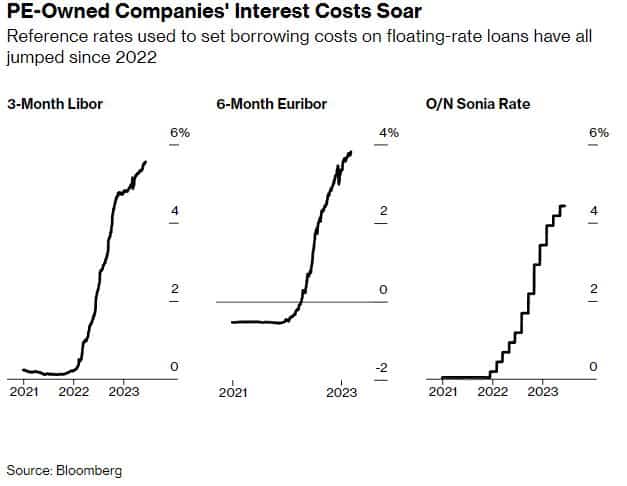

Private Equity (PE) firms are known for their use of leveraged buyouts in acquiring targets. In a leveraged buyout, the acquiring firm issues a large amount of debt to acquire the publicly traded equity of the target. The acquiring firm then places that debt on the target’s books. These transactions boomed during the cheap-money era of the last decade, with many taking on floating rate loans. Using high leverage amplifies the return realized by PE firms when things go to plan. However, following the Fed’s rate hikes, many are now facing the consequences of a bet on profits over protection.

According to Bloomberg, many buyout firms considered hedging “a waste of time and money” before the Fed began cranking rates to their current level. The article continues, “But in the US, nearly three-quarters of the floating-rate debt taken out during the leveraged-buyout boom lacked hedges as recently as August, according to an analysis by Bank of America.” As shown below, reference rates used to set the interest payments have surged since the Fed began fighting inflation. This combination is wreaking havoc on profits of private equity backed companies and carries the potential to push many into default if rates stay elevated for much longer.

Across North America, interest costs at the median private equity-backed company ballooned to 43% of Ebitda last year, according to research published last month by Verdad Advisers, which analyzed 350 such companies that are either publicly traded or have publicly traded debt. Not only is that six times as much as the median S&P 500 company, but the interest burden will keep growing this year as rates keep rising.

What To Watch Today

Earnings

Economy

Market Trading Update

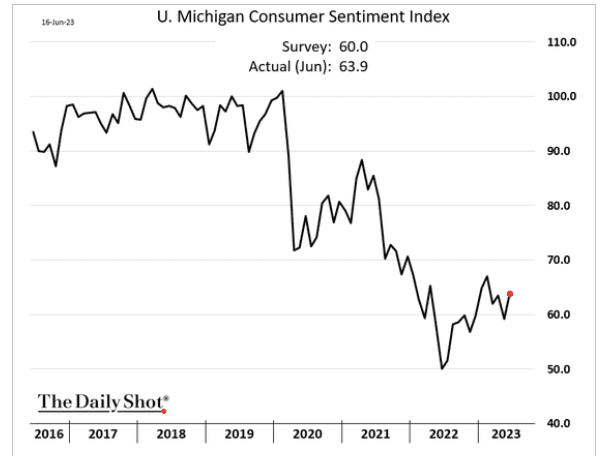

Consumer confidence has improved over the last few months as the market rallied. In 2010, then Fed Chairman Ben Bernanke introduced a “third mandate” to the Fed’s responsibilities – creating the “wealth effect.”

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose, and long-term interest rates fell when investors began to anticipate this additional action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.”

– Ben Bernanke, Washington Post Op-Ed, November, 2010.

As noted, consumer confidence bottomed with the market in October last year. The problem is that higher asset prices and rising consumer confidence will support stronger economic growth. I say it’s a problem because this is the opposite of what the Fed is trying to achieve in its inflation fight. If economic growth reaccelerates, such will keep prices more “sticky” at elevated levels causing the Fed to potentially hike rates further to its goals.

For now, the markets remain oblivious to stronger markets’ impact on monetary policy. What is clear is that markets continue to respond to increased liquidity as the Fed supports regional banks.

Housing Starts Exploded in May

US housing starts surged 21.7% to an annualized rate of 1.63 million in May, smashing expectations of 1.4 million. This increase was the largest since 2016 and represents the fastest pace of growth in over a year. Building permits also increased to an annualized rate of 1.49 million, climbing 5.2% in MoM.

Despite weak affordability, homebuilders are placing a bet on limited supply of existing homes to drive profits as consumers adjust to higher mortgage rates. Starts and building permits point to a residential construction market that’s on track to help fuel economic growth this year. The last time homebuilding positively contributed to GDP growth was in the 1st quarter of 2021.

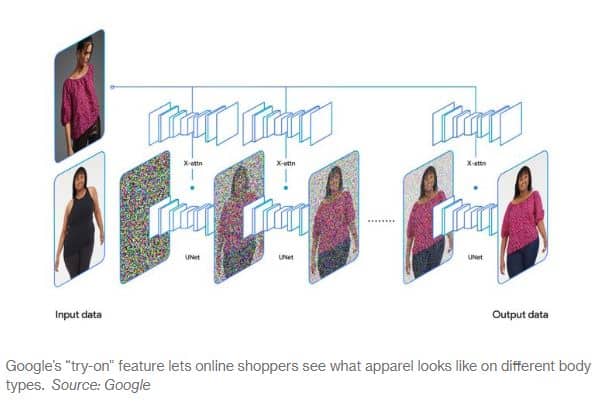

Google is Bringing AI to Your Shopping Experience

Despite its position as the world’s dominant search engine, nearly half of US shoppers surveyed by CivicScience said they started their online shopping endeavors on Amazon last year. Google plans on making further inroads into that market by being the first to incorporate image-based generative AI into its shopping experience. Per Bloomberg,

A new virtual “try-on” feature, launching on Wednesday, will let people see how clothes fit across a range of body types, from XXS to 4XL sizes. Apparel will be overlaid on top of images of diverse models that the company photographed while developing the capability.

The internally developed AI model will generate lifelike images by considering how the fabric stretches and wrinkles on a body. Google’s bet on capturing a greater share of online shopping is another avenue for the company to bolster its primary source of profits, advertising revenue.

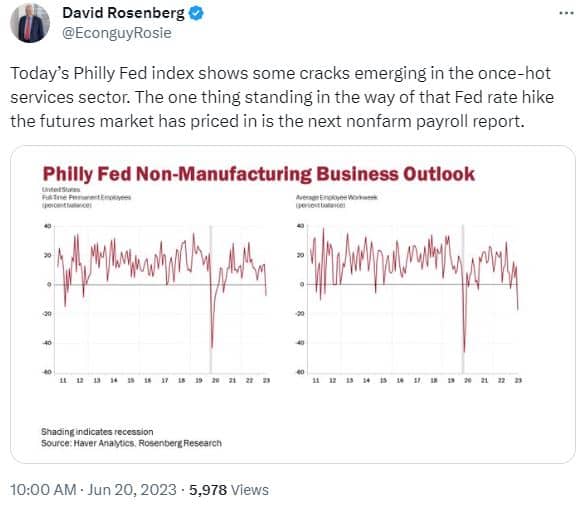

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.