There has been a growing concern over Technology stocks as investors “Party Like It’s 1999.” While no two periods are the same, the outcomes often are. For longer-term investors, if we are amid another “Tech Bubble,” the biggest challenge is navigating it and “living to tell about it.”

Interesting Times

“May you live in interesting times.” – Joseph Chamberlain

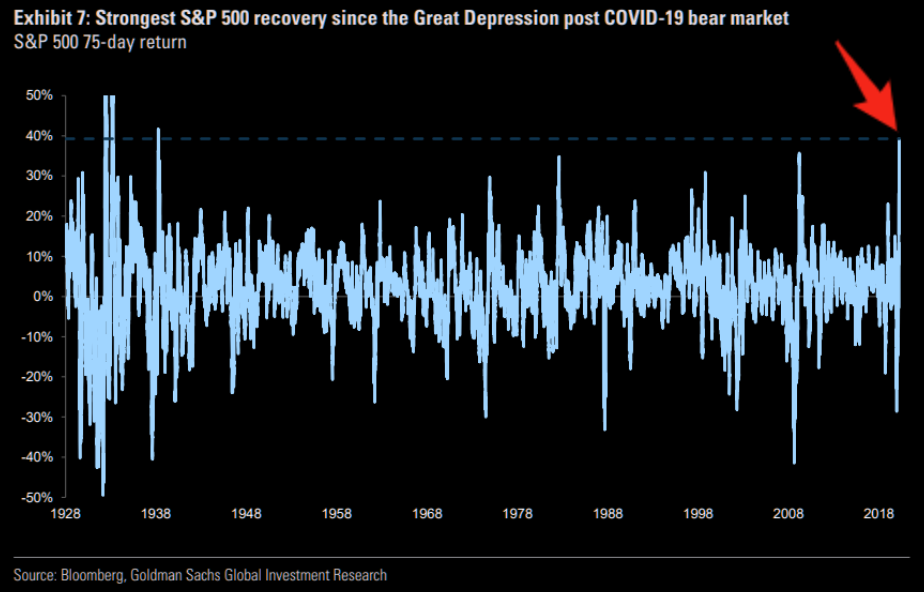

That certainly seems an apropos statement after watching the financial markets plunge 35% in March to recover back to positive territory by July. Interestingly, this is the fastest rebound in the market since 1938 but is occurring against a near economic depression.

Here are some current stats:

- -34.7% Annualized GDP Growth (-8.675% for Q2) via Atlanta Fed GDPNow Estimate

- ~50-million people unemployed

- -4.2% personal income

- -104.2 billion decrease in international transactions for Q1 (Q2 will be markedly worse)

- -54.6 billion decrease in international trade of goods and services.

- ~30% decline in corporate profits

- ~35% decline in corporate earnings based on current estimates

There is no precedent for such a dichotomy between the markets and the economy. Yet, as stated, this is the fast recovery in the market since 1938. Just not so much for the economy.

As I said, we certainly live in “interesting times.”

Party Like It’s 1999

Over the last couple of weeks, I have discussed the disparity in value, and the deviation between value and growth.

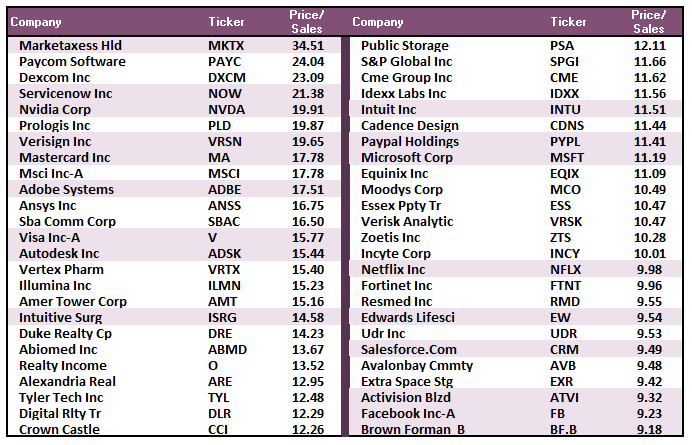

Part of those discussions related to similarities seen at previous market peaks where investors threw “caution to the wind” and paid astronomical prices to own the “hot stocks.” To this point specifically, we quoted Scott McNealy, then CEO of Sun MicroSystems, who chastised investors for paying 10x Price-to-Sales for his company. That was in 1999. Today, investors are doing it again.

Of course, much of this is “forgotten history” as many investors today were either a) not alive in 1999, or b) still too young to invest. For the newer generation of investors, the lack of “experience” provides no basis for the importance of “valuations” to future outcomes. That is something only learned through experience.

