On August 5, 2011, S&P downgraded the United States’ credit rating to AA+. Almost to the day, twelve years later, Fitch came to the same conclusion as S&P. The U.S. credit rating is not worthy of the AAA rating. If the U.S. were a corporation, Fitch and S&P would likely rate its debt as junk! But, the U.S. is not a company and has abilities that no corporation or other nation has. Fitch’s statement includes the following five reasons to justify their new AA+ rating for the United States:

- Erosion of Governance

- Rising government deficits

- General government debt rising

- Unaddressed medium-term fiscal challenges

- Fed interest rate hikes

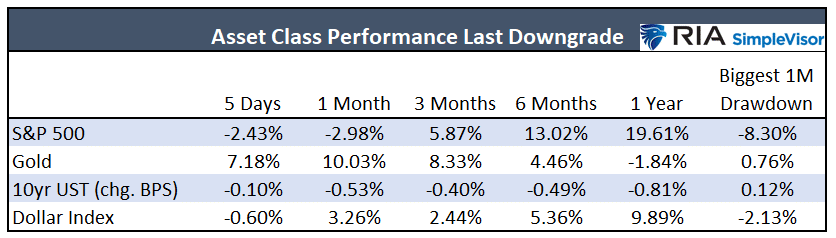

Fitch clarified that further downgrades are possible if the government does not address its fiscal issues and economic policies. So the question facing investors is, do we care? A credit rating on U.S. debt is ridiculous. The U.S. can print money and avoid default no matter how bad its fiscal position is. Accordingly, U.S. Treasury debt will still be considered the world’s only risk-free asset regardless of its ratings. The table below shows the market reactions to the S&P downgrade in 2011. Unexpectedly, bond yields fell appreciably, and the dollar rose, despite the downgrade. One would have thought gold would be a beneficiary. It was initially, but its price was slightly lower a year later. Stocks troughed 8% lower within the first week of the downgrade but were on solid footing afterward. Like twelve years ago, the downgrade may provide opportunities contrary to what many expect.

What To Watch Today

Earnings

Economy

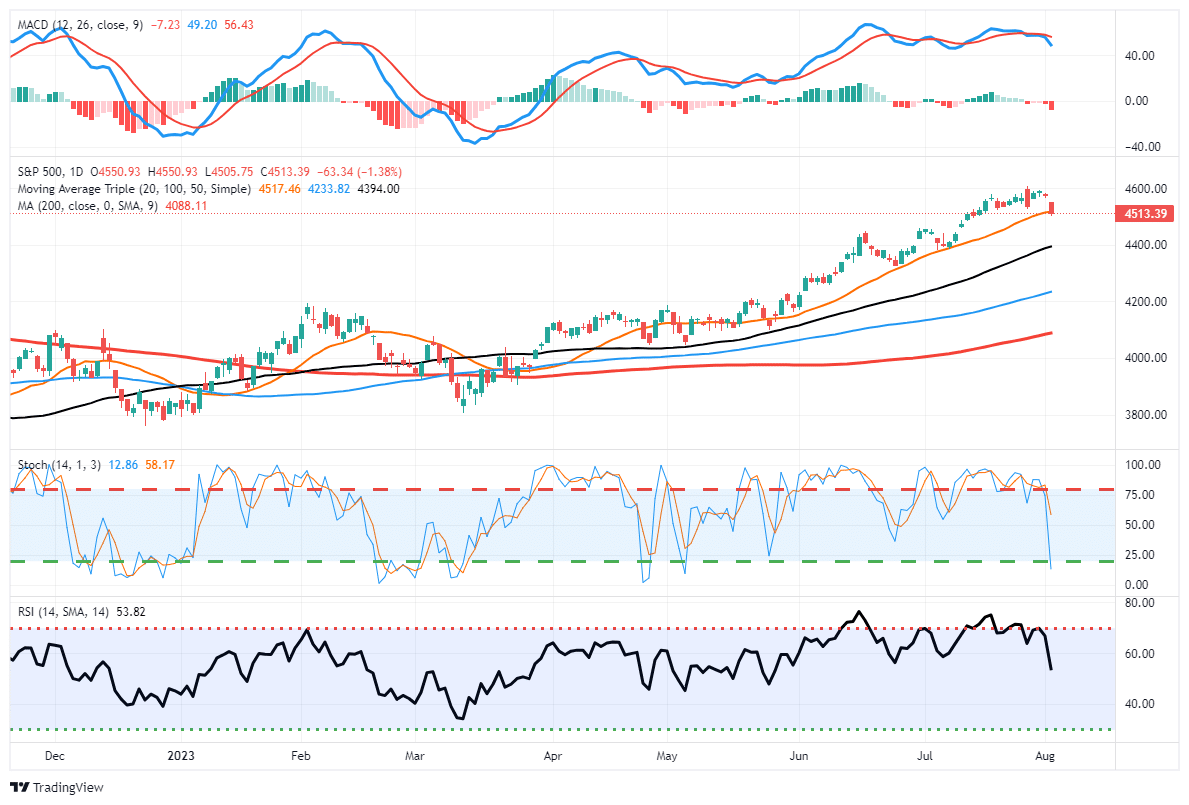

Market Trading Update

The market sold off to start the month of August. However, as noted recently, such would not be surprising given the sharp advance over the last few months. The selloff on Tuesday and Wednesday is beginning to work off some of that overbought condition and playing catch up to the negative divergences in RSI and the MACD discussed on Monday.

