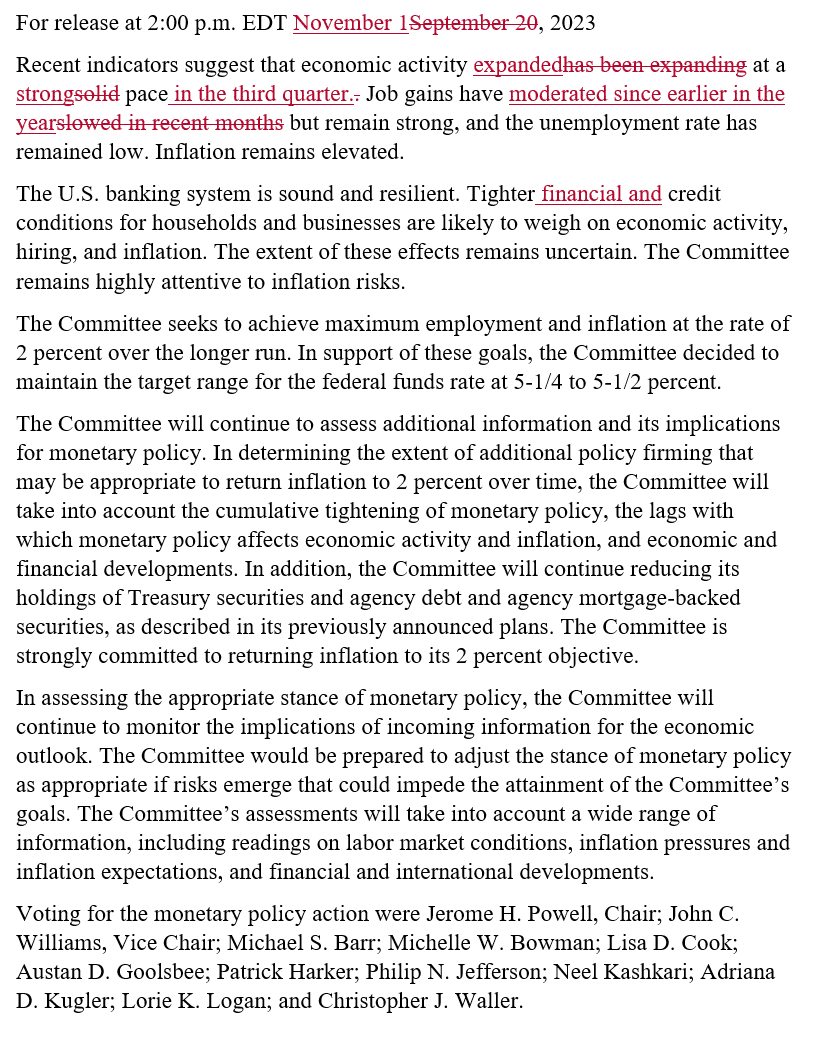

In the November FOMC statement, Chairman Powell and his colleagues at the Fed did as the market expected. Not surprisingly, in a unanimous decision, they left the Fed Funds rate at 5.25-5.50% and made minimal changes to the statement from the prior meeting, as shown below. The Fed continues to threaten another rate hike but, with the addition of the word “financial” in the second paragraph, acknowledges that higher long-term interest rates “are likely to weigh on economic activity, hiring, and inflation.” Therefore, given the Fed’s rhetoric and the recent surge in long-term borrowing rates, it’s quite likely a long pause started in July, and the next Fed move will ultimately be a rate cut.

Chairman Powell elaborated on the Fed’s mindset in his press conference following the FOMC statement. He started by stressing the utmost importance of getting inflation back to its 2% objective and said he is encouraged that inflation expectations have remained stable. Of importance, Chairman Powell stated: “Financial conditions have tightened significantly in recent months due to longer-term rates.” Further, he says the stronger dollar and weaker equity prices will weigh on economic growth. As long as those conditions remain persistent, the Fed is unlikely to hike rates. Based on trading yesterday afternoon, the stock and bond markets seem to agree the Fed is likely done raising rates. Assuming economic activity does slow, the market will start anticipating rate cuts. Fed Fund futures for mid-2024 jumped by 10-12bps, implying bond traders think rate cuts are more likely than they did before Chairman Powell spoke.

