Housing comprises almost 40% of CPI, of which rents account for about three-quarters of that amount. Therefore, to help forecast CPI and, notably, consider what the Fed may or may not do, let’s closely examine rent costs, particularly apartment rents. To do so, the graph below shows that owners’ equivalent rent (OER), mainly comprised of apartment and house rental prices, has risen. At first glance, the chart does not portend that inflation will fall immediately. However, OER lags months behind what is happening on the ground.

To further help, we share a WSJ to assess how apartment rents and OER might impact CPI. In Apartment Rents Fall as Crush of New Supply Hits Market, the author states: “Apartment rents fell in every major metropolitan area in the U.S. over the past six months through January, a trend that is poised to continue as the biggest delivery of new apartments in nearly four decades is slated for this year.” The article notes that nearly 500,000 units will hit the market this year, the most in 35 years. It also states many tenants are maxing out the rent they can afford.

OER will fall in the coming months. As we share below, the OER price index (blue) is over 10% above its 35-year trend line. Therefore we believe the recent increase is an anomaly that will correct as the supply-demand equation normalizes quickly this year.

What To Watch Today

Economy

- Advance Goods Trade Balance, January (-$91.0 billion expected, -$90.3 billion prior)

- Wholesale Inventories, month-over-month, January Preliminary (0.1% expected, 0.1% prior)

- Retail Inventories, month-over-month, January (0.5% prior)

- House Price Purchase Index, quarter-over-quarter, Q4 (0.1% prior)

- FHFA Housing Pricing Index, December (-0.1% prior)

- S&P CoreLogic Case-Shiller 20-City Composite, month-over-month, December (-0.54% prior)

- S&P CoreLogic Case-Shiller 20-City Composite, year-over-year, December (6.77% prior)

- S&P CoreLogic Case-Shiller U.S. National Home Price Index, year-over-year, December (7.69% prior)

- MNI Chicago PMI, February (44.3 prior)

- Richmond Fed Manufacturing Index, February (-11 prior)

- Conference Board Consumer Confidence, February (108.5 expected, 107.1 prior)

- Richmond Fed Business Conditions, February (-10 prior)

- Dallas Fed Services Activity, February (-15.0 prior)

Earnings

Market Trading Update

As noted yesterday, we were expecting a rally this week following last week’s selloff. The rally yesterday was disappointing, but the market did hold support at the 50-DMA and the rising trend line from the October lows. As long as that support holds, the bulls retain control. We are working through the current sell signal that started on February 10th. These signals tend to last 4-8 weeks before they complete, so we have some more work to do short-term.

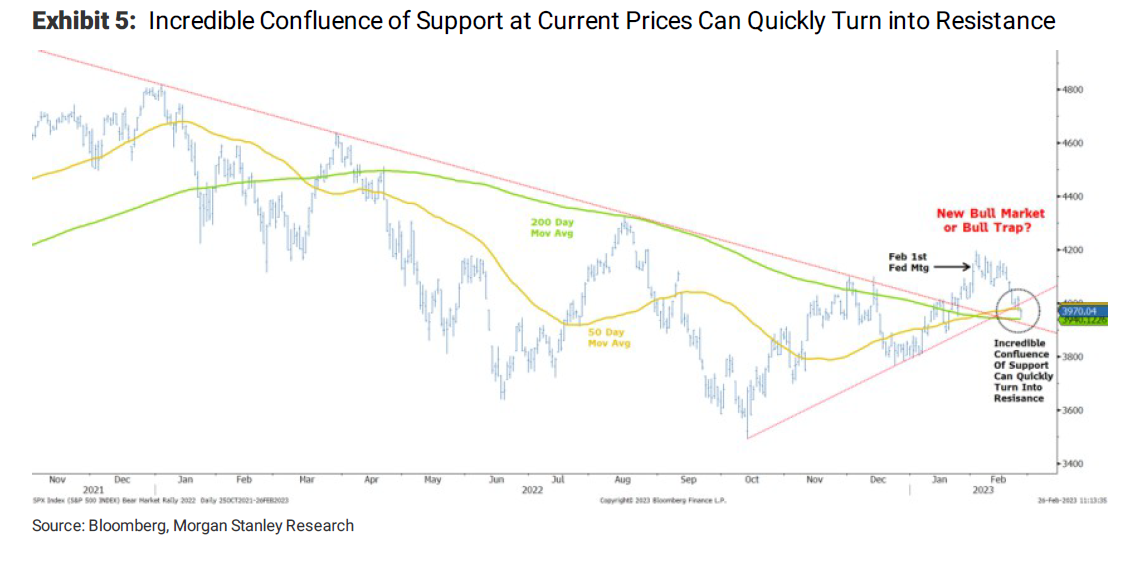

Morgan Stanley had a interesting take as well.

