Shares of Credit Suisse and other large European banks traded sharply lower yesterday. This occurs only a few days after European leaders expressed little concern that U.S. banking problems would spread across the Atlantic. Credit Suisse Bank, down nearly 25% yesterday, appears to be the culprit. Credit Suisse, a foreign bank domiciled in Switzerland, has been on the ropes for a while. The graph below shows Credit Suisse has been in perpetual decline since 2008. Making matters for the bank worse yesterday, their largest investor, the Saudi National Bank, said they would not provide any more capital.

As noted in recent commentaries and articles, banking is based on a fractional reserve system. Consequently, there are more bank deposits than cash in the system. Such a system works well, but any bank, no matter how well capitalized, is mortally susceptible to a rapid drain of deposits. Fears of bankruptcy, capital raising, increased bond yields, and a sinking stock are triggers that set off depositors. As we saw with SVB and Signature bank, a surge in withdrawals can make a bad situation much worse. The following large European banks are following Credit Suisse bank lower: BNP Paribas, Deutsche Bank, UBS, Societe General, and Banco Santander, to name a few.

What To Watch Today

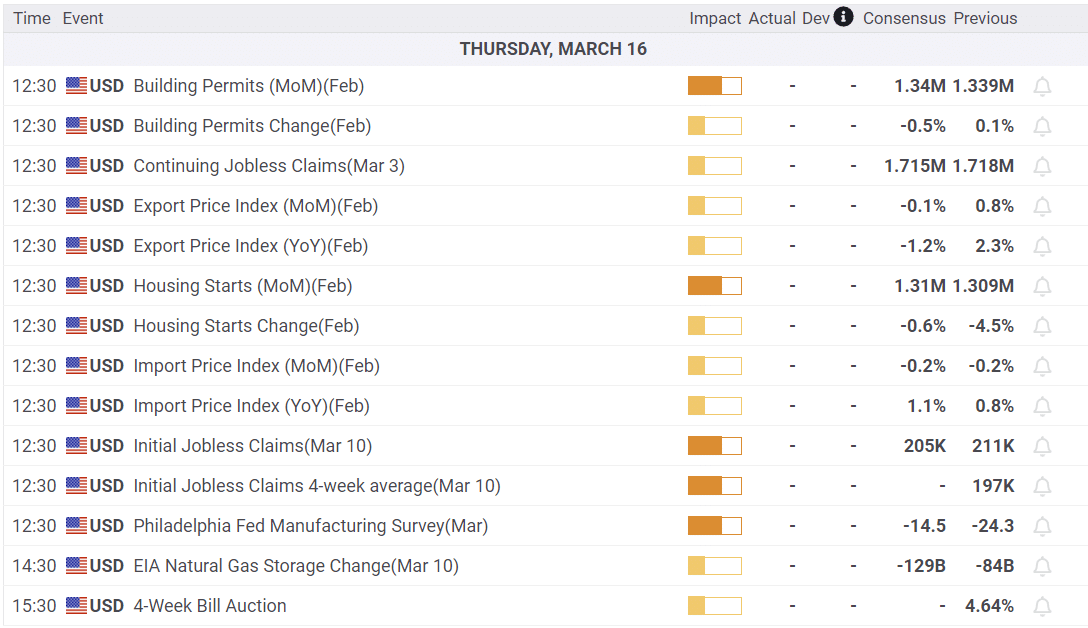

Economy

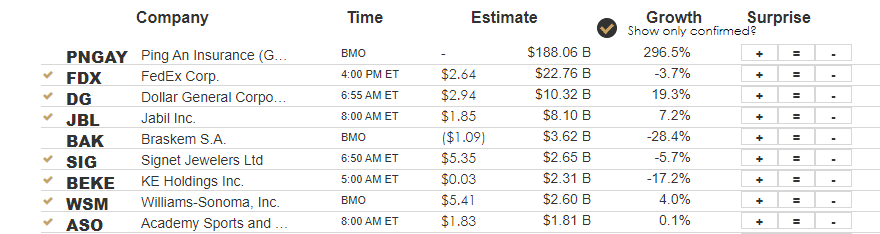

Earnings

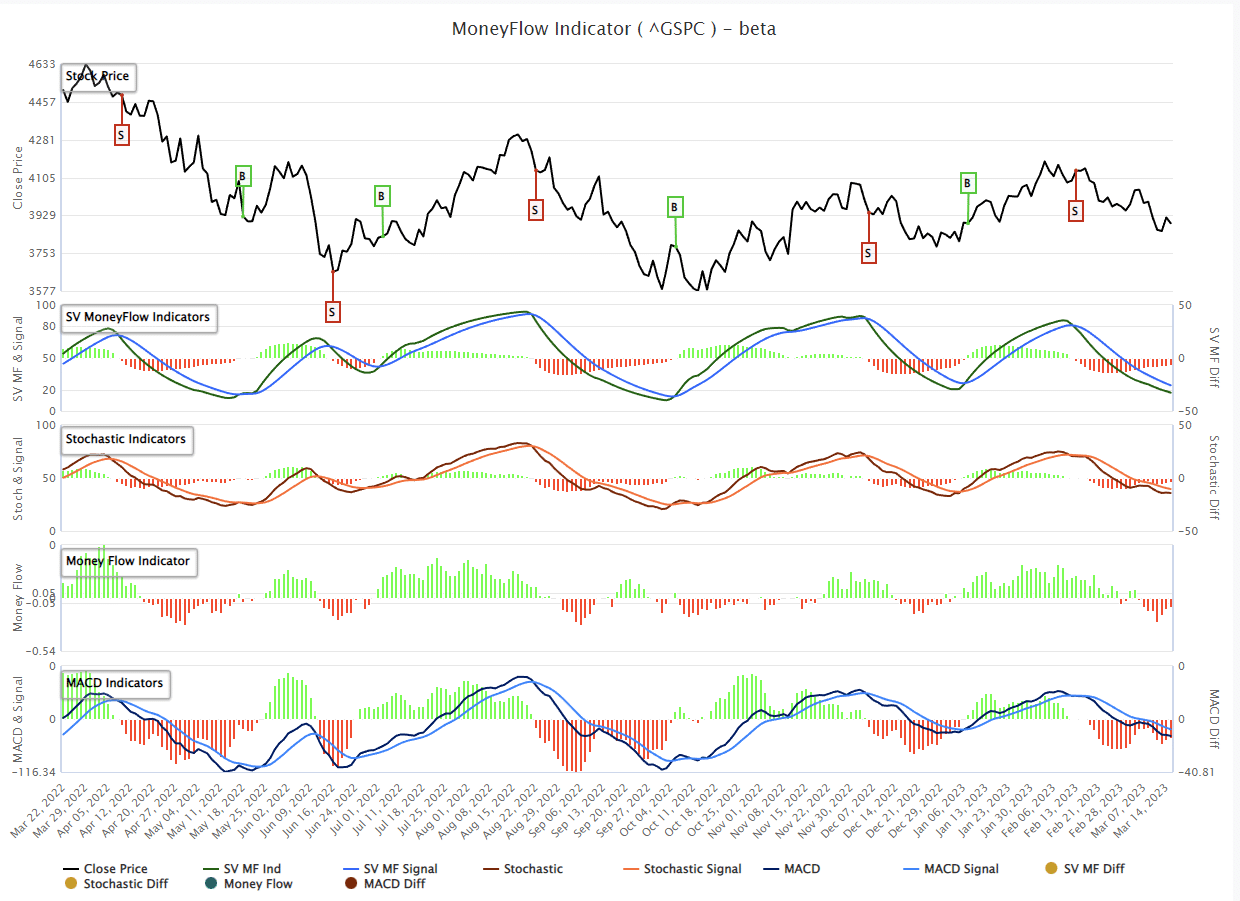

Market Trading Update

The market sold off again on Wednesday as Credit Suisse hit the headlines. However, by mid-afternoon, a plan emerged to save the troubled bank that is systemically important to the entire financial food chain. While the market cut its losses in half by the close, the failed test of the previous 200-DMA is now concerning. The market is oversold enough for a rally, so stocks could get a bid if we can get a day without a bank crisis unfolding.

With that said, we continue to suggest using rallies to reduce risk and rebalance portfolios for now. We raised cash further in portfolios yesterday and will likely add more to our bond holdings on any bond price pullback. Until the bulls regain control of the narrative, the risk remains elevated.

