Heading into next week’s FOMC meeting, the Fed’s big dilemna is whether to address recent financial instability or adhere to their Fed mandates. Per the San Francisco Fed: “Congress has given the Fed two coequal goals for monetary policy: first, maximum employment; and, second, stable prices, meaning low, stable inflation.” The Fed’s mandates argue the Fed should continue to focus on inflation. The unemployment is at historic lows which some at the Fed argue is too low. Prices, on the other hand are far from low and stable. Economic activity, which significantly affects employment and prices, is robust. The Atlanta Fed estimates 3+% GDP growth for the first quarter.

Based on the Fed mandates, the Fed should remain aggressive toward fighting inflation. Jerome Powell told Congress as much a week ago. Then came Silicon Valley Bank and Credit Suisse. The Fed has a self-created third mandate, financial stability. Financial stability often trumps the Congressional mandates. Investors are pricing in a 25bps rate hike, down from 50bps a week ago. More importantly, the markets imply Fed Funds will end the year at 3.75-4.00%. Quite the decline from 5.50-5.75%! Will the Fed aggravate inflation by ignoring its Fed mandate and focus on financial instability?

What To Watch Today

Economics

Earnings

- No notable earnings reports

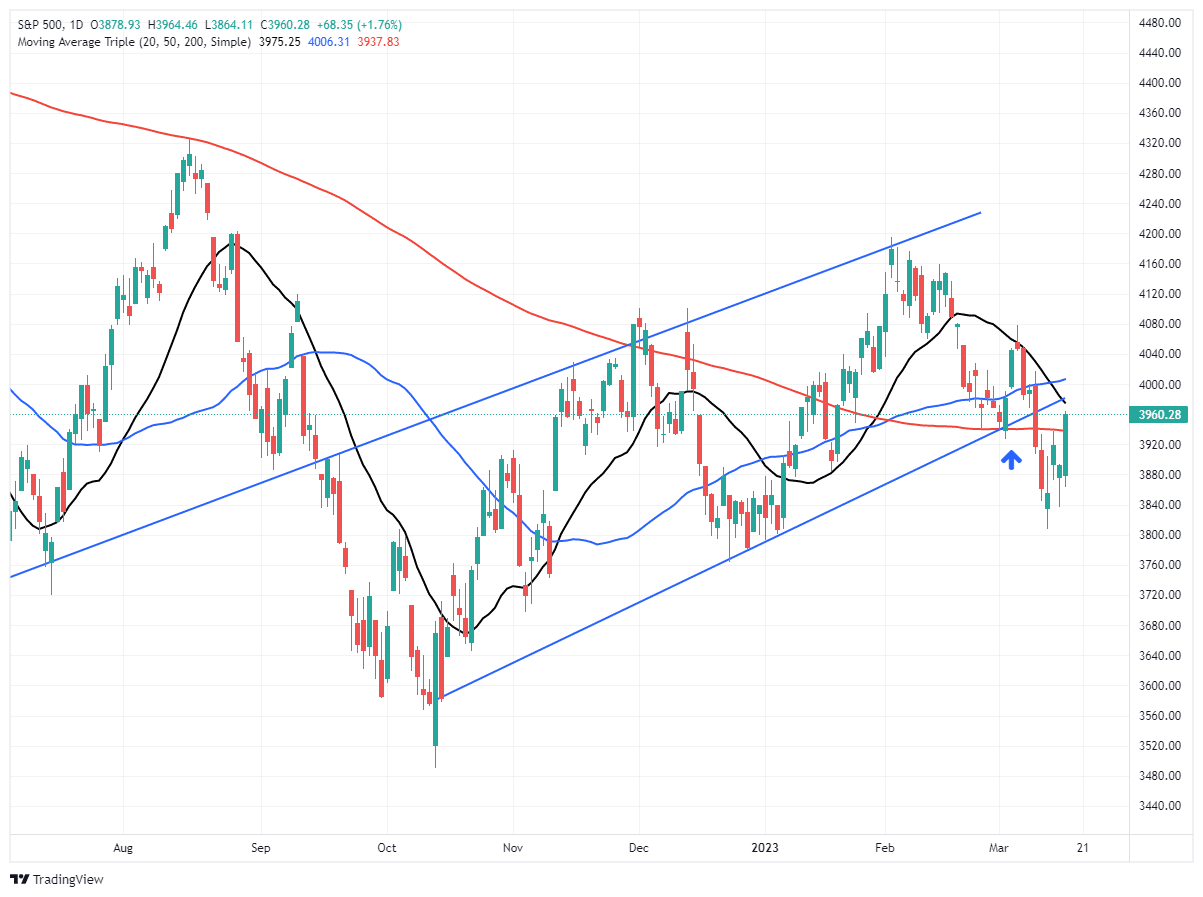

Market Regains Broken Support – Bulls Maintain Control

As I noted several times over the last few days, the broken support of the 200-DMA was important. However, a break of support needs to confirm itself by staying below that support for a trading week. Yesterday, the market rallied on news of more bank bailouts that pushed the money back into the market. The rally, led by Technology stocks, cleared the 200-DMA putting the bulls back in control of the market narrative.