So far, the correction has triggered a MACD “sell signal,” suggesting lower prices over the next couple of weeks. While the market is currently testing the 20-DMA support levels, the 50-DMA seems to be a more logical target for the correction. Such would also move markets to a more oversold condition allowing for a better entry point to add to equity exposures.

Given the magnitude of the runup since April, a deeper correction certainly remains possible. As such, we do need to factor in that risk. However, bullish momentum and sentiment remain strong for now, which will likely limit downside draws near term.

Crude Oil Jumps On Massive Inventory Drawdown

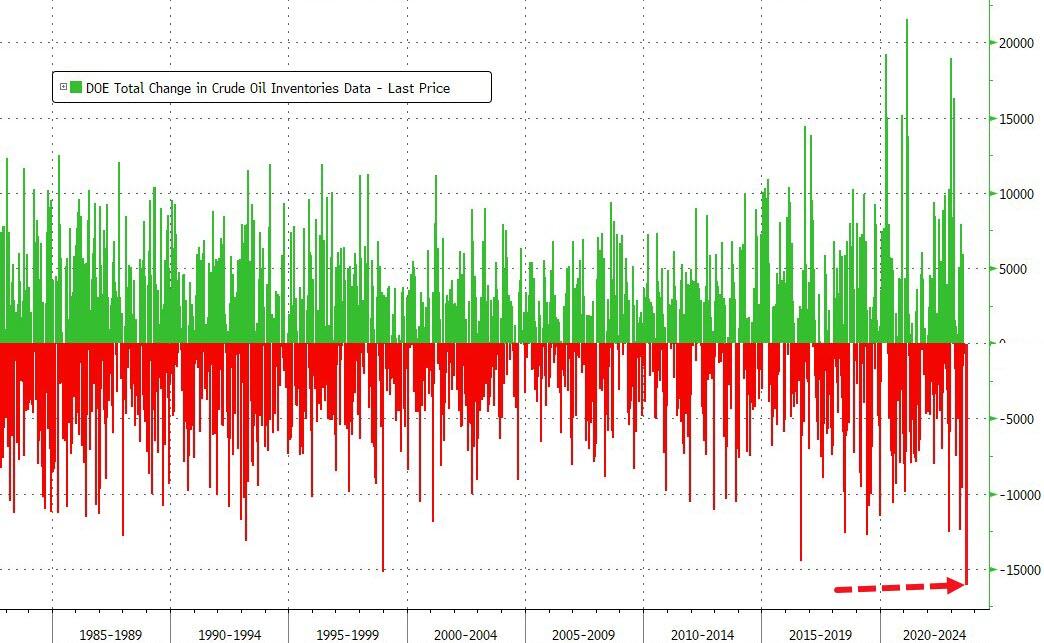

The American Petroleum Institute (API) reported crude inventories fell by 15.4 million barrels in the latest week. As shown below, courtesy of ZeroHedge, it was the largest weekly drawdown on record. Expectations were for a relatively minor 1.5 million barrel drawdown. Making matters worse, OPEC claims it is adhering to its 1 million barrel per day production cut.