Just as was the case in 1999, investors believe that stocks are essentially a “one-decision” investment. You buy them, and they only go up in price. In 1999, a large majority of these companies were financially unstable or grossly overvalued at best. Today, as shown above, it isn’t much different.

Bubbles Are About Psychology

In 1999, there was “no one” saying there was a “Tech Bubble.” As Mark Hulbert recently noted, it was quite the opposite. It also smacks of current sentiment as well:

“After reading through my newsletter archives from January 2000, I was struck by the similarities between now and then. For example, one newsletter editor in mid-January 2000 said he was encouraged that the Fed was signaling that it wouldn’t be raising rates as aggressively as previously thought. Another said, “inflation is dead.” A third celebrated the strength of the economy, as evidenced by robust consumer spending in the Christmas season that had just ended.

Sound familiar? To be sure, these similarities don’t mean the U.S. market is at or near a top. It does illustrate the false comfort we gain when telling ourselves a bear market can’t happen since the economy is strong, inflation is moribund, and the Fed is accommodative.”

As Mark goes on to note, the extension of valuations is concerning. However, valuations are a poor measure of market “bubbles.” Why? Because “bubbles” are a “psychological phenomenon” where investor “greed” completely overrides “logic” and “restraint.”

“Greed” Really Isn’t Good

Throughout history, all market crashes have been the result of things unrelated to valuation levels, such as liquidity issues, government actions, monetary policy mistakes, recessions, or inflationary spikes. Those events were the catalyst, or trigger, that started the “reversion in sentiment” by investors.

Market crashes are an “emotionally” driven imbalance in supply and demand.

Such has nothing to do with fundamentals. It is strictly an emotional panic, which is ultimately reflected by a sharp devaluation in market fundamentals. As Bob Bronson once penned:

“It can be reasonably assumed that markets are sufficient enough that every bubble is significantly different than the previous one, and even all earlier bubbles. It’s to be expected that a new bubble will always be different from the previous one(s). Investors will only bid prices to extreme overvaluation levels if they are sure it is not repeating what led to the last, or previous bubbles.

Comparing the current extreme overvaluation to the dotcom is intellectually silly.

I would argue that when comparisons to previous bubbles become most popular, like now, it’s a reliable timing marker of the top in a current bubble. As an analogy, no matter how thoroughly a fatal car crash is studied, there will still be other fatal car crashes, even if drivers avoid the previous accident-causing mistakes.”

Comparing the current market to any previous period in the market is rather pointless. The current market is not like 1995, 1999, or 2007? Valuations, economics, drivers, etc. are all different from cycle to the next. Most importantly, however, the financial markets adapt to the cause of the previous “fatal crashes.” Still, that adaptation won’t prevent the next one.

Signs Of Exuberance

So, if “bubbles” are specifically a function of “speculative appetite,” there should be some relevant indications suggestion that such exists.

One of the best measures of “exuberance” is looking at “options speculation.” Options are leveraged bets for market participants, which can, and often do, wind up worthless in value. There have only been two previous points in history where options speculation was this high – February 2020 and March 2000.

