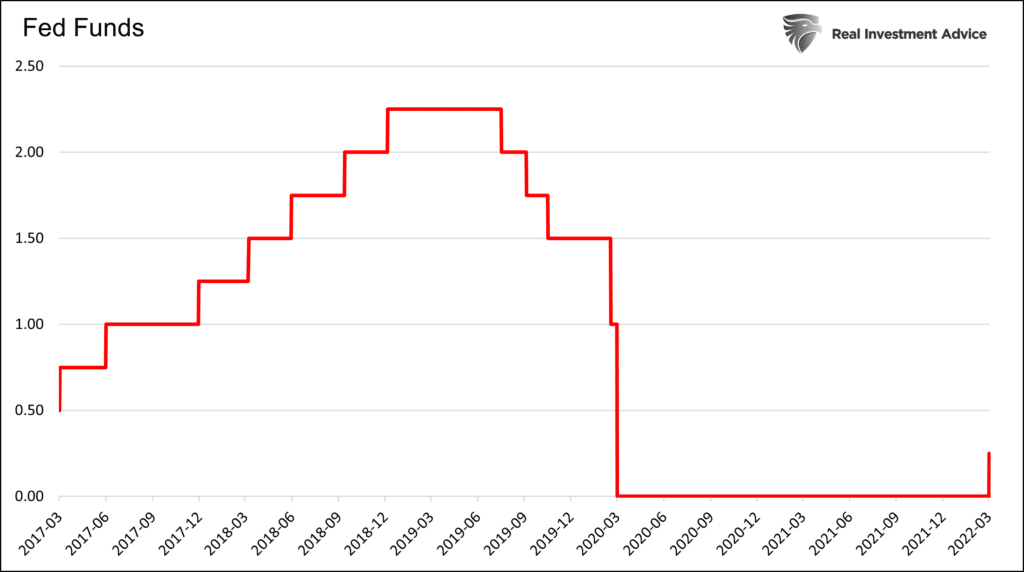

On March 3, 2020, the Federal Reserve reduced its Fed Funds rate and bought Treasury and mortgage assets as the Pandemic rattled the economy and markets. Nearly two years later, after a tremendous amount of monetary and fiscal stimulus and outsized economic growth and inflation, the Fed reverses its policies. To that end, the Fed raised rates by 25bps on Wednesday. While it may seem bearish, consider that since World War II, the Fed has embarked on 17 rate hike cycles. Six months following the initial rate hike, the S&P 500 on average was up by 1.3%.

[dmc]

What To Watch Today

Economy

- 8:30 a.m. ET: Housing starts, February (1.700 million expected, 1.638 million in January)

- 8:30 a.m. ET: Building permits, February (1.850 million expected, 1.899 million in January, downwardly revised to 1.895 million)

- 8:30 a.m. ET: Housing starts, month-over-month, February (3.8% expected, -4.1% in January)

- 8:30 a.m. ET: Building permits, month-over-month, February (-2.4% expected, 0.7% in January, downwardly revised to 0.5%)

- 8:30 a.m. ET: Philadelphia Fed Business Outlook Index, March (15.0 expected, 16.0 in February)

- 8:30 a.m. ET: Initial jobless claims, week ended March 12 (220,000 expected, 227,000 during prior week)

- 8:30 a.m. ET: Continuing claims, week ended March 5 (1.480 million expected, 1.494 during prior week)

- 9:15 a.m. ET: Industrial Production, month-over-month, February (0.5% expected, 1.5% during prior month)

- 9:15 a.m. ET: Capacity Utilization, February (77.9% expected, 77.6% during prior month)

- 9:15 a.m. ET: Manufacturing (SIC) Production, February (1.0% expected, 0.2% during prior month)

Earnings

Pre-market

- Warby Parker (WRBY) to report an adjusted loss of $0.09 on revenue of $134.29 million

