Despite the largest bull market in history, 80% of Americans still struggle with their finances and are unprepared for retirement. Such a reality is a stark difference from the belief that rising asset prices benefit the masses.

**** New Report for update

https://collabfund.com/blog/its-supposed-to-be-hard/

A year after the Covid-19 pandemic struck the U.S. economy more than 80% of American’s surveyed stated the events affected their retirement plans. One-third of the more than 1,200 financial decision-makers said it would take them two to three years to get back on track. Such was due to factors like job loss or withdrawals from retirement savings.

Another study from the National Council For Aging also shows rising financial risks for American households.

“Our July 2021 updated analysis revealed that most older Americans have made little to no progress toward financial security. As in 2016, our analysis of 2018 data finds that 80%—or 47 million households with older adults—are financially struggling today or are at risk of falling into economic insecurity as they age. Between 2016 and 2018, we see that any increases in the net value of wealth occur to a greater extent for those with the most wealth. Moreover, this trend is worsening over time, as 90% of older households experienced decreases in income and net value of wealth between 2014 and 2016.“

Interestingly, these surveys come after the Government injected nearly $5 trillion into the economy and the Fed’s $120 billion monthly injections doubled asset prices from the March 2020 lows.

So, what went wrong?

Stark Inequality

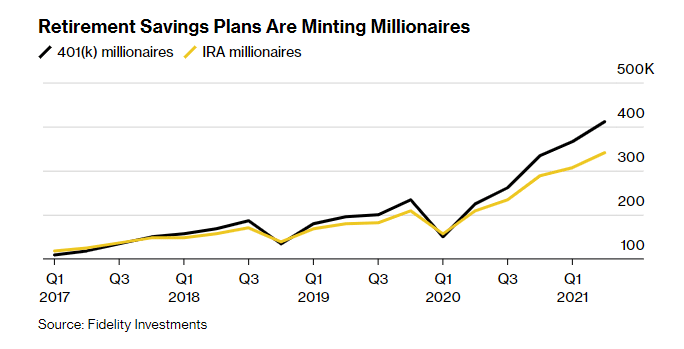

In 2021, Fidelity published its latest analysis showing that a record number of retirement accounts achieved balances of more than $1 million dollars. To wit:

The ranks of 401(k) and IRA millionaires are exploding.

The number of 401(k) accounts with balances of at least $1 million at Fidelity Investments grew 84% year over year to 412,000, while the number of seven-figure IRAs jumped more than 64% to 341,600 in the 12 months that ended in the second quarter, Fidelity said. Together, the number of accounts with $1 million or more grew 74.5% — though it isn’t clear how many individuals that represents, because people can have multiple accounts.” – Bloomberg

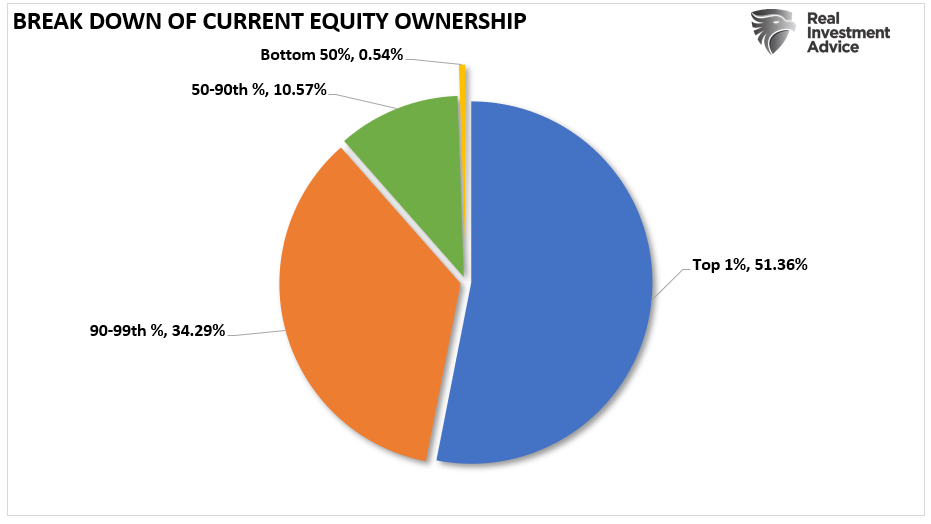

While the “number of retirement millionaires” made headlines, an important piece of the analysis was overlooked.

