This morning market futures are pointing lower as oil breaks above $80 and bond yields rise. Furthermore, investors need to fasten their seat belts, for a busy week full of economic data, Fed minutes, and corporate earnings. The market gets a rest from data today due to the Columbus day holiday. Between CPI, PPI, Retail Sales, and JOLTs, all set for release this week, the Fed will have a new round of data to guide their tapering decision. Expect more tug of war in the markets as investors deal with new data.

[dmc]

What To Watch Today

Economy

- No notable reports scheduled for release

Earnings

- No notable reports scheduled for release

Politics

- The U.S. House of Representatives and Senate are both out of session until Oct. 18.

- The World Bank Group and the International Monetary Fund (IMF) kick off their annual meetings in Washington D.C. They will release the World Economic Outlook tomorrow morning.

Courtesy of Yahoo

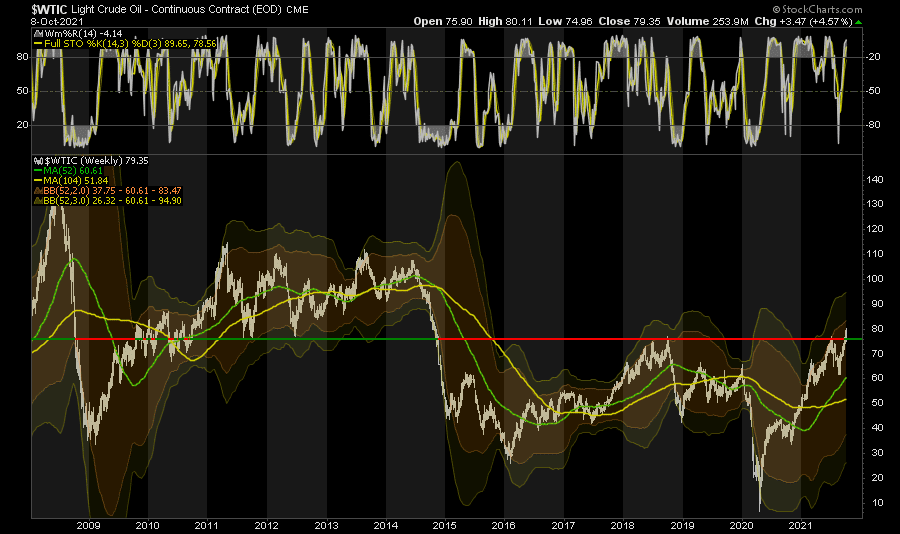

Oil Breaks Above Key Resistance

This morning oil futures are pointing significantly higher with oil breaking above key resistance levels going back to 2009. While oil is very overbought, and a very overcrowded trade, at the moment, such does not mean prices can’t surge higher given the bottlenecks in the system. There is a good bit of overhead resistance as oil prices move into the $90-$100 range, and the bigger issue becomes the inflationary backlash of higher prices on consumption and economic growth.

Stock Futures Are Lower To Start The Week

“Stock futures were slightly lower on Monday to start the week as traders eyed surging energy prices and the start of earnings season around the corner.

Dow Jones Industrial average futures fell 107 points, 0.3%. S&P 500 futures lost 0.5% and Nasdaq 100 futures shed 0.7%. The Dow is coming off its best week since June.” – CNBC

As noted in “Is The Great Bear Market Of 2021 Over?” We need to see some follow through buying this week in markets to confirm the break above resistance last week. If we fall back below the 100-dma, stocks will retest recent lows. The risk is that continued failures to advance will lead to a break of support and a deeper correction will ensue.

