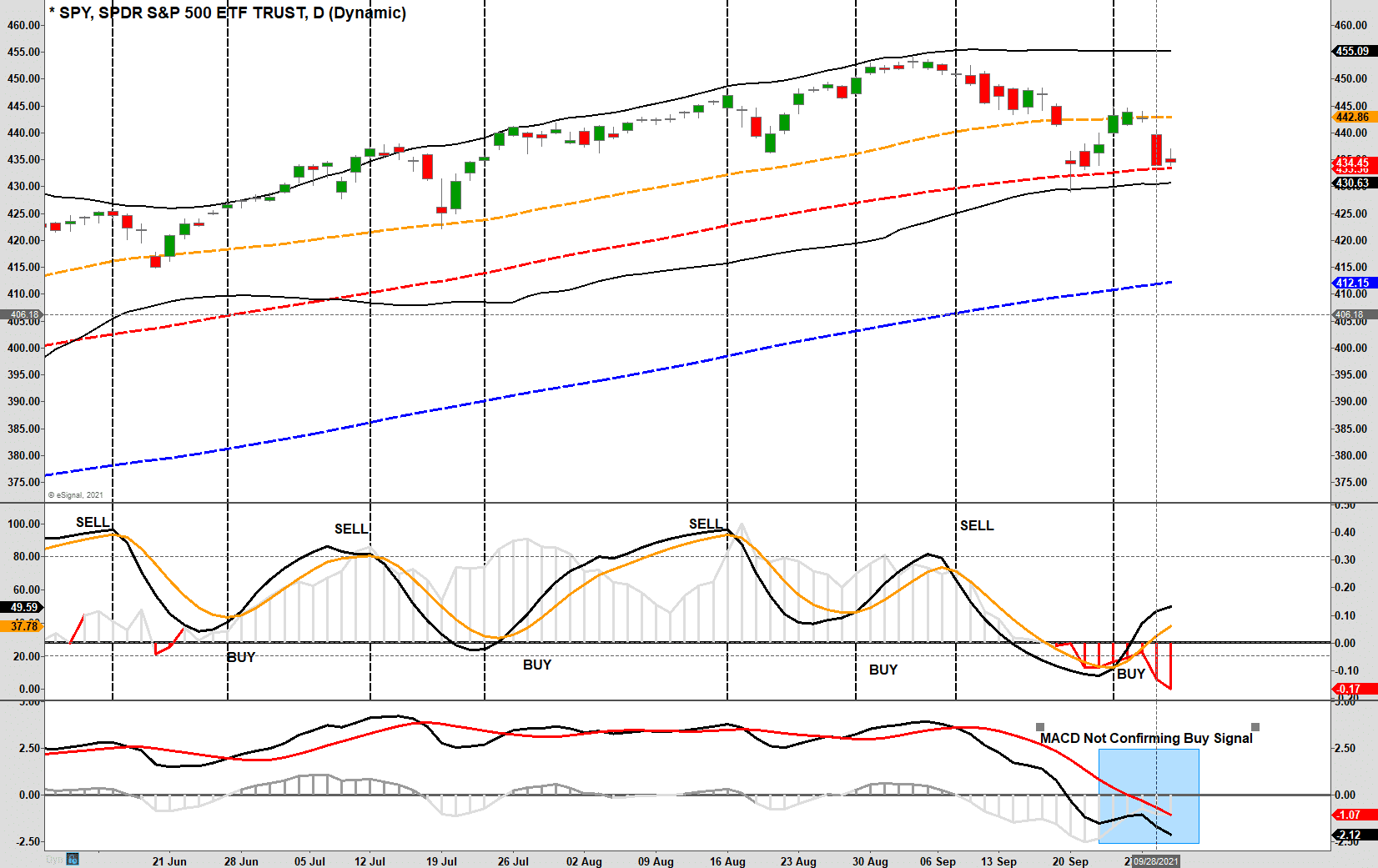

The market held its 100-dma yesterday as stocks mustered a very weak rally. Stocks need to muster a rally off of support and clear the 50-dma next week if bulls are to maintain control. Otherwise, every day the market remains weak, the greater the potential for a larger breakdown becomes.

