The FOMC will announce its Fed Fund’s rate policy decision this Wednesday. Given the recent events in the banking sector, we return to the question posed Friday in Fed Mandates or Financial Stability: Will the Fed aggravate inflation by ignoring its Fed mandate and focusing on financial instability? The ECB’s rate decision last Thursday provides insight into what we can expect the Fed to do later this week.

Christine Lagarde announced a 50bps rate hike while reiterating the ECB’s focus on taming inflation. However, she also noted that the central bank closely monitors conditions and will step in with liquidity if necessary.

“The Governing Council is monitoring current market tensions closely and stands ready to respond as necessary to preserve price stability and financial stability in the euro area.”

Lagarde implied that the ECB doesn’t have to ditch its commitment to bring down inflation in favor of maintaining financial stability. It can focus on both simultaneously. Given the congressional mandate in the US, we expect the Fed to adopt a similar tone on Wednesday.

It certainly appears that financial cracks are showing as over the weekend, ailing 167-year-old Credit Suisse will now see itself into a forced marriage with stronger rival UBS. Furthermore, the Federal Reserve announced “coordinated” daily US Dollar swap lines to provide bank liquidity to ease financial stress with other banks.

Of course, this is just the first step that Federal Reserve takes in reversing monetary tightening. Historically, once the Fed takes this action, the next steps are rate cuts, QE, and other monetary supports. While the bulls may think the monetary policy reversal will be bullish for equities, history suggests the initial pivot will not be.