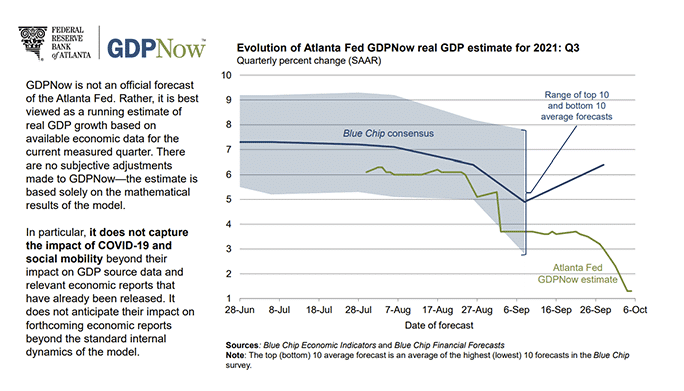

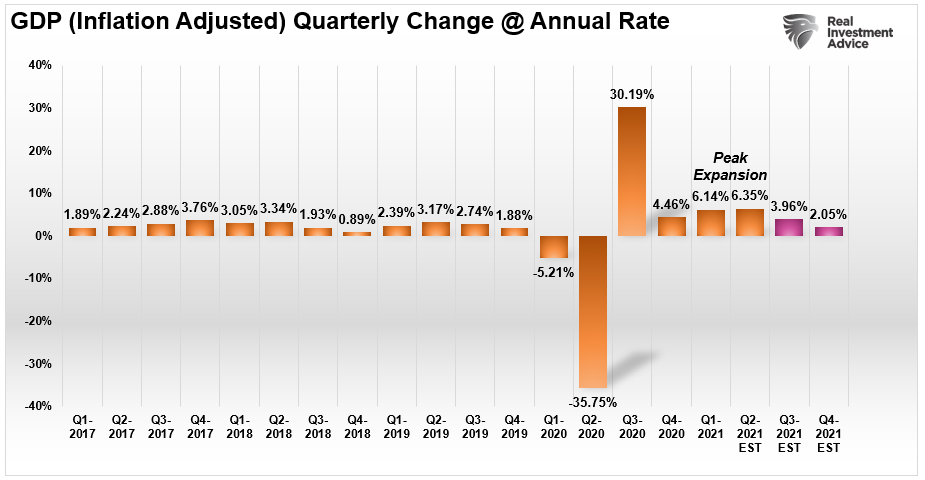

GDP Revised Down As Expected.

Futures also took a hit as Goldman Sachs cut its economic growth forecast. Goldman cut its 2022 growth estimate to 4% from 4.4% and took its 2021 estimate down a tick to 5.6% from 5.7%. The firm cited the expiration of fiscal support from Congress and a slower-than-expected recovery consumer spending, specifically services.” – CNBC

Such is not a surprise and is a function of the “second derivative” effect we have discussed since the beginning of this year.

In Q2 of this year, G.D.P. estimates started that quarter at 13.5% and ended at 6.5%. The third quarter started at 6% and is now tracking at 1.3%, as shown below.

As we discussed in “The Coming Reversion To The Mean,” the “second derivative” effect of economic growth is manifesting itself. To wit:

“We are at that point in the recovery cycle. Over the next few quarters, the year-over-year comparisons will become much more challenging. Q2-2021 will likely mark the peak of the economic recovery.“ – 09/24/21

When writing that blog, our estimates were for a cut in growth to 3.9%. We are currently closer to 1%.

Secondly, fourth-quarter growth will also remain under significant pressure for several reasons:

- Year-over-year comparisions remain challenging.

- Manufacturing surveys look to slow in a challenging enviroment.

- Employment continues to quickly revert to long-term norms.

- Liquidity continues to turn negative.

The last point is the most problematic. The massive surge in economic growth in 2020 was a direct function of the massive direct fiscal injections into households. With that support gone, economic growth will revert to normality, particularly in an environment where wage growth does not keep up with inflation.

Payrolls Report

The BLS Jobs report was weaker than expected, with job growth of 194k. Expectations were for a gain of between 475k and 500k jobs. The BLS revised the prior month higher to 366k from 235k. The unemployment rate did fall from 5.1 to 4.8%, however, it was in part due to people dropping out of the workforce. 183k people left the workforce causing the participation rate to fall from 61.7 to 61.6%. With the number of job openings so high and jobless benefits ending we find it surprising people are leaving the workforce. Also interesting was temporary help fell slightly. With so many job openings one would expect many companies to hire temporary workers to fill gaps until they can hire permanent workers. The graph below from True Insights shows payroll growth is starting to fall back in line with pre-pandemic rates of 150-200k per month.

The Danger of Fighting the “Last War”

Bill Dudley, President of the New York Fed from 2009 to 2018, in a Bloomberg editorial, voices concern the Fed is too worried about deflation, or as he says, the “last war.” He argues the Fed should be concerned inflationary pressures are more than transitory. He prefers the Fed take on a more hawkish tack sooner rather than later. Per Dudley:

“This dovishness increases the risk of a major policy error. If the economic outlook evolves in unexpected ways, Fed officials will almost certainly be slow to respond. Hence, if inflation proves more persistent than anticipated and even accelerates as the economy pushes beyond full employment, they’ll have to tighten much more aggressively than they expect.

A faster pace of tightening would come as a shock for financial markets and could risk tipping the economy back into recession. That’s the danger of fighting the wrong war.”

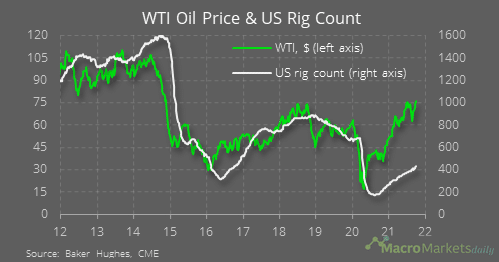

Oil Prices and Rig Counts

The graph below compares oil prices to rig counts. After falling to recent lows, rig counts are rising. However, they are still well less than should be expected given current oil prices. Why are oil producers not adding rigs and producing more oil to take advantage of higher prices? There are a few reasons.

First, OPEC is increasing production and will get more aggressive if prices keep rising. Second, oil producers realize the current economic boom and spike in economic activity, and demand for oil is temporary. It is the result of short-term fiscal stimulus and economic normalization. Lastly, President Biden is threatening to release oil from the strategic oil reserves. If the government indiscriminately caps the price of oil via rhetoric and action, the incentive to produce and add rigs is lessened.