As noted below, while our “money-flow” buy signal is intact, the MACD has yet to confirm the bullish signal. Such keeps us cautious near term and does not preclude another down-leg in the market currently. However, with the Democrats ready to fund the Government through December, such should take pressure off of the markets near term.

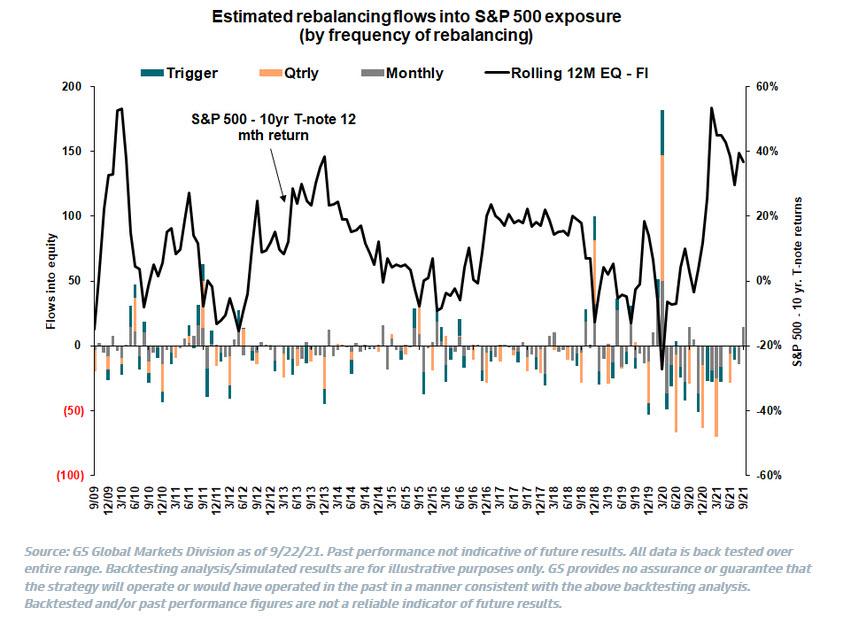

$14 Billion Into Quarter-End Pension Buying

While there are many reasons for the recent market volatility we mustn’t forget window dressing. At quarter-ends, money managers tend to “clean up” quarter-end holdings to appease client concerns. The recent uptick in inflation concerns, debt cap issues, and taper are reasons for said managers to sell some holdings and buy others.

It’s likely they will start buying back stocks and bonds today.

“With month- and quarter-end on deck, Goldman’s theoretical, “model-based” estimates are for a net $14 billion of US equities to buy from US pensions given the moves in equities and bonds over the month and quarter.

How does this stack up vs history? According to Goldman’s Gillian Hood, this ranks in the 36th percentile amongst all buy and sell estimates in absolute dollar value over the past three years. In absolute terms, this falls below the three-year average absolute dollar value of $26bn worth of equities to be rebalanced.” – Zerohedge

Defense is not Working

As we discuss in our 3 Minutes on Markets video, bonds didn’t rally to help offset losses in stocks yesterday. While bonds and gold tend to historically provide diversification to an equity portfolio, such is not always the case. In fact, days like yesterday are recently becoming a little more common. The last 3 times the S&P fell by 2% or more in a day, the 10-year Treasury price, gold, and bitcoin also fell on the same day.