What To Watch Today

Earnings

Economy

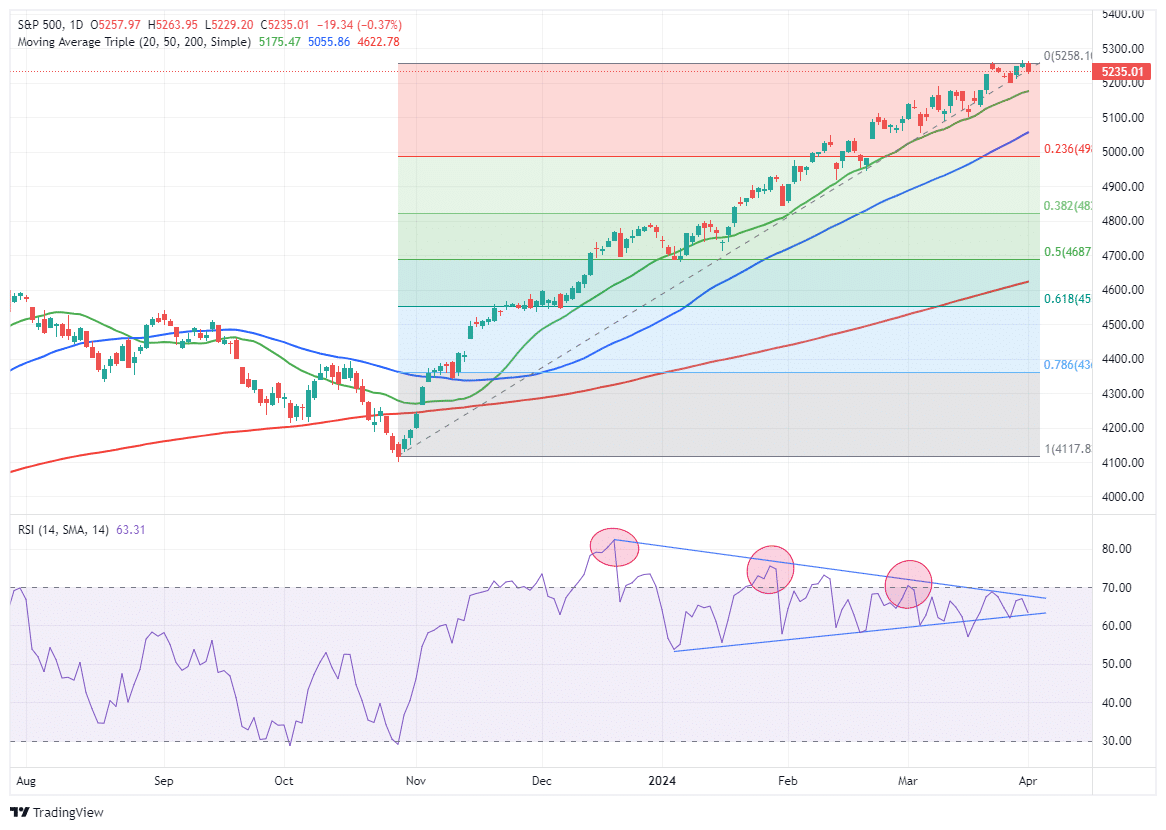

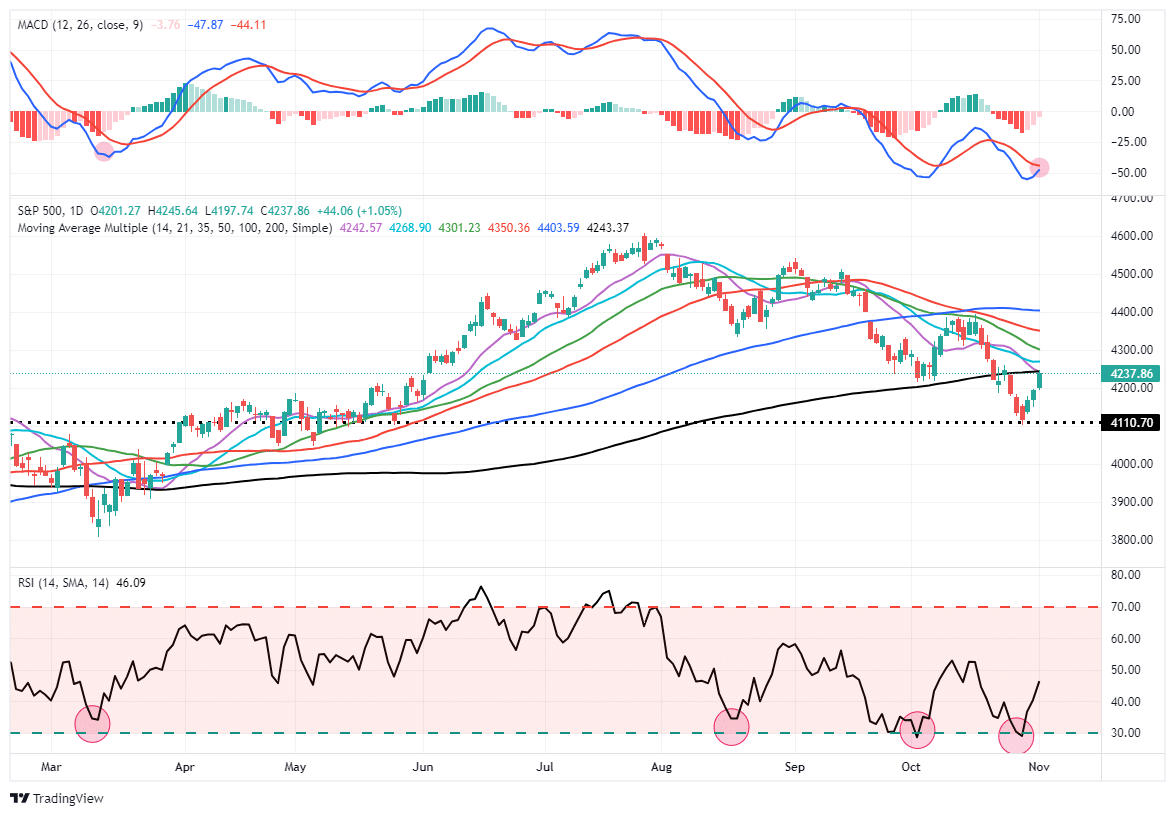

Market Trading Update

Yesterday, the FOMC was as expected, noting that there was one rate hike left on the table. However, the market saw through that and has now determined the Fed is on pause. As such, both the stock and bond markets rallied sharply yesterday as the market looks forward to next year and the beginning of rate cuts.

Yesterday’s rally pushed the market into its first resistance test at the 200-DMA. A failure at this initial test will be unsurprising as many trapped longs will be looking for an exit. The recent low is now critical support. We are also closing in on a reversal of the MACD sell signal, which would give the market a more optimistic outlook in the near term. With the market not overbought, there is more room for the market to push higher. However, I would not expect that push higher to be without a bit of volatility along the way. Look for pullbacks to add exposure if needed as we head into year-end. However, such will be a short-term trade, so look to take profits between 4200-4250.

ADP And JOLTS Jobs Market Update

The ADP jobs report underwhelmed for the second month in a row. ADP reported the private sector added 113k jobs in October, versus expectations for 155k. September job growth was 89k, which is in stark contrast to the 336k growth in jobs reported by the BLS. Typically, we would suspect some catch-down in this Friday’s BLS report. However, that may not occur, as the correlation between the two measures of job growth has been less dependable since the pandemic. The graph below compares the BLS and ADP jobs data. As it shows, they tend to correlate. But, the BLS has been running 150k more than ADP monthly since 2021. Such compares to slightly less than 100k before the pandemic.

