The April CPI inflation headline number, most followed by the media, provided a pleasant downward inflation surprise. The year-over-year inflation number was 4.9%, .1% lower than expectations. This is the first time annual inflation has been below 5% in two years. The monthly change was +.4%, in line with expectations. We call it a “surprise” because many Wall Street banks and dealers thought the inflation numbers would be higher than expected. While the headline was a surprise, the core inflation data, most followed by the Fed, continues to show stickiness in prices falling. Core CPI, excluding food and energy, fell by .1% to 5.5%, as expected.

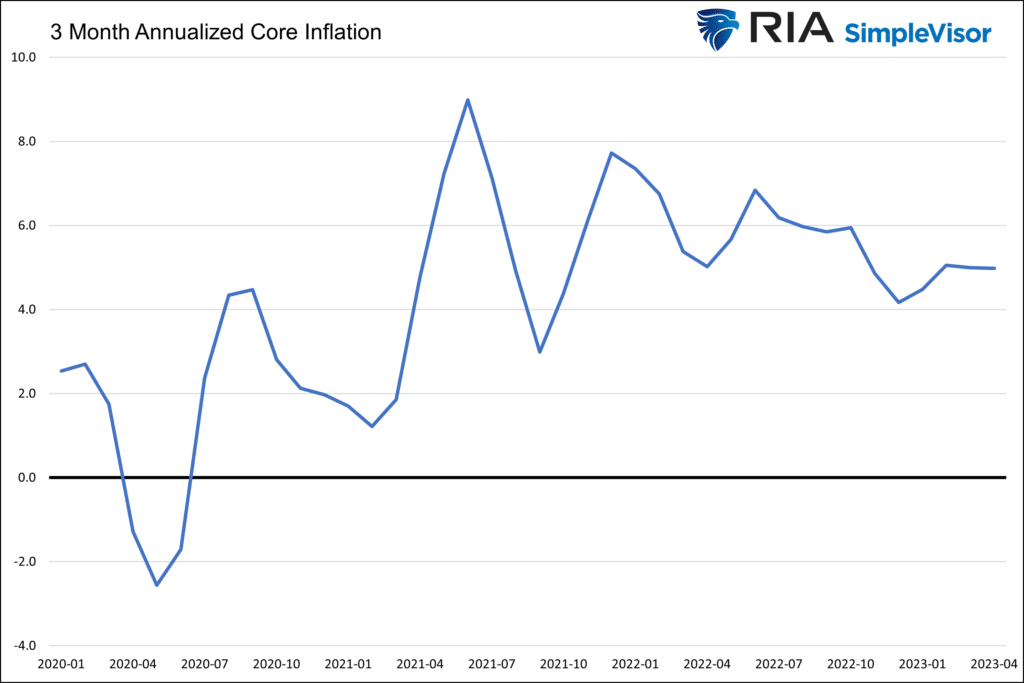

Given the high inflation rates a year ago and their outsized effect on annual data, we prefer to focus on the recent trend. Accordingly, in this environment, we use the running three-month annualized data. The graph below shows the downward surprise was limited to the headline inflation data. Three-month annualized core inflation, while certainly lower than its 9% peak in June 2021, remains stubborn. However, inflation surprises may be just around the corner. About a third of the inflation data is based on imputed rents. The Zillow Rent Index (ZROI) was up 4.62% year over year and 2.81% on a three-month annualized basis. ZROI peaked in January 2022 at 16%. The CPI rent measure is still at its peak and will inevitably follow ZROI lower in the coming months.

Bottom line: Inflation is falling by not at the rate the Fed would like it to. That said, they may be pleasantly surprised in a few months if the BLS measure of rents declines as expected.

What To Watch Today

Earnings

Economy

Market Trading Update

As noted in yesterday’s update, the CPI report was a “nothing burger” coming in as expected with the headline up 0.4%, which is 4.8% annualized inflation. While the market struggled with the data and sold off in the first half of the day, a late-day rally returned the market towards the day’s highs and above the 20-DMA once again. Even with the rally, the market remains range bound but continues to flirt with the top of a narrowing consolidation pattern. At some point, the market will make a decisive break out of this pattern, giving us the best opportunity to position ourselves for the next leg of the market’s move. Unfortunately, we don’t know with certainty whether that will be higher or lower.

As such, we continue to suggest remaining cautious. We will likely have our answer to “what’s next” sooner than later.