Rates Spike and Stocks Decline

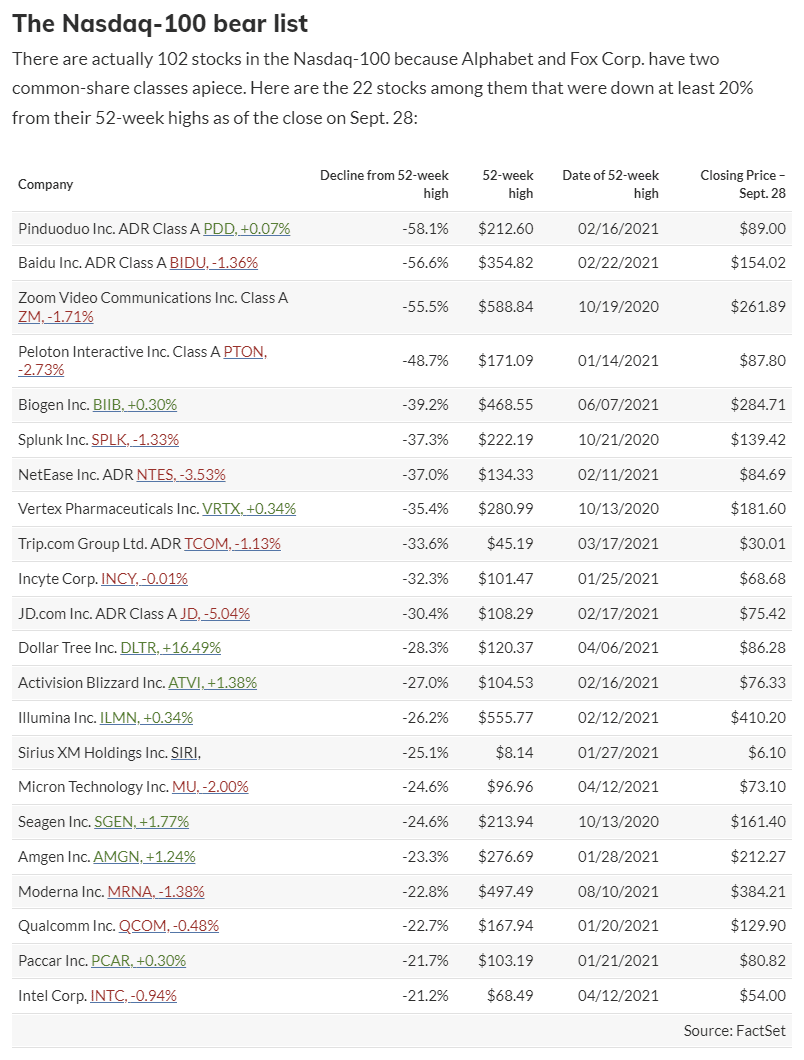

Is Their Opportunity In The Nasdaq?

There are quite a few stocks in the Nasdaq in bear markets (down by 20%). Interesting list from MarketWatch.