The number of job openings was 9.55 million, slightly higher than expectations (9.42 million) and last month’s downwardly revised number (9.50 million). The quit rate was steady at 2.3% and back to the pre-pandemic highs. The second graph below shows the job quit rate tends to lead wages by about six months. Given the Fed follows wages closely as they tend to correlate with inflationary pressures, the recent quit rate should ease their inflation concerns.

Treasury Refunding Announcement

Every quarter, the U.S. Treasury announces its plans for debt issuance for the coming three months. These reports are often ignored by all except bond traders. However, given the impact higher yields are having on stock and bond returns, yesterday’s announcement was closely followed by many investors,

Per the U.S. Treasury’s quarterly refunding announcement:

The U.S. Department of the Treasury is offering $112 billion of Treasury securities to refund approximately $102.2 billion of privately-held Treasury notes maturing on November 15, 2023. This issuance will raise new cash from private investors of approximately $9.8 billion.

The market was expecting $114 billion, $2 billion more than the Treasury will auction. The table below shows the actual auction sizes for the three months ended October 2023 (highlighted gray) and the anticipated auction sizes for November 2023 through January 2024. The Treasury is favoring shorter-term debt as it likely wants to avoid locking in current yields for long periods. Consequently, less than 10% of the debt increase will come from the 10-30 year sectors. Long-term Treasury note and bond investors should like the Treasury’s stance.

ISM Manufacturing Survey

The ISM manufacturing survey remains in economic contractionary (<50) as it has for the last 12 months. The index was 46.7, decently below expectations of 49.1 and 49 in the prior survey. The graph below shows every factor except production fell, accounting for the 3.3 decline. Of the most interest of economic forecasters, new orders and employment came in at 45.5 and 46.8, respectively. Both figures signal manufacturing woes. As a result, the Tweet of the Day shares a recession warning from the ISM report.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.