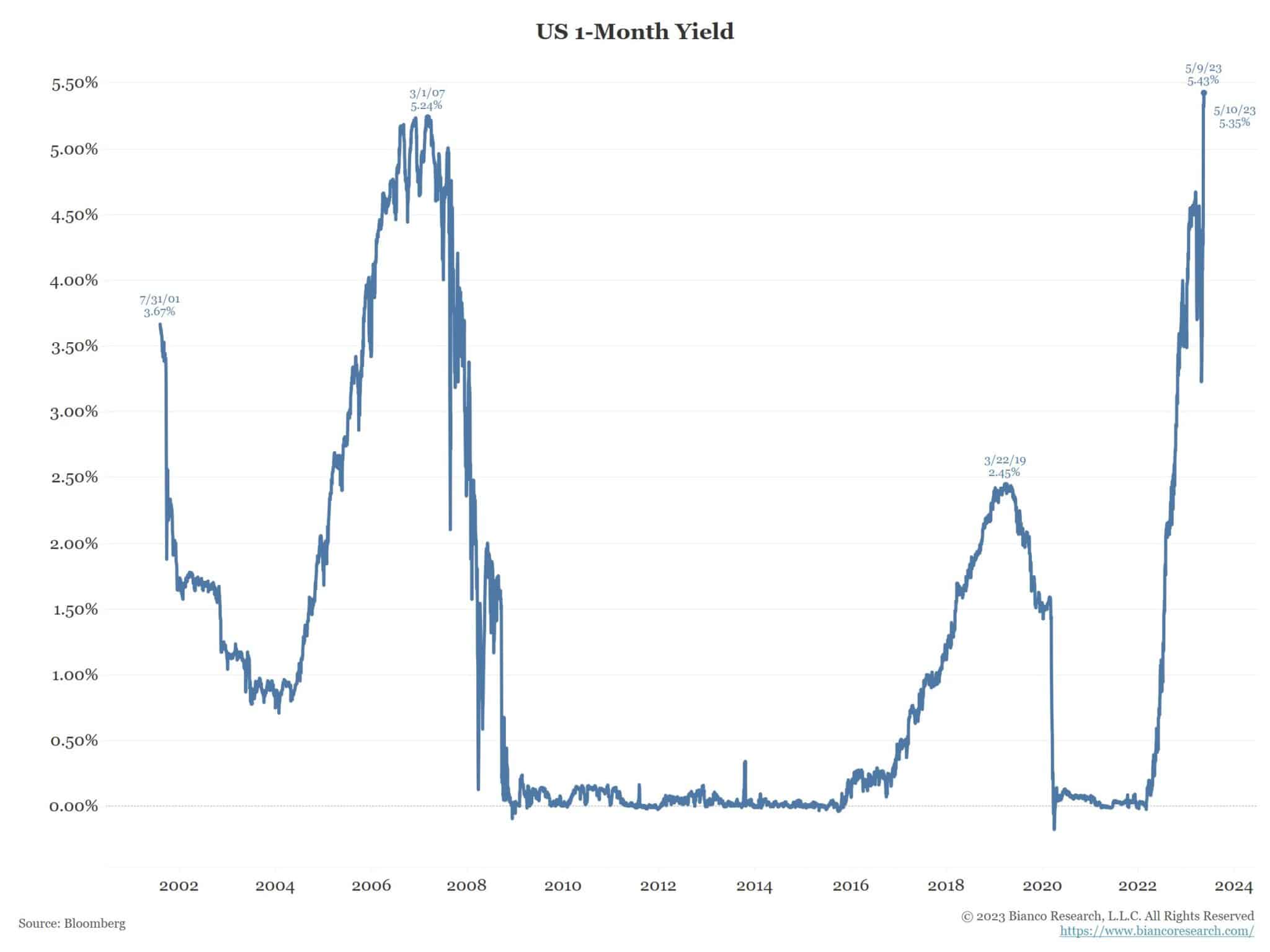

One-Month T-Bills Hit Record High Yield Awaiting The Debt Cap

As the graph below from Bianco Research shows, the year on a one-month Treasury bill hit 5.43%. Such is a record high since the Treasury began issuing one-month bills over 20 years ago. If you recall, a few weeks ago, we discussed how the one-month yield was plummeting while two and three-month bills stayed the same. At that time, the one-month yield at times was more than 1% below the three-month bill. Today it’s about 25bps above.

The culprit is the coming debt cap negotiations. The concern for one-month bill investors is not a default but a delayed payment. Given the short duration of a one-month bill, a multi-day delay can have a decent effect on the annualized yield.