However, while reclaiming the 200-DMA is important, the market now faces several more challenges ahead with the broken bullish trend line, the 20-DMA, and the 50-DMA all between current levels and 4000 on the index. Those resistance levels will likely limit the upside in the market ahead of the FOMC meeting next Wednesday.

If the market clears 4000, you can increase equity allocations accordingly. If not, we may be looking at another leg lower short term. Remain cautious for now and pick your spots to increase risk cautiously.

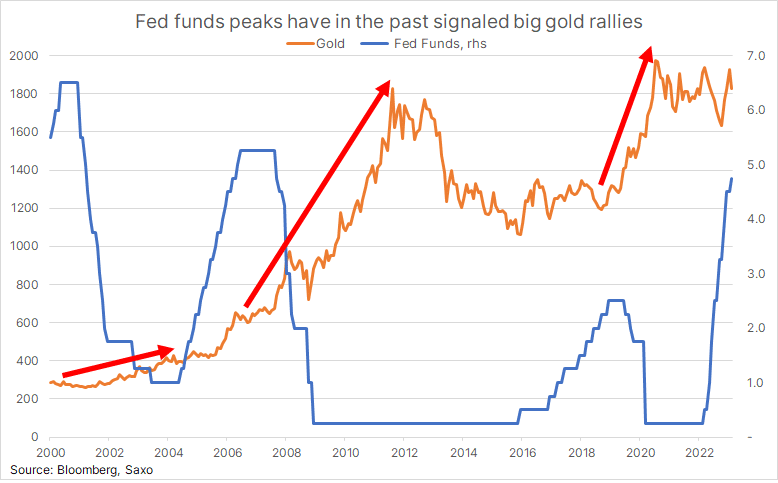

Time for Gold?

As noted in the opening, the market expects the Fed to cut rates aggressively later this year. As the market rapidly repriced Fed Fund expectations, gold rose sharply. Gold rose over $100 per ounce in just the last week. Gold is not necessarily soaring because of banking problems. The graph below from Ole Hansen of Saxo Bank shows that gold tends to have strong rallies when the Fed lowers interest rates. Gold investors are betting on an easy Fed. We also wrote about this phenomenon in Gold Investors Are Betting on the Fed. To wit:

The bottom line, gold prices are highly correlated with real yields when real yields are near or below zero. The correlation is negative, meaning that as real yields fall, gold prices rise. Said differently, gold prices increase when the Fed enacts a monetary policy that is too stimulative given the circumstances.

If the market is correct and the Fed is close to starting an easing campaign, gold may be in the early innings of a rally. However, gold can easily give up recent gains if fighting inflation remains goal number one. Longer term, the odds of a recession are high, in our opinion. Therefore a gold rally and decline in Fed Funds is likely, but it may not start yet.