- Dollar General (DG) to report adjusted earnings of $2.55 on revenue of $8.70 billion

Post-market

- FedEx (FDX) to report adjusted earnings of $4.65 on revenue of $23.49 billion

- GameStop (GME) to report adjusted earnings of $0.84 on revenue of $2.23 billion

Fed Hikes “Fed Funds” And Stocks Surge

As we have noted over the last couple of weeks, there was a lot of “fuel” for a rally, all that was needed was a bit of an excuse. That excuse came Wednesday afternoon as the Fed did “NOT” surprise the markets and only hiked Fed funds by 0.25%. Such was well telegraphed and in line with expectations. The presser following the announcement was equally “dovish” by delaying any announcement of “tapering” the existing balance sheet.

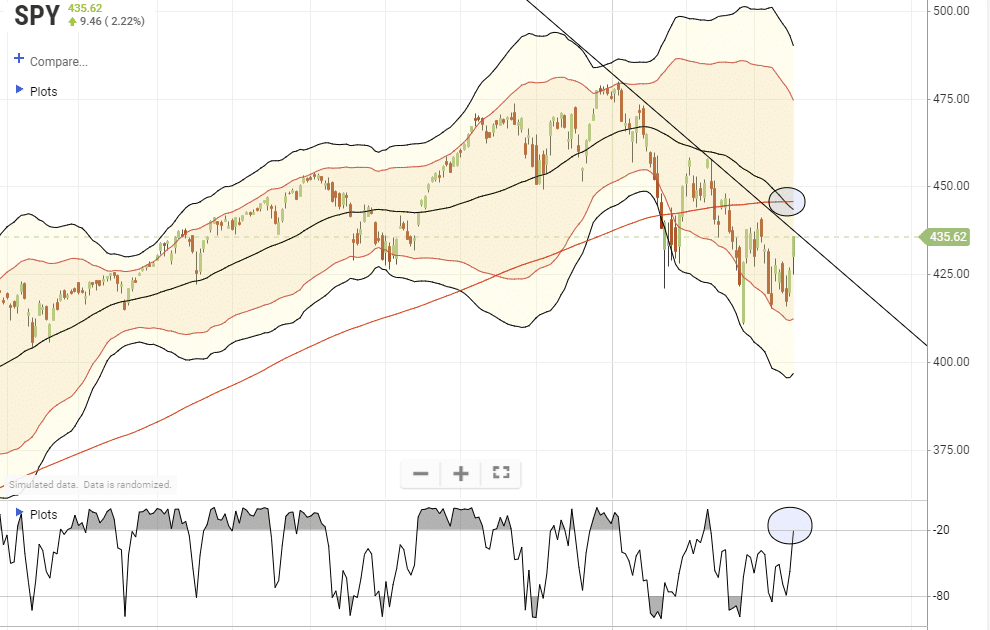

The rally was broad buy heavily concentrated in the “most shorted” names, namely technology stocks which we increased our weighting to on Tuesday morning. We had also reduced our “inflation names” on Monday as the coming reversion in oil prices was quite evident.

The rally in stocks face one more challenge on Friday with options expiration, but the market is not overbought short-term. The market is now challenging the downtrend line, a break above that level could see a retracement back to the 50-dma. We will likely look to rebalance risk at that point.

Jerome Powell and the Fed

The Fed voted 8-1 for a 25bps rate hike. St. Louis Fed President Bullard dissented in favor of a 50bps rate increase. Based on the Fed’s new projections, they expect 2.0% Fed Funds by the end of the year and 2.8% by the end of 2023. They expect inflation at 4.3% by the end of the year, up from their January projection of 2.5%. The following quote from the statement alludes to more inflation due to the Russian invasion. “The invasion of Ukraine by Russia is causing tremendous human & economic hardship. The implications for the U.S. economy are uncertain, but in the near term, the invasion & related events are likely to create additional upward pressure on inflation & weigh on economic activity” The statement may explain the increase in inflation and Fed Funds expectations.