What To Watch Today

Economy

- There are no notable releases today

Earnings

- There are no notable releases today

Market Trading Update

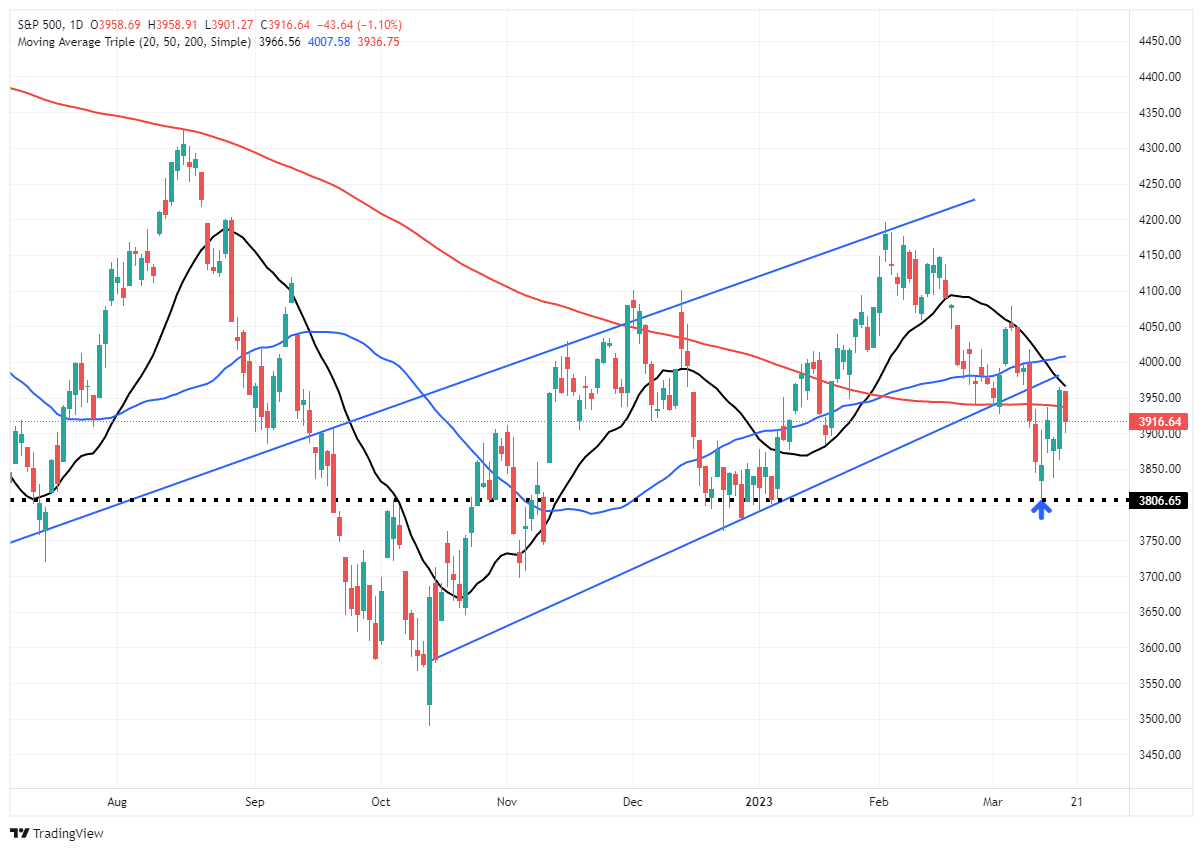

The market took out the support at the rising trend line and the 200-DMA, which violated our stop-loss levels, where we reduced exposure to equities. With all of the previous bullish support levels broken, the next logical level of support is the December lows. A failure there will then set supports at the June and October lows.

The failed retest of the 200-DMA to close the week is not a good look. However, with markets fairly oversold, a rally attempt early next week before the Fed meeting won’t be a surprise. Hopes of a “pivot” due to financial stress could contribute to some buying pressure. However, any rally will be limited due to the 20- and 50-DMA just above Thursday’s rally peak.

One important point I discussed in Before The Bell is the importance of perspective.

Take A Step Back

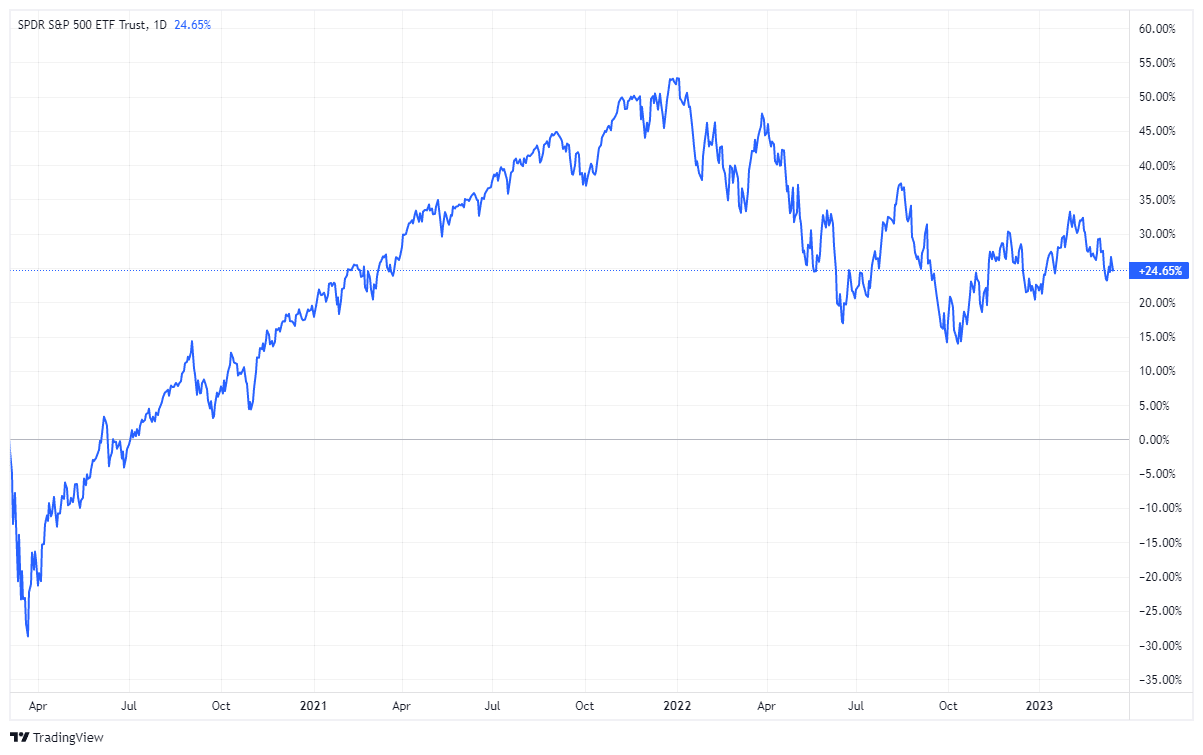

While there are many headlines of “doom, gloom, and disaster,” a step back from the noise reveals a much different picture. As investors, one of the mistakes we make is viewing our portfolios on a year-to-date basis.