PPI and Retail Sales

PPI provided welcome news on the inflation front. The monthly change fell by 0.1% versus expectations for a 0.3% increase. Further, the prior month was revised from +0.7% to +0.3%. While the Fed will undoubtedly like the data, they continue to hang onto prices in the service sector, excluding housing, as their primary inflation gauge. As we share below from Charlie Bilello, PPI continues progressing toward more normal levels.

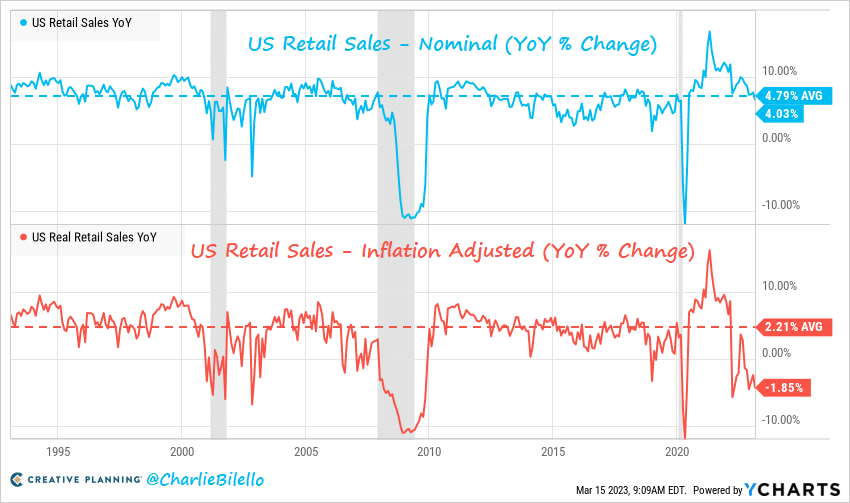

Retail Sales fell by 0.4% but keep in mind that last month they rose a shocking 3.2%. Excluding vehicles and gas, both volatile sectors, sales were flat. The consensus was for a 0.9% decline. The graph below from Charlie Bilello shows that nominal annual retail sales growth is 4.03%, below the historical average of 4.79%. Further, inflation-adjusted retail sales remain almost 4% below the average.