The Fed is not reducing their balance sheet now, but “expects to begin reducing holdings of Treasury securities and agency mortgage-backed securities at a coming meeting.”

Retail Sales

Despite poor consumer sentiment, Retail Sales were positive for February. More encouraging was the +1.1% revision to January’s number (3.8% to 4.9%). There is a caveat, however. Retail Sales rose by just 0.3% for the month. But, CPI rose 0.8%, meaning that if we subtract inflation, retail sales fell by about 0.5%. Not surprisingly, retail sales excluding vehicles and gas were down 0.4%. The control group used to calculate GDP, fell by 1.2% but after its 6.7% increase last month. More details on the report can be found in Mish Shedlock’s latest report.

“Finally, and suggesting that these numbers are all bunk, the unadjusted retail sales continued to slide, and after a record gap in January between the two series, in February the gap got even bigger, suggesting that the only “growth” in US spending is due to some Commerce Department seasonal adjustment calculator.” – Zerohedge

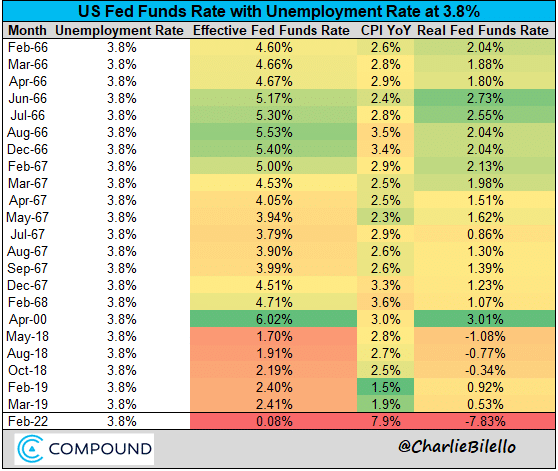

This Time Is Very Different

The table below from Charlie Bilello (@charliebilello) shows how unique the current economic/monetary policy situation is. The table shows every month in which the unemployment was at the current 3.8%, which is generally considered full employment. It then compares those historical instances to the Fed Funds rate and inflation. The real Fed Funds (Fed Funds less CPI) column provides context to how much more monetary stimulus is being applied today than at any other time unemployment was this low. Considering the Fed’s two congressionally chartered objectives are maximum employment and stable prices, it is shocking how far behind the eight ball they are in fighting inflation thus far.

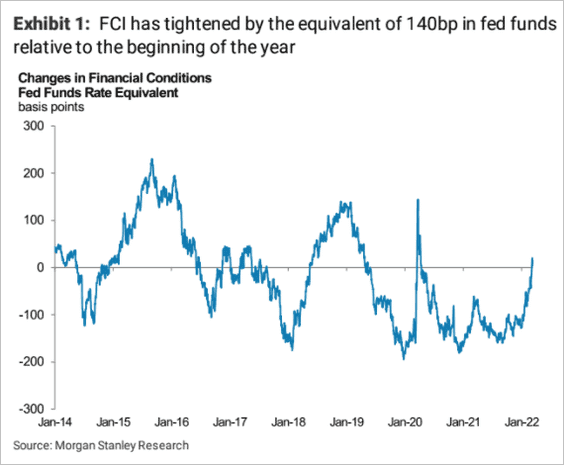

Is The Fed Behind The Eight Ball?

The following graph runs counter to the last table and paragraph. The graph below charts Morgan Stanley’s Financial Conditions Index. It uses recent changes in stock prices, short and long-term interest rates, and the dollar to assess their impact on financial conditions. As shown, the index is now at an average level for the last eight years. According to Morgan Stanley, all three factors have contributed to the equivalent of a 140bps Fed Funds rate increase. To better understand, consider that mortgage rates, a significant driver of economic activity has risen by over 1% since last August.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.