Sam Goldfarb of the Wall Street Journal adds to the debate the bulls and bears are having about the recent rally. In The NASDAQ Composite is Back in a Bull Market, Goldfarb says: “The technology-focused index rose 2.9% Wednesday, reflecting a rise of more than 20% from its low in mid-June.” Further, “The recent rise in the NASDAQ ended its longest bear market since 2008 in the depths of the financial crisis.”

Mr. Goldfarb seems to have a poor sense of history about when bear markets end and bull markets begin. Michael Burry notes this in the tweet below. Burry’s claim to fame is the fortune he made betting against subprime in 2008 and his portrayal in The Big Short. As we share below, he points to the 2000-2002 NASDAQ bear market as evidence a 20% bullish rally can be meaningless. In that tech-driven bear market, the NASDAQ rose 20% or more on seven occasions. Ultimately each “bull market” was quickly erased, and the bear market ultimately dragged the NASDAQ lower by nearly 80%. The bulls today seem to be acting like the bears in June. Has sentiment changed enough to warrant caution that the rally is peaking?

What To Watch Today

Economy

- 8:30 a.m. ET: Import Price Index, month-over-month, July (-0.9% expected, 0.2% prior)

- 8:30 a.m. ET: Import Price Index excluding petroleum, month-over-month, July (-0.4% prior)

- 8:30 a.m. ET: Import Price Index, year-over-year, July (9.5% expected, 10.7%prior)

- 8:30 a.m. ET: Export Price Index, month-over-month, July (-1.0% expected, 0.7% prior)

- 8:30 a.m. ET: Export Price Index, year-over-year, March (18.2% prior)

- 10:00 a.m. ET: University of Michigan Consumer Sentiment, August preliminary (52.4 expected, 51.5 prior)

- 10:00 a.m. ET: U. of Mich. Current Conditions, August preliminary (57.5 expected, 58.1 prior)

- 10:00 a.m. ET: U. of Mich. Expectations, August preliminary (48.8 expected, 47.3 prior)

- 10:00 a.m. ET: U. of Mich. 1 Year Inflation, August preliminary (5.1% expected, 5.2% prior)

- 10:00 a.m. ET: U. of Mich. 5-10 year Inflation, August preliminary (2.8% expected, 2.8% prior)

Earnings

Market Trading Update

The market opened up fairly strongly yesterday morning as money chased the “inflation is subsiding rally.” However, as the day went on, profit taking took over as the market is now very extended and overbought. The market needs a correction to add exposure to portfolios, and the 100-dma will be the first important test of support. The 50-dma is also a viable retest level which would likely work off most of the short-term overbought condition. If either support levels hold and consolidation removes the overbought condition, then a rally to the 200-dma is likely. A failure at the 50-dma remains our “line in the sand” for a re-engagement of the bear market trend.

