Equity futures are trading flat this morning after giving up half a percent yesterday. The dollar is slightly higher overnight after its strong performance yesterday. At 2 pm ET, the Fed will release its minutes from the July FOMC meeting. Investors will be looking for indications of the Fed’s willingness to begin tapering QE.

Chairman Powell, speaking to educators, had little to say about the future path of monetary policy. It looks like we will have to wait for next week’s Jackson Hole conference to see if he agrees with many Fed members that taper is in the cards for this fall. The following headline is the only clue he left us:

- THE FED IS IN THE PROCESS OF PUTTING AWAY ALL OF ITS TOOLS THAT WERE BUILT FOR TRUE CRISES.

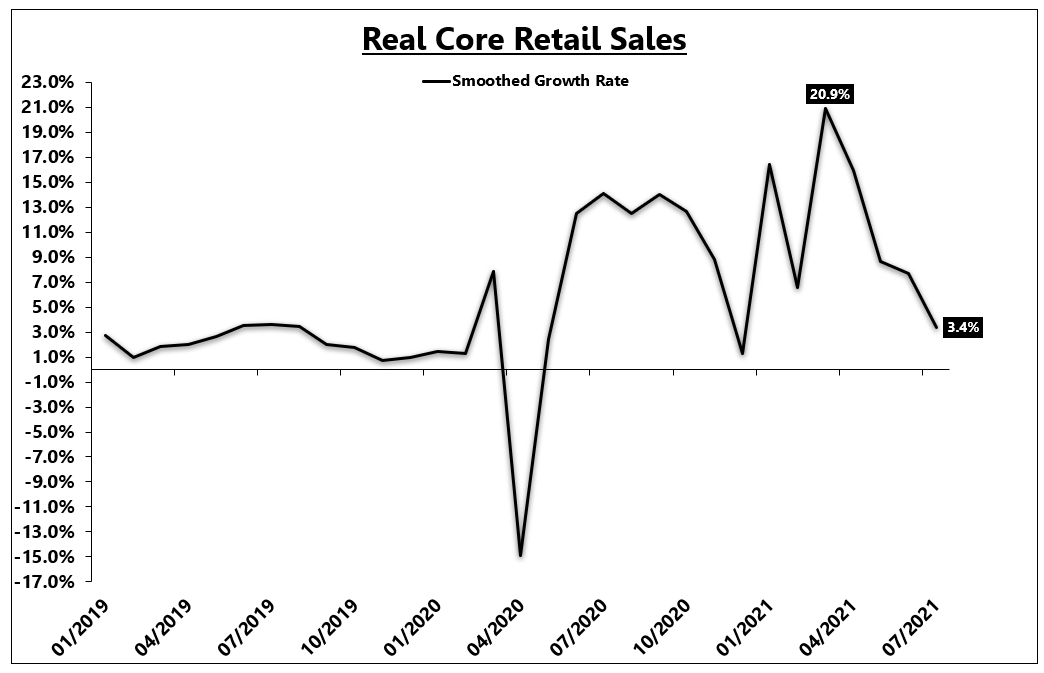

Retail Sales can be a misleading data point as it doesn’t account for inflation. For instance, if inflation was 5% and retail sales grew by 5%, 100% of the growth in retail sales is due to price increases, not more consumption of goods. The graph below takes the inflation component of sales to give us a clearer reading of true sales. Core retail sales exclude vehicle and vehicle parts, gas stations, and building materials. At a 3.4% annualized growth rate, real core retails sales are back to near pre-pandemic levels.

July Retail Sales came in at -1.1%, versus expectations of -0.2% and +0.7% last month. Excluding autos and gas retails sales fell by 0.7% versus expectations of a 0.3% decline. The weaker than expected data should not be a total surprise as BofA and JPM credit card spending tracking data has shown a decent drop-off in credit card usage.

Risky Business

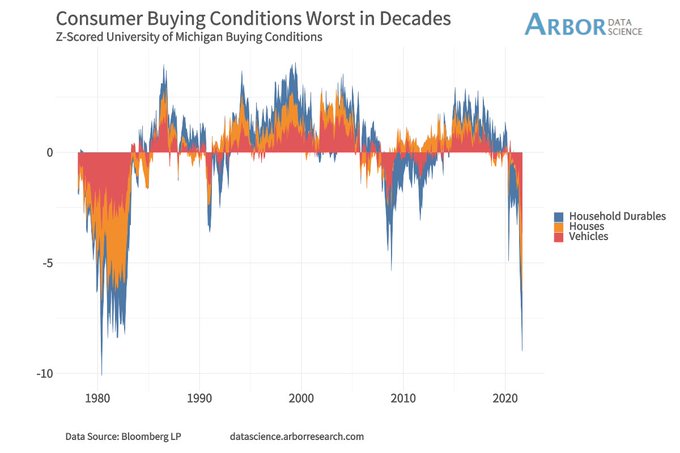

Per Arbor Research, the University of Michigan’s Consumer Survey reported that buying conditions for durable goods, homes, and vehicles are at the lowest levels since 1980.

