The October labor report, released Friday, indicated slowing job growth in the US last month. The economy added 150k jobs in October versus a consensus estimate of 180k. A sharp decline from the 297k jobs added in September, and although the media is touting a “goldilocks labor report,” the numbers are more concerning under the surface. Government payroll growth remained steady at 51k in October, beating the consensus estimate of 29k. However, private payroll growth of 99k came in significantly below expectations of 158k. The UAW strikes removed roughly 33k from manufacturing payrolls, but even excluding that impact, private payrolls still would’ve missed expectations.

The unemployment rate ticked up to 3.9% from 3.8% in September, while average weekly hours declined to 34.3 from 34.4 in September. Additionally, wage growth slowed to 0.2% MoM in October from 0.3% in September, which bodes well for inflationary pressures. The lukewarm labor report sent yields screaming lower as traders re-assessed the odds of further policy tightening by the Federal Reserve. The S&P 500 also finished higher to cap off its best week this year as investors welcome falling yields.

What To Watch Today

Economic

- No notable economic releases of note

Earnings

Market Trading Update

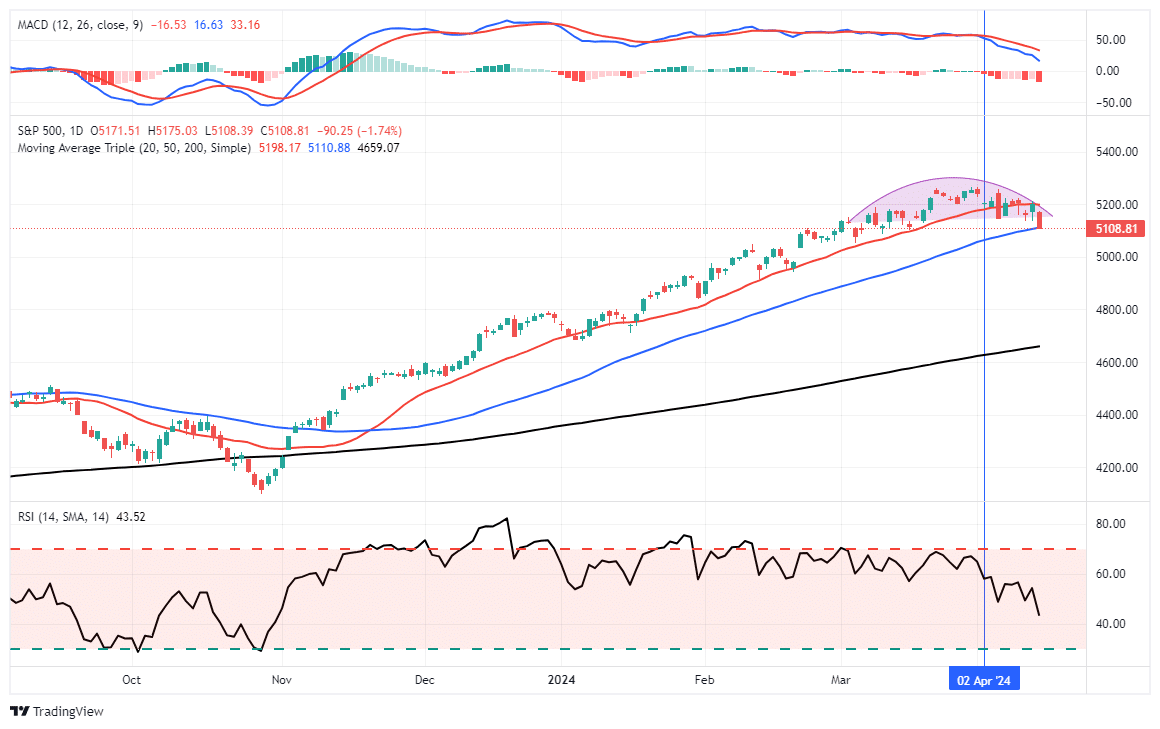

While there is support for a rally into year-end, there are also substantial risks ahead. As shown in the chart below, while we are looking for a rally, we also have several levels that will provide resistance where we will look to rebalance risks. We pushed through the 50% retracement level, which is also the 50-DMA. As noted above, that clears the way for a rally higher with a more bullish tone. That now sets the next targets at the 61.8% and 78.6% levels, then this year’s highs. While the highs are certainly possible, it is most likely a low-probability event.

Regardless of the eventual outcome, the market will not go to those levels in a straight line. Therefore, as we noted last week:

“The market is oversold, and the recent selling pressure across all assets is nearing exhaustion. If you are worried about what is happening overseas or with the Fed and the economy, use rallies to reduce risk at better price levels.”

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against more significant market declines.

- Take profits in positions that have been big winners.

- Sell laggards and losers.

- Raise cash and rebalance portfolios to target weightings.

From a portfolio management perspective, we have to trade the market we have rather than the one we think should be. This can make the challenge of battling emotions difficult from week to week. However, the rally we expected has arrived and is providing a better risk/reward opportunity to rebalance equity exposure.

As noted last week, “Periods like this are never fun, but the market never goes straight up or down. However, the psychological strain during periods of market weakness leads to a host of behavioral mistakes that lead to longer-term underperformance. This period will pass, and the next bullish cycle will begin. Sometimes, turning off the television can help reduce the emotional toll of headline news.”

It may have passed for now, but such doesn’t mean the risk is entirely removed. Trade accordingly.

The Week Ahead

This week will be light on the economic data front as earnings season rolls on. The only reports of note are the Weekly Jobless Claims on Thursday and Michigan Consumer Sentiment on Friday. Economists expect jobless claims of 215k, down from 217k last week. Consumer sentiment is expected to creep up to 64 from 63.8 but remains well below pre-pandemic norms.

There are several speeches by Federal Reserve officials scheduled throughout the week. Most notably, Chair Powell will speak Wednesday at 10:15am EST and Thursday at 3pm EST.

Extreme Divergences Don’t Last Forever

The chart below shows the YTD relative performance versus the S&P 500 for various factors and themes we monitor in SimpleVisor. Only a handful of the factors have outperformed the index this year, and market developments have resulted in some oddities in relative performance. What’s more alarming is the magnitude of the divergences. The Mega Cap Growth basket has outperformed the index by 22.5% this year, while the Large Cap Growth basket has only outperformed by 5%. On the other side of the ledger, small and mid-caps have underperformed by -15% and -12%, respectively. The harsh reality of this year is that if your portfolio wasn’t concentrated in a small group of stocks, you’ve most likely underperformed the index. The market has punished well-diversified portfolios this year, but extreme divergences like this tend not to persist forever. Opportunity exists whether the underperformers catch up to the outperformers or vice versa.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.