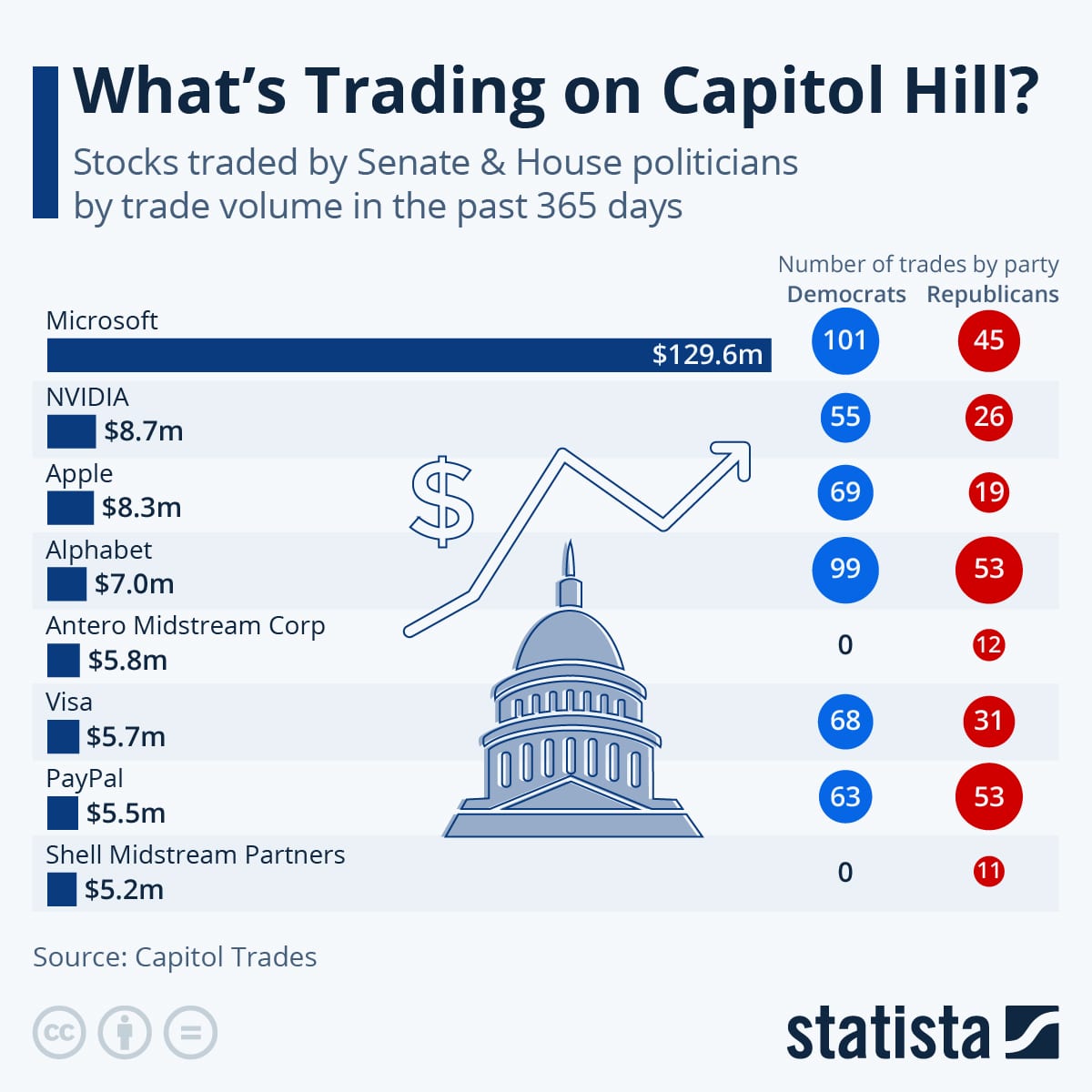

Want To Trade Like An Insider? Buy What Congress Is Buying.

“Politicians using their knowledge of upcoming bills in conjunction with stock trading activities could, in theory, constitute insider trading. Discussing its perceived legality or illegality has long been a staple of the stock market. Still, the practice flies under the radar in day-to-day trading activities. While the so-called STOCK Act which prohibits trading commodities based on nonpublic information was signed into law in 2012, the fines tied to a violation are often minuscule. This could change soon though: Business Insider and other media outlets have identified 67 politicians not complying with the law in a recent report, and Congress is open to debating measures that would ban all federal lawmakers from trading stocks.” – Statista

What’s Hot and What’s Not

The graph below shows the Relative Strength Index (RSI) broken out by industry and major indexes. The most overbought sectors are those that were lagging before the recent bounce. Conversely, the “least hot” sectors exhibited the most strength when the market fell. If this bullish run continues, expect overbought sectors to continue to outperform the broader market. The opposite holds if the bears take the wheel from the bulls.

PPI Confirms CPI

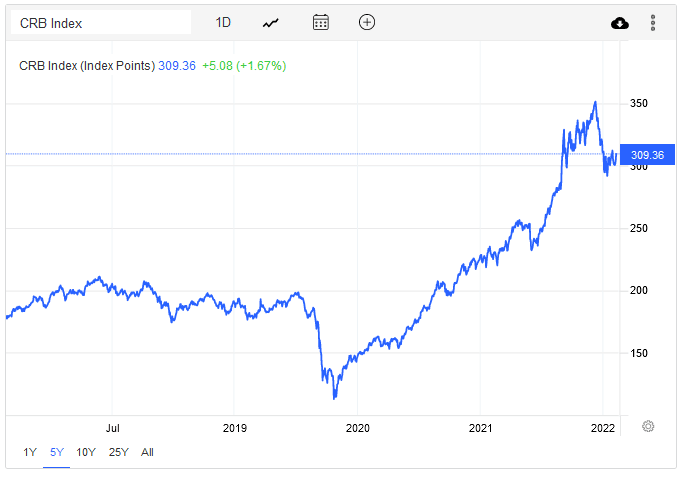

July PPI fell by .5%, bringing down the year-over-year rate to 9.8%. The core rate rose .2%, which was below expectations of a .4% increase. The data suggest that supply line problems continue to ease. Further, the report is good news for manufacturers as their input costs are falling quicker than CPI inflation. The information is promising but not surprising. As we have noted over the last few weeks, many commodities prices have fallen sharply over the previous few months. The graph below shows the recent decline in the CRB commodity price index. As we have discussed, the trend is favorable, but we are not close to being out of the woods as the index is still way above pre-pandemic levels and appears to be stalling.

Curb Your CPI Enthusiasm

John Authers of Bloomberg wrote a great piece yesterday about Wednesday’s CPI data. While he notes the recent round of inflation data is positive, and inflation may have peaked, we remain unsure how quickly inflation will fall. Per the article:

However, even if the peak has been scaled, the issue of the descent now confronts us. And it will be difficult. Although undeniably positive, this consumer price index report is not a big game-changer, and it’s unlikely to have much impact on how the Federal Reserve behaves for the rest of the year.