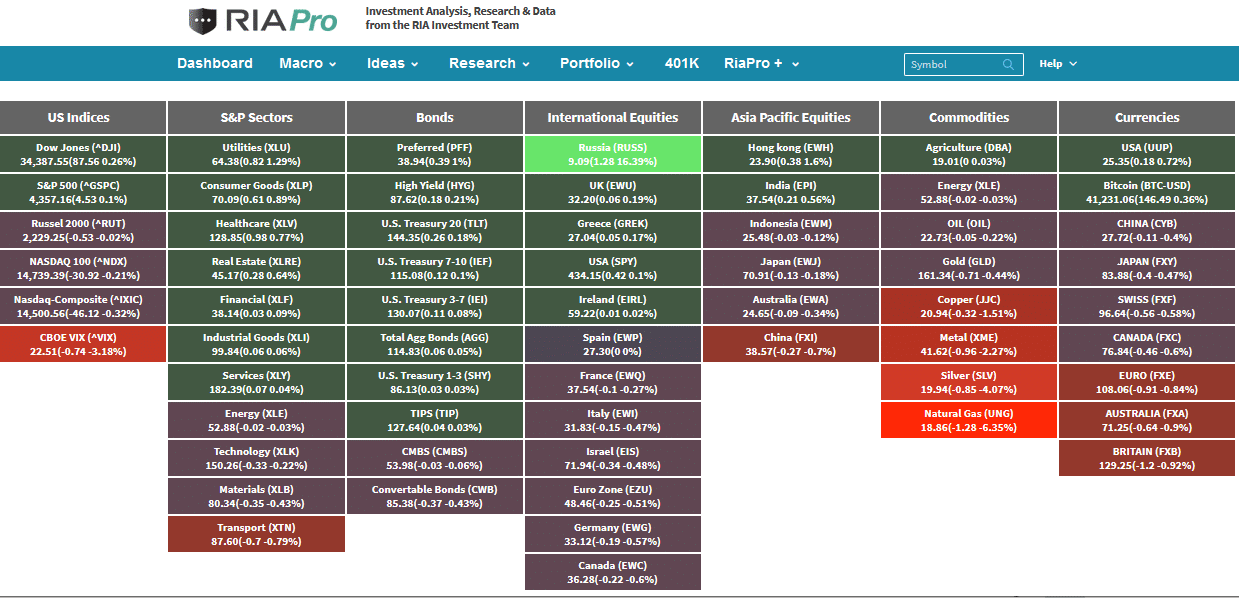

Silver is not so Hot

The RIA Pro heat map below shows silver (-4%) and metals were among the worst-performing assets yesterday. As a result, materials were lower on the day.

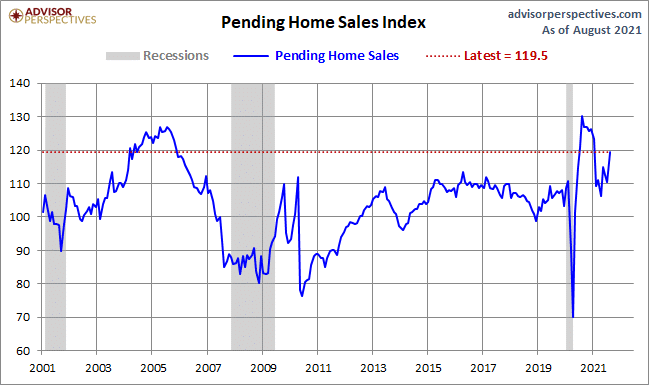

Housing is Red Hot

Pending Home Sales rose 8.5% in August after two straight monthly declines. The change in year-over-year sales is still negative but the monthly trend is rising again as shown below. Per the National Association of Realtors President, Lawrence Yun: “rising inventory and moderating price conditions are bringing buyers back to the market.”

His comment about moderating price conditions is debatable. Yesterday, the Case-Shiller 20-City Home Price Index rose another 1.5% monthly and is now up nearly 20% annually. Prior to the pandemic, the index rose approximately 3-6% a year. At the housing market’s peak in 2006, the Case-Shiller Index rose 15% annually.