Wall Street designed this terrible practice to keep you upset so you will move money around the markets. Money in motion creates fees for Wall Street and generally losses for you.

Yes, the market has been challenging over the last 15 months. However, for most, we have been invested in the markets for longer. Therefore, step back and look at your portfolio over the last 3- or 4-years. Once you do that, a much different picture emerges, as shown. For example, if we look at the period from the March 2020 peak to the present, we find our portfolios are still higher by 24%. That roughly equates to an 8% annualized return which is exactly what would expect from the market.

With 24/7 media looking for anything to make a headline out of, not to mention a bunch of commentators looking for clicks and views, try and focus on what matters to your investment goals.

Removing some of the emotions from our investment strategies can help us reach our long-term goals.

The Week Ahead

This week will be relatively quiet except for the Fed meeting on Wednesday and the durable goods order on Friday. We expect the Fed to increase the Fed Funds rate by 25bps at 2 pm ET on Wednesday. Jerome Powell will likely maintain his stance on bringing down inflation during the FOMC press conference at 2:30. However, we expect him to stress that the Fed aims to maintain flexibility and will be there to provide liquidity should financial instability arise.

We will receive data for February Durable Goods Orders and the S&P Global PMI Flash for March on Friday. While Durable Goods Orders data are received on a lag, the Flash PMI survey should provide better insight into how broad manufacturing activity is evolving.

Consumer Sentiment Takes a Breather

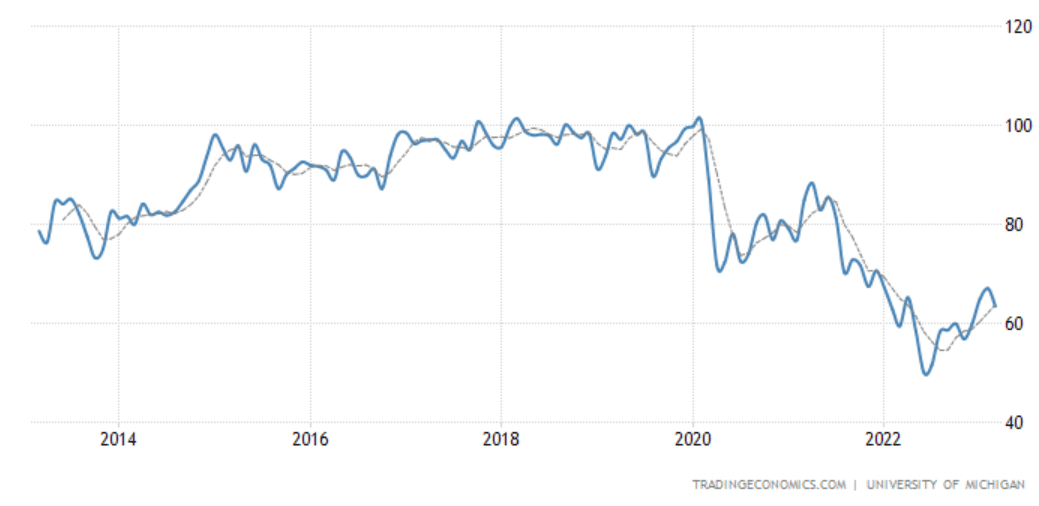

On Friday, the University of Michigan’s Consumer Sentiment indicator dipped lower for the first time in four months to 63.4 in March from 67 in February. Notably, according to the survey director, about 85% of the surveys had been conducted before the SVB failure. Thus, recent volatility in the banking sector was not a significant factor in the results. The current conditions and consumer expectations components fell, and year-ahead inflation expectations declined to 3.8% in March from 4.1% in February.