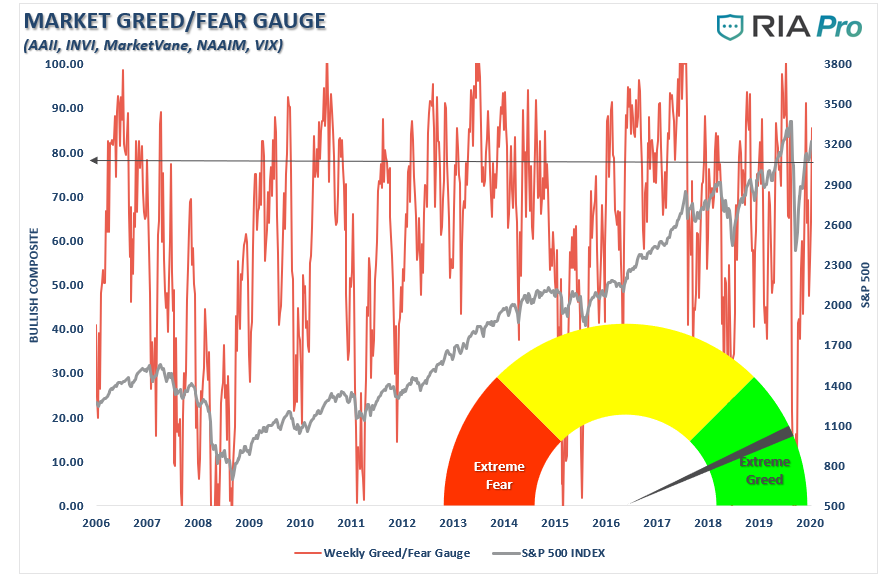

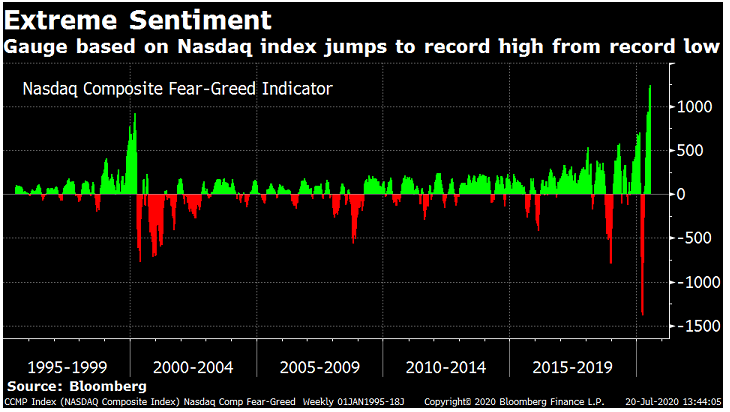

The RIAPro “Fear/Greed” gauge is based on both retail and professional investor positioning in the markets. That indicator is well back into “greed “ territory.

However, those measures are more reflective of the broader markets. Like 1999, the real exuberance is in the Nasdaq, where sentiment has jumped to a record high.

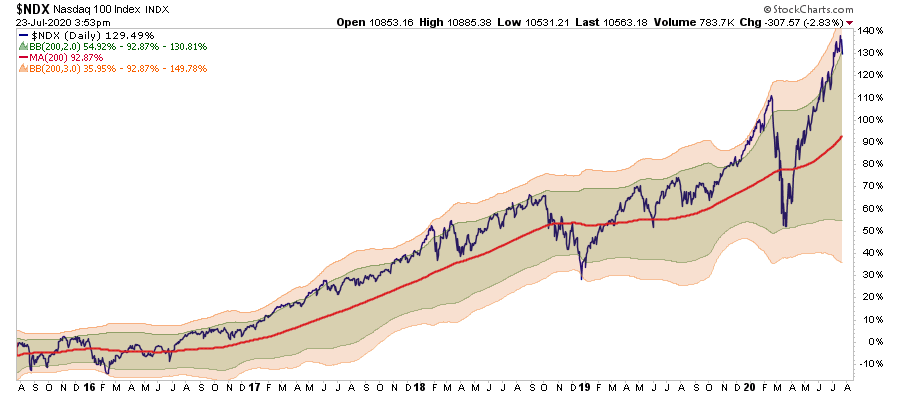

Furthermore, a reflection of the underlying “greed” is in the market’s price relative to its longer-term moving averages. The chart below shows the 2- and 3-standard deviation ranges of the Nasdaq 100 index from the underlying 200-dma.

Longer-term moving averages are the “gravity” to prices. The greater the deviation from the long-term moving average, the greater the “pull” on prices. With regularity, extreme deviations in one-direction lead to a “mean reverting” event in the other. Currently, the Nasdaq 100 index is trading 3-standard deviations above the 200-dma. The last time was this past February.

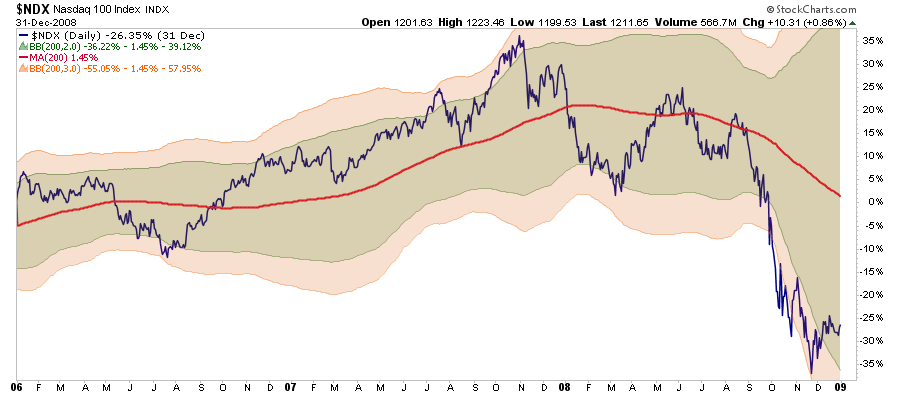

But we saw it previously in August and November of 2007.