Those 412,000 accounts make up only a small fraction of the 27.2 million retirement accounts at Fidelity.

How small of a fraction? About 1.6%, which aligns with the Top 1% of equity ownership in America.

The Bottom 98% Have A Different View

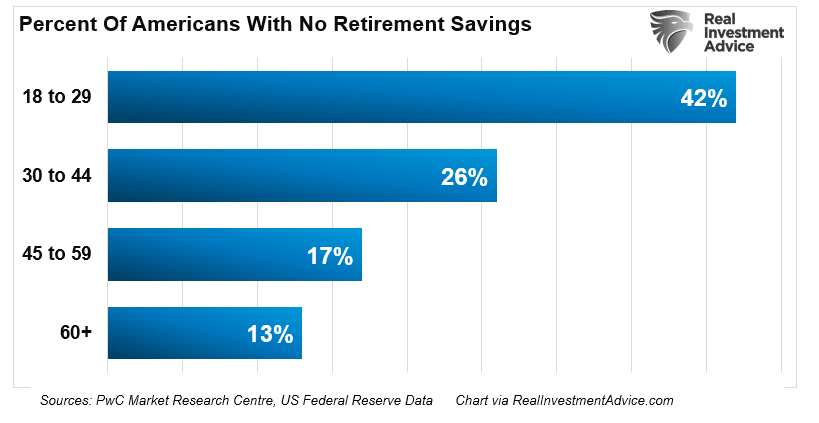

For the other 98% of retirement account holders, the future is not so optimistic. According to Motley Fool:

- The average retirement account savings for American households is $65,000.

- The average American under 35 has $13,000 saved for retirement.

- 62% of Americans aged 18 to 29 have some retirement savings, but only 28% percent feel on track for retirement.

- 55% of non-retirees have a 401(k) or 403(b) while 25% have no retirement savings.

- Americans with a high school degree have an average retirement savings account value of $20,000, while those with a college degree have an average account value of $119,000.

- The average retirement savings of white Americans was roughly $45,000 more than that of Black and Hispanic Americans.

- Retirement savings for households in the bottom 25% of net worth grew by $2,710 from 1989 to 2019. Savings for the top 10% of net worth grew by over $600,000 during that same time period.

- 51% of Americans retire at 61 or earlier, and 23% retire between 62 and 64, before Medicare coverage kicks in at 65. White Americans tend to retire later than Black or Hispanic Americans, despite having more savings.

PwC’s Retirement In America report confirms the same.

“One in 4 Americans have no retirement savings and those who are saving aren’t saving enough. Those that are [saving], on average, what they have saved will afford them like $1,000 a month of actual cash while they’re in retirement.”

The report found that the median retirement account balance for 55-to-64-year-olds is $120,000. When divided over 15 years, that would generate a modest distribution of less than $1,000 per month. The bigger problem is the large percentages of individuals with no retirement savings.

Hard To Save When Income Doesn’t Cover The Bills

There are three primary reasons why individuals fail to save money for retirement:

- Lack of knowledge about budgeting and saving. (15%)

- Cost of living exceeds incomes. (70%)

- Bad previous investing experience (bear market). (15%)

If you ask anyone who doesn’t save or invest money, you will get one of those three answers.

The biggest reason, not surprisingly, is the lack of capital to invest.

In order to save and invest, one must have disposable income that exceeds their cost of living.

While much of the mainstream analysis utilizes “averages,” the message gets distorted when the data set becomes skewed. Such is particularly the case with disposable incomes (DPI). The calculation of DPI (income minus taxes) is a guess due to the variability of household income and individual tax rates.