Bear Stearns and the Pandemic; This Day in History

On March 16, 2020, exactly three years ago, the S&P 500 fell from 2711 to 2386, a 12% decline. While not as significant in percentage terms as 1987, it was the largest daily point decline. That happened a day after the Fed held an emergency meeting, cutting rates from 1.25% to 0%. They also enacted a massive $700 billion QE program and cut reserve requirements for banks to zero.

The market’s reaction was fearful despite the unprecedented Fed response. The market would sputter around for another week or two before a massive surge lasting the remainder of 2020 and 2021.

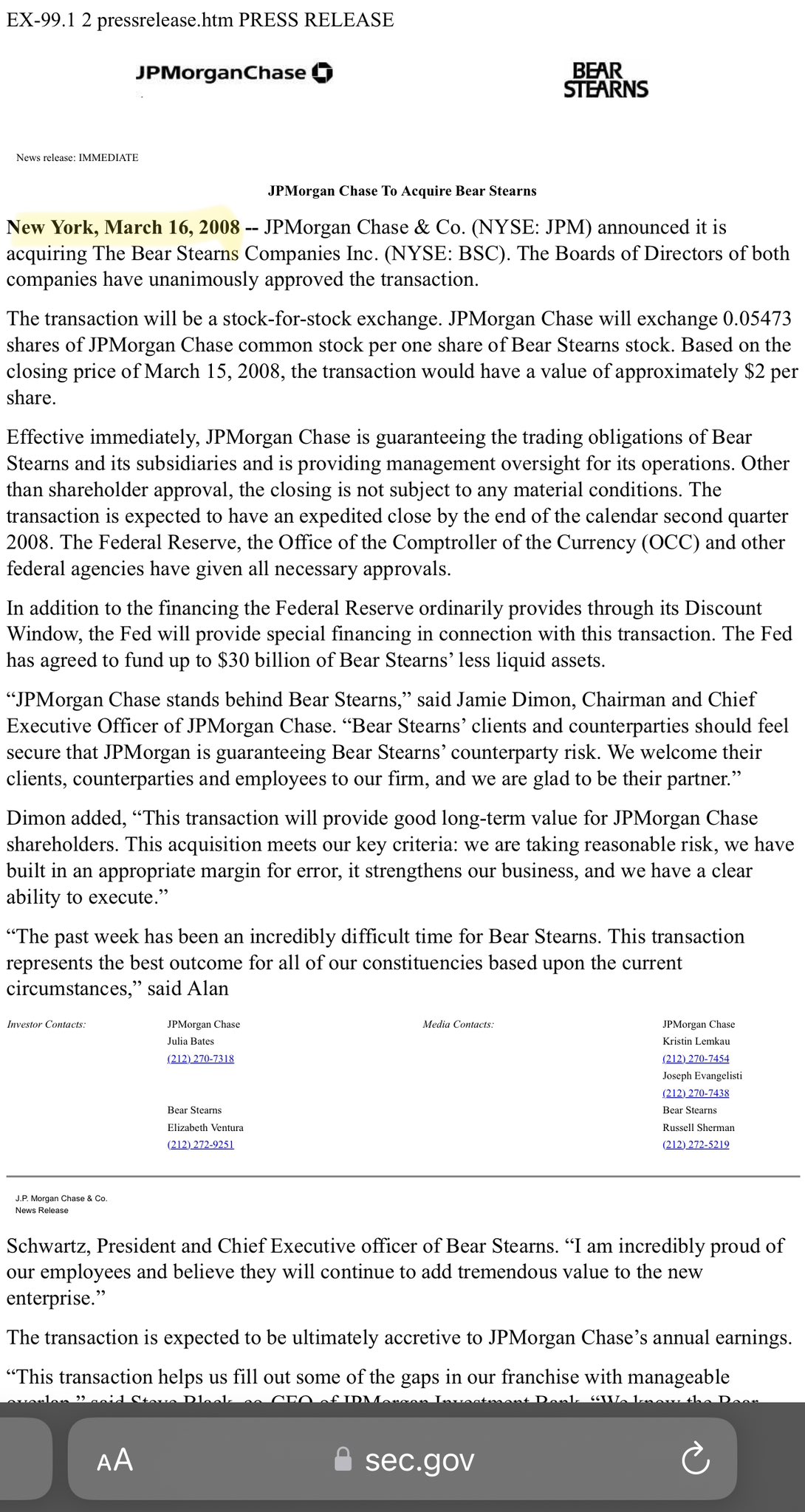

Also, on this day in 2008, JPM bought failing Bear Stearns for $2 per share. As a result of financial instability, the Fed cut rates from 3% to zero by the end of 2008. The stock market seemed to ignore the failure of a Wall Street powerhouse and instead focus on the bailout and Fed reaction. The S&P 500 would rally over 15% in the next two months, only to be cut in half in the next ten months.

We remind you of both events, not because they occurred on this day, but because they show the initial market reaction to Fed action can be wrong. Prudence is advised.

New York and Philadelphia Point to a Recession

The New York Empire and Philadelphia Manufacturing Surveys were much weaker than expected. These regional surveys of business leaders tend to be good leading economic indicators.