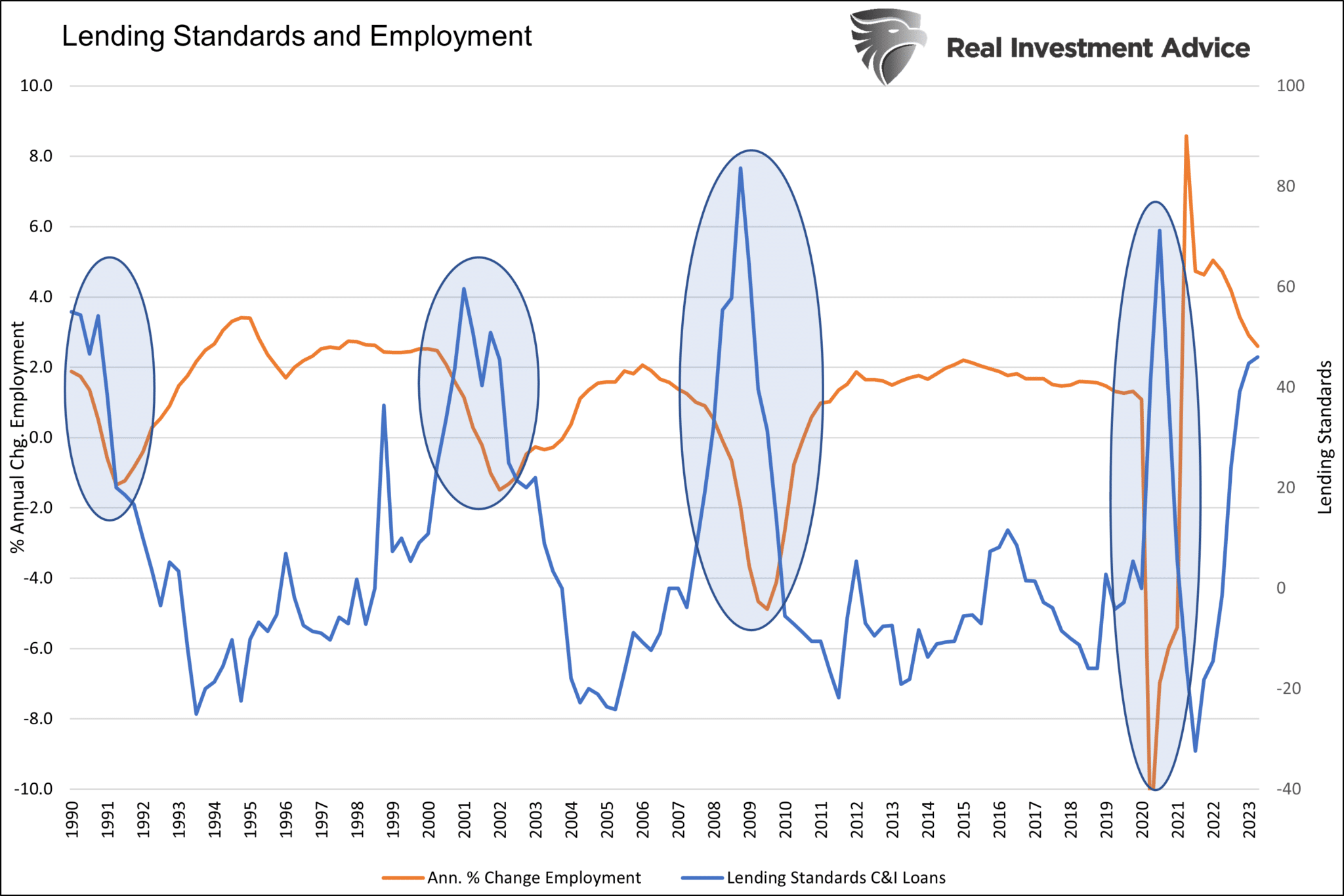

Lending Standards Lead Employment

In Monday’s Commentary, we noted:

Meanwhile, demand for commercial and industrial loans weakened considerably. The survey reported the broadest share of banks with weaker loan demand since 2009.

The graph below shows lending standards for commercial and industrial (C&I) loans (blue) have tightened considerably. It also shows that in the last three recessions, excluding 2020, the annual change in employment fell and troughed about 3-4 quarters later. There was no lag in 2020 as the pandemic had an immediate economic impact. Based solely on this data, we should expect the unemployment rate to increase.

When Druckenmiller Speaks, People Listen

Famed investor Stanley Druckenmiller presented at the Sohn Investment Conference on Tuesday and provided plenty of advice. Druckenmiller made a name for himself as one of George Soros’s top portfolio managers and ultimate successor.

Druckenmiller is bearish on the near-term outlook and sees a hard landing. He thinks that NBER will ultimately find a recession started this quarter. That says he does see opportunities once the economy bottoms. To wit- “A hard landing will offer unbelievable opportunities.“

…when you have free money, people do stupid things. When you have free money for 11 years, people do really stupid things. So there’s stuff under the hood, it’s starting to emerge. Obviously the regional banks recently, we had Bed Bath and Beyond.

But I would assume there’s a lot more bodies coming.

Just make sure to preserve your capital until they present themselves.

Druckenmiller likes copper due to what he thinks will be explosive EV growth. That said, he is waiting on buying it as he fears a recession will hurt demand and allow him to buy it at lower prices. He does like gold and silver, although he says, “They historically have not done well in hard landings.“

He also thinks AI “could be every bit as impactful as the internet literally going forward.” However, like copper, he seems to be waiting for a hard landing to make a bigger bet in the industry. Currently, he owns Microsoft and Nvidia.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.