“The S&P 500 has recently been trying to break the well established downtrend that defines this bear market that we think remains incomplete. The question for investors is whether this signifies a new bull market that began in October or a classic Bull Trap? Without any fundamental view, most technicians would likely take the more positive outcome: i.e., new uptrend being established. However, we do have a strong fundamental view; therefore, we are inclined to conclude this as a bull trap.

In addition to earnings risk, we also have extreme valuation risk (Equity Risk Premium still at a historically low 168bps after last week’s sell-off), and we could argue positioning and sentiment is neutral at best and even bullish on several measures. We would also point out that much of the rally since October has been driven by non-fundamental flows (trend following strategies) that have been flattered by extraordinary global liquidity that may not continue to be supportive. In other words, in our view, this support looks rather weak and can quickly turn into resistance if the S&P 500 drops a modest 1 percent further.“

Continue to use rallies to reduce risk and raise some cash. We are starting to buy longer-duration bonds in small amounts as yields approach what we expect will be the Fed’s terminal rate.

Jim Colquitt Chart Review

Jim Colquitt, Founder and President of Armor Index ETFs, is now regularly publishing on Real Investment Advice. For more information, check out his debut article, Do Not Be Fooled. Jim also publishes a weekly chart book. Therefore, we chose a few excerpts below to introduce you to Jim better.

