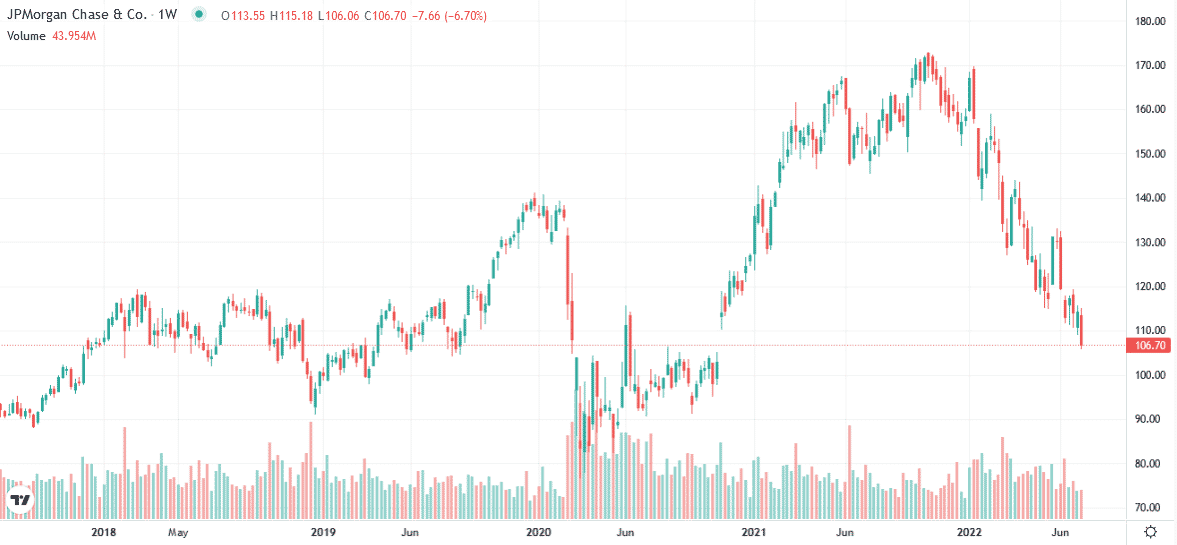

JP Morgan (JPM) kicked off the Q2 earnings season with disappointing results. JPM earnings per share and revenues missed expectations as interest rates and the inverted yield curve weigh on profitability. For example, JPM’s mortgage production fees are down by 71% year over year. That one line item reduces its revenue by $357 million. Global investment banking fees fell 54% as capital market activity, such as IPOs and SPAC issuance, are light this year. Morgan Stanley echoed similar problems regarding capital market revenue.

In early June, JPM CEO Jamie Dimon warned we should brace for an “economic hurricane.” JPM is doing just that. The company suspended share buybacks as it bolsters capital to meet higher capital requirements. Translation: they are battering down the hatches as the hurricane approaches.

What To Watch Today

Economy

- 8:30 a.m. ET: Empire Manufacturing, July (-2.0 expected, -1.2 prior),

- 8:30 a.m. ET: Retail Sales Advance, month-over-month, June (0.9% expected, 0.3% prior)

- 8:30 a.m. ET: Retail Sales excluding autos, month-over-month, June (0.7% expected, 0.5% prior)

- 8:30 a.m. ET: Retail Sales excluding autos and gas, month-over-month, June (0.1% expected, 0.1% prior)

- 8:30 a.m. ET: Retail Sales Control Group, June (0.3% expected, 0.0% prior)

- 8:30 a.m. ET: Import Price Index, month-over-month, June (0.7% expected, 0.6% prior)

- 8:30 a.m. ET: Import Price Index excluding Petroleum, month-over-month, June (0.2% expected, -0.1% prior)

- 8:30 a.m. ET: Import Price Index, year-over-year, June (11.4% expected, 11.7% prior)

- 8:30 a.m. ET: Export Price Index, month-over-month, June (1.2% expected, 2.8% prior)

- 8:30 a.m. ET: Export Price Index, year-over-year, June (19.9% expected, 18.97% prior)

- 9:15 a.m. ET: Industrial Production, month-over-month, June (0.1% expected, 0.2% prior)

- 9:15 a.m. ET: Capacity Utilization, June (80.8% expected, 79.0% prior, upwardly revised to 80.8%)

- 9:15 a.m. ET: Manufacturing (SIC) Production, June (-0.1% expected, -0.1% prior)

- 10:00 a.m. ET: Business Inventories, May (1.4% expected, 1.2% prior)