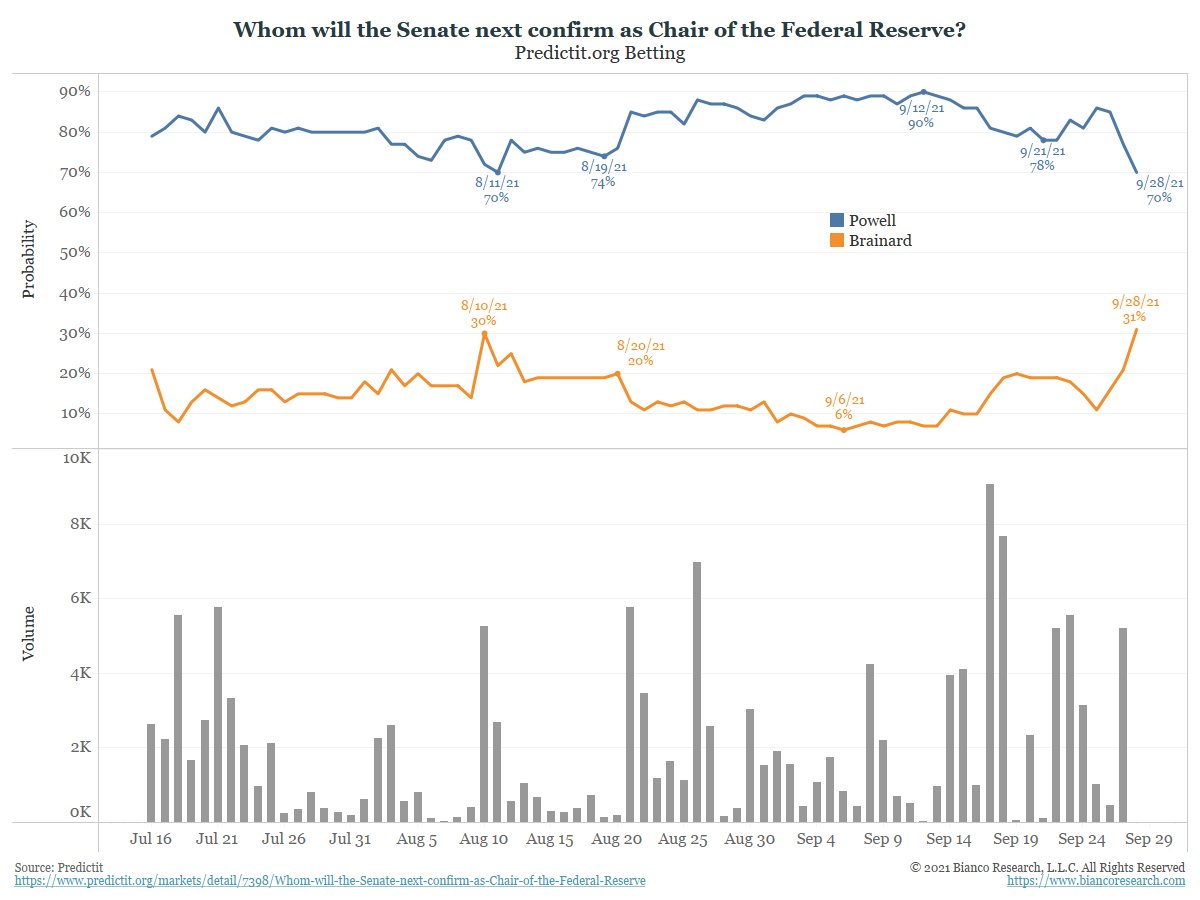

Is Powell On His Way Out?

Extreme stock and bond market valuations are largely predicated on the Fed’s ability to provide excessive liquidity via low rates and QE. Given confidence in the Fed is paramount to valuations we offer some concern at recent disclosures implicating Fed members. In particular, are those of Dallas President Robert Kaplan. The quote below is from Wall Street On Parade.

Each of Kaplan’s financial disclosures forms dating back to when he first became Dallas Fed President on September 8, 2015 (which we obtained directly from the Dallas Fed), show that Kaplan was trading in and out of S&P 500 futures, a highly speculative form of trading used by hedge funds and day traders.

Given Kaplan had access to non-public information, the allegations are serious. Over the coming days and weeks, we need to ascertain if investors care and further if Congress will take any action that might inhibit the Fed’s policy thought process.

Another consideration is whether or not the disclosures provide President Biden a reason to nominate Lael Brainard instead of granting Powell a second term. The graph below shows the odds favor Powell, but they have come down in recent days.

Will Yields Surprise To The Upside?

The graph below, courtesy of Ed Yardeni, shows the strong correlation between the Citi Economic Suprise Index and ten-year UST yield changes. The Citi index measures economic data estimates versus actual readings. Over time the index oscillates as economists move back and forth from overestimating economic activity to underestimating it. As shown below in red, economists have been over-optimistic recently but given this data series in the past, it is likely reaching a point where economists start under forecasting economic data. If this proves true, yields are likely to rise over the coming weeks.