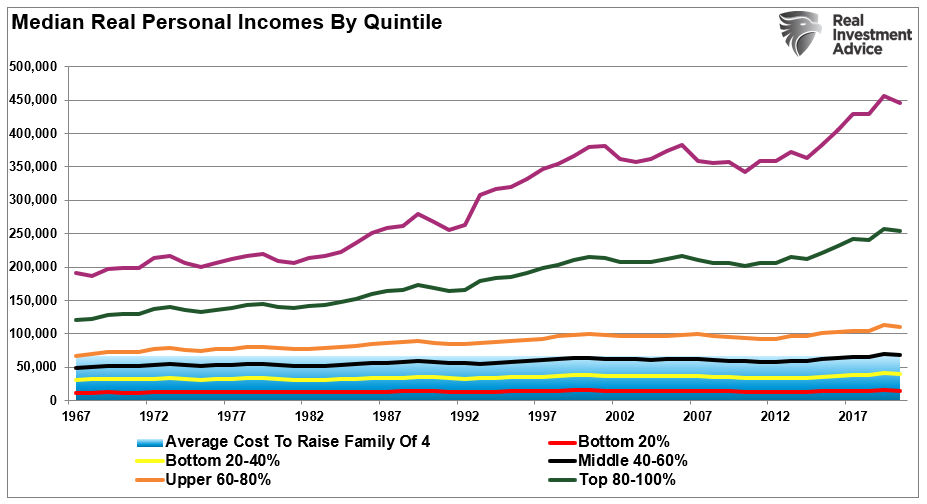

More importantly, the measure becomes skewed by the top 20% of income earners and particularly the top 5%. The chart below shows those in the top 20% saw substantially larger median wage growth versus the bottom 80%. (Note: all data used below is from the Census Bureau and the IRS.)

Furthermore, disposable and discretionary incomes are two very different animals.

Discretionary income is the remainder of disposable income after paying for all mandatory spending like rent, food, utilities, health care premiums, insurance, etc. For the bottom 80% of income earners, the cost of living outstrips a vast majority of those individuals (shaded area).

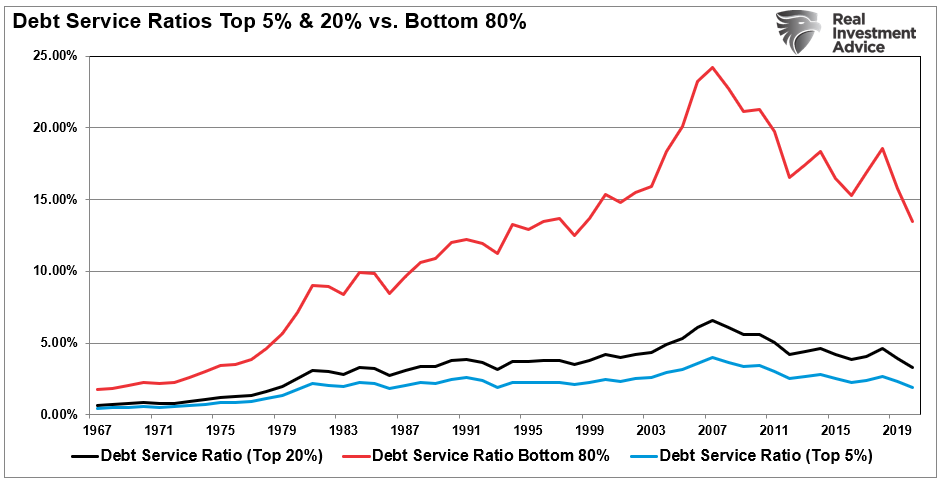

In other words, given the bulk of the wage gains are in the upper 20%, any data that reports an “average” of the information is inherently skewed higher. Such is why a vast difference between the debt service levels (per household) exists between the bottom 80% and top 20%.

No Money, But I Got Credit

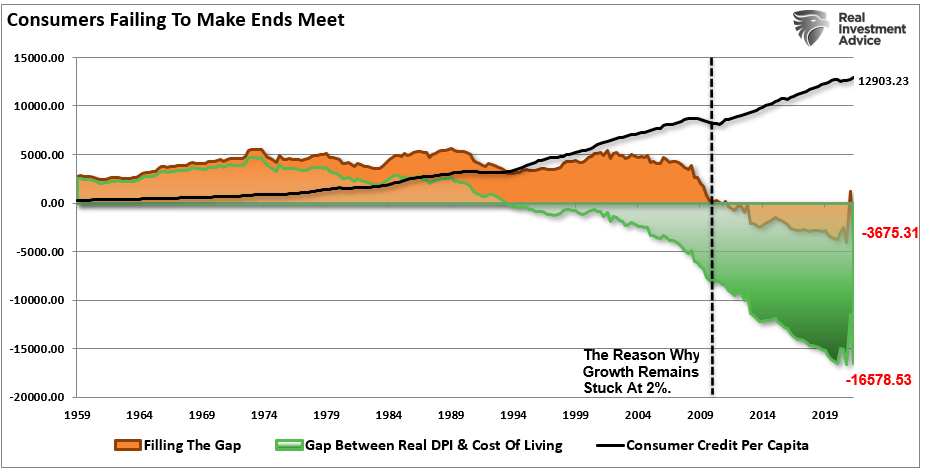

As noted above, sluggish wage growth has failed to keep up with the cost of living which has forced an entire generation into debt just to make ends meet. While savings spiked during the Covid crisis, the rising cost of living for the bottom 80% has outpaced the median level of “disposable income” for that same group. As a consequence, the inability to “save” has continued.