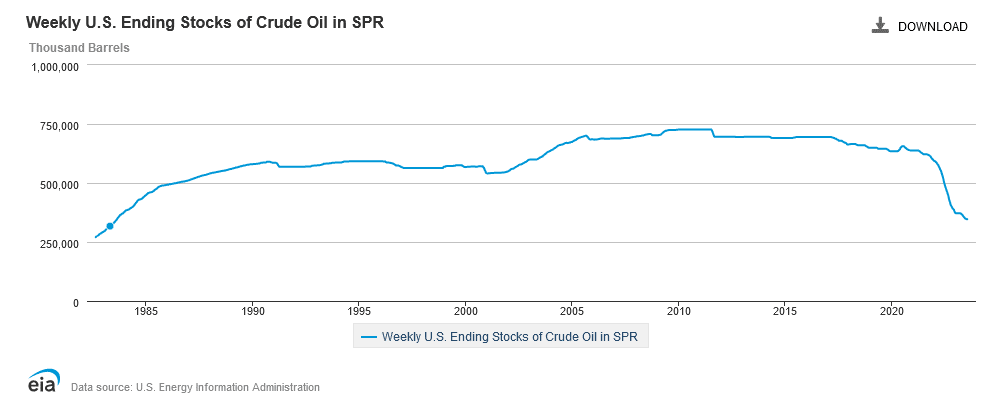

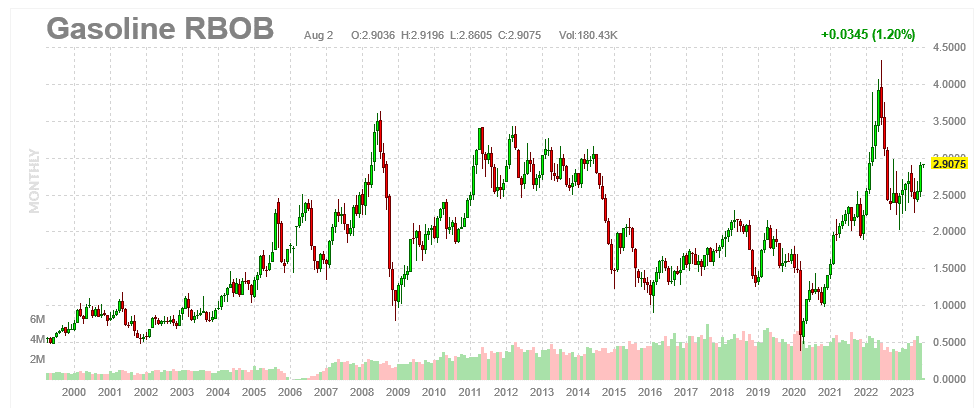

Given the tight supply of crude oil, we doubt President Biden will be able to refill the strategic reserves (second graph) as he recently promised. It’s more likely he will continue to draw down the reserves, which have already been cut by over 40% since 2022. With the Presidential election nearly a year away, managing the price of gasoline will become an increasingly important issue for the Biden team. As such, we suspect they will take whatever actions necessary to keep oil prices contained or even lower. The third graph shows that gasoline futures are in the upper region of its long-standing price range but far from the extremely high prices in early 2022.

On the demand side of the equation, global demand is expected to rise; however, as Bloomberg recently reported: “China’s appetite for fuels and other oil-derived products such as plastics may have peaked for the year as the nation’s economic woes continue to stand in the way of a full rebound from Covid Zero.” China accounts for about 13% of world oil demand, second to the U.S. at 20%. However, their economic growth rate makes them the marginal price setter of oil. As such, watch their economic activity closely, as weakening Chinese demand may help offset supply problems.

ADP Signals A Strong BLS Report Is Coming Tomorrow

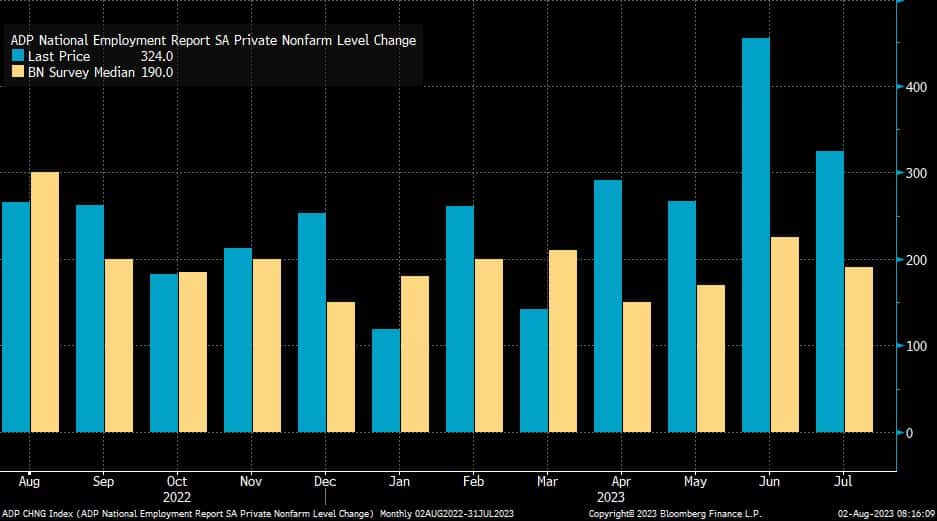

The private ADP labor report continues to point to a strong labor market. Wednesday’s ADP report shows the economy gained 324k versus forecasts of just under 200k. The Bloomberg graph below shows the ADP report handily beat expectations for the fourth straight month.

Job growth this past month came predominately from smaller companies. Companies with greater than 500 employees saw jobs decline by 67k. Conversely, companies with 49 or fewer employees reported a 237k gain in their payrolls. Leisure and hospitality continue to power the labor market, accounting for 201k of the 324k new jobs. While the data is excellent, leisure and hospitality jobs tend to be low paying and often temporary. That said, it speaks to the strong consumer demand for travel and dining services.

As we noted with the weak ISM manufacturing survey yesterday, the manufacturing sector lost jobs for the fifth straight month.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.