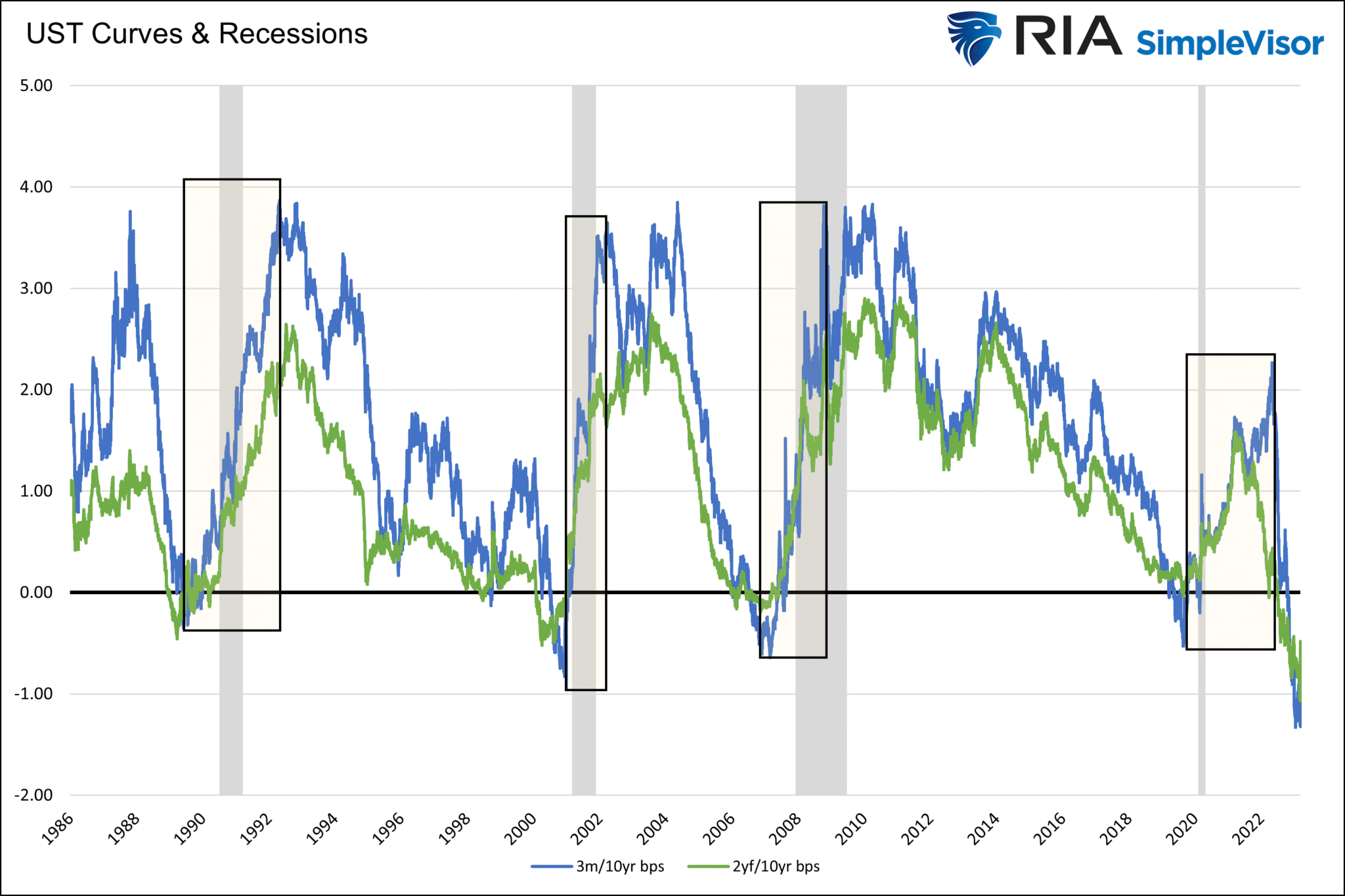

Yield Curve Recession Warnings are Strengthening

The graph below shows that yield curve inversions are an excellent leading recession warning. However, recessions do not start until yield curves un-invert. Before the SVB banking crisis, yield curves were inverting to 40-year lows. The U.S. banking crisis, spreading to Credit Suisse Bank and other large European banks, rapidly steepened the 2yr/10yr yield curve. While hard to see below, the 2yr/10-year yield curve has un-inverted by over 40bps in the last week. Despite two-year yields falling rapidly, 3-month yields remain steady. The market is pricing in aggressive Fed easing later this year but not in the next few months. The 2/10yr curve will often steepen before the 3m/10yr curve.

The recession warning is growing louder, but until the very short maturity yields start falling, it’s too early to have 100% confidence a recession is imminent.

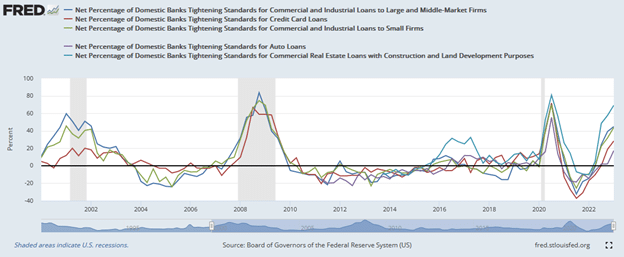

The Aftershock- Tighter Lending Standards

ZeroHedge shared the following quote from UBS:

After such a long period of catastrophically negative real wages, US consumers have used credit card borrowing to maintain living standards. Higher interest rates do little to deter this borrowing. Tighter lending standards stop it abruptly.

Our latest article Aftershock discusses how the SVB crisis will cause a significant tightening of bank lending standards. In the article, we share the graph below and write the following:

Financial lending standards quantify how easy or hard it is to attain a loan. The Federal Reserve graph below shows that the number of banks tightening lending standards for various loan types is increasing. The percentage of banks with tighter standards is on par with typical recession periods. The data for the graph was taken before the Silicon Valley Bank was on anyone’s radar. We suspect the percentages will proliferate as the aftershocks of the crisis are felt.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.