- 10:00 a.m. ET: University of Michigan Sentiment, July preliminary (50 expected, 50 prior)

- 10:00 a.m. ET: University of Michigan Current Conditions, July preliminary (53.7 expected, 53.8 prior)

- 10:00 a.m. ET: University of Michigan Expectations, July preliminary (47 expected, prior)

- 10:00 a.m. ET: University of Michigan 1-Year Inflation, July preliminary (5.3 expected, 5.3% prior)

- 10:00 a.m. ET: University of Michigan 5-10-Year Inflation, June final (3.0% expected, 3.1% prior)

Earnings

Pre-market

- Wells Fargo (WFC) to report adjusted earnings of 80 cents on revenue of $17.54 billion

- BlackRock (BLK) to report adjusted earnings of $7.90 on revenue of $4.65 billion

- Citigroup (C) to report adjusted earnings of $1.70 on revenue of $18.48 billion

- BNY Mellon (BK) to report adjusted earnings of $1.12 on revenue of $4.18 billion

- UnitedHealth (UNH) to report adjusted earnings of $5.19 on revenue of $79.62 billion

- Progressive (PGR) to report adjusted earnings of 85 cents on revenue of $12.39 billion

- US Bancorp (USB) to report adjusted earnings of $1.07 on revenue of $5.92 billion

- State Street (STT) to report adjusted earnings of $1.73 on revenue of $3 billion

- PNC Financial (PNC) to report adjusted earnings of $3.14 on revenue of $5.14 billion

Post-market

- No notable reports are set for release.