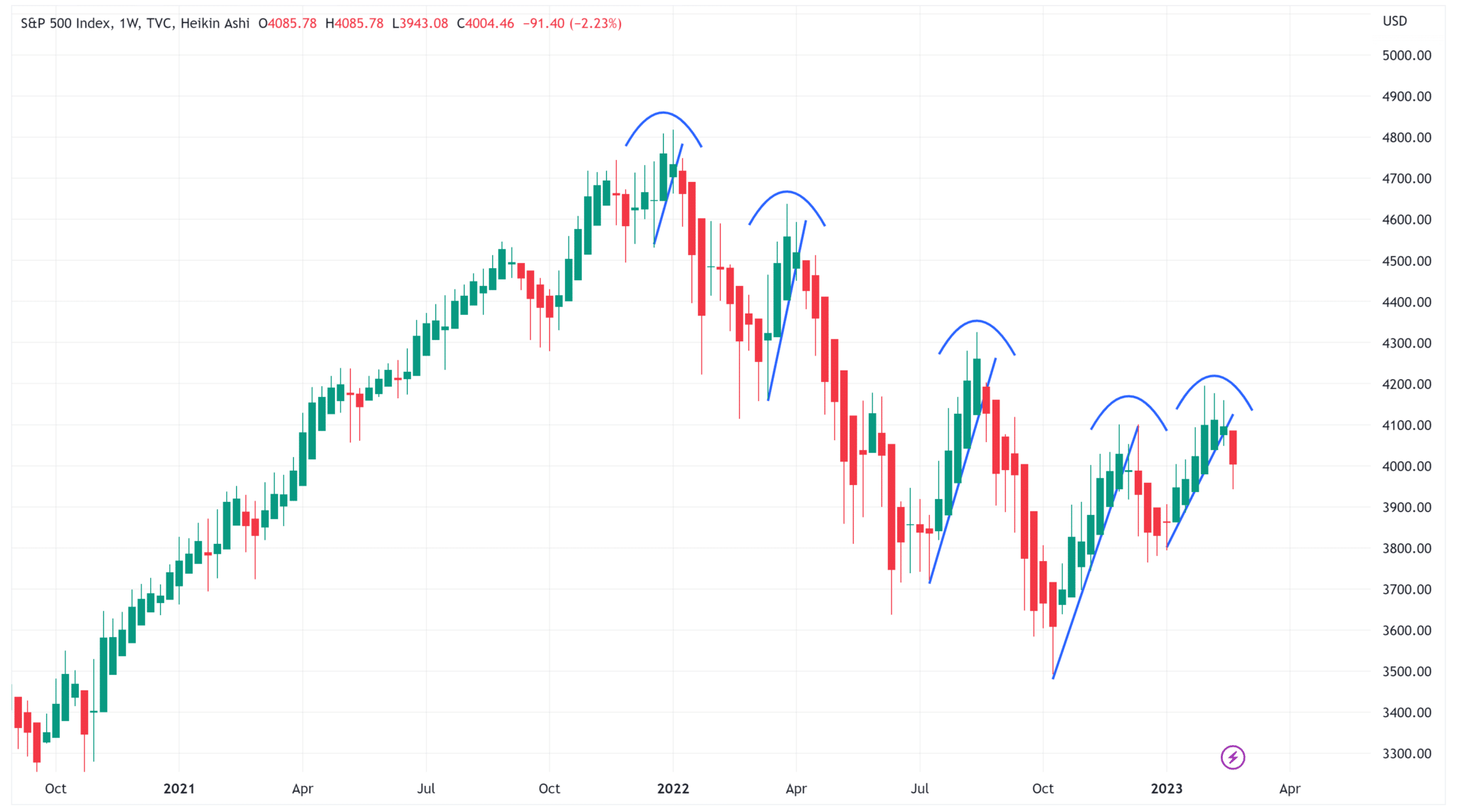

In the first chart, we’re looking at the S&P 500 Index. If you’re a bull, you have to be hoping (praying) that last week’s price action was simply a retest of the prolonged downtrend line and that it will bounce from here.

It looks more likely that this is a very similar pattern that we’ve seen repeat itself repeatedly since the beginning of 2022. One where we see a sustained rally for several weeks only to have it break down and move appreciably lower.

You can see this in the chart below, denoted by the blue trendlines. Note that each of these moves was foreshadowed by a rounding top.