Squashing Misconceptions

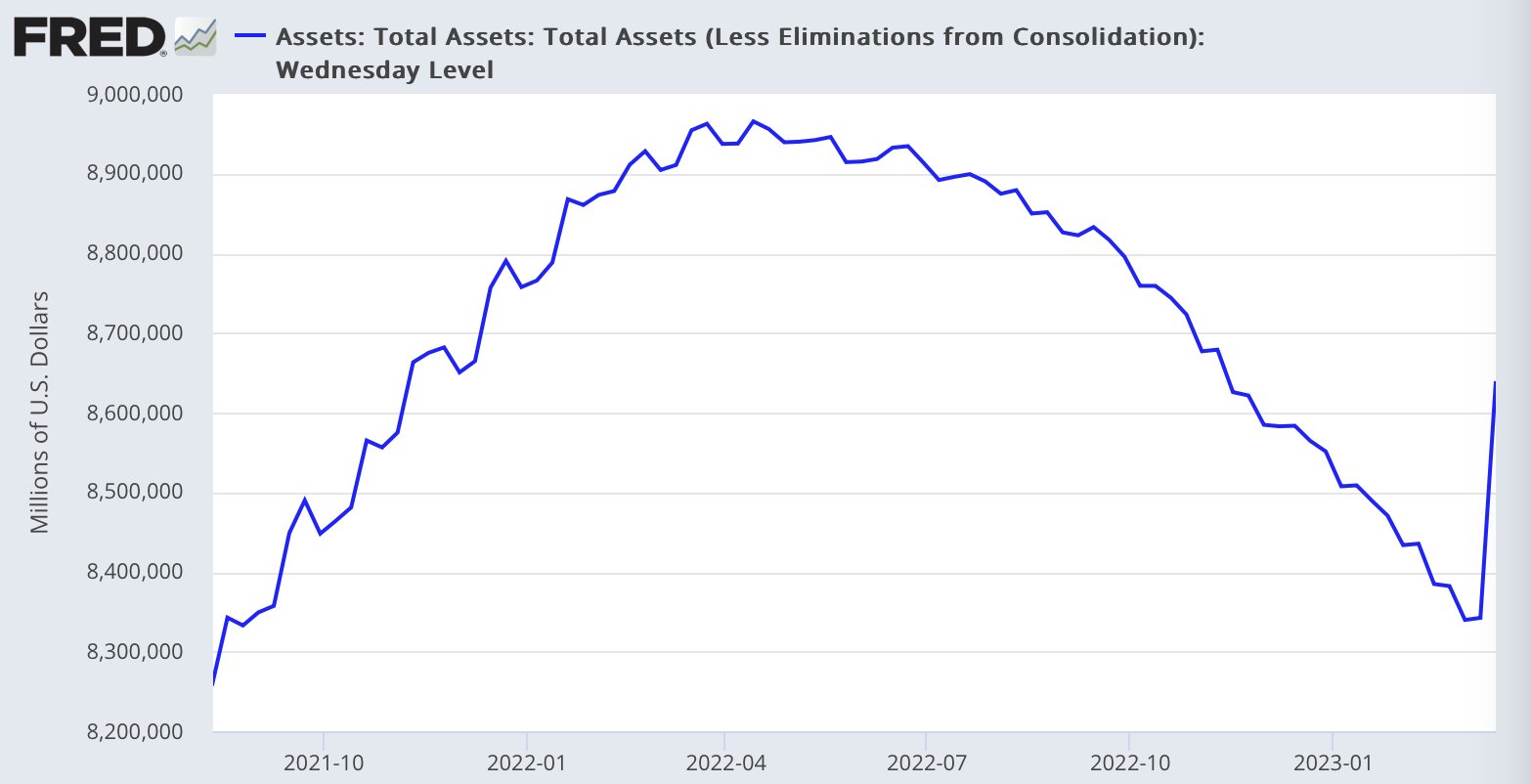

The following chart made its rounds over the weekend. Some financial pundits claim this signals the end of QT, and QE has returned. This is not the case, however. The Fed’s balance sheet increased last week due to financial institutions borrowing from its Discount Window lending facility to meet withdrawals. Ayesha Tariq wrote a nice explainer:

“There are perhaps misconceptions surrounding the issue of the banks borrowing at the Discount Window but, the most important thing to remember is that no new money is being created. Hence, this is not QE, this is not bullish and this is just a temporary fix.

Since, no new money is being created this is actually not going to be inflationary either. This is just depositors getting their money back in a timely manner.

If anything, this gives the Fed the stability and ability to keep tightening without causing a full-blown banking crisis. But, even this is temporary.”

No new money is created because these are loans under the Discount Window facility, which are collateralized by the banks’ eligible assets. The Fed is not purchasing the collateral. Once the loans are repaid, the collateral gets returned to the banks, and the Fed’s balance sheet will shrink again. This is just a way for banks needing liquidity to meet withdrawals without creating a fire sale in the financial markets- not a return to QE. Treasuries and MBS continue rolling off the Fed’s balance sheet for now.