The Empire index fell to -24.6 versus expectations of -7.7. There are two subcomponents in the report worth discussing. Per the Empire report:

The new orders index fell fourteen points to -21.7, indicating that orders declined substantially, and the shipments index fell fourteen points to -13.4, pointing to a decline in shipments.

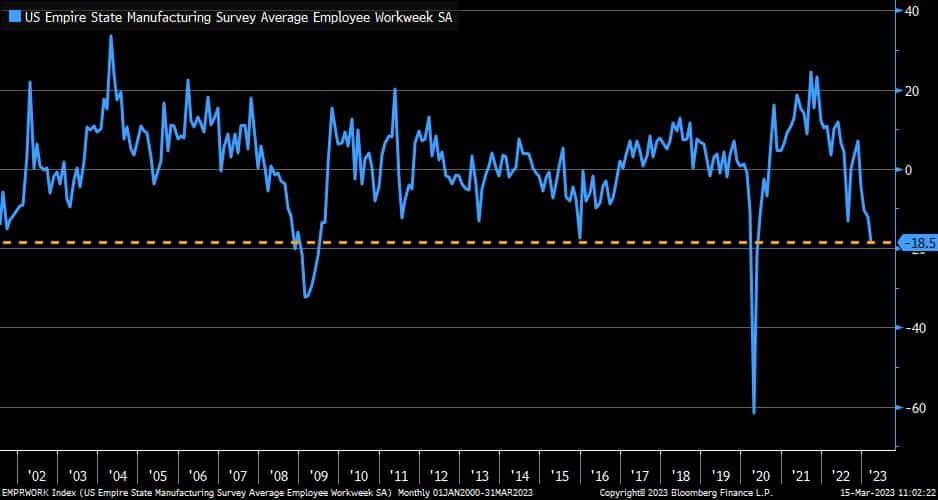

New Orders are one of the best leading economic indicators. Currently, the broad ISM New Orders index is at levels on par with prior recessions. The Empire survey confirms that warning. The second concerning signal is in the chart below. While unemployment sits near 50-year lows and initial jobless claims are equally strong, the average employee workweek is declining. Often, companies will cut back on hours before firing employees. This may indicate that the labor market is about to weaken.

The Philadelphia Fed was also weaker than expected at -23.2 vs. -15.5. Prices paid and received are still above zero, but the percentage responding that they see higher prices are falling quickly. Like the Empire report, new orders fell sharply, from -13.6 to -28.2. The number of employees and average workweek declined into negative territory.

The problem with both surveys is they do not reflect the recent banking crisis. Recent events will likely make them more negative on their immediate economic prospects.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.