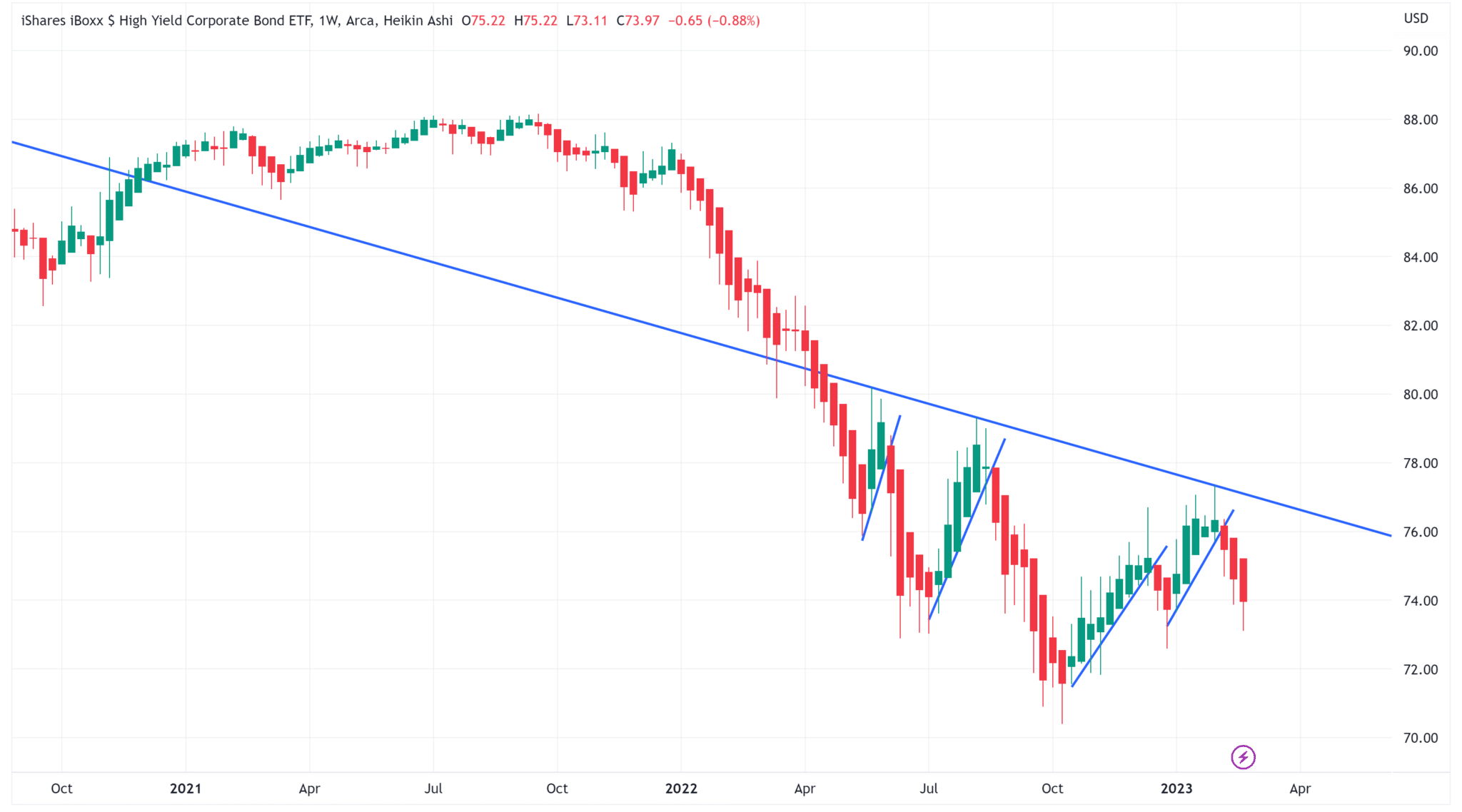

Having spent a fair amount of time in the high-yield bond market, I tend to believe that high-yield bonds lead equities. With that said, note what HYG is showing us. Similar pattern as above except that HYG is on week three of the downtrend.

Inflation Expectations

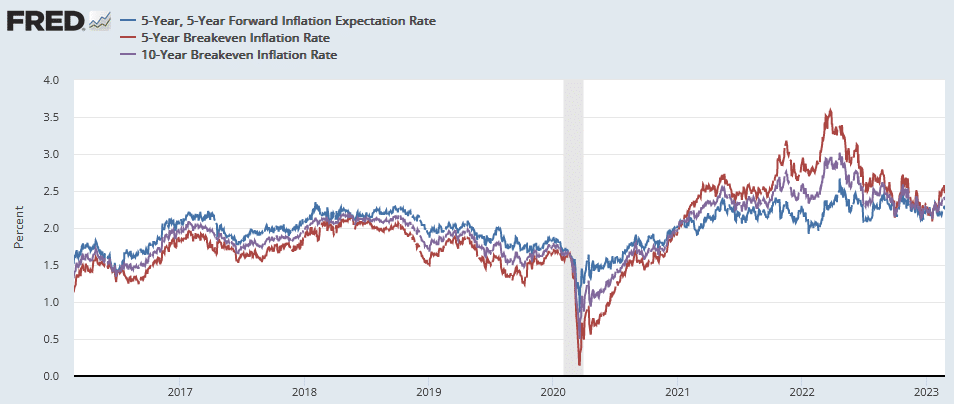

On the heels of last week’s higher-than-expected PCE inflation data and CPI and PPI from the prior week, it’s worth revisiting how inflation expectations are affected. The first graph shows inflation expectations for the next five years (red), ten years (purple), and for the five years starting five years from now (blue). They have all upticked but not in a concerning manner. Further, they have fallen decently over the last year but remain about half a percent of the pre-pandemic range.