His concern that inflation does not fall quickly is based on transitory prices versus core prices. Transitory price surges and recent declines in some goods were due to the Pandemic. For example, the prices of used cars, rental cars, and energy are now lower than the grossly elevated prices of a year ago. While the prices are still historically high, they reduce the overall CPI inflation rate. The Fed has been vocal they don’t pay much attention to the prices of goods greatly affected by the pandemic. They are more concerned with the other, less extreme volatility goods and services.

The problem is that most of those extreme price moves were essentially supply line based and had less to do with demand. As such, monetary policy had little ability to affect their prices. That isn’t true of most other products. The Fed closely follows “core” inflation to look at underlying price pressures, which are still rising. These less volatile prices make the Fed less confident that inflation will retreat as quickly as it came.

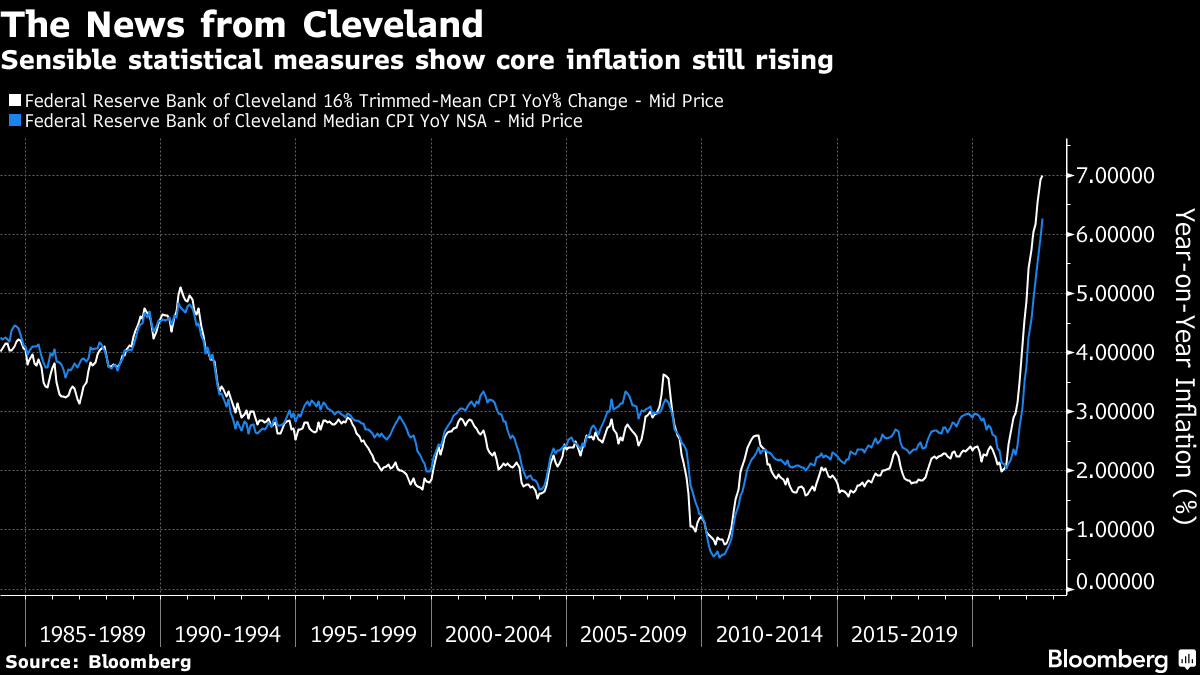

Two widely followed measures come from the Cleveland Fed, which publishes a trimmed mean (excluding the biggest outliers in either direction and taking the average) and the median. These measures were never moved by rental cars or gasoline in the first place. And unfortunately, both continued to rise, and both are at their highest since the series started in 1984.

He warns that it is too early to be overly optimistic that inflation will fall rapidly. Further, he cautions against betting on a pivot.

Put all this together, and Jerome Powell would probably like the markets to be helping a bit more by making financing a little more expensive. So there’s no case for a dovish pivot as yet, and a pretty good argument to show the markets who’s boss with a 75-basis-points hike next month.

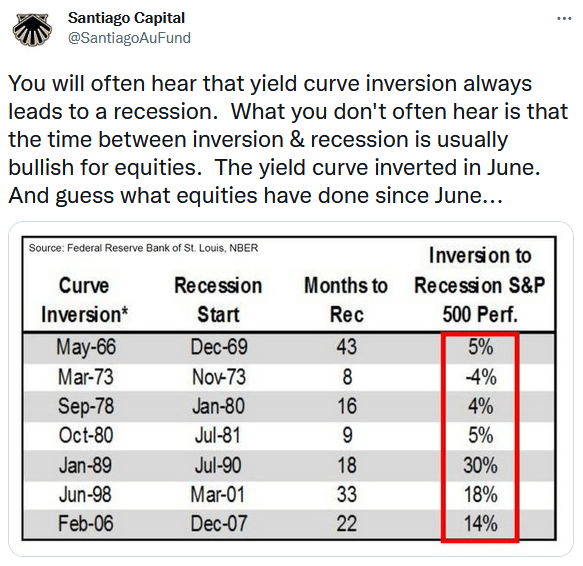

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.