Economic data from China continues to come in weaker than expectations. China is the world’s second-largest economy and has been an important driver of global economic growth. While many developed economies continue to post outsized growth, China is flashing warning signals. This past weekend China reported the following:

Industrial Production 6.4% versus expectations of 7.8% and prior month 8.3%

Chinese Retail Sales 8.5% versus expectations of 11.5% and prior month 12.1%

Chinese Fixed Assets Investment excluding rural 10.3% versus Expectations of 11.3% and prior month 12.6%

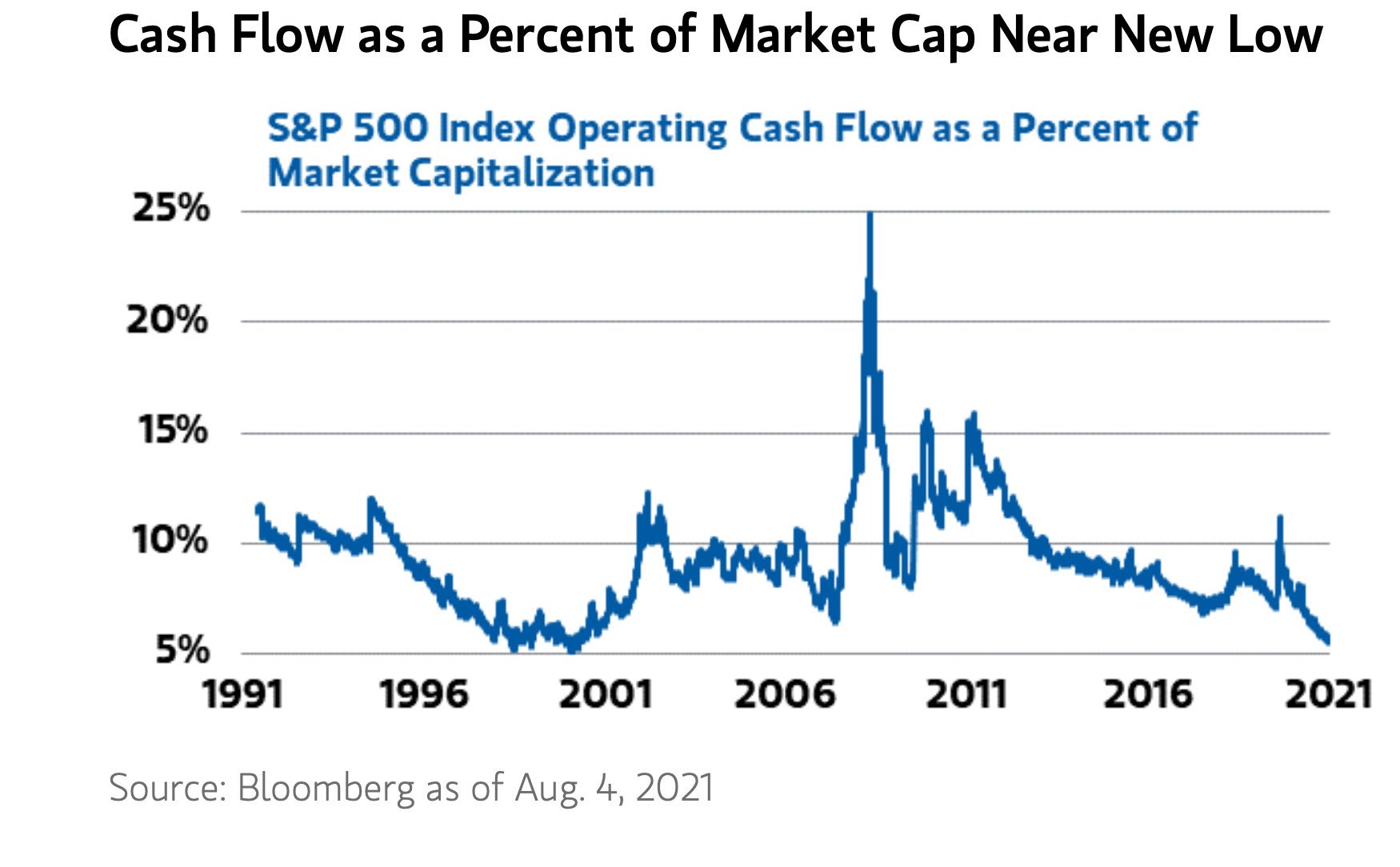

The graph below serves as another reminder that valuations are at extreme levels. However, despite the graph below and many other valuation techniques at or near records, the market can get more expensive. Pay close attention to technical indicators to help navigate the current environment.