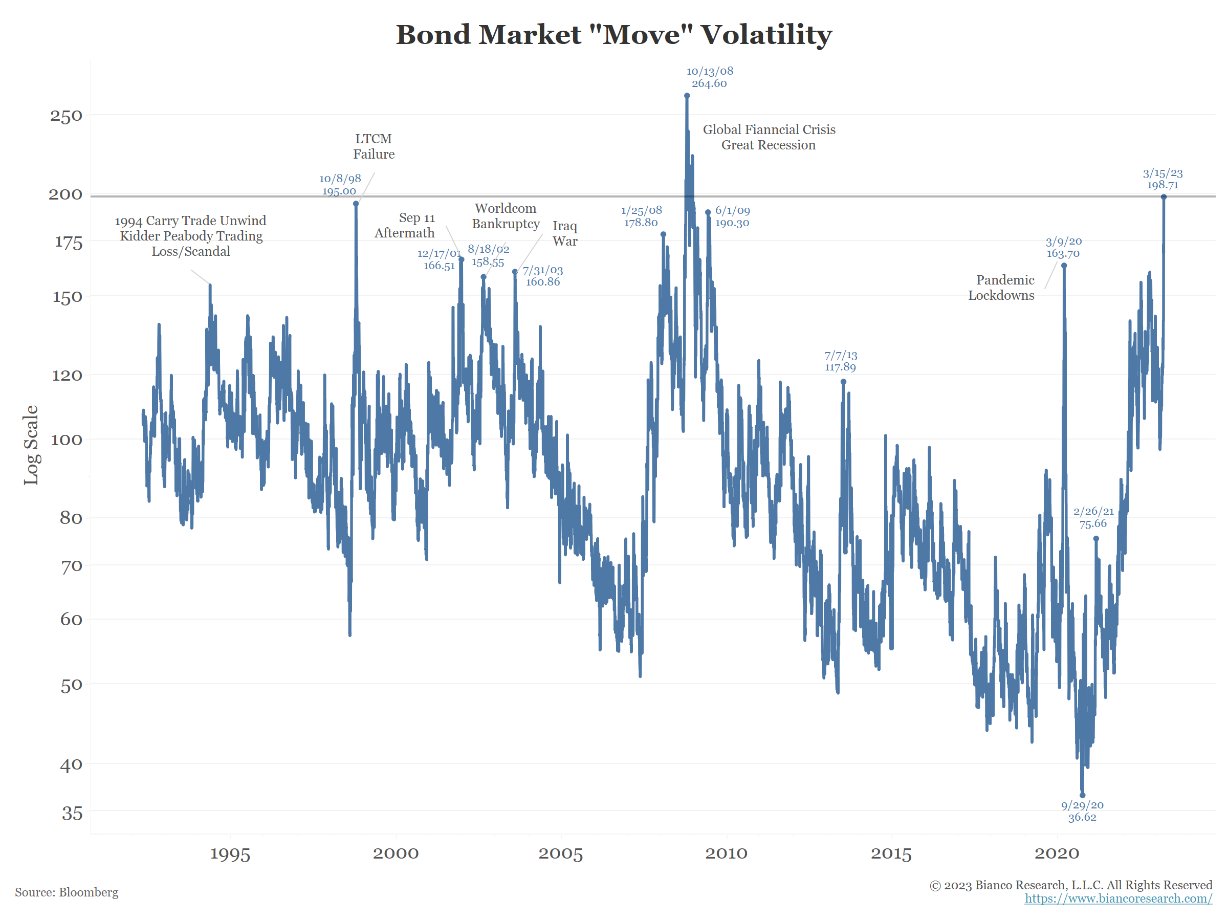

Is the MOVE Index Flashing a Warning Signal?

The MOVE index measures the month-ahead implied volatility in Treasury yield volatility. It’s akin to a VIX for the fixed-income market, which has been surging recently. The chart below, courtesy of Jim Bianco, shows the MOVE index approaching levels last seen during the financial crisis. Essentially, the fixed-income market is pricing increasing uncertainty as short-term yields have begun plunging. The surge in the MOVE index alongside a rising VIX could signal that trouble lies ahead.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.