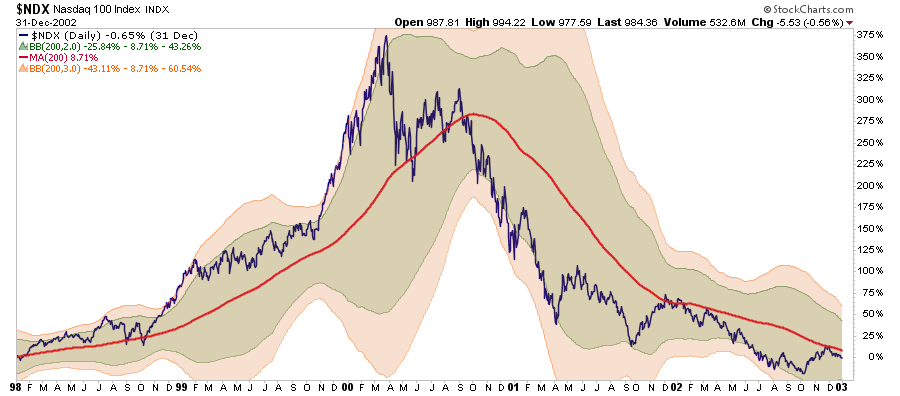

And, of course, in 1999-2000.

While such deviations do not necessarily mean that a massive correction is imminent, it does suggest elevated risk. When prices become this extreme, it only takes a little “nudge” to start a correction.

History Doesn’t Repeat

“History Doesn’t Repeat Itself, but It Often Rhymes” – Mark Twain.

Again, none of this suggests the market is going to crash tomorrow. But a mean-reversion process is coming, it is inevitable, the only question is of the timing.

Remaining fully invested in the financial markets without a thorough understanding of your ‘risk exposure’ will likely not have the promised result you desire.

My job, as a steward of our client’s assets, is to participate in the markets while keeping a measured approach to capital preservation. Since it is considered “bearish” to discuss investment “risk,” then I guess you can call me a “bear.”

Just make sure you understand I am still in “theater,” we are just moving much closer to the “exit.”

As we saw in March, when someone does eventually yell “fire,” we want to make sure there is easy access to an “exit.”

Defining Our Job

“The more things change, the more they remain the same.”

If you have been around the markets for any length of time, you can quickly spot the “pigeons at the poker table.” They are the ones that rationalize why prices can only rise, why “this time is different,” and focus only on the bullish supports. Trying to “draw to an inside straight” is not impossible, it just leads to losses more often than not.

But therein lies an important point.

As investors, our job is NOT making a case for why markets will go up.

Read that again.

Coming up with reasons why markets will rise is a pointless endeavor when you are already invested.

If the markets rise, terrific. We all made money, and we are the better for it. However, that is not our job.

Our job is to analyze, understand, measure, and prepare for what will reduce the value of our invested capital.

Period.

How To Survive The Tech Bubble

If we are to accumulate capital over the long-term, the most important thing to ensure success is to avoid large capital losses.

Therefore, our job as investors is quite simple:

- Capital preservation

- A rate of return sufficient to keep pace with the rate of inflation.

- Expectations based on realistic objectives. (The market does not compound at 8%, 6% or 4%)

- Higher rates of return require an exponential increase in the underlying risk profile. Such tends to not work out well.

- You can replace lost capital – but you can’t replace lost time. Time is a precious commodity that you cannot afford to waste.

- Portfolios are time-frame specific. If you have a 5-years to retirement but build a portfolio with a 20-year time horizon (increasing draw-down risk,) the results will likely be disastrous.

With forward returns likely to be lower and more volatile than promised by the mainstream media, the need for a more conservative approach is rising. Controlling risk, reducing emotional investment mistakes, and limiting the destruction of investment capital is the formula for investment success.

The Rules

The following investment guidelines are not new, nor totally unique, but are ones I have learned, and relearned, over the last 30 years.

- Investing is not a competition. There are no prizes for winning but there are severe penalties for losing.

- Emotions have no place in investing.You are generally better off doing the opposite of what you “feel” you should be doing.

- The ONLY investments that you can “buy and hold” are those that provide an income stream with a return of principal function.

- Market valuations (except at extremes) are very poor market timing devices.

- Fundamentals and Economics drive long-term investment decisions – “Greed and Fear” drive short-term trading. Knowing what type of investor you are determines the basis of your strategy.

- “Market timing” is impossible– managing exposure to risk is both logical and possible.

- Investment is about discipline and patience. Lacking either one can be destructive to your investment goals.

- There is no value in daily media commentary– turn off the television and save yourself the mental capital.

- Investing is no different than gambling– both are “guesses” about future outcomes based on probabilities. The winner is the one who knows when to “fold” and when to go “all in”.

- No investment strategy works all the time. The trick is knowing the difference between a bad investment strategy and one that is temporarily out of favor.

As an investment manager, I am neither bullish or bearish. I simply view the markets through the lens of statistics and probabilities. Our job is to manage the inherent risk to investment capital.

Yes, markets have always recovered their losses, but that isn’t the same thing as making money.