Market Trading Update – Going Nowhere Fast

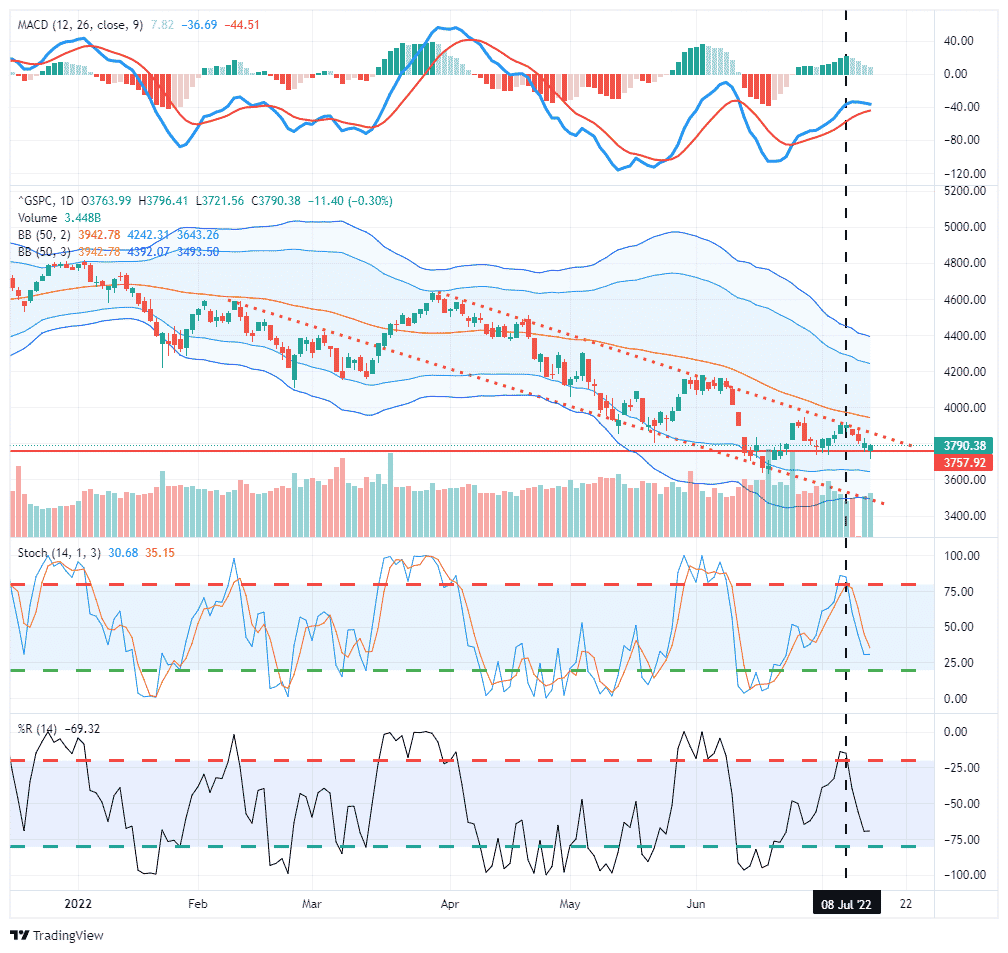

The market remains under pressure after triggering sell signals (two lower panels). However, as noted earlier this week, support continues to hold at last week’s lows. As such, the overbought condition is getting worked off, but the MACD has turned down and threatens a more important sell signal. That signal could get reversed if the market can muster a rally; however, the downtrend line from the March highs continues to be formidable resistance. We continue to remain risk-averse for now and raised cash a bit more this week. Earnings will be a big market driver over the next several weeks. While JPM may be setting a tone, we will continue to adjust our views accordingly if earnings surprise on the upside, but we think that is a very low probability event.

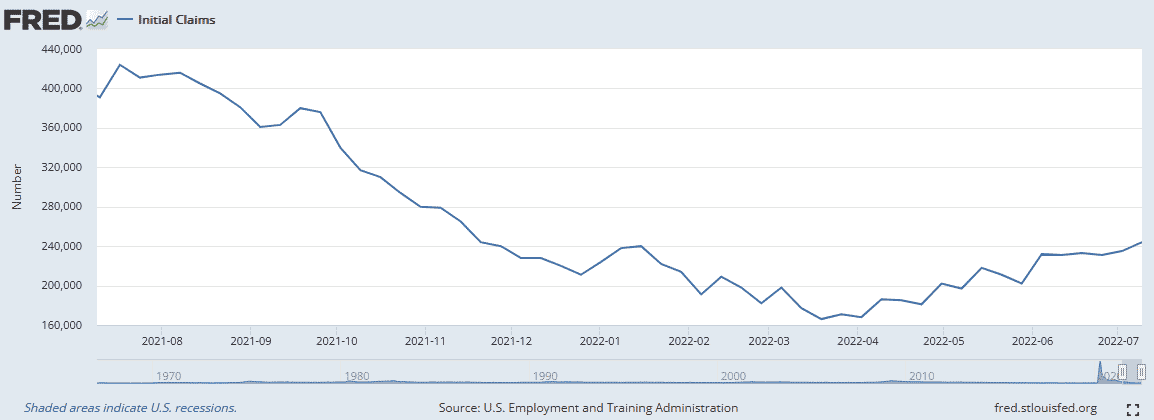

PPI and Jobless Claims

Jobless Claims came in at 244K. While it is not much higher than the previous week’s 235K, it is the high water mark for the year. The number of claims remains relatively low, but the trend is clearly rising. For some context, jobless claims bottomed at 166k in mid-March but only a year ago were above 400k.

PPI, like CPI, rose more than expected. However, unlike CPI, the core reading (excluding food and energy) was below expectations. PPI, at +1.1% is a 13.2% annualized increase. Core PPI only rose .4%, which equates to 4.8% annualized. In yesterday’s commentary, we shared a table highlighting relatively steep price declines in many food and energy commodities. Those price declines did not work their way to the prices consumers pay at restaurants, grocery stores, and gas stations. It also appears they did not have much of an effect on the PPI calculations. We suspect they will help temper PPI readings next month. PPI will likely lead CPI as lower prices work their way from farm to table, so to speak.

Fears of a 1% Rate Hike Inverts the Yield Curve

The higher-than-expected CPI report sent shock waves through the rates markets. As the graph below shows, Fed Funds futures fell about 20bps yesterday, implying an 80% chance the Fed will hike rates by 1.00% at the July 27th meeting. While the shorter maturities rose in yield with expectations for a more aggressive Fed, yields on longer maturities fell. As a result, the 2yr/10yr yield curve is now inverted by 25bps, the most negative since March 2000, when it dipped to -47bps. In no uncertain terms, the bond market is warning that the Fed will aggressively raise rates to fight inflation but will trigger a recession in the process. There is a silver lining. Implied breakeven inflation rates fell yesterday, meaning the bond market has confidence that the Fed will get inflation back to more normal levels.

NASDAQ at a Critical Support Line

The graph below shows two long-term support lines for the NASDAQ (QQQ). Currently, as shown in blue, QQQ is sitting on a support line going back to the bottom of the financial crisis in 2009. If that line fails to hold, the next support, and we would argue more critical of the two in red, sits at 240, which is about 15% below current levels. The red line has repelled the NASDAQ on five occasions since 2010. Also, note, the pre-pandemic peak is at the same level as the red support line, providing additional support.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.