The “gap” between the “standard of living” and real disposable incomes gets shown below. Beginning in 1990, incomes alone were no longer able to meet the standard of living. Such forced consumers into debt to fill the “gap.” Currently, there is a $3600 annual deficit that must get filled by debt.

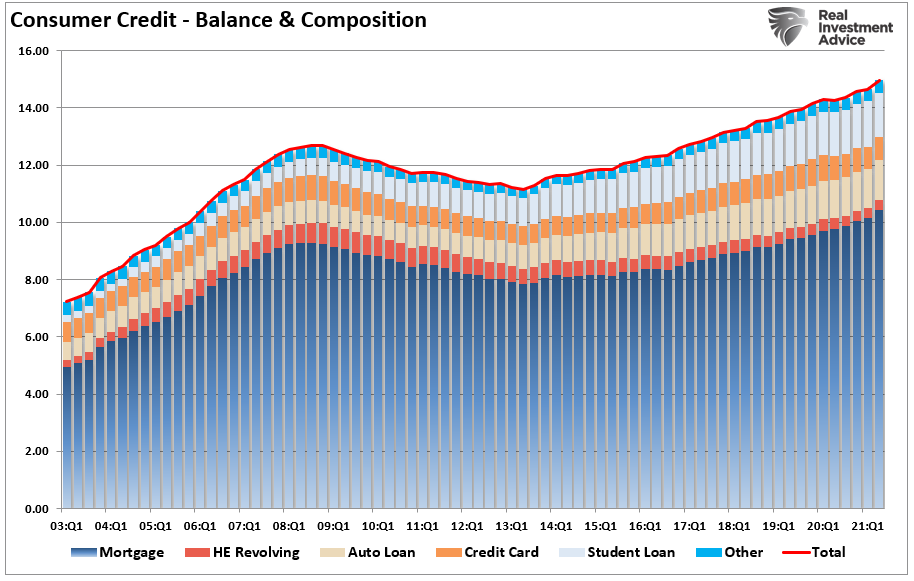

This is why we continue to see consumer credit hitting all-time records despite an economic boom, rising wage growth, historically low unemployment rates.

It is hard to save money and invest when credit card debt is the only backstop between paying bills and feeding the family.

Important Considerations For The Bottom 98%

There are 75.4 million “boomers,” about 26% of the population, heading into retirement by 2030. Only about 20% will be able to retire. The rest will be faced with tough decisions in the years ahead.

However, there are steps to improve your outlook.

- Start cutting expenses and paying of debt to increase monthly cashflow. (No cashflow = no success)

- Excess cashflows go into a standard savings account while building the “saving habit.”

- Once the “habit” is built, continue to increase savings rates. (Ultimate goal is 30% of incomes.)

- Slowly start an investment program with a focus on capital preservation over growth.

For those already in the habit of saving and investing, the following points need careful consideration.

- Expectations for future returns and withdrawal rates must be downwardly adjusted.

- The potential for front-loaded returns going forward is unlikely.

- Consider the impact of taxation on the planned withdrawal rate.

- Calculate future inflation expectations.

- Drawdowns during declining markets accelerate principal bleed. Make plans during up years to harbor capital for reduced portfolio withdrawals during adverse market conditions.

- The low-interest rate environment poses problems for retirement income planning. Don’t chase yield.

- Substitute variable rates of returns from for compounded returns in planning.

With debt levels rising globally, interest rates near zero, economic growth weak, and valuations high, the uncertainty in retirement planning is elevated. Such lends itself to the problem of individuals having to spend a bulk of their “retirement” continuing to work.

The reality is the majority of American’s don’t have $1 million, or more, for retirement. In actuality, most have far less than $250,000. Such is why the vast majority of Americans are working well into their retirement years.

We can all do better.

But we have to start with taking action and educating ourselves on how money, and investing, works.