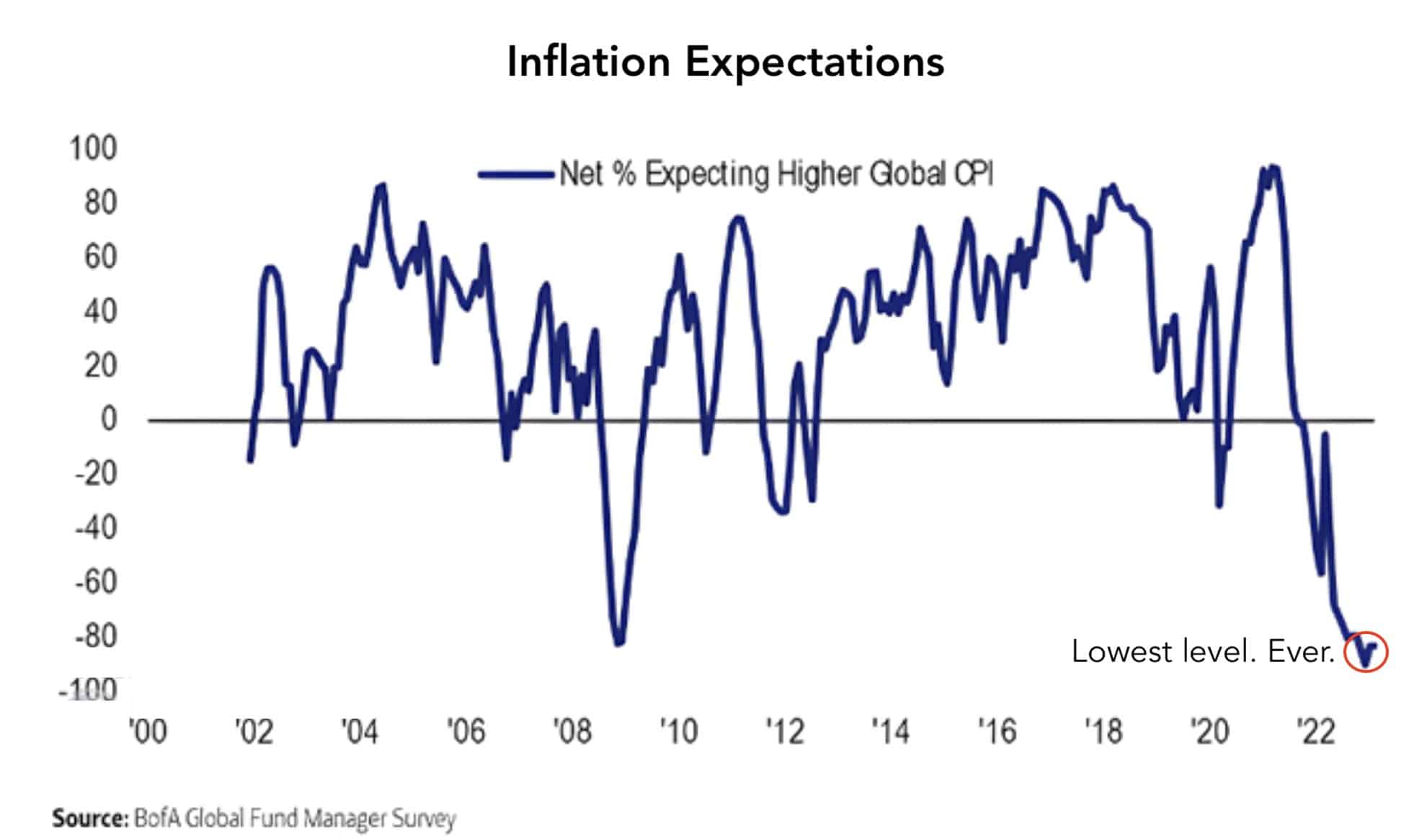

The second graph is a bit different. The BofA graph shows the percentage of investment managers surveyed who think global inflation will be lower in the year ahead. As shown in the graph, it is now at a record low.

Martin Zweig’s Trading Rules

Martin Zweig, a successful, highly regarded stock investor and author, published his 17 investing rules in 1990. His guidance is still highly valid and worth reminding ourselves of.

- The trend is your friend.

- Let profits run, take losses quickly.

- If you buy for a reason and that reason is discounted or no longer valid, then sell!!

- If the values don’t make sense, then don’t participate.

- The cheap get cheaper, the dear get dearer.

- Don’t fight the FED.

- Every indicator eventually bites the dust.

- Adapt to change.

- Don’t let your opinion of what should happen bias your trading strategy.

- Don’t blame your mistakes on the market.

- Don’t play all the time.

- The market is not efficient but is still tough to beat.

- You’ll never know all the answers.

- If you can’t sleep at night, reduce your positions or get out.

- Don’t put too much faith in the “experts.”

- Don’t focus too much on short-term information flows.

- Beware “New Era” thinking, i.e. “This time is different.”

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.